Free Cg 20 26 04 13 PDF Template

Free Cg 20 26 04 13 PDF Template

In the labyrinth of commercial insurance policies, endorsements such as the CG 20 26 04 13 form play a crucial role in defining the scope and extent of coverage. This specific endorsement, integral to commercial general liability insurance, aims at extending the insurance protection to include additional insured persons or organizations, thereby modifying the standard coverage. Typically appended to the commercial general liability coverage part, this document necessitates careful attention because it delineates the conditions under which an additional insured is covered, focusing particularly on liability arising from bodily injury, property damage, or personal and advertising injury. Specifically, it addresses the cover for such liabilities when they stem from the actions or omissions of the named insured or those acting on their behalf, either in the execution of ongoing operations or in association with the insured’s premises. Crucially, the endorsement outlines that coverage for additional insureds is subject to legal permissibility and, when mandated by contractual agreements, will not exceed the obligations outlined within those contracts. Additionally, it adjusts the insurance limits, stating clearly that any coverage extended will not surpass the lesser of the contractual requirements or the limits depicted in the policy declarations, ensuring that the endorsement does not inadvertently increase the overall limits of insurance. Exploring the specifics of the CG 20 26 04 13 form unravels the complexities of extending coverage to additional insureds, highlighting the importance of understanding the nuanced legal and contractual obligations that govern these amendments to insurance policies.

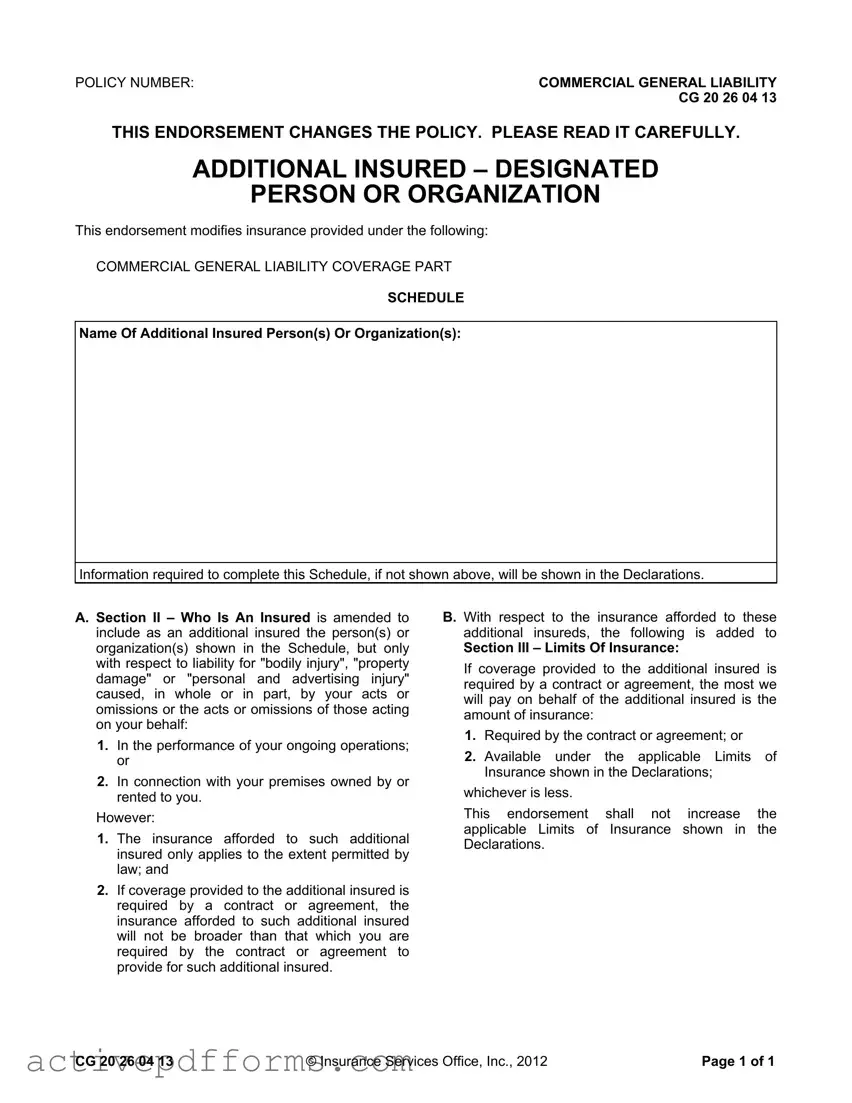

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 26 04 13 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – DESIGNATED

PERSON OR ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s) Or Organization(s):

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by your acts or omissions or the acts or omissions of those acting on your behalf:

1.In the performance of your ongoing operations; or

2.In connection with your premises owned by or rented to you.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable Limits of Insurance shown in the Declarations;

whichever is less.

This endorsement shall not increase the applicable Limits of Insurance shown in the Declarations.

CG 20 26 04 13 |

© Insurance Services Office, Inc., 2012 |

Page 1 of 1 |

| Fact Number | Fact Description |

|---|---|

| 1 | Form Number: CG 20 26 04 13 |

| 2 | Purpose: Provides additional insured status to a designated person or organization. |

| 3 | Applicable Coverage: Commercial General Liability Coverage Part |

| 4 | Scope of Coverage: Includes additional insureds for liability arising from the policyholder's acts or omissions or those acting on their behalf, in relation to ongoing operations or premises owned/rented. |

| 5 | Legal Limitations: Coverage for additional insureds applies only to the extent permitted by law. |

| 6 | Contractual Requirements: Coverage will not exceed requirements of a contract or agreement necessitating additional insured status. |

| 7 | Limit of Insurance Modification: The most paid on behalf of an additional insured will not exceed the amount specified by the contract or the policy limits, whichever is less. |

| 8 | Non-Increase of Policy Limits: Endorsement does not increase the overall Limits of Insurance of the policy. |

| 9 | Document Copyright: Insurance Services Office, Inc., 2012 |

Before diving into the steps for filling out the CG 20 26 04 13 form, it is crucial to understand the context and the significance of this document. This form plays a significant role for businesses seeking to expand their coverage to include additional insured persons or organizations. It modifies the commercial general liability coverage, specifically tailoring the policy to include designated third parties. The form outlines conditions under which the additional insureds are covered, emphasizing the importance of understanding these details to ensure compliance and adequate coverage. Below are the steps to correctly complete this form, ensuring that the additional insureds are properly listed and covered under your policy.

After completing these steps, your policy will extend to cover the designated additional insured(s), as specified in the CG 20 26 04 13 form. It is paramount to understand that this endorsement could significantly affect your policy's coverage and should be filled out with utmost accuracy and attention to detail. Should there be any confusion or uncertainty at any point during this process, consulting with an insurance professional or legal advisor is highly advisable to ensure that the interests of all parties are adequately protected.

What is the CG 20 26 04 13 form?

The CG 20 26 04 13 form is an endorsement used in commercial general liability (CGL) policies. It specifically modifies the policy to include certain individuals or organizations as additional insureds. This change extends the policy's protection to cover liabilities for bodily injury, property damage, or personal and advertising injury caused partly or entirely by the actions or omissions of the named insured or those acting on their behalf, linked to the insured's operations or premises.

Who can be added as an additional insured on this endorsement?

Individuals or organizations specified in the CG 20 26 04 13 form’s schedule can be added as additional insureds. These entities are typically added because of a legal or contractual relationship with the named insured, such as landlords, lessors, or business partners, whose exposure to risks is increased by their association with the named insured's operations or premises.

Under what conditions does the additional insured coverage apply?

Coverage for additional insureds under this endorsement applies only with respect to liability for bodily injury, property damage, or personal and advertising injury caused, in whole or in part, by the named insured's actions or those acting on their behalf. This includes actions taken during the performance of the named insured’s ongoing operations or in connection with the named insured’s premises. However, the coverage is subject to the restrictions of applicable law and the specific requirements of any contract or agreement stipulating the need for such coverage.

Does this endorsement affect the policy's limits of insurance?

No, the CG 20 26 04 13 endorsement does not increase the policy's overall limits of insurance for additional insureds. If coverage for an additional insured is mandated by a contract or agreement, the maximum that will be paid on behalf of the additional insured is either the amount required by the contract or agreement or the limits shown in the policy's Declarations, whichever is lesser.

Is the coverage for additional insureds broader than the coverage for the named insured?

No, the insurance provided to additional insureds will not exceed the scope of coverage the named insured is obligated to provide as per any contract or agreement. Essentially, if the named insured is required by contract to extend certain protections to an additional insured, the coverage afforded through this endorsement will mirror those requirements but will not surpass the insured’s contractual obligations or the policy's terms.

How does adding an additional insured impact the named insured’s policy?

Adding an additional insured to a CGL policy via the CG 20 26 04 13 endorsement extends the policy's liability protections to cover certain risks associated with the additional insured, as-per contractual obligations. This can help the named insured comply with business agreements requiring such coverage. However, it does not increase the policy's limits of insurance, and care should be taken to ensure that any such addition aligns with the named insured’s coverage needs and legal or contractual obligations.

When filling out the CG 20 26 04 13 form, commonly known as the Additional Insured – Designated Person or Organization endorsement, individuals often make mistakes. These errors can significantly impact the coverage and protection offered under a Commercial General Liability insurance policy. It is crucial to avoid these common pitfalls to ensure the intended individuals or organizations gain the correct level of insurance protection.

Not clearly identifying the additional insured person or organization in the Schedule, leading to confusion about who is covered.

Omitting relevant information that should be included in the Declarations to complete the Schedule properly.

Assuming the additional insured's coverage is automatic without verifying the extent of coverage permitted by law.

Misunderstanding the scope of coverage, especially that it only applies to liability caused by the named insured’s acts or omissions.

Overlooking that coverage for the additional insured is no broader than required by any contract or agreement if such requirement exists.

Failure to realize that the insurance might not extend to all acts or omissions outside the performance of ongoing operations or in connection with the named insured’s premises.

Failing to note that the limits of insurance for the additional insured may be capped by a contract or agreement or by the limits shown in the Declarations.

Not understanding that this endorsement does not increase the overall Limits of Insurance for the policy.

Not regularly reviewing and updating the endorsement to reflect changes in the contractual relationship or extent of the required coverage.

Incorrectly believing that additional insured status grants broader rights under the policy than it actually does.

It's vital to approach this form with careful attention to detail and a thorough understanding of the coverage implications it brings. Consulting with a qualified insurance professional can provide clarity and guidance, reducing the risk of these common mistakes.

When managing commercial general liability, the CG 20 26 04 13 form, which designates certain entities or individuals as additional insureds, is a critical document that broadens the scope of who is covered under a policy. However, to fully understand and implement the insurance coverage, several other forms and documents often accompany this endorsement. These forms play crucial roles in defining the parameters of coverage, outlining responsibilities, and ensuring compliance with legal and contractual obligations.

Together with these forms, the CG 20 26 04 13 endorsement becomes part of a comprehensive approach to managing risk through commercial insurance. Each document has a specific function, from proving insurance coverage to defining the scope and limits of coverage, making it essential for policyholders and additional insureds to understand their content and implications.

CG 20 10 (Additional Insured – Owners, Lessees or Contractors): Similar to the CG 20 26, the CG 20 10 form extends additional insured status but focuses on owners, lessees, or contractors. Both forms modify the “Who Is An Insured” section of a general liability policy, specifying under what conditions additional parties are covered.

CG 20 33 (Additional Insured – Owners, Lessees Or Contractors – Automatic Status When Required In Construction Agreement With You): This document, like the CG 20 26, offers additional insured status. It automatically provides this status to owners, lessees, or contractors whenever required by a construction contract, emphasizing its use in construction agreements, similar to the CG 20 26's applicability to ongoing operations or premises related agreements.

CG 20 37 (Additional Insured – Completed Operations): The CG 20 37 form extends additional insured coverage for completed operations, whereas the CG 20 26 typically covers ongoing operations. Despite this difference, both serve the purpose of modifying who is covered under a commercial general liability policy in specific, outlined scenarios.

CG 24 26 (Waiver of Subrogation – Designated Person or Organization): While the CG 24 26 involves a waiver of subrogation rights rather than extending additional insured status, it similarly amends a policy to benefit a third party. Both forms require specific scheduling of the person or organization afforded new rights under the policy.

CG 00 01 (Commercial General Liability Coverage Form): This is the standard commercial general liability (CGL) coverage form. Forms like CG 20 26 are endorsements that attach to and modify the coverage provided by CG 00 01, specifying conditions under which additional insureds are covered.

ISO Form CA 20 48 (Designated Insured Endorsement for Auto Liability): Although this form pertains to automobile liability, the concept mirrors the CG 20 26, as it designates additional insureds under specific circumstances. Both forms involve modifying an original policy to extend coverage to additional entities or individuals.

CG 21 39 (Contractual Liability Limitation): This endorsement restricts coverage for contractual liability, contrasting with CG 20 26’s role in extending coverage to additional insureds under certain contractual scenarios. They are similar in their function to amend the scope of a general liability policy based on contractual requirements.

CG 20 15 (Additional Insured – Vendors): This form specifically extends additional insured status to vendors, similar to how CG 20 26 extends it to designated persons or organizations. Both endorsements amend the insurance policy to include additional insureds, albeit for different parties and under different conditions.

CG 04 13 (Additional Insured – Grantor of Franchises): The CG 04 13 offers additional insured status to franchisors, akin to how the CG 20 26 covers designated persons or organizations. Each targets specific types of operations and defines the scope of coverage extension within a general liability framework.

CG 20 38 (Additional Insured – Mortgagee, Assignee, or Receiver): Similar to the CG 20 26 form, the CG 20 38 extend additional insured status, this time to mortgagees, assignees, or receivers. Both documents serve to expand the list of insured under a policy for specified roles and under predetermined conditions.

Filling out the CG 20 26 04 13 form, an essential document for adding an additional insured to a Commercial General Liability policy, requires attention to detail and a clear understanding of what's required. Here are some dos and don'ts to guide you through the process:

Accurately completing the CG 20 26 04 13 form plays a pivotal role in extending liability coverage effectively. Always proceed with diligence and, when in doubt, consult with a professional to clarify complex points. The goal is to ensure that all parties understand and agree upon the extent of coverage provided.

It grants automatic coverage for all activities. A common misconception is that the CG 20 26 04 13 form extends coverage to the additional insured for all their business activities. In reality, it only covers liability arising from the named insured's operations or premises.

It provides unlimited insurance to additional insureds. Some may believe this endorsement offers unlimited coverage to additional insureds. However, coverage is limited to what is required by a contract or the limits specified in the Declarations, whichever is less. It clearly does not increase the overall Limits of Insurance.

The form covers all types of liabilities. While it may seem comprehensive, this particular endorsement specifically limits coverage to "bodily injury", "property damage", or "personal and advertising injury". It does not extend to all possible liabilities that may arise.

It only benefits the additional insured. While the form does add an additional insured, it's essential to understand that its primary function is to protect the named insured's interests, especially in a contractual relationship requiring such an endorsement. The protection afforded benefits both parties involved.

The coverage is automatically broader than required. There's a belief that the CG 20 26 04 13 automatically provides broader coverage than mandated by contract for the additional insured. Conversely, it expressly states that the coverage will not be broader than required by the agreement or law.

It replaces a primary insurance policy for the additional insured. Some may incorrectly assume that this endorsement can act as a primary insurance policy for the additional insured. This is not the case; it supplements the primary coverage that the additional insured should already have in place, providing specific coverage related to the named insured's actions.

Any updates to the policy automatically apply to the additional insured. It's a common misconception that if the named insured's policy is updated or amended, those changes automatically apply to the coverage extended to the additional insured. In fact, any changes to the scope of coverage for the additional insured would need to be made explicitly, often requiring a new endorsement or agreement.

Understanding the CG 20 26 04 13 form is crucial for ensuring that additional insureds are properly covered under a commercial general liability policy. Here are key takeaways to help navigate this important aspect of business insurance:

Ensuring all parties have the necessary coverage in place is fundamental to the protection of business interests. When used properly, the CG 20 26 04 13 form plays a crucial role in managing risk and safeguarding against potential liabilities.

Contract for Deed Texas - This agreement method is beneficial for buyers who may not qualify for traditional mortgage financing.

Controlled Drugs Register - A comprehensive documentation tool that captures essential details of controlled substances, facilitating audits and ensuring compliance with federal and state regulations.

Tb Risk Assessment Form - Offers a means to systematically track the outcomes of individuals tested for TB, facilitating follow-up and care.