Free Credit Report Dispute PDF Template

Free Credit Report Dispute PDF Template

In the vast financial landscape, one's credit report is like a passport to opportunities, determining access to loans, mortgages, and even the rates one qualifies for. However, inaccuracies in this crucial document can unjustly hinder one’s financial journey. Enter the Credit Report Dispute Form, an essential tool for individuals who find discrepancies in their credit reports. This document serves as the primary means to formally challenge and rectify any errors, ensuring that the information held by credit reporting agencies is accurate and fair. Whether it's a mistaken identity, an account incorrectly marked as late, or an outright error in account balances, the dispute form is the first step in the correction process. It is through this procedure that individuals can communicate directly with the credit bureaus, supplying evidence to support their claims, thereby advocating for their right to a fair and accurate credit portrait. Understanding the nuances of this form, including when and how to submit it, can empower consumers, affording them the control needed to safeguard their financial identity.

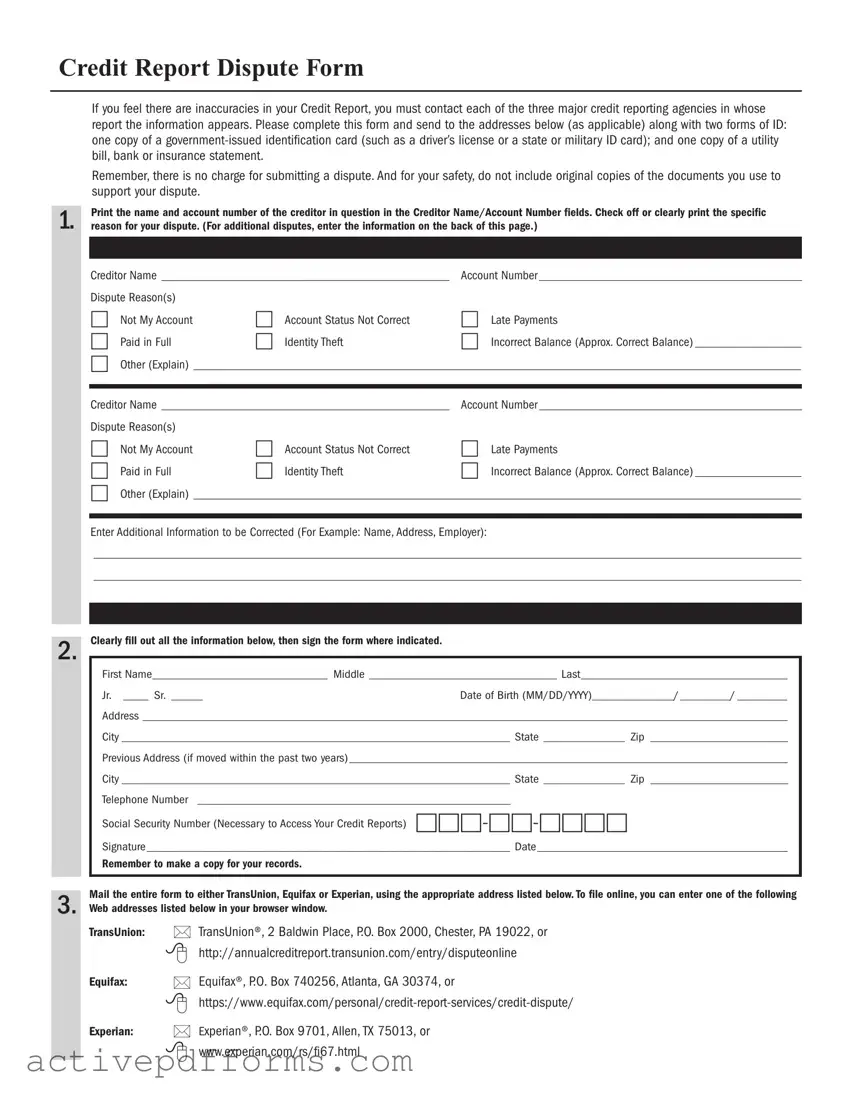

Credit Report Dispute Form

If you feel there are inaccuracies in your Credit Report, you must contact each of the three major credit reporting agencies in whose report the information appears. Please complete this form and send to the addresses below (as applicable) along with two forms of ID: one copy of a

Remember, there is no charge for submitting a dispute. And for your safety, do not include original copies of the documents you use to support your dispute.

Print the name and account number of the creditor in question in the Creditor Name/Account Number fields. Check off or clearly print the specific

1. reason for your dispute. (For additional disputes, enter the information on the back of this page.)

2.

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Enter Additional Information to be Corrected (For Example: Name, Address, Employer):

_________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________

Clearly fill out all the information below, then sign the form where indicated.

First Name____________________________ Middle ______________________________ Last_________________________________

Jr. ____ Sr. _____Date of Birth (MM/DD/YYYY)_____________/________/ ________

Address _______________________________________________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Previous Address (if moved within the past two years) ______________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Telephone Number __________________________________________________

Social Security Number (Necessary to Access Your Credit Reports)

Signature __________________________________________________________ Date________________________________________

Remember to make a copy for your records.

Mail the entire form to either TransUnion, Equifax or Experian, using the appropriate address listed below. To file online, you can enter one of the following

3. Web addresses listed below in your browser window.

TransUnion:

Equifax:

Experian:

•TransUnion®, 2 Baldwin Place, P.O. Box 2000, Chester, PA 19022, or

•http://annualcreditreport.transunion.com/entry/disputeonline

•Equifax®, P.O. Box 740256, Atlanta, GA 30374, or

•

•Experian®, P.O. Box 9701, Allen, TX 75013, or

•www.experian.com/rs/fi67.html

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

| # | Fact | Details |

|---|---|---|

| 1 | Purpose | Used to dispute inaccuracies or incomplete information in a credit report. |

| 2 | Applicable to | Any individual with a credit report in the United States. |

| 3 | Method | Disputes can be filed online, by mail, or sometimes by phone, depending on the credit reporting agency. |

| 4 | Processing Time | Credit bureaus are required to investigate the dispute within 30 to 45 days. |

| 5 | Outcome | If a dispute is resolved in the consumer's favor, the incorrect information must be corrected or removed from their credit report. |

| 6 | Cost | Filing a dispute is free of charge. |

| 7 | Governing Law(s) | The Fair Credit Reporting Act (FCRA) is the primary federal law that governs credit reporting and dispute procedures. |

When you find mistakes on your credit report, it's essential to take action by filling out a Credit Report Dispute form. This process lets you communicate your concerns to the credit bureau, aiming to correct inaccuracies that could impact your financial reputation. After submission, the bureau will investigate your claim, typically within 30 to 45 days. They'll then inform you of their findings, and if your dispute is validated, the inaccuracies will be corrected. Here's a straightforward guide to help you fill out the form correctly.

After you've submitted the form, it's a waiting game, but know you've taken a critical step towards ensuring your credit report accurately reflects your financial history. The credit bureau will reach out with their findings, and should corrections be necessary, they will adjust your credit report accordingly. Throughout this period, keep a close eye on your report and be prepared to follow up if the process takes longer than expected or if the response does not align with your evidence.

What is a Credit Report Dispute form?

A Credit Report Dispute form is a document you use to challenge inaccuracies or errors found on your credit report. When you identify a mistake, such as a debt you don’t owe or a payment wrongfully marked as late, this form allows you to formally request a correction from the credit reporting agency.

When should I submit a Credit Report Dispute form?

You should submit a Credit Report Dispute form as soon as you notice an error on your credit report. Acting quickly can prevent the mistake from affecting your credit score negatively, which can impact your ability to secure loans or other credit lines. Review your credit report regularly to ensure all information is accurate.

What information do I need to provide on the Credit Report Dispute form?

To complete a Credit Report Dispute form, you need to provide your personal details (name, address, social security number), details about the disputed item (account number, creditor’s name, nature of the dispute), and any evidence that supports your claim. This evidence might include bank statements, payment records, or letters from the creditor.

How do I submit the Credit Report Dispute form?

You can submit your Credit Report Dispute form through the mail or, in some cases, online through the credit reporting agency’s website. It’s advisable to send it by certified mail, with a return receipt requested, so you have proof that your dispute was received.

What happens after I submit the form?

After submitting your dispute, the credit reporting agency usually has 30 to 45 days to investigate the issue. They will review the information you provided, check with the creditor who reported the data, and then either confirm the accuracy of the information or update your report with the correct information. You will receive a written notice of the outcome.

Is there a fee to file a Credit Report Dispute?

Submitting a Credit Report Dispute form is free. Credit reporting agencies are required by law to investigate disputes without charging a fee. Be wary of any service that charges you to dispute errors on your behalf. It's an unnecessary expense for a process you can do yourself at no cost.

When individuals attempt to correct inaccuracies on their credit reports by submitting a dispute form, errors can occur that may hinder the process. Avoid these common mistakes to ensure your dispute is processed smoothly and effectively:

Not reviewing the credit report thoroughly before disputing. Many people rush to file a dispute before fully understanding their credit report. It's crucial to review every detail of your credit report from all three bureaus since mistakes can differ across reports.

Failing to dispute each mistake separately. Submitting a blanket dispute without addressing each error individually can lead to some inaccuracies being overlooked or not properly addressed by the credit bureaus.

Omitting supporting documentation. Providing evidence to support your dispute significantly increases the chances of having the mistake corrected. This can include bank statements, letters of deletion from creditors, or payment confirmations.

Using vague language in the dispute. Clearly and concisely state why the information is inaccurate and what outcome you expect. Vague language can lead to misunderstandings or insufficient investigation by the bureau.

Overlooking contact information. Double-check that you have provided your current and complete contact information. This ensures the credit bureau can reach you should they need further information or to notify you of the outcome.

Ignoring timelines. Credit bureaus have a specific time frame, typically 30 days, to investigate disputes. Keeping track of when you submitted your dispute allows you to follow up if you haven't received a response in a timely manner.

Submitting the same dispute without new information. If your initial dispute was not resolved in your favor, resubmitting the same dispute without providing new evidence or clarifying information is likely to yield the same result.

Assuming minor details don't matter. Even small discrepancies, such as the wrong date of a payment or a misspelled name, can affect your credit. Addressing these details can make a difference in your credit score.

Avoiding these errors can make the dispute process more effective and increase the likelihood of correcting inaccuracies on your credit report. It's important to approach the process with diligence and attention to detail.

When engaging with the process of disputing inaccuracies on a credit report, there's a collection of forms and documents that typically accompany the Credit Report Dispute Form. These materials play a significant role in ensuring that the dispute is not only heard but also adequately addressed. Each document serves a unique purpose, contributing vital information to support the claim of inaccuracies. Here's a brief look at some of the other forms and documents often involved in this process.

Utilizing these documents in conjunction with the Credit Report Dispute Form strengthens the case for dispute by providing a comprehensive overview of the inaccuracies and evidence to support the claims. Keeping these documents organized and readily accessible accelerates the dispute process, moving individuals closer to resolving their credit report issues efficiently.

Identity Theft Report: The Identity Theft Report shares a significant similarity with the Credit Report Dispute form because both documents serve as formal notifications to authorities or organizations about fraudulent activities. While the Credit Report Dispute form specifically addresses inaccuracies or unauthorized transactions on one's credit report, the Identity Theft Report encompasses a broader scope, informing law enforcement and credit bureaus about identity theft. However, both documents are integral in the process of rectifying the consequences of identity fraud, offering the affected individuals a pathway to reclaim their financial security and accuracy in personal records.

Annual Credit Report Request Form: This form, like the Credit Report Dispute form, is closely related to personal financial oversight. Individuals use the Annual Credit Report Request Form to obtain a free copy of their credit report from each of the three major credit bureaus once every 12 months. The critical connection between these two forms is their role in personal credit management. Reviewing one's credit report annually can lead to discovering inaccuracies or outdated information, which then could be challenged through the Credit Report Dispute form, underscoring their complementary nature in maintaining credit accuracy.

Billing Error Dispute Letter: Similar to the Credit Report Dispute form, this document is used by individuals who notice unauthorized charges or billing errors on their account statements. The Billing Error Dispute Letter is directed towards the creditor or service provider responsible for the billing, requesting a correction of the mistake. Both documents function as formal grievances about financial discrepancies, albeit targeted at different entities. They protect consumers’ rights by providing a method to dispute unwarranted financial transactions or reports.

Loan Discrepancy Report: When borrowers find inconsistencies in loan statements or believe there has been a mistake in the calculation of their loan dues, they can file a Loan Discrepancy Report. This document bears similarity to the Credit Report Dispute form in its purpose to correct errors within financial documents. Though one pertains directly to credit reporting and the other to loan account details, both empower individuals to seek rectification of errors that could adversely affect their financial responsibilities and creditworthiness.

Privacy Complaint Form: People concerned about the misuse or unauthorized sharing of their personal information can file a Privacy Complaint Form with the pertinent organizations or government bodies. This form and the Credit Report Dispute form are alike in their function to safeguard personal information and financial integrity. They both serve as tools for individuals to voice their concerns regarding privacy breaches or inaccuracies that could have lasting impacts on their personal and financial lives. The underlying goal of both documents is to protect and rectify personal information, ensuring its correct use and reportage.

Addressing inaccuracies on your credit report is crucial for maintaining your financial health. When filling out a Credit Report Dispute form, certain practices should be followed to ensure your dispute is handled efficiently and effectively. Here’s a compiled list of do’s and don’ts to guide you through the process:

Do:

Gather all relevant documentation supporting your dispute before you start filling out the form. This could include bank statements, letters, or emails.

Clearly identify each item on your credit report that you believe is incorrect, providing a detailed explanation of why it should be corrected or removed.

Be precise in your language. Use direct and straightforward wording to convey your concerns without ambiguity.

Include your complete contact information. Ensure you provide a current address, phone number, and email so you can be reached easily for any follow-up.

Retain a copy of the dispute form and all correspondence for your records. It’s important to have a paper trail documenting your efforts to correct the issue.

Don't:

Overlook minor errors. Even small mistakes can have a significant impact on your credit score. Report any inaccuracy, no matter how small it seems.

Send original documents. Always send copies to protect your valuable originals. Losing original documents can lead to additional headaches.

Get discouraged if your first attempt doesn’t resolve the issue. Sometimes, it may take more than one attempt to correct an error on your credit report.

By following these guidelines, you're taking proactive steps to safeguard your financial reputation. A well-prepared dispute can lead to corrections that positively impact your credit score, making it easier to secure loans or credit cards in the future. Remember, your right to dispute inaccuracies on your credit report is protected by law, so use it wisely to maintain your financial health.

Many people carry misconceptions about the Credit Report Dispute form, a crucial tool for correcting inaccuracies on one’s credit report. Understanding these misconceptions is key to effectively managing one's credit health.

It costs money to file a dispute. This is not the case. Consumers can file a dispute with the credit reporting agencies at no charge. This process is a consumer right protected under the Fair Credit Reporting Act (FCRA).

A dispute can remove all negative information. Not all negative information can be removed through a dispute. Accurate negative information will typically remain on your credit report for up to seven years.

Disputing online is always the best option. While disputing online may be convenient, mailing a dispute might provide a paper trail that could be useful for complex disputes or if the issue escalates to legal action.

Once something is disputed, it gets removed immediately. The credit reporting agencies have up to 30 days to investigate disputes. The disputed information will only be removed if it is found to be inaccurate or can no longer be verified.

You need a lawyer to dispute inaccuracies. Consumers can initiate disputes on their own using the information provided by the credit reporting agencies. Consulting a lawyer might be beneficial for complicated situations but is not a necessity.

Disputing accurate information will help your score. Filing a dispute does not affect your credit score directly. If the dispute leads to the removal of inaccuracies, your score could improve as a result.

Submitting multiple disputes at once is more effective. Bombarding the credit bureaus with disputes can actually be counterproductive. It's more effective to prioritize and submit disputes individually or in small groups, focusing on the most significant errors first.

You can't dispute information you previously agreed was correct. You have the right to dispute any information on your credit report at any time. If your situation changes or you find new evidence, you can initiate a new dispute.

A successful dispute will fix your credit instantly. While removing inaccurate negative information can improve your credit, rebuilding your credit score is a process that involves managing debt responsibly and making timely payments.

You only need to dispute inaccuracies with one credit bureau. Each credit bureau operates independently. An error on one report might not exist on another. It's critical to check all your credit reports and file disputes with each bureau that is reporting the inaccurate information.

Understanding these misconceptions can empower individuals to take charge of their credit reports and, by extension, their financial health. Clearing up inaccuracies can be a straightforward process if approached with the correct information and expectations.

When addressing inaccuracies on your credit report, the Credit Report Dispute form serves as a crucial tool. Its correct use can significantly influence your financial health, potentially improving your credit score by removing erroneous information. Here are 10 key takeaways for effectively filling out and using the Credit Report Dispute form:

Effectively using the Credit Report Dispute form can lead to corrections that positively impact your credit score. It is a process that requires attention to detail and persistence but can ultimately protect your financial well-being.

Sr13 Form - Addresses the protocol for vehicles uninsured at the time of the accident and their reporting requirements.

Legal Guardianship Forms - Can be used to prove to authorities or institutions the legal basis for the temporary guardianship arrangement.

How to File Mechanics Lien California - By leveling the playing field between property owners and construction professionals, it plays a significant role in maintaining a balanced industry ecosystem.