Free Fl Dr 312 PDF Template

Free Fl Dr 312 PDF Template

When managing the estate of a deceased individual in Florida, especially when it pertains to the issue of estate taxes, the Form DR-312, known as the Affidavit of No Florida Estate Tax Due, becomes a crucial document. This form, specifically designed for use when no federal estate tax return is needed and the estate owes no Florida estate tax, serves as a testament by the personal representative of the deceased. The role of the personal representative, as defined by Florida statutes, encompasses anyone in actual or constructive possession of the estate, signifying that this affidavit could extend to a varied group of individuals managing the decedent's properties. The completion and submission of Form DR-312 are vital steps in ensuring that the estate is not improperly encumbered by Florida estate tax liens, aligning with regulations specified in Chapter 198 of the Florida Statutes. Instructions outlined on the form detail the filing process, highlighting that it should be filed directly with the clerk of the circuit court in the relevant county or counties where the decedent owned property, explicitly stating not to send it to the Florida Department of Revenue. Furthermore, the form is a declaration under penalty of perjury by the personal representative that, to the best of their knowledge, the estate is not liable for Florida estate taxes, effectively streamlining the process for estates exempt from both federal and Florida estate taxes.

Affidavit of No Florida Estate Tax Due

Rule

Effective 01/21

Page1 of 2

(This space available for case style of estate probate proceeding) |

(For official use only) |

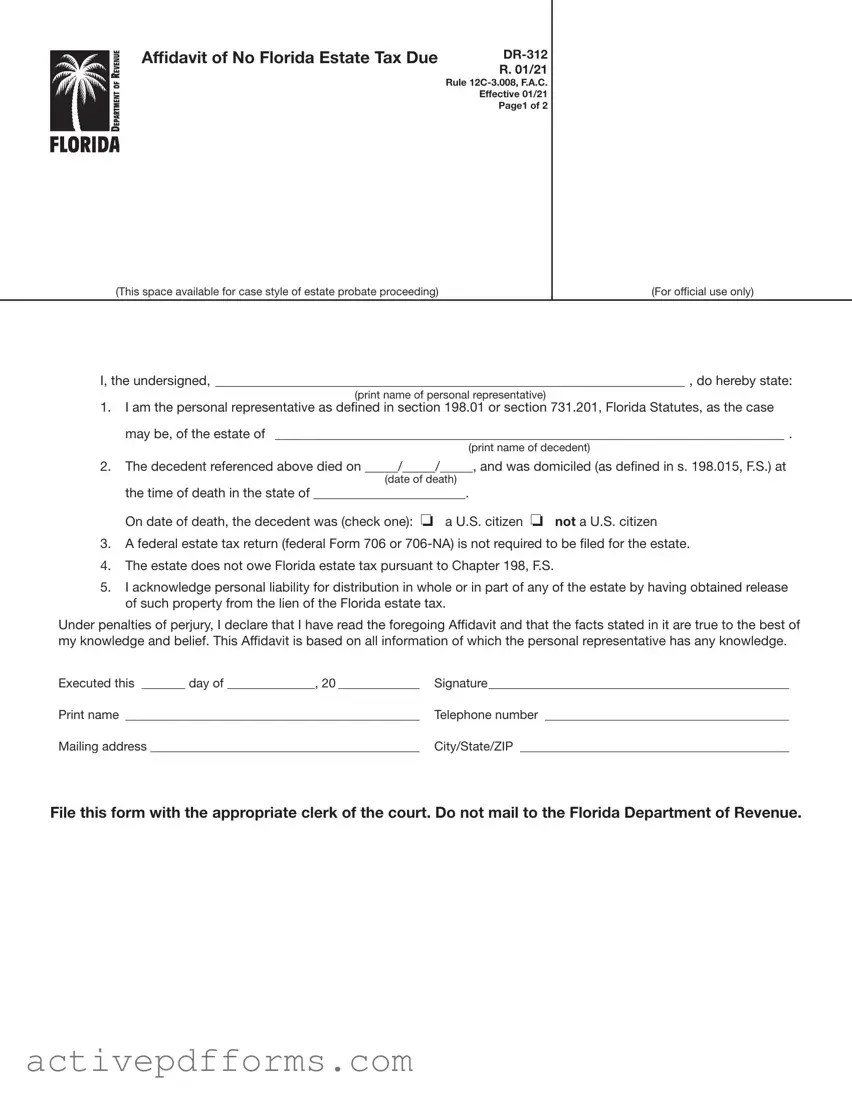

I, the undersigned, _______________________________________________________________________ , do hereby state:

(print name of personal representative)

1.I am the personal representative as defined in section 198.01 or section 731.201, Florida Statutes, as the case may be, of the estate of _____________________________________________________________________________ .

(print name of decedent)

2.The decedent referenced above died on _____/_____/_____, and was domiciled (as defined in s. 198.015, F.S.) at

(date of death)

the time of death in the state of _______________________.

On date of death, the decedent was (check one): o a U.S. citizen o not a U.S. citizen

3.A federal estate tax return (federal Form 706 or

4.The estate does not owe Florida estate tax pursuant to Chapter 198, F.S.

5.I acknowledge personal liability for distribution in whole or in part of any of the estate by having obtained release of such property from the lien of the Florida estate tax.

Under penalties of perjury, I declare that I have read the foregoing Affidavit and that the facts stated in it are true to the best of my knowledge and belief. This Affidavit is based on all information of which the personal representative has any knowledge.

Executed this _______ day of ______________, 20 _____________ |

Signature________________________________________________ |

Print name _______________________________________________ |

Telephone number _______________________________________ |

Mailing address ___________________________________________ |

City/State/ZIP ___________________________________________ |

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

R. 01/21

Page 2 of 2

Instructions for Completing Form

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

General Information

If Florida estate tax is not due and a federal estate tax return (federal Form 706 or

Form

The

Where to File Form

Form

When to Use Form

Form

and a federal estate tax return (federal Form 706 or

Federal thresholds for filing federal Form 706 only: (For informational purposes only. Please confirm with Form 706 instructions.)

Date of Death |

Dollar Threshold |

(year) |

for Filing Form 706 |

|

(value of gross estate) |

|

|

2000 and 2001 |

$675,000 |

|

|

2002 and 2003 |

$1,000,000 |

|

|

2004 and 2005 |

$1,500,000 |

|

|

For 2006 and forward |

|

go to the IRS website at |

|

www.irs.gov to obtain |

|

thresholds. |

|

|

|

For thresholds for filing federal Form

If an administration proceeding is pending for an estate, Form

To Contact Us

Information, forms, and tutorials are available on the Department’s website floridarevenue.com

If you have any questions, or need assistance, call Taxpayer Services at

To find a taxpayer service center near you, go to: floridarevenue.com/taxes/servicecenters

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email when Tax Information Publications and proposed rules are posted to the Department’s website. Subscribe today at floridarevenue.com/dor/subscribe.

Reference Material

Rule Chapter

| Fact Name | Detail |

|---|---|

| Form Title | Affidavit of No Florida Estate Tax Due DR-312 |

| Revision Date | 01/21 |

| Governing Rules | Rule 12C-3.008, F.A.C. (Florida Administrative Code) |

| Governing Law | Chapter 198, Florida Statutes |

| Purpose | To declare that no Florida estate tax is due and a federal estate tax return is not required |

| Who Should File | Personal representatives of estates not subject to Florida estate tax and for which a federal estate tax return is not required |

| Submission Location | Filed with the clerk of the circuit court in the county or counties where the decedent owned property |

| Contact Information | Taxpayer Services - 850-488-6800, floridarevenue.com |

Filling out the FL DR-312 form, known as the Affidavit of No Florida Estate Tax Due, is a requirement for personal representatives or “persons in possession” of estates in Florida when no Florida estate tax is owed and a federal estate tax return is not necessary. This step-by-step guide aims to simplify the process, ensuring that personal representatives can fulfill their obligations accurately and efficiently.

Once completed, the FL DR-312 serves as a crucial document in estate administration, evidencing that no Florida estate tax is due and thereby releasing the estate from the Florida Department of Revenue’s tax lien. Ensure to secure a copy for personal records after filing the form with the relevant court clerk, as it may be needed for future reference or proceedings related to the estate.

Frequently Asked Questions about the Florida Form DR-312

Form DR-312, the Affidavit of No Florida Estate Tax Due, is a document used by personal representatives or individuals in possession of a decedent's property. It attests that there is no Florida estate tax owed by the estate and that a federal estate tax return (Form 706 or 706-NA) is not required to be filed. This form helps remove the Department’s estate tax lien on the decedent's property.

Personal representatives of estates that are not subject to Florida estate tax under Chapter 198, F.S., and do not require a federal estate tax return, should complete and file Form DR-312. This includes any person in actual or constructive possession of any property included in the decedent's gross estate.

Form DR-312 must be filed directly with the clerk of the circuit court in the county or counties where the decedent owned property. It should be filed when an estate is not subject to Florida estate tax and a federal estate tax return is not required. If an estate administration proceeding is pending, this form can be filed as part of that proceeding.

Filers should not use the 3-inch by 3-inch space in the upper right corner of the form, as it is reserved for the clerk of the court. All other sections should be completed based on the detailed instructions provided on the form. This includes the personal representative’s declaration under penalties of perjury that the facts stated in the affidavit are true, based on their knowledge.

Failure to file Form DR-312 when required can result in the Florida estate tax lien not being removed. This can affect the clear transfer or sale of the decedent’s property, as potential buyers or transferees may be unwilling to proceed without clear title.

For more information or assistance, you can call Taxpayer Services at 850-488-6800, visit the Florida Department of Revenue website, or contact a taxpayer service center. Tutorials, additional forms, and contact information for written tax questions are available online for your convenience.

Filling out official forms is crucial, especially when it's the FL DR-312, Affidavit of No Florida Estate Tax Due. This document, seemingly straightforward, has its crevices where errors can hide. To help navigate this task, below are eight common mistakes people often make when completing the form.

Not correctly identifying the personal representative: The form requires the name of the personal representative to be clearly printed. This mistake can create confusion about who is legally handling the estate's affairs.

Incorrect decedent information: Failing to accurately provide the decedent's name or incorrectly stating their domicile can have significant repercussions on the estate's legal and tax implications.

Overlooking the date of death: This is not just any date but a vital piece of information that determines many time-sensitive actions post-death, including tax obligations.

Mishandling the citizenship checkbox: This requires a simple check, but incorrectly identifying the decedent's citizenship status can lead to unwarranted tax complications.

Assuming no federal estate tax return is required without verification: Often, personal representatives may not fully understand when a federal estate tax return is needed, leading to inaccuracies on the form.

Asserting the estate owes no Florida estate tax without proper assessment: Just because an estate is under a certain value or meets specific conditions doesn't automatically exempt it from all taxes.

Not acknowledging personal liability: By signing the document, the personal representative accepts personal liability for the estate's tax obligations— this should not be taken lightly or misunderstood.

Improper submission: The form must be filed with the clerk of the court in the county where the decedent owned property, not mailed to the Florida Department of Revenue. Overlooking or misunderstanding this directive can delay the process.

To prevent these common errors, a careful review of both the form's instructions and the estate's specifics are crucial. Remember, when in doubt, seeking assistance ensures that these essential documents are completed accurately and in compliance with the law.

When handling estate affairs, especially in the state of Florida, it’s important to make sure all paperwork is correctly filled out and duly submitted. Among these forms, the Affidavit of No Florida Estate Tax Due (Form DR-312) is commonly used by personal representatives to declare that a decedent’s estate owes no Florida estate tax. However, this affidavit is just one component of a larger collection of forms and documents often required in estate proceedings. The following list includes additional forms and documents frequently used alongside Form DR-312, each serving a unique purpose in the estate management process.

Navigating the complexities of estate administration requires a keen understanding of required legal documents and procedures. The proper completion and filing of these forms not only facilitates a smoother probate process but also helps ensure that the decedent’s wishes are honored, creditors are paid, and beneficiaries receive their rightful inheritance with minimal delay. Preparing and organizing these documents early can help avoid potential complications and legal hurdles down the road. Nonetheless, given the technical nature and legal implications of these documents, consulting with a legal professional can provide invaluable guidance and peace of mind throughout the process.

The IRS Form 706 (United States Estate (and Generation-Skipping Transfer) Tax Return) is similar to the Florida DR-312 form in that both are used in the context of estate administration to report and determine tax liability. While the DR-312 form is specific to asserting that no Florida estate tax is due, the IRS Form 706 details the federal estate tax obligations of a decedent's estate.

The IRS Form 706-NA (United States Estate (and Generation-Skipping Transfer) Tax Return) for Nonresident Aliens is another form comparable to the DR-312, as it deals with the federal estate tax for estates of nonresident aliens. Just like the DR-312 form ensures compliance with state-level estate tax requirements, Form 706-NA addresses such compliance at the federal level for nonresident aliens.

The Affidavit of Domicile is used to verify the state of residence of a decedent at the time of their death. This is similar to the FL DR-312 form, which also requires disclosure of the decedent's domicile to determine the applicability of Florida estate tax laws.

A Small Estate Affidavit is another document with similar operational functions, designed to facilitate the transfer of estate assets without formal probate in certain circumstances. Although serving a different purpose, it, like the DR-312, plays a crucial role in estate administration by simplifying the process under specified conditions.

The Release of Lien document, often used in real estate transactions and estate settlements, is similar to the DR-312 form to the extent that filing a completed DR-312 can lead to the release of the Florida Department of Revenue’s estate tax lien on a decedent's property.

The Probate Petition initiates the formal legal process of administering a decedent's estate, which may include determining the estate's tax liabilities. While the DR-312 form itself is not a petition, it is an integral part of the probate process regarding tax matters in Florida.

An Inventory and Appraisal form lists the assets of a decedent's estate and their fair market values, which is a vital part of assessing estate tax obligations. Though the DR-312 does not perform this function, it indirectly depends on the outcomes of such inventories to assert that no estate tax is due in Florida.

When filling out the Florida DR-312 form, an Affidavit of No Florida Estate Tax Due, it's important to approach the task with precision to ensure all legal requirements are met. This document is a crucial step in settling an estate when a federal estate tax return is not required and no Florida estate tax is due. The following lists highlight key dos and don'ts to keep in mind.

Dos when filling out the FL DR-312 form:

Don'ts when filling out the FL DR-312 form:

By observing these dos and don'ts, personal representatives can ensure that the FL DR-312 form is filled out correctly, helping to streamline the process of settling an estate in Florida where no estate tax is due.

One common misconception is that the FL DR-312 form must be filed with the Florida Department of Revenue. Actually, this form should be filed directly with the clerk of the circuit court in the county or counties where the decedent owned property, not sent to the Florida Department of Revenue.

Another misunderstanding is that this form is only for use by the formal personal representative of the estate. In reality, the definition of “personal representative” in Chapter 198, F.S., includes any person who is in actual or constructive possession of any property included in the decedent's gross estate. This means that the affidavit can be completed by “persons in possession” of property included in the decedent’s gross estate, expanding its applicability.

Many believe that an Affidavit of No Florida Estate Tax Due DR-312 can be used for any estate, regardless of size. However, it cannot be used for estates that are required to file a federal estate tax return (federal Form 706 or 706-NA), an important distinction based on the value of the estate and federal thresholds.

There's a misconception that the completion and filing of this form are complicated processes. The instructions on the second page of the form provide clear guidance on how to complete and file it, emphasizing its user-friendly nature designed to assist personal representatives in asserting that no Florida estate tax is due without undue hassle.

Some believe that after filing the FL DR-312 form, the personal representative must take additional steps to obtain a “Nontaxable Certificate” from the Florida Department of Revenue. This is inaccurate, as the form itself, once duly filed, serves as evidence of nonliability for Florida estate tax and effectively removes the Department’s estate tax lien, eliminating the need for a Nontaxable Certificate.

Another misconception is that the FL DR-312 form can be used as a substitute for a federal estate tax return when it is, in fact, a distinct document strictly related to Florida estate tax liability. This form asserts that no Florida estate tax is due and a federal estate tax return (federal Form 706 or 706-NA) is not required to be filed, but it does not replace the need for filing federal returns if applicable based on federal laws.

Finally, there is a false notion that filing the FL DR-312 form is optional and merely a formality that does not have significant legal implications. Filing this affidavit is an essential step in the estate administration process in Florida when applicable. It helps to ensure that the estate is properly cleared of Florida estate tax liens, allowing for the proper distribution of the decedent’s assets among heirs or beneficiaries.

Understanding the FL DR 312 form is crucial for personal representatives handling estates in Florida. Here are some key takeaways to ensure its proper use and avoid potential legal hurdles.

Properly completing and filing the FL DR 312 form requires attention to detail and an understanding of both Florida and federal estate tax laws. Personal representatives are encouraged to carefully follow the instructions and, if necessary, seek professional legal guidance to ensure compliance and smooth administrative proceedings for the estate.

Da Form 31 Printable - Addresses terminal leave requests, facilitating the transition of service members from military to civilian life.

California Bbs - The form facilitated a precise calculation of hours dedicated to direct clinical work versus other professional activities, aligning with licensure requirements for clinical social workers.

Lausd Benefits Enrollment - Ensures benefits remain in pending status until official documentation from retirement systems like CalSTRS or CalPERS is received.