Free 4490 PDF Template

Free 4490 PDF Template

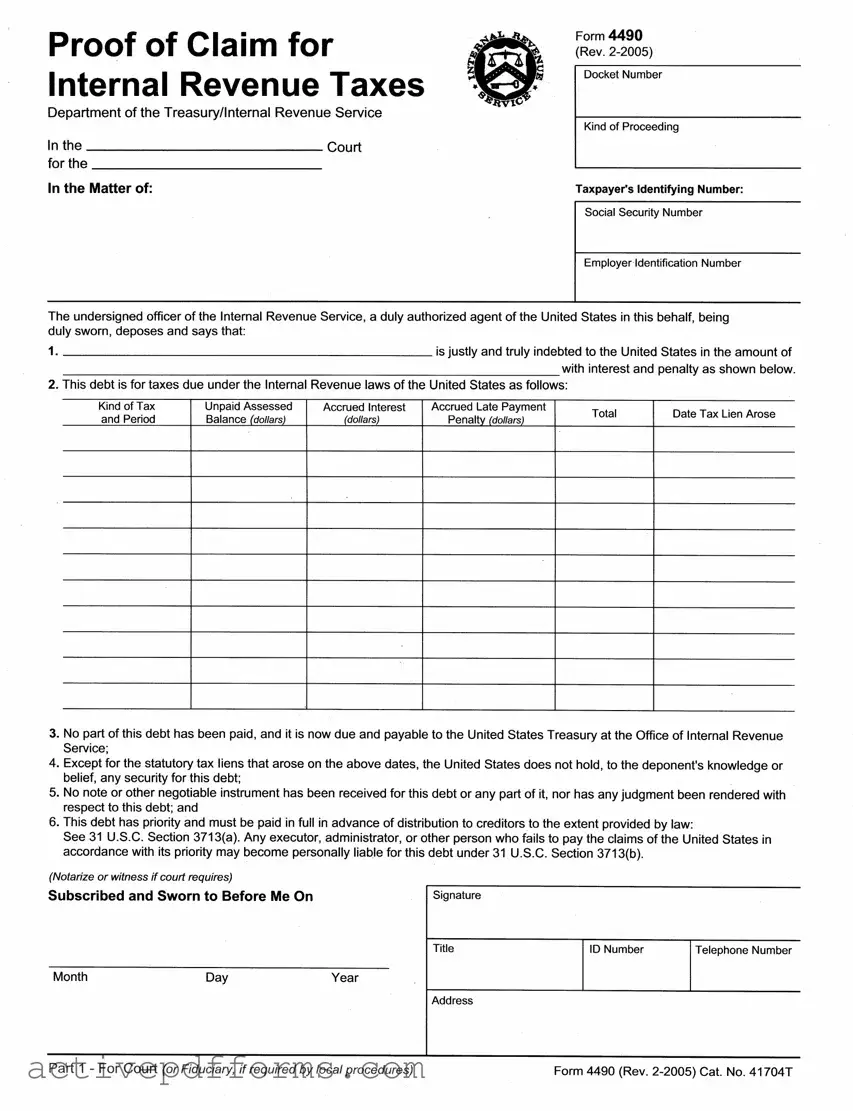

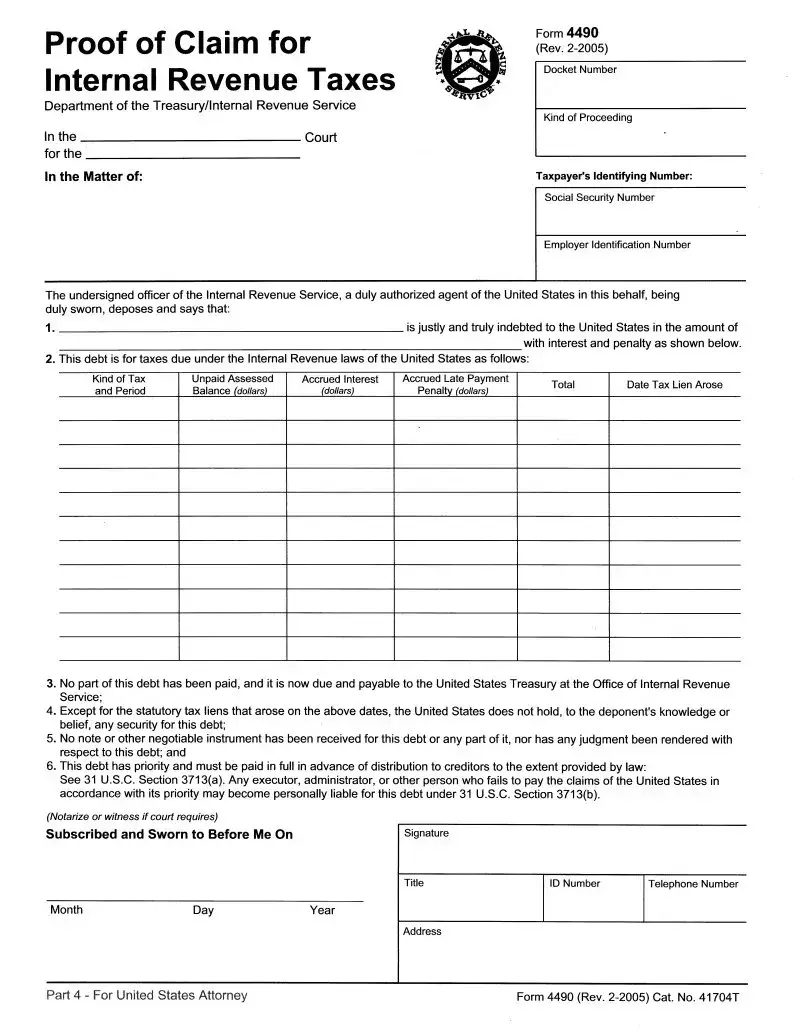

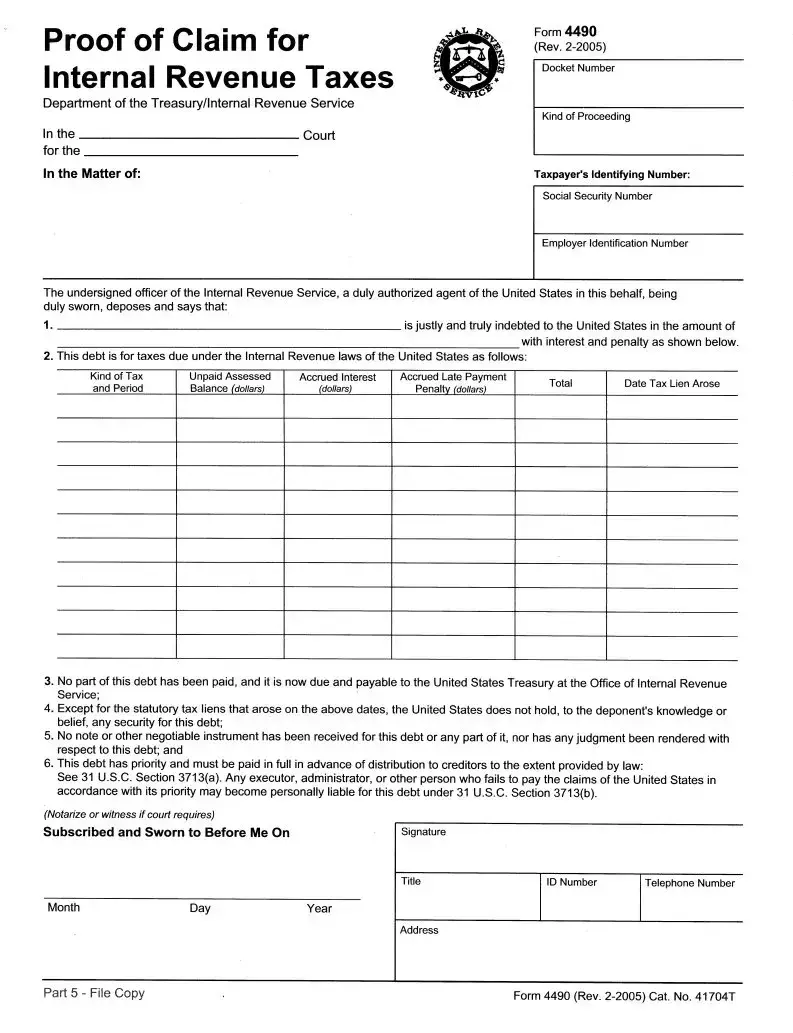

The Form 4490, issued by the Department of the Treasury/Internal Revenue Service, serves as a crucial document in legal proceedings regarding unpaid internal revenue taxes. This form, revised in February 2005, is used to assert the United States government's claim for unpaid taxes, including penalties and accrued interest, against an individual or entity. Presented under oath by an authorized IRS officer, it details the amount owed to the United States, categorizes the type of tax in arrears, and outlines the accrued interest and penalties. Furthermore, the form certifies that no payment has been received towards settling the debt, which remains due and payable at the Office of the Internal Revenue Service. Notably, it emphasizes the legal precedence of this debt over other creditor claims, under 31 U.S.C. Section 3713(a), and flags the potential personal liability for executors, administrators, or others who fail to honor this priority, as specified in 31 U.S.C. Section 3713(b). The form requires notarization or witnessing depending on court requirements and includes sections for court processing, acknowledgment by IRS officials, fiduciary handling, and for use by the United States Attorney, each tailored to streamline the claim verification and processing workflow.

| Fact | Detail |

|---|---|

| Form Number and Revision | Form 4490 (Rev. 2-2005) |

| Title | Proof of Claim for Internal Revenue Taxes |

| Issuing Authority | Department of the Treasury/Internal Revenue Service |

| Purpose | To declare a taxpayer's debt to the United States for unpaid taxes, including interest and penalties. |

| Legal Basis | 31 U.S.C. Section 3713(a) for priority of claims and 31 U.S.C. Section 3713(b) regarding personal liability for failure to pay. |

| Contents | Information about the taxpayer, type and amount of tax debt, accrued interest, late payment penalties, and statutory tax liens. |

| Use in Proceedings | Filed with the court or relevant fiduciary authority in cases involving the disposition of assets to assert the priority of the United States government's claim for unpaid taxes. |

Completing Form 4490 requires careful attention to detail and accuracy to ensure the claim for Internal Revenue taxes is properly documented. This form is used in the context of court proceedings where a claim is made for unpaid taxes, including penalties and interest. Each section of the form should be filled out based on the specific information related to the tax debtor's case. The steps below guide you through filling out Form 4490, starting from identifying information to detailing the tax debt and concluding with legal acknowledgment.

Remember, the 4490 form is a legal document and must be filled out with the utmost accuracy and completeness. Failing to accurately represent the tax debt information may result in legal consequences. Once the form is completed, follow the instructions regarding submission carefully, making sure it reaches the correct department or office for processing.

What is Form 4490?

Form 4490, titled "Proof of Claim for Internal Revenue Taxes," is a document issued by the Department of the Treasury/Internal Revenue Service. It is used by an officer of the IRS, as an authorized agent of the United States, to declare that an individual or entity owes a debt to the United States for unpaid taxes. This form outlines the amount owed, including taxes, interest, and penalties, and asserts the government's priority to claim the debt.

Who needs to complete Form 4490?

This form is completed by a duly authorized IRS officer. It is not a form that the taxpayer or debtor completes but rather a formal claim filed in legal proceedings, such as bankruptcy cases, where a taxpayer has outstanding tax debts. The form serves as official notification of the debt owed to the United States government.

What information is required on Form 4490?

The form requires detailed information about the tax debt, including:

The form must be notarized or witnessed if required by court proceedings.

What implications does Form 4490 have on bankruptcy proceedings?

In bankruptcy proceedings, Form 4490 asserts the government's claim to unpaid taxes as a creditor. The form lays out the IRS's claim to any assets for tax debts owed by the individual or entity declaring bankruptcy. As tax debts have priority according to the law, this form signals to the bankruptcy court that these debts must be paid before other creditors' claims. Not addressing this claim can result in personal liability for executors, administrators, or other individuals involved under 31 U.S.C. Section 3713(b).

Can a taxpayer dispute the claim made on Form 4490?

Yes, a taxpayer can dispute the claim. If a taxpayer believes that the claim filed by the IRS on Form 4490 is incorrect, they should contact the IRS directly to discuss the matter. It may also be beneficial to seek legal advice from a tax attorney who can provide guidance on how to proceed with disputing the claim in court or with the IRS.

What should one do after receiving a copy of Form 4490?

Upon receiving Form 4490, it is important to review the claim's details carefully. If the debt is valid, arrangements should be made to address the outstanding tax liability. This may involve consulting with a tax advisor or attorney to discuss available options, such as setting up a payment plan with the IRS. If the claim is disputed, immediate action should be taken to resolve the discrepancies with the IRS. Ignoring the claim can result in further legal action and financial penalties.

Filling out Form 4490, the document for claiming internal revenue taxes, requires careful attention to detail. Mistakes can lead to delays or even legal complications. Here are five common mistakes people often make:

Understanding and avoiding these mistakes can significantly streamline the process of filing Form 4490. Properly completed, this form ensures that obligations to the United States Treasury are clearly communicated and efficiently processed.

When handling the complexities of tax-related matters, especially those requiring the submission of Form 4490 (Proof of Claim for Internal Revenue Taxes), it's crucial to familiarize oneself with other pertinent documents often required by the Internal Revenue Service (IRS) and the courts. These forms and documents ensure compliance and accuracy in reporting, representing vital components in the resolution of tax obligations and disputes.

Each of these documents plays a significant role in managing and resolving tax matters efficiently. Whether addressing individual income, business operations, or estate planning, comprehending these forms and documents allows for better preparation and submission in conjunction with Form 4490. Legal and financial professionals, as well as individuals dealing directly with these issues, should ensure they have accurate and complete documentation to present a clear and comprehensive case to the IRS or the court.

Form 1040 (U.S. Individual Income Tax Return): Similar to the 4490 in that it's also a key IRS document used for tax purposes. However, while Form 1040 is used by individuals to file their annual income taxes, Form 4490 is used specifically for claiming taxes due from an estate or insolvency proceedings.

Form 706 (United States Estate (and Generation-Skipping Transfer) Tax Return): This form shares similarities with Form 4490 as both deal with taxes related to an estate. Form 706 is filed by the executor of a decedent's estate to calculate estate tax owed, whereas Form 4490 is a proof of claim for taxes owed by the estate to the IRS.

Form 941 (Employer's Quarterly Federal Tax Return): Both Form 941 and Form 4490 are used by entities to report taxes. Form 941 is specifically for employers to report payroll taxes quarterly, while Form 4490 is used within court proceedings to claim taxes owed.

Form 940 (Employer's Annual Federal Unemployment (FUTA) Tax Return): Similar to Form 4490, Form 940 is used for tax reporting. However, Form 940 focuses on unemployment taxes paid by employers at the end of each year, contrasting with Form 4490's role in claiming taxes due from estates or bankrupt entities in legal proceedings.

Form 8821 (Tax Information Authorization): While not a tax return, Form 8821 authorizes individuals or organizations to request or inspect confidential tax information, somewhat similar to Form 4490 which involves the IRS making a formal claim in court regarding tax liabilities. Both forms exemplify instances where tax information interaction is necessary beyond the straightforward filing of returns.

When filling out Form 4490 - Proof of Claim for Internal Revenue Taxes, individuals are urged to pay meticulous attention to detail and follow specific procedures to ensure accurate and prompt processing. Below are several recommended dos and don'ts to guide you through the completion of this form:

Understanding the Form 4490 can often be complex, with various misconceptions surrounding it. Here are ten common misunderstandings and the actual facts:

This is incorrect. Form 4490, "Proof of Claim for Internal Revenue Taxes," is a document used by the IRS to submit a claim in a bankruptcy proceeding, not a tax return.

Actually, this form is filed by an authorized IRS officer, not by taxpayers or businesses themselves.

This form is not a means to dispute tax obligations. It's a formal claim by the IRS for taxes owed by a debtor in bankruptcy.

Filing this form is part of bankruptcy proceedings and does not halt other IRS collection actions outside of those proceedings.

There is no filing fee associated with Form 4490, as it is a claim form used by the IRS in bankruptcy cases.

This form is specifically for submitting a claim for unpaid taxes owed to the United States government. The necessity of filing it depends on the particulars of the bankruptcy case and tax debt.

Incorrect. Form 4490 is signed by an authorized IRS officer, not the taxpayer.

While the form does claim priority according to law, the actual prioritization of the claim within the bankruptcy proceedings is determined by the court.

There are specific deadlines and procedures within bankruptcy proceedings for filing claims like those made on Form 4490, and it’s not always at any time.

Filing this form does not absolve an executor, administrator, or other responsible person of personal liability for the debt if they fail to comply with priority payment requirements.

It's crucial to recognize and understand these misconceptions to better grasp the intricacies of bankruptcy proceedings and how tax debts are treated within them. The Form 4490 plays a vital role in this process, representing the U.S. government's claim to unpaid taxes.

The Form 4490, titled "Proof of Claim for Internal Revenue Taxes," plays a crucial role in the legal process concerning tax debts to the United States. It is used by the Internal Revenue Service to assert claims in various legal proceedings. Here are eight key takeaways regarding its completion and use:

Understanding these key points can aid individuals and legal professionals in navigating situations where the Form 4490 is used, ensuring proper attention to tax obligations in legal proceedings.

IRS E-file Signature Authorization - It is a critical component of the e-file process, ensuring that tax returns are submitted securely and efficiently.

Florida Lottery Claim - Its comprehensive coverage of the claim process, from identification to tax considerations, aids claimants in navigating the complexities of claiming lottery winnings with ease.