Free Gift Letter PDF Template

Free Gift Letter PDF Template

When it comes to receiving financial gifts, particularly those intended to assist with down payments on a home, the importance of documenting this transaction cannot be overstated. This is where a Gift Letter form becomes an essential tool. Serving as a formal declaration, it provides clear evidence that the money received is not a loan but a gift, free from any obligation of repayment. Lenders require this document to ensure that the gift does not covertly inflate the buyer's financial health, potentially misrepresenting their ability to afford the mortgage. The Gift Letter must include specific information: the donor's name, relationship to the recipient, the gift amount, and a clear statement that no repayment is expected or required. Additionally, both the donor and recipient must sign the document, further solidifying its legitimacy. By laying out these details, the Gift Letter form plays a critical role in the home buying process, ensuring transparency and compliance with lender requirements, as well as providing peace of mind to all parties involved.

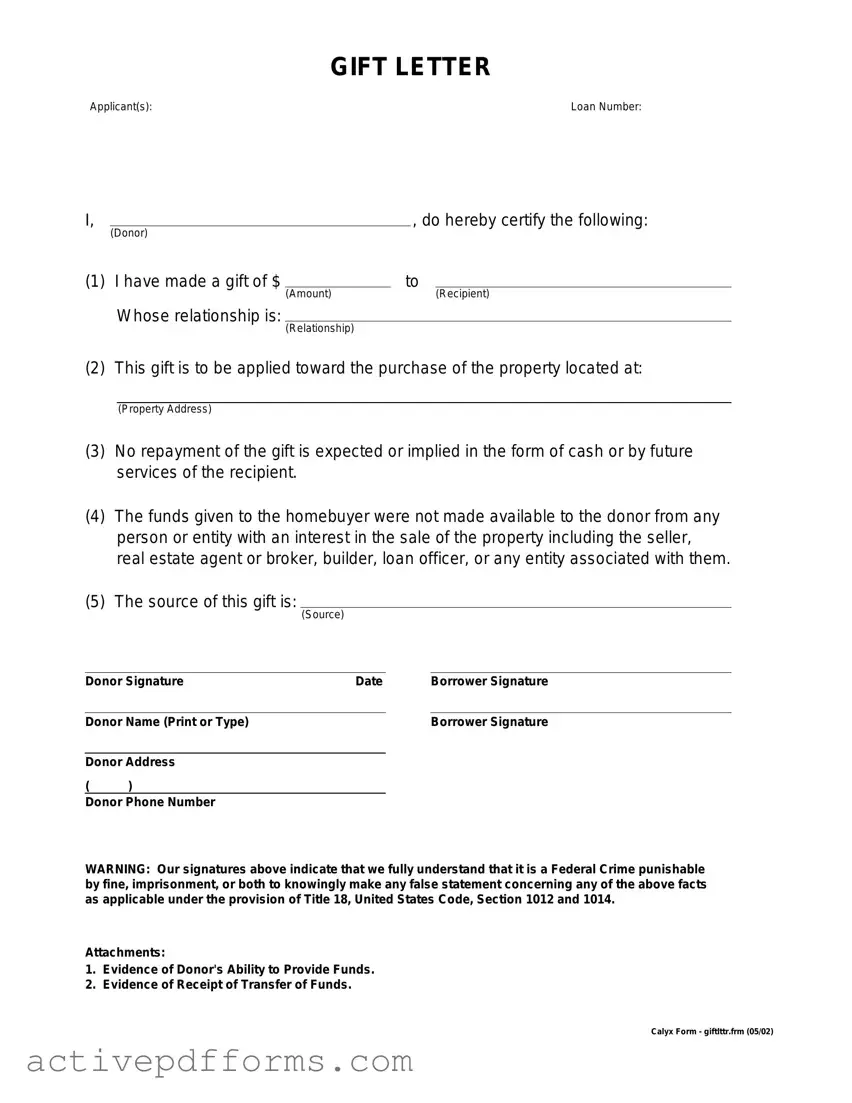

GIFT LETTER

Applicant(s): |

Loan Number: |

I, |

|

|

, do hereby certify the following: |

||

|

(Donor) |

|

|

|

|

(1) I have made a gift of $ |

|

to |

|

||

|

|

(Amount) |

|

|

(Recipient) |

|

Whose relationship is: |

|

|

|

|

|

|

(Relationship) |

|

|

|

(2) This gift is to be applied toward the purchase of the property located at:

(Property Address)

(3)No repayment of the gift is expected or implied in the form of cash or by future services of the recipient.

(4)The funds given to the homebuyer were not made available to the donor from any person or entity with an interest in the sale of the property including the seller, real estate agent or broker, builder, loan officer, or any entity associated with them.

(5)The source of this gift is:

(Source)

Donor Signature |

Date |

Borrower Signature |

||

|

|

|

|

|

Donor Name (Print or Type) |

|

|

Borrower Signature |

|

|

|

|

|

|

Donor Address |

|

|

|

|

( |

) |

|

|

|

Donor Phone Number

WARNING: Our signatures above indicate that we fully understand that it is a Federal Crime punishable by fine, imprisonment, or both to knowingly make any false statement concerning any of the above facts as applicable under the provision of Title 18, United States Code, Section 1012 and 1014.

Attachments:

1.Evidence of Donor's Ability to Provide Funds.

2.Evidence of Receipt of Transfer of Funds.

Calyx Form - giftlttr.frm (05/02)

| Fact Number | Description |

|---|---|

| 1 | A Gift Letter is a document that proves money received by someone was a gift and not a loan. |

| 2 | This form is often used when a gift is made towards the purchase of real estate. |

| 3 | The letter typically states the donor's name, relationship to the recipient, and the gift amount. |

| 4 | It also includes a statement that no repayment is expected or required. |

| 5 | Mortgage lenders usually require a Gift Letter to ensure that the gift does not need to be repaid. |

| 6 | The specific format and content of a Gift Letter can vary by lender and by state. |

| 7 | State laws may impose additional requirements or formalities for the validity of a Gift Letter. |

| 8 | In some states, the letter must be notarized to confirm the identity of the signatory and the authenticity of the letter. |

| 9 | Tax implications for the donor or recipient may arise, necessitating the Gift Letter for documentation. |

| 10 | Even with a Gift Letter, the source of the funds may be scrutinized by lenders to comply with anti-money laundering laws. |

When it comes time to fill out a Gift Letter form, many individuals may find themselves navigating uncharted waters. This document is critical in certain financial transactions, particularly in the context of home buying, where it serves to formally acknowledge that an individual or entity is giving a sum of money to another person without any expectation of repayment. The rationale behind this might be to assist with the down payment or closing costs on a home. Filling out this form accurately and thoroughly is essential to ensuring that the financial gift does not encounter any unnecessary obstacles in its contribution to the recipient's goals.

Steps for Filling Out the Gift Letter Form

Following these steps will lead to the successful completion of the Gift Letter form. This document plays a pivotal role in the financial dynamics of acquiring a home, serving as proof of the recipient's financial backing. With careful attention to detail and clarity, the process of filling out the form can be straightforward and efficient, ensuring the financial gift aids in the joyous occasion of purchasing a home.

What is a Gift Letter Form?

A Gift Letter Form is a document that a donor uses to provide proof that money given to a recipient is indeed a gift and not a loan or an expectation of repayment. It's most commonly required by lenders when someone uses gifted funds for a down payment on a home. The form certifies that the giver has no financial interest in the property being purchased and does not expect the money to be paid back.

Why do I need a Gift Letter?

When you're applying for a mortgage and plan to use a financial gift as part of your down payment, lenders will ask for a Gift Letter. This is to ensure that the gift does not increase your debt obligations, which could impact your ability to repay the mortgage. By confirming the money is a gift, lenders can proceed with an accurate assessment of your financial status.

What information should be included in a Gift Letter?

Who needs to sign the Gift Letter Form?

Only the donor is required to sign the Gift Letter Form to confirm that the details provided are true and accurate. However, some lenders might also request the recipient's signature for their records.

Can I use a template for a Gift Letter?

Yes, you can use a template for a Gift Letter as long as it contains all the necessary information required by your lender. It's important to make sure any template you use complies with your lender's specific requirements. You may also want to consult with your lender beforehand to see if they provide a preferred template.

Is there a difference between a Gift Letter for a mortgage and other types of gifts?

While the fundamental purpose of a Gift Letter is to clarify that funds are a gift and not a loan, a Gift Letter for a mortgage has specific requirements set forth by lenders to meet mortgage application standards. For other types of gifts, a simpler letter might suffice, especially if it’s just for personal records or the amount is below the IRS reporting threshold. Always make sure the Gift Letter meets the criteria for its intended use.

When filling out a Gift Letter form, it's important to pay attention to detail and follow instructions closely. Even small mistakes can lead to delays or issues with the processing of the form. Here are some common errors that individuals often make:

Not specifying the relationship between the donor and the recipient clearly. The exact nature of their relationship should be detailed to avoid any ambiguity.

Failing to provide the exact amount of the gift. It’s crucial to specify the full amount in numbers and words for clarity.

Omitting the date the gift was made. This date is important for various legal and tax reasons.

Forgetting to state that the gift does not need to be repaid. The letter must clearly declare the transfer as a gift.

Not including the donor’s full legal name and contact information. Accurate details ensure the letter is legally binding.

Leaving out the recipient’s full legal name. Like the donor’s details, this information must be exact.

Not specifying the purpose of the gift. For instance, if it’s for the purchase of a home, this should be clearly stated.

Incorrect signing practices, such as the donor not signing the document or using an electronic signature where an ink signature is required.

Lack of witness or notary signatures when required. Some jurisdictions may require these for the document to be valid.

Misunderstanding the tax implications and not consulting a tax professional or attorney. This can lead to unexpected tax liabilities.

Here are some additional tips to consider:

Always double-check the form for completeness and accuracy before submitting.

Ensure the form matches the requirements of the institution or agency it is being submitted to.

Consider consulting with a professional if you have any doubts or questions regarding the form or the process.

When dealing with the nuances of financial transactions, especially those involving gifts of money towards significant purchases like a home, a Gift Letter form often plays a crucial role. However, to ensure the process runs smoothly and complies with all legal and financial requirements, several other forms and documents are frequently necessary to provide alongside a Gift Letter. These documents help in verifying the legitimacy of the gift and the financial status of the involved parties, among other details.

Together, these forms and documents form the backbone of a secure and lawful financial transaction. Each plays a specific role in painting a complete picture of the financial health and intentions of the parties involved. While the Gift Letter clarifies the nature of the funds as a gift, the additional documents ensure that all aspects of the gift, the purchase, and the financial backgrounds of the involved parties are appropriately recorded and reviewed. This comprehensive approach not only facilitates smoother transactions but also adheres to legal and regulatory standards.

Affidavit of Support: This document is akin to a Gift Letter in that it legally verifies an individual's commitment to financially support another person. Like the Gift Letter, it provides pertinent details about the donor or sponsor, including their relationship to the recipient and an assurance of financial support, which is crucial for immigration purposes.

Loan Agreement: Similar to the Gift Letter, a Loan Agreement outlines the terms under which one party lends money to another. Both documents detail the amount of money involved and identify the parties. However, unlike a Gift Letter, a Loan Agreement includes repayment terms, interest rates, and a repayment schedule.

Grant Deed: A Grant Deed is used to transfer ownership of real property and, like the Gift Letter, it specifies the parties involved and the item being transferred. Both documents are formal records that ensure the legal transfer of assets, although a Grant Deed is specifically used for real estate transactions.

Mortgage Gift Letter: This is a specific type of Gift Letter used when gifts of money are given to help someone buy a house. It confirms that the money is a gift and not a loan, detailing the donor and recipient's information, mirroring the Gift Letter's purpose in real estate transactions.

Promissory Note: While primarily used for loans, a Promissory Note shares similarities with a Gift Letter, as it outlines an amount of money to be transferred between parties. However, it differs in its commitment to repayment by the borrower, including interest and repayment terms.

Declaration of Trust: This document is used to state that one person holds property on behalf of another, showing a trust relationship between the parties. Similar to a Gift Letter, it outlines a transfer of assets, but it focuses on the management and control of the assets rather than the transfer itself.

When filling out a Gift Letter form, it's important to follow specific guidelines to ensure the process goes smoothly. Here are some dos and don'ts to keep in mind:

Do's:

Don'ts:

When it comes to gift letters, there are many misconceptions that can cause confusion. A gift letter is a document that proves money received by a homebuyer from a relative or friend is a gift, not a loan. This letter is required by lenders to ensure that the money will not need to be repaid. Below are ten common misconceptions about the gift letter form that need to be clarified.

Any gift amount is acceptable without documentation: Not all gifts require a gift letter, but for significant amounts, especially in relation to home purchases, lenders will require a gift letter to ensure the gift does not need to be repaid.

The gift letter needs to be notarized: This is not always the case. While some lenders might have specific requirements, most do not require the gift letter to be notarized. However, it must be signed by both the giver and the receiver.

A gift letter is only necessary for mortgage applications: While commonly associated with homebuying, gift letters may also be requested by other financial institutions or for other large transactions to prove the financial gift is not a loan.

The gift letter must specify the exact use of the gift: The primary purpose of the letter is to state that the money is a gift and not a loan. Specifying how the gift will be used is not always necessary, though some lenders may require more details for large sums.

Gift letters are only for cash gifts: Gift letters can also document gifts of equity, such as when a family member sells a property to another family member at a price below market value. The difference in value can be considered a gift.

Gift letters can be informal: While the tone can be straightforward, certain information must be included, such as the names of the donor and recipient, the donor's relationship to the recipient, the gift amount, and a statement that no repayment is expected.

The recipient alone can fill out and sign the gift letter: The donor is the one who must provide the gift letter, even though it benefits the recipient, to clearly establish the nature of the gift.

Gift letters are legally binding contracts: A gift letter is a statement of fact, not a contract. It does not legally bind the donor to anything beyond stating that the funds are a gift and not a loan.

Only family members can provide gift letters: Friends and, in some cases, distant relatives can give financial gifts with a gift letter, although lenders may require more information to ensure the gift does not need to be repaid.

The donor’s bank account information is always required: This requirement varies by lender. Some may ask for account statements to verify the donor's ability to give the gift, while others do not.

Dispelling these misconceptions is important for anyone looking to use a gift letter in their financial transactions, as understanding the requirements and expectations can help streamline the process for all parties involved.

Filling out and using a Gift Letter form is an important process in certain financial transactions, particularly in the realm of home buying. When someone receives financial assistance from a family member or friend for a down payment on a house, a Gift Letter form is often required by lenders to document that the funds are indeed a gift and not a loan that needs to be repaid. Here are key takeaways to consider:

Properly completed and documented, a Gift Letter can smooth the way for financial transactions, demonstrating to lenders that the gift does not adversely affect the borrower's financial situation. It is a crucial step in the process of securing a mortgage with the help of gifted funds.

Puppy Shot Record Printable Free - A legally sound document that records a dog’s vaccination schedule, including essential vaccinations from DHPP to Rabies, ensuring public safety.

H&p Medical Abbreviation - Enables meticulous recording of patient health narratives, presenting illness particulars, and thorough systems examination for informed clinical decisions.

Hold Mail Request - Allow USPS to safeguard your mail through this hold request, offering you one less thing to worry about while away.