Free Cg 20 10 07 04 Liability Endorsement PDF Template

Free Cg 20 10 07 04 Liability Endorsement PDF Template

The CG 20 10 07 04 Liability Endorsement form plays a crucial role in defining the scope of coverage under the Commercial General Liability policy, significantly impacting both policyholders and additional insureds, such as owners, lessees, or contractors. This endorsement modifies the existing insurance coverage, carefully specifying who qualifies as an additional insured and under what circumstances. The form delineates that additional insureds are covered for liability arising from bodily injury, property damage, or personal and advertising injury caused by the policyholder's actions or those acting on their behalf. However, it also sets boundaries on this coverage, noting that it applies only to the extent permitted by law and is not broader than required by any contract or agreement necessitating such coverage. Additional exclusions and limitations are outlined, such as the exclusion of coverage for injuries or damages occurring after the completion of work or after the covered operations have been put to their intended use, except by certain parties. Moreover, it caps the amount payable to additional insureds to either the amount required by contract or agreement or the available limits of insurance, whichever is less, ensuring that this endorsement does not extend the policy's overall limits of insurance. This careful balance aims to protect all parties involved, providing vital liability coverage while managing expectations and legal requirements.

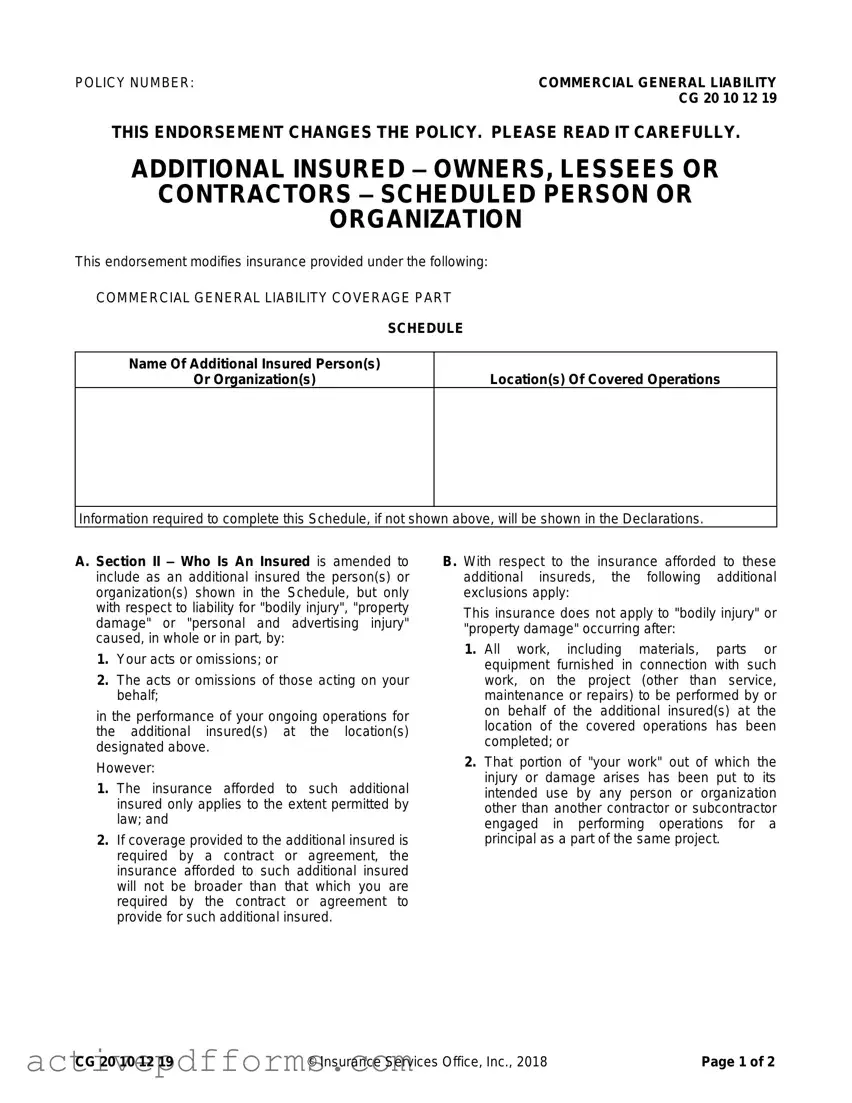

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

| Fact Number | Fact Detail |

|---|---|

| 1 | The form is identified as CG 20 10 12 19. |

| 2 | This endorsement modifies the Commercial General Liability Coverage Part. |

| 3 | It provides additional insured status to persons or organizations specified in the Schedule. |

| 4 | Coverage extends to liability for "bodily injury", "property damage", or "personal and advertising injury" caused in part or in whole by the named insured's acts or omissions, or those acting on their behalf. |

| 5 | The insurance for additional insureds applies only to the extent permitted by law and is not broader than required by a contract or agreement. |

| 6 | Additional exclusions apply to the insurance afforded to these additional insureds concerning injuries or damages occurring after the completion of the work or after the work has been put to its intended use by someone other than another contractor or subcontractor on the same project. |

| 7 | Should coverage be mandated by a contract or agreement, the maximum payable amount on behalf of the additional insured is the lesser of the required amount by the contract or the available limits of insurance. |

| 8 | The endorsement does not increase the limits of insurance. |

Filling out the CG 20 10 07 04 Liability Endorsement form is a crucial step in modifying your commercial general liability policy to include additional insured persons or organizations. This process involves providing specific details about who is to be added as an additional insured and under what circumstances. The steps below guide you through completing this form accurately to ensure your policy reflects your specific needs and obligations.

After submitting the CG 20 10 07 04 Liability Endorsement form, your insurance provider will review the documentation. You should receive a confirmation or a request for additional information. Ensuring all details are correct and submitted promptly will facilitate a smoother adjustment to your commercial general liability policy.

What is the CG 20 10 07 04 Liability Endorsement form?

This form is an endorsement commonly added to commercial general liability insurance policies. It serves to extend coverage to additional insureds, typically owners, lessees, or contractors, as identified in the policy's schedule. The form amends who is considered an insured under the policy in relation to specific liabilities that arise from the named insured's operations or the actions of those working on their behalf.

Who can be listed as an additional insured on this form?

The CG 20 10 endorsement allows various third parties to be named as additional insureds. These can include owners, lessees, or contractors engaged with the named insured in a business relationship or project. The specific parties must be listed in the schedule of the endorsement or the declarations of the policy.

What extent of coverage do additional insureds receive?

Additional insureds are covered for liability arising from bodily injury, property damage, or personal and advertising injury. However, coverage is only provided for incidents caused, in whole or in part, by the named insured or those acting on their behalf during the performance of ongoing operations. The scope of this coverage may be constrained by legal requirements or specific contractual obligations that dictate the limits and breadth of coverage extended to these additional insureds.

Are there any limitations to this coverage?

Yes, there are specific limitations and exclusions. Coverage for additional insureds does not apply to injuries or damages occurring after all work has been completed or once the project's operations have ceased. Additionally, coverage does not apply to damages ensuing from parts of the insured's work that have been put to use by entities other than contractors or subcontractors involved in the project.

How does this endorsement affect the policy's limits of insurance?

The CG 20 10 endorsement specifies that the maximum payable amount on behalf of an additional insured will not exceed the limits required by any contract or agreement or the policy's own limits of insurance, whichever is lesser. Importantly, it does not increase the overall limits of insurance provided by the policy.

Is it required to list all additional insureds by name?

Yes, for an individual or organization to be covered as an additional insured under this endorsement, they must be explicitly listed either in the schedule attached to the CG 20 10 form or within the policy's declarations. This ensures clarity regarding who is afforded coverage under the policy's terms.

Can coverage be broader than that required by a contract?

No, if the coverage afforded to the additional insured is necessitated by a contractual agreement, the insurance will not exceed the scope required by that contract. This means the coverage specificity and limits are directly influenced by the terms of the contract between the named insured and the additional insured.

What happen if the required coverage by a contract exceeds the policy's limits?

In cases where a contract stipulates coverage requirements that surpass the policy's limits, the insurance provided will only extend up to the maximum limits of the insurance policy itself. The endorsement clarifies that it does not increase the policy's overall limits of insurance, thus, any contractual requirements for higher coverage do not alter this condition.

Where can one find specific details about the coverage for additional insureds?

Details about the coverage, including named additional insureds, limits, and any specific conditions or exclusions, will be listed in the schedule of the CG 20 10 endorsement or within the policy's declarations. These documents should be reviewed carefully to understand the precise nature and extent of coverage extended to additional insureds.

Filling out the CG 20 10 07 04 Liability Endorsement form is a critical process that requires attention to detail. Unfortunately, many people make errors during this process. Here are seven common mistakes:

Not including the full legal name of the additional insured person or organization. Many individuals simply use nicknames or incomplete names, which can lead to coverage issues.

Failing to specify the correct location(s) of covered operations. Accuracy in this area is crucial for ensuring the scope of coverage is clear and applicable.

Omitting information required in the Schedule that is not immediately obvious. All necessary details that are indicated to be shown in the Declarations must be thoroughly reviewed and included.

Assuming coverage without understanding the limits as defined by law. Individuals often overlook that the endorsement specifies coverage is only applicable to the extent permitted by law.

Ignoring the specifics of the additional exclusions. This endorsement outlines conditions under which the insurance does not apply, an area frequently overlooked.

Misinterpreting the limits of insurance. There's a common misconception that the additional insured's coverage is unlimited or matches the primary policyholder's limits, without considering the stipulated conditions.

Overlooking the endorsement's requirement for the insurance coverage to not exceed that required by contract or agreement. This leads to misunderstandings regarding the breadth of coverage.

Here are several additional recommendations to avoid errors when filling out this form:

Double-check the legal names of all parties involved and ensure they are correctly spelled.

Clarify the details of covered operations and locations with all relevant parties to ensure accuracy.

Review the contract or agreement meticulously to understand the insurance requirements and ensure they align with the endorsement.

Pay close attention to the additional exclusions section to clearly understand the limitations of coverage.

Consult with a legal advisor or insurance professional if any part of the endorsement or its requirements is unclear.

By being meticulous and seeking clarity on these points, individuals can more accurately complete the CG 20 10 07 04 Liability Endorsement form, thus ensuring the intended coverage is in place.

When it comes to managing liability and ensuring comprehensive coverage, the CG 20 10 07 04 Liability Endorsement form plays a crucial role. However, to ensure a robust and protective legal foundation, this form is often accompanied by additional documents. These documents, each serving a specific purpose, contribute to forming a comprehensive insurance and liability management approach for businesses and individuals alike. The following list provides a brief description of other forms and documents frequently used alongside the CG 20 10 07 04 Liability Endorsement form.

Ensuring the right combination of these documents and forms is in place offers businesses and individuals a layered protection strategy against various liabilities. Such thoroughness addresses potential risks proactively, safeguarding assets and fostering a stable operational environment. The utilisation of these forms and documents, in conjunction with the CG 20 10 07 04 Liability Endorsement form, enables a comprehensive approach to liability and insurance management.

CG 20 37 07 04 – Additional Insured – Owners, Lessees or Contractors – Automatic Status for Other Parties When Required in a Written Construction Agreement: Like the CG 20 10 07 04, this endorsement extends additional insured status to other parties involved in a construction project. However, the automatic status is given when a written construction agreement requires it, underlining the flexibility in extending coverage, contingent upon contractual obligations.

CG 20 33 07 04 – Additional Insured – Owners, Lessees or Contractors – Completed Operations: This document is akin to the CG 20 10 07 04 in that it amends the liability insurance policy to include additional insureds. However, its focus is specifically on the coverage of completed operations, providing protection after the work at the project site has finished, reflecting a longer-term liability coverage approach.

CG 00 01 – commercial general liability (CGL) Policy Form: This foundational document outlines the standard coverage provided under a commercial general liability policy, of which the CG 20 10 07 04 is an endorsement. It sets the primary framework for liability coverage from which the CG 20 10 makes specific alterations, thereby serving as the base policy that is modified by endorsements like the CG 20 10 07 04.

ISO Form CG 20 26 – Additional Insured – Designated Person or Organization: This form is quite similar to the CG 20 10 07 04 in that it provides a way to extend coverage to additional insureds. The distinction lies in its broader applicability to include not just owners, lessees, or contractors, but any person or organization designated in the schedule, offering a wider net of coverage.

CG 24 26 – Waiver of Transfer of Rights of Recovery Against Others to Us: While this form does not directly modify who is considered an insured, it complements forms like the CG 20 10 by stipulating conditions under which rights of recovery (subrogation) are waived. Such waivers are often critical in contracts where parties agree to mutual indemnification and waiver of subrogation clauses, affecting the overall risk allocation and liability among parties.

CG 21 39 – Contractual Liability Limitation: This endorsement limits the scope of contractual liability coverage provided under the CGL policy. It parallels the CG 20 10 07 04 in the context of contractual obligations; however, the CG 21 39 restricts coverage, whereas the CG 20 10 07 04 expands it to additional insureds. This showcases the balancing act between extending and limiting coverage based on specified contractual agreements.

When filling out the CG 20 10 07 04 Liability Endorsement form, it's important to adhere to specific guidelines to ensure the information is recorded accurately and completely. Below are lists of what you should and shouldn't do during this process.

What You Should Do:

What You Shouldn't Do:

The CG 20 10 07 04 Liability Endorsement, commonly misunderstood, serves a critical role in the realm of commercial liability insurance. Clarifying misconceptions surrounding this endorsement is essential for policyholders to accurately grasp its impact on their coverage.

Misconception 1: It provides blanket coverage for all additional insureds under any circumstance. It's often thought that once a person or organization is listed as an additional insured under this endorsement, they receive broad coverage for any liability claim they might face. However, the coverage is explicitly conditioned upon the liability arising out of the named insured's operations or premises. Thus, the scope is significantly narrower, focusing on specific liabilities directly connected to the insured's acts or the acts of those acting on their behalf.

Misconception 2: The additional insured has the same level of coverage as the primary insured. While it adds parties as additional insureds, this endorsement does not extend all the policy's privileges to them. The coverage for additional insureds is subject to the terms outlined in the endorsement, which may offer a reduced scope compared to what the named insured receives. Particularly, the coverage is only applicable "to the extent permitted by law" and is often conditional upon being required by a contract or agreement.

Misconception 3: The endorsement covers all acts or omissions by the additional insured. A common error is to assume that once added to the policy, any act or negligence by the additional insured is covered. The truth is, coverage only applies to the liability for bodily injury, property damage, or personal and advertising injury that are directly caused, in whole or in part, by the named insured's actions or those acting on their behalf, not the additional insured's independent actions.

Misconception 4: The coverage is indefinite and applies to all completed work. Another mistaken belief is that the endorsement provides perpetual coverage for completed work. The coverage explicitly excludes bodily injury or property damage occurring after all work on the project has been completed or after the completed work has been put to its intended use, signaling a clear temporal limit on the insurance provided.

Misconception 5: The limits of insurance increase with the addition of an insured. It is often presumed that adding an additional insured inherently increases the policy's overall limits of insurance. However, the endorsement specifically states that it does not increase the applicable limits of insurance. For an additional insured, the insurance limit is the lesser of the amount required by the contract or the available limits under the policy, further emphasizing the controlled and specific nature of this coverage extension.

Understanding the precise functionality and limitations of the CG 20 10 07 04 Liability Endorsement is paramount for businesses navigating their insurance needs. Dispelling these common misconceptions enables policyholders and additional insureds to set appropriate expectations for coverage and risk management.

Understanding the CG 20 10 07 04 Liability Endorsement form is essential for individuals and entities involved in commercial activities, especially those hiring contractors or being hired as contractors. Here are key takeaways to ensure clarity and compliance:

In conclusion, the CG 20 10 07 04 Endorsement is a critical tool in managing risks and liabilities in commercial operations, particularly in construction and contracting industries. Properly completing and incorporating this document into a CGL policy can significantly affect the protection against claims and legal disputes for all parties involved.

How Much Does It Cost to Join Melaleuca - Benefit from the option to suspend your Melaleuca MORE subscription and other services with this straightforward form.

Bgs Pricing - Card details such as sport, quantity, year, set name, card number, and player name must be clearly listed alongside the declared value for insurance purposes.

Broward County Animal Care - Facilitates legal compliance by providing a designated space for the animal control license number, if applicable in your jurisdiction.