Free Fee Worksheet PDF Template

Free Fee Worksheet PDF Template

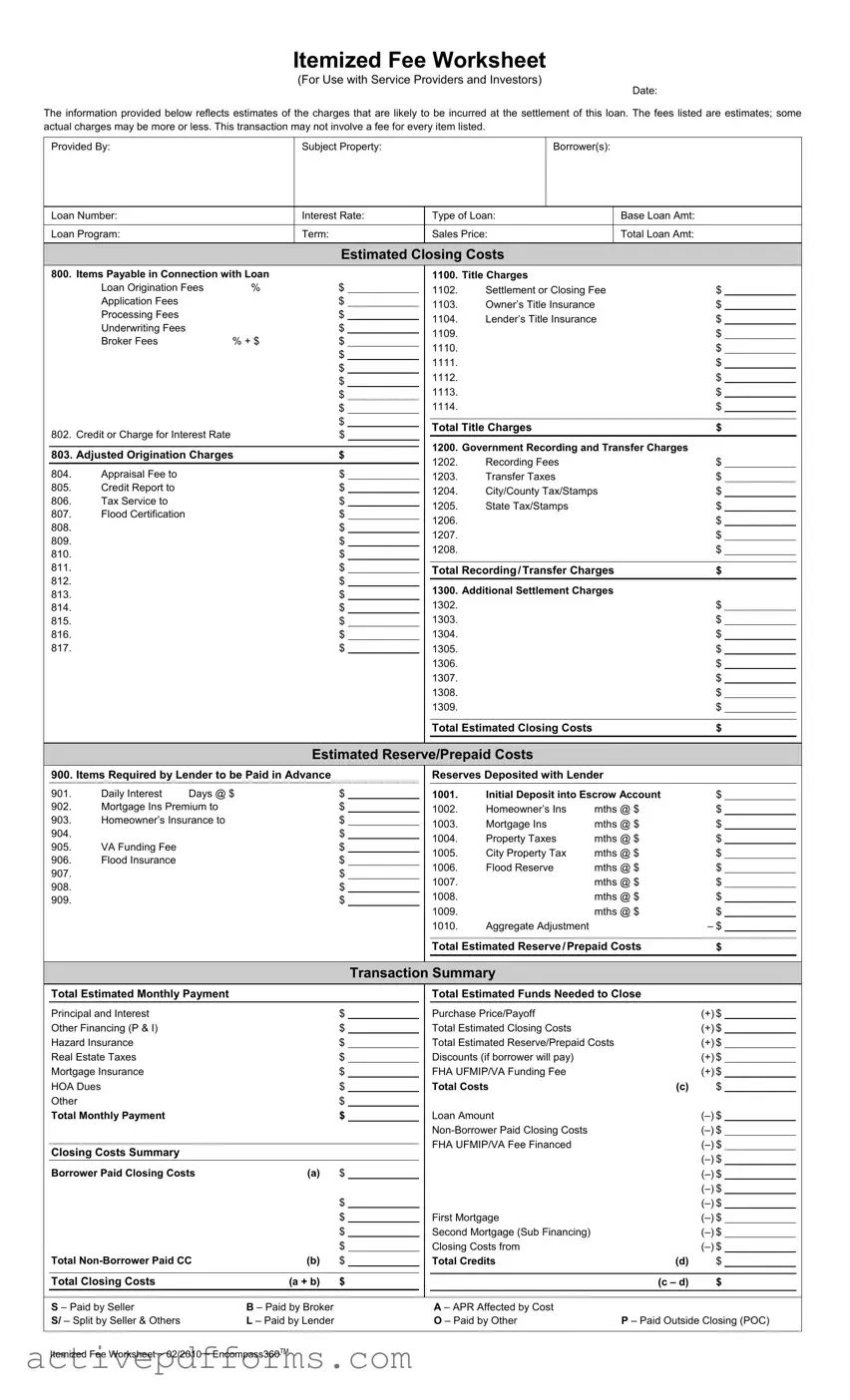

When navigating the complexities of acquiring a mortgage, borrowers and their service providers come across a crucial document known as the Itemized Fee Worksheet. This detailed document, essential for transparency in mortgage transactions, outlines the estimated costs that borrowers are likely to encounter at the close of the loan. It breaks down numerous charges, from loan origination fees and title charges to government recording and transfer charges, as well as additional settlement charges and reserve/prepaid costs. The form serves a vital role in providing an early estimate of what the borrower can expect in terms of fees, thereby aiding in financial planning and decision-making. Not only does it list each fee, but it also categorizes them into easily understandable sections, offering insight into the total estimated closing costs, monthly payments, and the total funds needed to close the transaction. As it includes potential variations like discounts and non-borrower paid closing costs, the worksheet ensures a comprehensive overview, although it's important to note that the final costs may vary. Providing such estimates empowers borrowers and investors with greater control over their financial commitments and expectations throughout the mortgage process.

Itemized Fee Worksheet

(For Use with Service Providers and Investors)

Date:

The information provided below reflects estimates of the charges that are likely to be incurred at the settlement of this loan. The fees listed are estimates; some actual charges may be more or less. This transaction may not involve a fee for every item listed.

|

Provided By: |

|

|

Subject Property: |

|

|

|

Borrower(s): |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Loan Number: |

|

|

Interest Rate: |

|

Type of Loan: |

|

Base Loan Amt: |

|

|

|

||||||

|

Loan Program: |

|

|

Term: |

|

|

|

|

Sales Price: |

|

Total Loan Amt: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Estimated Closing Costs |

|

|

|

|

|

||||||

800. |

Items Payable in Connection with Loan |

|

|

|

1100. |

Title Charges |

|

|

|

|

|

||||||

|

|

Loan Origination Fees |

% |

|

$ |

|

|

1102. |

Settlement or Closing Fee |

$ |

|

|

|||||

|

|

|

|

|

|||||||||||||

|

|

Application Fees |

|

|

|

$ |

|

|

1103. |

Owner’s Title Insurance |

$ |

|

|

||||

|

|

|

|

|

|

|

|||||||||||

|

|

Processing Fees |

|

|

|

$ |

|

|

1104. |

Lender’s Title Insurance |

$ |

|

|

||||

|

|

Underwriting Fees |

|

|

|

$ |

|

|

|

|

|||||||

|

|

|

|

|

|

|

1109. |

|

|

|

|

$ |

|

|

|||

|

|

Broker Fees |

|

% + $ |

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

1110. |

|

|

|

|

$ |

|

|

||||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1111. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1112. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1113. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

$ |

|

|

1114. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Title Charges |

|

|

$ |

|

|

|||

802. |

Credit or Charge for Interest Rate |

|

|

$ |

|

|

|

|

|

|

|

||||||

|

|

|

|

1200. |

Government Recording and Transfer Charges |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

803. Adjusted Origination Charges |

$ |

|

|

|

|

|

||||||||||

|

|

|

1202. |

Recording Fees |

|

|

$ |

|

|

||||||||

804. |

Appraisal Fee to |

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

1203. |

Transfer Taxes |

|

|

$ |

|

|

||||||

|

|

|

|

|

|

|

|||||||||||

805. |

Credit Report to |

|

|

|

$ |

|

|

1204. |

City/County Tax/Stamps |

$ |

|

|

|||||

806. |

Tax Service to |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1205. |

State Tax/Stamps |

|

|

$ |

|

|

||||||

807. |

Flood Certification |

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

1206. |

|

|

|

|

$ |

|

|

|||||

808. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

1207. |

|

|

|

|

$ |

|

|

||||

809. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

1208. |

|

|

|

|

$ |

|

|

||||

810. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

811. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Total Recording/Transfer Charges |

$ |

|

|

|||||||

|

|

|

|

|

|

||||||||||||

812. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1300. |

Additional Settlement Charges |

|

|

|

|||||||

813. |

|

|

|

|

$ |

|

|

|

|

|

|||||||

814. |

|

|

|

|

$ |

|

|

1302. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

815. |

|

|

|

|

$ |

|

|

1303. |

|

|

|

|

$ |

|

|

||

816. |

|

|

|

|

$ |

|

|

1304. |

|

|

|

|

$ |

|

|

||

817. |

|

|

|

|

$ |

|

|

1305. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

1306. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1307. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1308. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1309. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Total Estimated Closing Costs |

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

Estimated Reserve/Prepaid Costs |

|

|

|

|

|

|||||||

|

900. Items Required by Lender to be Paid in Advance |

|

|

|

|

Reserves Deposited with Lender |

|

|

|

||||||||

901. |

Daily Interest |

Days @ $ |

$ |

|

|

1001. |

Initial Deposit into Escrow Account |

$ |

|

|

|||||||

902. |

Mortgage Ins Premium to |

|

|

$ |

|

|

1002. |

Homeowner’s Ins |

mths @ $ |

$ |

|

|

|||||

|

|

|

|

|

|

||||||||||||

903. |

Homeowner’s Insurance to |

|

|

$ |

|

|

1003. |

Mortgage Ins |

mths @ $ |

$ |

|

|

|||||

904. |

|

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

|

1004. |

Property Taxes |

mths @ $ |

$ |

|

|

||||||

905. |

VA Funding Fee |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1005. |

City Property Tax |

mths @ $ |

$ |

|

|

|||||||

906. |

Flood Insurance |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1006. |

Flood Reserve |

mths @ $ |

$ |

|

|

|||||||

907. |

|

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

|

1007. |

|

|

mths @ $ |

$ |

|

|

|||||

908. |

|

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

1008. |

|

|

mths @ $ |

$ |

|

|

|||||

909. |

|

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

1009. |

|

|

mths @ $ |

$ |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

1010. |

Aggregate Adjustment |

|

|

– $ |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

Total Estimated Reserve/Prepaid Costs |

$ |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

Transaction Summary |

|

|

|

|

|

|||||

|

Total Estimated Monthly Payment |

|

|

|

|

|

|

Total Estimated Funds Needed to Close |

|

|

|

||||||

|

Principal and Interest |

|

|

|

$ |

|

|

|

Purchase Price/Payoff |

|

|

(+) $ |

|

|

|||

|

Other Financing (P & I) |

|

|

|

$ |

|

|

|

Total Estimated Closing Costs |

|

|

(+) $ |

|

|

|||

|

Hazard Insurance |

|

|

|

$ |

|

|

|

Total Estimated Reserve/Prepaid Costs |

(+) $ |

|

|

|||||

|

Real Estate Taxes |

|

|

|

$ |

|

|

|

Discounts (if borrower will pay) |

|

|

(+) $ |

|

|

|||

|

Mortgage Insurance |

|

|

|

$ |

|

|

|

FHA UFMIP/VA Funding Fee |

|

|

(+) $ |

|

|

|||

|

HOA Dues |

|

|

|

$ |

|

|

|

Total Costs |

|

(c) |

$ |

|

|

|||

|

Other |

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Monthly Payment |

|

|

|

$ |

|

|

|

Loan Amount |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

FHA UFMIP/VA Fee Financed |

|

|

|

|

|||

|

Closing Costs Summary |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Borrower Paid Closing Costs |

|

(a) |

$ |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

First Mortgage |

|

|

|

|

|||

|

|

|

|

|

|

$ |

|

|

|

Second Mortgage (Sub Financing) |

|

|

|

|

|||

|

Total |

|

(b) |

$ |

|

|

|

Closing Costs from |

|

|

|||||||

|

|

$ |

|

|

|

Total Credits |

|

(d) |

$ |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Total Closing Costs |

|

(a + b) |

$ |

|

|

|

|

|

|

|

(c – d) |

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

S – Paid by Seller |

|

B – Paid by Broker |

|

|

|

|

A – APR Affected by Cost |

|

|

|

|

|

||||

|

S/ – Split by Seller & Others |

|

L – Paid by Lender |

|

|

|

|

O – Paid by Other |

|

P – Paid Outside Closing (POC) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Itemized Fee Worksheet ~ 02/2010 ~ Encompass360TM

| Fact Name | Detail |

|---|---|

| Purpose of the Form | This form provides estimates of the charges likely to be incurred at the settlement of a loan. |

| Fee Estimation | The fees listed are estimates, meaning actual charges may vary. |

| Itemization | The worksheet itemizes various fees, including loan origination, title charges, and government recording charges. |

| Non-Uniformity of Charges | Not every transaction will involve a fee for every item listed. |

| Additional Costs | It includes sections for estimating reserve/prepaid costs and summarizes the total estimated monthly payment and funds needed to close. |

| Governing Laws | Applies universally but may include state-specific governing laws for certain charges, like recording and transfer taxes. |

Completing the Itemized Fee Worksheet is a crucial step for service providers and investors in the real estate industry. This document provides an estimated overview of the charges that could be incurred at the closing of a loan. Although the figures are approximations, they offer a comprehensive picture of potential financial responsibilities. Each section of the form must be filled out thoroughly to ensure transparency and accuracy in the loan settlement process. Here's a detailed guide on how to fill out each part of the Form.

After carefully filling out all sections of the form, review the information for accuracy and completeness. This meticulous approach ensures all parties involved in the transaction have a clear understanding of the financial expectations at closing. With the Itemized Fee Worksheet fully completed, stakeholders can proceed with confidence towards finalizing the loan settlement.

What is an Itemized Fee Worksheet?

The Itemized Fee Worksheet is a document that outlines the estimated fees and costs associated with a mortgage or loan settlement. This can include fees for the loan origination, title charges, government recording, and transfer charges, among others. These estimates are designed to give service providers, investors, and borrowers an idea of the charges they are likely to incur at the settlement of the loan.

Why are some fees on the Itemized Fee Worksheet estimated?

Fees on the Itemized Fee Worksheet are estimated because the exact costs can vary based on a range of factors such as location, loan type, and service providers involved. The worksheet provides an approximation to help borrowers understand potential settlement costs, with the understanding that some actual charges may be more or less than the estimates provided.

Are all the items listed on the Worksheet applicable to my transaction?

No, not every item listed on the Fee Worksheet will be applicable to every transaction. The document lists a variety of potential charges, some of which may not apply in all cases. For example, some loans may not require a flood certification fee or mortgage insurance premium. The applicable fees will depend on the specific details of the loan and property.

How can I find out the actual costs after receiving the Estimated Closing Costs?

The actual costs will be detailed in the Closing Disclosure, a document that provides the final costs of the mortgage transaction. This disclosure is required to be given to borrowers at least three business days before the closing of the loan, allowing you to compare the estimated costs from the Fee Worksheet with the final amounts.

What are "Items Required by Lender to be Paid in Advance"?

These are fees and adjustments that the lender requires to be paid before or at the time of closing. This can include prepaid interest, initial escrow deposits for homeowners insurance and property taxes, mortgage insurance premiums, and other applicable charges. They are necessary to establish and fund the escrow account that will be used to pay recurring costs associated with the property and loan.

How does the Total Estimated Monthly Payment get calculated?

The Total Estimated Monthly Payment is calculated by adding together the principal and interest of the loan, real estate taxes, homeowner’s insurance, mortgage insurance (if applicable), and any homeowners association (HOA) dues. These components reflect the monthly costs you will be responsible for paying as part of your mortgage. It’s a critical figure that helps borrowers understand their financial commitment in the loan agreement.

Filling out the Fee Worksheet form is an essential step in securing a loan for purchasing or refinancing a property. However, several common mistakes can impact the accuracy of this financial document and potentially the terms of the loan. Being aware of these errors can help ensure a smoother transaction. Below are eight common mistakes:

Failing to double-check the Date at the top of the form to ensure it reflects the current transaction date. This mistake can cause confusion and delays.

Not accurately listing the Subject Property details, including the address and legal description. This information is critical for identifying the property tied to the loan.

Incorrectly filling out the Borrower(s) section by either omitting a co-borrower or misspelling names. This can lead to issues with loan processing and legal documents.

Misunderstanding the Interest Rate and Type of Loan fields by not confirming the exact terms agreed upon. An incorrect interest rate can significantly affect loan payments.

Overlooking the Total Loan Amount and not ensuring it matches up with other documents. Discrepancies here can affect closing costs and loan-to-value ratios.

Entering incorrect figures under Items Payable in Connection with Loan and Title Charges, often due to misunderstanding what fees are actually payable and which party is responsible.

Omitting details in the Estimated Reserve/Prepaid Costs section, such as insurance premiums and property taxes, leading to underestimating the amount needed at closing.

Not checking the calculations in the Transaction Summary and Closing Costs Summary sections for accuracy. Even a small error can result in a significant financial discrepancy.

Lenders and borrowers alike benefit from careful attention to these details, ensuring the financial aspects of the property transaction are accurately captured. Understanding and avoiding these common mistakes can lead to a smoother closing process and prevent unexpected issues.

When processing a mortgage, the Itemized Fee Worksheet is a crucial document that provides an estimate of the fees and charges a borrower might incur during the settlement of a loan. However, this form does not exist in isolation. Several other forms and documents typically accompany it, playing vital roles in ensuring the mortgage process is transparent, compliant, and smoothly executed. Each of these documents serves a specific purpose, contributing to a comprehensive understanding of the financial responsibilities and legal implications of obtaining a loan.

Together, these documents ensure that all parties involved in a mortgage transaction are fully informed about the financial and legal aspects of the deal. They work in conjunction with the Itemized Fee Worksheet, providing a comprehensive picture of the costs, terms, and obligations associated with the loan. Understanding the purpose and content of each form is pivotal for anyone navigating through the mortgage process, ensuring transparency and compliance every step of the way.

The Good Faith Estimate (GFE) document is comparable because it provides an estimate of settlement charges and loan terms that borrowers can expect to pay during the mortgage process, much like the Fee Worksheet outlines estimated charges and fees associated with the loan settlement.

The Loan Estimate document is similar as it also gives a detailed preview of the loan terms, projected payments, and closing costs the borrower is likely to face, paralleling the Fee Worksheet's goal of offering an early look at expected loan-related expenses.

Settlement Statement (HUD-1 or Closing Disclosure) shares similarities, detailing final closing costs, loan terms, and other settled transactions. The Fee Worksheet serves a similar purpose but at an earlier stage, estimating what those final numbers might be.

Initial Escrow Statement resembles the Estimated Reserve/Prepaid Costs section of the Fee Worksheet by itemizing the costs the borrower will prepay or reserve at closing, including insurance premiums and property taxes.

The Closing Cost Worksheet is akin to the Fee Worksheet as it details an estimate of all costs and fees due at closing, designed to prepare borrowers for what financial obligations they will face.

Truth in Lending Act (TILA) Disclosure parallels the Fee Worksheet's functionality by detailing the cost of credit, APR, and other finance charges. While the TILA disclosure focuses more on the cost of the loan over time, the Fee Worksheet provides immediate cost estimates necessary for loan closing.

When tackling the Fee Worksheet, an essential form for those navigating the complexities of loans and real estate transactions, there are several critical dos and don'ts that one should adhere to. This guidance ensures accuracy and completeness, helping to avoid common pitfalls that could delay or complicate your loan process. Below is a curated list catering specifically to the Fee Worksheet intricacies:

Following these structured guidelines will facilitate a smoother transaction process, minimizing setbacks and ensuring that all parties are well-informed of the financial specifics of the deal. Remember, the Fee Worksheet is not just a formality but a foundational document that outlines the financial framework of your loan. Handling it with care and attention to detail is paramount.

Understanding the Fee Worksheet form is crucial in the loan process, but misconceptions can lead to confusion. Here are four common misunderstandings:

By addressing these misconceptions, borrowers can have a clearer understanding of the Fee Worksheet and its role in the loan process.

When filling out and using the Fee Worksheet, it is crucial to familiarize oneself with the following key takeaways:

Keeping these points in mind while working with the Fee Worksheet can greatly assist in navigating the financial aspects of service agreements with providers and investors.

How to Ask a Dad to Date His Daughter - It leverages absurdity and hyperbole to underscore the seriousness with which a parent approaches the prospect of someone dating their daughter, demanding high standards and thorough scrutiny.

Odometer Reading Form - Includes a formal declaration by the vehicle's owner, verified by a notary, about the odometer reading.

What Is a Ngb Form 22 - A comprehensive document that supports veterans in their transition to civilian life.