Free IRS 1023 PDF Template

Free IRS 1023 PDF Template

For many organizations seeking to operate as tax-exempt entities under Section 501(c)(3) of the Internal Revenue Code, the journey begins with the crucial step of completing the IRS 1023 form. This document, often perceived as daunting due to its comprehensive nature, serves as the formal application required for obtaining federal tax-exempt status. It asks for detailed information about the organization's structure, governance, financial data, and its planned activities. The purpose behind the form is to ensure that the organization meets the strict criteria set by the IRS for providing a public benefit and thus, qualifying for exemption from federal income taxes. Completing the form accurately and thoroughly is imperative, as it allows the IRS to evaluate the entity's eligibility. The process can be intricate, involving a thorough examination of the organization's mission, activities, and financial projections to establish its nonprofit bona fides. Organizations must also be prepared to maintain compliance with ongoing regulatory requirements once exempt status is achieved. With tax-exempt status comes the ability to accept tax-deductible donations, a critical component for many nonprofit organizations in achieving their funding goals. Therefore, navigating the application process successfully is a fundamental step for organizations aiming to make a positive impact while ensuring compliance with federal regulations.

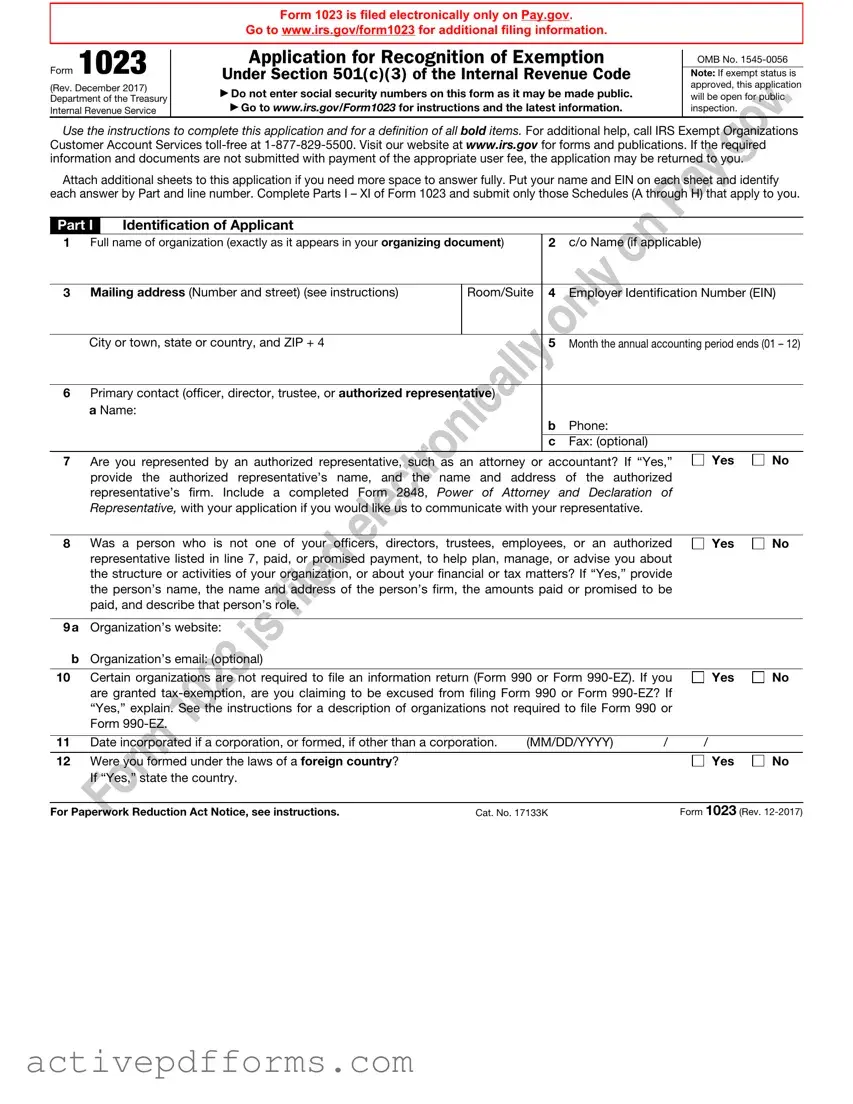

Form 1023 is filed electronically only on Pay.gov.

Go to www.irs.gov/form1023 for additional filing information.

Form 1023

(Rev. December 2017)

Department of the Treasury

Internal Revenue Service

Application for Recognition of Exemption

Under Section 501(c)(3) of the Internal Revenue Code

▶Do not enter social security numbers on this form as it may be made public. ▶ Go to www.irs.gov/Form1023 for instructions and the latest information.

OMB No.

Note: If exempt status is approved, this application will be open for public inspection.

Use the instructions to complete this application and for a definition of all bold items. For additional help, call IRS Exempt Organizations Customer Account Services

Attach additional sheets to this application if you need more space to answer fully. Put your name and EIN on each sheet and identify each answer by Part and line number. Complete Parts I – XI of Form 1023 and submit only those Schedules (A through H) that apply to you.

Part I |

Identification of Applicant |

|

|

|

|

1 |

Full name of organization (exactly as it appears in your organizing document) |

2 |

c/o Name (if applicable) |

||

|

|

|

|

|

|

3 |

Mailing address (Number and street) (see instructions) |

Room/Suite |

4 |

Employer Identification Number (EIN) |

|

|

|

|

|

|

|

|

City or town, state or country, and ZIP + 4 |

|

5 |

Month the annual accounting period ends (01 – 12) |

|

|

|

|

|

||

6 |

Primary contact (officer, director, trustee, or authorized representative) |

|

|

||

|

a Name: |

|

|

|

|

|

|

|

|

b |

Phone: |

|

|

|

|

|

|

|

|

|

|

c |

Fax: (optional) |

7Are you represented by an authorized representative, such as an attorney or accountant? If “Yes,” provide the authorized representative’s name, and the name and address of the authorized representative’s firm. Include a completed Form 2848, Power of Attorney and Declaration of Representative, with your application if you would like us to communicate with your representative.

Yes

No

8Was a person who is not one of your officers, directors, trustees, employees, or an authorized representative listed in line 7, paid, or promised payment, to help plan, manage, or advise you about the structure or activities of your organization, or about your financial or tax matters? If “Yes,” provide the person’s name, the name and address of the person’s firm, the amounts paid or promised to be paid, and describe that person’s role.

Yes

No

9a Organization’s website:

bOrganization’s email: (optional)

10Certain organizations are not required to file an information return (Form 990 or Form

Yes

No

11 |

Date incorporated if a corporation, or formed, if other than a corporation. |

(MM/DD/YYYY) |

/ |

/ |

|

|

12 |

Were you formed under the laws of a foreign country? |

|

|

|

Yes |

No |

|

If “Yes,” state the country. |

|

|

|

|

|

|

|

|

|

|||

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 17133K |

|

Form 1023 (Rev. |

|||

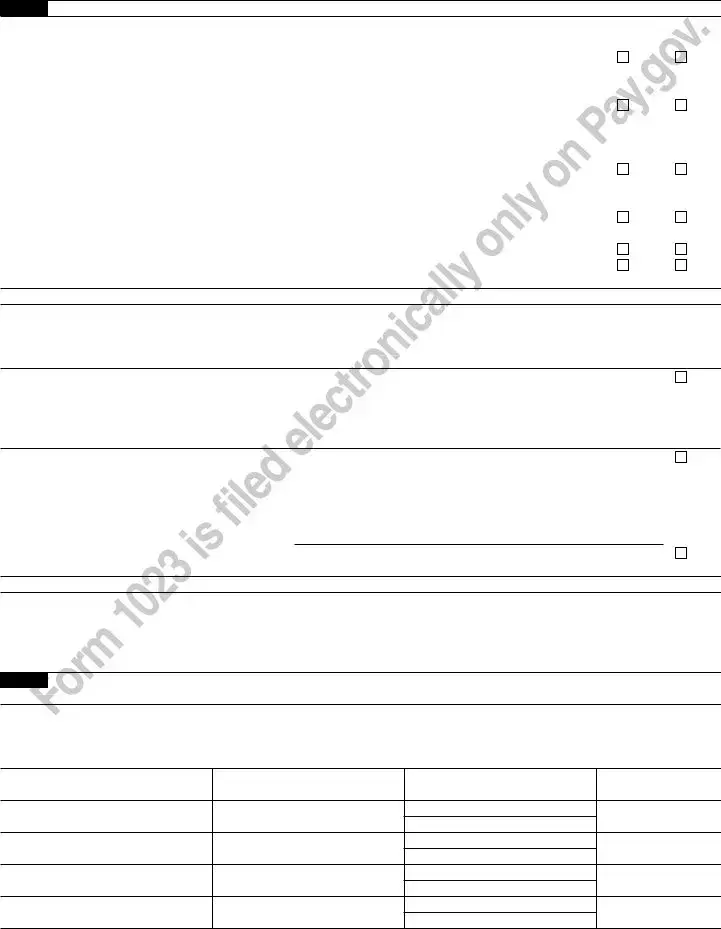

Form 1023 (Rev. |

Name: |

EIN: |

Page 2 |

Part II Organizational Structure

You must be a corporation (including a limited liability company), an unincorporated association, or a trust to be tax exempt.

See instructions. DO NOT file this form unless you can check “Yes” on lines 1, 2, 3, or 4.

1 |

Are you a corporation? If “Yes,” attach a copy of your articles of incorporation showing certification of |

Yes |

No |

|

|

|

filing with the appropriate state agency. Include copies of any amendments to your articles and be sure |

|

|

|

|

they also show state filing certification. |

|

|

|

|

|

|

|

2 |

Are you a limited liability company (LLC)? If “Yes,” attach a copy of your articles of organization showing |

Yes |

No |

|

|

|

certification of filing with the appropriate state agency. Also, if you adopted an operating agreement, attach |

|

|

|

|

a copy. Include copies of any amendments to your articles and be sure they show state filing certification. |

|

|

|

|

Refer to the instructions for circumstances when an LLC should not file its own exemption application. |

|

|

|

|

|

|

|

3 |

Are you an unincorporated association? If “Yes,” attach a copy of your articles of association, |

Yes |

No |

|

|

|

constitution, or other similar organizing document that is dated and includes at least two signatures. |

|

|

|

|

Include signed and dated copies of any amendments. |

|

|

|

|

|

|

|

|

4a |

Are you a trust? If “Yes,” attach a signed and dated copy of your trust agreement. Include signed and |

Yes |

No |

|

|

dated copies of any amendments. |

|

|

|

b |

Have you been funded? If “No,” explain how you are formed without anything of value placed in trust. |

Yes |

No |

|

5 |

Have you adopted bylaws? If “Yes,” attach a current copy showing date of adoption. If “No,” explain |

Yes |

No |

|

|

how your officers, directors, or trustees are selected. |

|

|

Part III Required Provisions in Your Organizing Document

The following questions are designed to ensure that when you file this application, your organizing document contains the required provisions to meet the organizational test under section 501(c)(3). Unless you can check the boxes in both lines 1 and 2, your organizing document does not meet the organizational test. DO NOT file this application until you have amended your organizing document. Submit your original and amended organizing documents (showing state filing certification if you are a corporation or an LLC) with your application.

1Section 501(c)(3) requires that your organizing document state your exempt purpose(s), such as charitable, religious, educational, and/or scientific purposes. Check the box to confirm that your organizing document meets this requirement. Describe specifically where your organizing document meets this requirement, such as a reference to a particular article or section in your organizing document. Refer to the instructions for exempt purpose language.

Location of Purpose Clause (Page, Article, and Paragraph):

2 a Section 501(c)(3) requires that upon dissolution of your organization, your remaining assets must be used exclusively for exempt purposes, such as charitable, religious, educational, and/or scientific purposes. Check the box on line 2a to confirm that your organizing document meets this requirement by express provision for the distribution of assets upon dissolution. If you rely on state law for your dissolution provision, do not check the box on line 2a and go to line 2c.

bIf you checked the box on line 2a, specify the location of your dissolution clause (Page, Article, and Paragraph). Do not complete line 2c if you checked box 2a.

c See the instructions for information about the operation of state law in your particular state. Check this box if you rely on operation of state law for your dissolution provision and indicate the state:

Part IV |

Narrative Description of Your Activities |

Using an attachment, describe your past, present, and planned activities in a narrative. If you believe that you have already provided some of this information in response to other parts of this application, you may summarize that information here and refer to the specific parts of the application for supporting details. You may also attach representative copies of newsletters, brochures, or similar documents for supporting details to this narrative. Remember that if this application is approved, it will be open for public inspection. Therefore, your narrative description of activities should be thorough and accurate. Refer to the instructions for information that must be included in your description.

Part V Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees, Employees, and Independent Contractors

1a List the names, titles, and mailing addresses of all of your officers, directors, and trustees. For each person listed, state their total annual compensation, or proposed compensation, for all services to the organization, whether as an officer, employee, or other position. Use actual figures, if available. Enter “none” if no compensation is or will be paid. If additional space is needed, attach a separate sheet. Refer to the instructions for information on what to include as compensation.

Name

Title

Mailing address

Compensation amount (annual actual or estimated)

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

Page 3 |

|

Part V |

Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees, Employees, |

|||

|

and Independent Contractors (Continued) |

|

|

|

bList the names, titles, and mailing addresses of each of your five highest compensated employees who receive or will receive compensation of more than $50,000 per year. Use the actual figure, if available. Refer to the instructions for information on what to include as compensation. Do not include officers, directors, or trustees listed in line 1a.

Name

Title

Mailing address

Compensation amount (annual actual or estimated)

cList the names, names of businesses, and mailing addresses of your five highest compensated independent contractors that receive or will receive compensation of more than $50,000 per year. Use the actual figure, if available. Refer to the instructions for information on what to include as compensation.

Name

Title

Mailing address

Compensation amount (annual actual or estimated)

The following “Yes” or “No” questions relate to past, present, or planned relationships, transactions, or agreements with your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed in lines 1a, 1b, and 1c.

2a |

Are any of your officers, directors, or trustees related to each other through family or business |

Yes |

No |

|

relationships? If “Yes,” identify the individuals and explain the relationship. |

|

|

b |

Do you have a business relationship with any of your officers, directors, or trustees other than through |

Yes |

No |

|

their position as an officer, director, or trustee? If “Yes,” identify the individuals and describe the business |

|

|

|

relationship with each of your officers, directors, or trustees. |

|

|

c |

Are any of your officers, directors, or trustees related to your highest compensated employees or highest |

Yes |

No |

|

compensated independent contractors listed on lines 1b or 1c through family or business relationships? If |

|

|

|

“Yes,” identify the individuals and explain the relationship. |

|

|

|

|

|

|

3 a |

For each of your officers, directors, trustees, highest compensated employees, and highest |

|

|

|

compensated independent contractors listed on lines 1a, 1b, or 1c, attach a list showing their name, |

|

|

|

qualifications, average hours worked, and duties. |

|

|

b |

Do any of your officers, directors, trustees, highest compensated employees, and highest compensated |

Yes |

No |

|

independent contractors listed on lines 1a, 1b, or 1c receive compensation from any other organizations, |

|

|

|

whether tax exempt or taxable, that are related to you through common control? If “Yes,” identify the |

|

|

|

individuals, explain the relationship between you and the other organization, and describe the |

|

|

|

compensation arrangement. |

|

|

4In establishing the compensation for your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed on lines 1a, 1b, and 1c, the following practices are recommended, although they are not required to obtain exemption. Answer “Yes” to all the practices you use.

a |

Do you or will the individuals that approve compensation arrangements follow a conflict of interest policy? |

Yes |

No |

b |

Do you or will you approve compensation arrangements in advance of paying compensation? |

Yes |

No |

c |

Do you or will you document in writing the date and terms of approved compensation arrangements? |

Yes |

No |

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

Page 4 |

|

Part V |

Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees, Employees, |

|||

|

and Independent Contractors (Continued) |

|

|

|

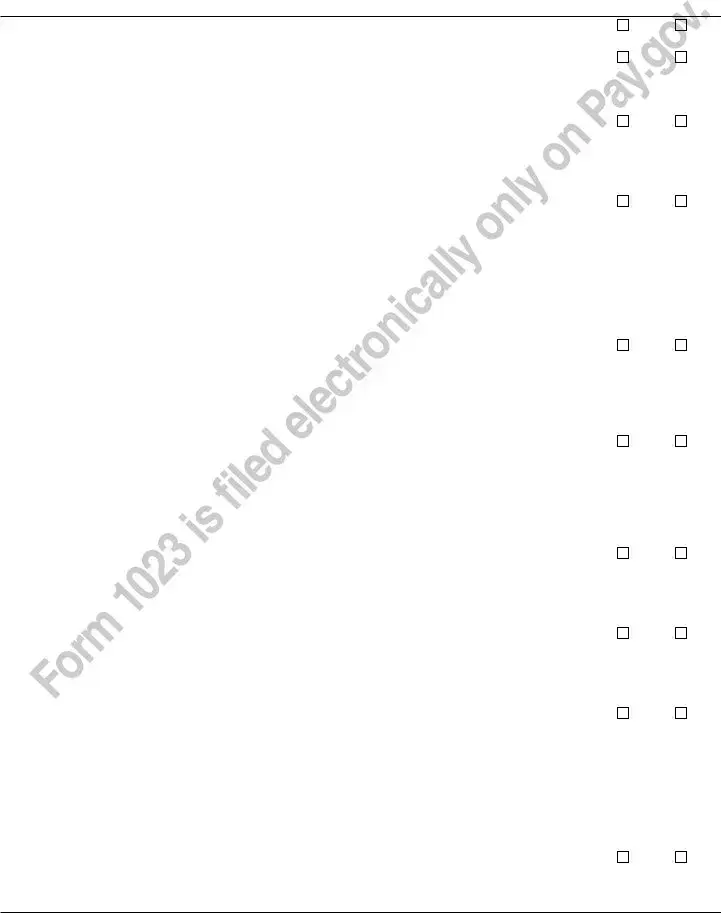

dDo you or will you record in writing the decision made by each individual who decided or voted on compensation arrangements?

eDo you or will you approve compensation arrangements based on information about compensation paid by similarly situated taxable or

Yes |

No |

Yes |

No |

f Do you or will you record in writing both the information on which you relied to base your decision and its |

Yes |

No |

source? |

|

|

gIf you answered “No” to any item on lines 4a through 4f, describe how you set compensation that is reasonable for your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed in Part V, lines 1a, 1b, and 1c.

5a Have you adopted a conflict of interest policy consistent with the sample conflict of interest policy in |

Yes |

No |

Appendix A to the instructions? If “Yes,” provide a copy of the policy and explain how the policy has |

|

|

been adopted, such as by resolution of your governing board. If “No,” answer lines 5b and 5c. |

|

|

bWhat procedures will you follow to assure that persons who have a conflict of interest will not have influence over you for setting their own compensation?

cWhat procedures will you follow to assure that persons who have a conflict of interest will not have influence over you regarding business deals with themselves?

Note: A conflict of interest policy is recommended though it is not required to obtain exemption. Hospitals, see Schedule C, Section I, line 14.

6a |

Do you or will you compensate any of your officers, directors, trustees, highest compensated employees, and highest |

Yes |

No |

|

compensated independent contractors listed in lines 1a, 1b, or 1c through |

|

|

|

bonuses or |

|

|

|

amounts are determined, who is eligible for such arrangements, whether you place a limitation on total compensation, |

|

|

|

and how you determine or will determine that you pay no more than reasonable compensation for services. Refer to |

|

|

|

the instructions for Part V, lines 1a, 1b, and 1c, for information on what to include as compensation. |

|

|

b |

Do you or will you compensate any of your employees, other than your officers, directors, trustees, or your |

Yes |

No |

|

five highest compensated employees who receive or will receive compensation of more than $50,000 per |

|

|

|

year, through |

|

|

|

describe all |

|

|

|

is or will be eligible for such arrangements, whether you place or will place a limitation on total compensation, |

|

|

|

and how you determine or will determine that you pay no more than reasonable compensation for services. |

|

|

|

Refer to the instructions for Part V, lines 1a, 1b, and 1c, for information on what to include as compensation. |

|

|

|

|

|

|

7a |

Do you or will you purchase any goods, services, or assets from any of your officers, directors, trustees, highest |

Yes |

No |

|

compensated employees, or highest compensated independent contractors listed in lines 1a, 1b, or 1c? If “Yes,” |

|

|

|

describe any such purchase that you made or intend to make, from whom you make or will make such purchases, how |

|

|

|

the terms are or will be negotiated at arm’s length, and explain how you determine or will determine that you pay no |

|

|

|

more than fair market value. Attach copies of any written contracts or other agreements relating to such purchases. |

|

|

b |

Do you or will you sell any goods, services, or assets to any of your officers, directors, trustees, highest |

Yes |

No |

|

compensated employees, or highest compensated independent contractors listed in lines 1a, 1b, or 1c? If “Yes,” |

|

|

|

describe any such sales that you made or intend to make, to whom you make or will make such sales, how the |

|

|

|

terms are or will be negotiated at arm’s length, and explain how you determine or will determine you are or will be |

|

|

|

paid at least fair market value. Attach copies of any written contracts or other agreements relating to such sales. |

|

|

|

|

|

|

8a |

Do you or will you have any leases, contracts, loans, or other agreements with your officers, directors, |

Yes |

No |

|

trustees, highest compensated employees, or highest compensated independent contractors listed in |

|

|

lines 1a, 1b, or 1c? If “Yes,” provide the information requested in lines 8b through 8f.

bDescribe any written or oral arrangements that you made or intend to make.

cIdentify with whom you have or will have such arrangements.

dExplain how the terms are or will be negotiated at arm’s length.

eExplain how you determine you pay no more than fair market value or you are paid at least fair market value. f Attach copies of any signed leases, contracts, loans, or other agreements relating to such arrangements.

9a Do you or will you have any leases, contracts, loans, or other agreements with any organization in which |

Yes |

No |

any of your officers, directors, or trustees are also officers, directors, or trustees, or in which any individual officer, director, or trustee owns more than a 35% interest? If “Yes,” provide the information requested in lines 9b through 9f.

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

Page 5 |

|

Part V |

Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees, |

|

||

|

Employees, and Independent Contractors (Continued) |

|

|

|

bDescribe any written or oral arrangements you made or intend to make.

cIdentify with whom you have or will have such arrangements.

dExplain how the terms are or will be negotiated at arm’s length.

eExplain how you determine or will determine you pay no more than fair market value or that you are paid at least fair market value.

fAttach a copy of any signed leases, contracts, loans, or other agreements relating to such arrangements.

Part VI |

Your Members and Other Individuals and Organizations That Receive Benefits From You |

The following “Yes” or “No” questions relate to goods, services, and funds you provide to individuals and organizations as part of your activities. Your answers should pertain to past, present, and planned activities. See instructions.

1 a In carrying out your exempt purposes, do you provide goods, services, or funds to individuals? If “Yes,” describe each program that provides goods, services, or funds to individuals.

bIn carrying out your exempt purposes, do you provide goods, services, or funds to organizations? If “Yes,” describe each program that provides goods, services, or funds to organizations.

Yes |

No |

Yes |

No |

2 |

Do any of your programs limit the provision of goods, services, or funds to a specific individual or group |

Yes |

No |

|

|

of specific individuals? For example, answer “Yes,” if goods, services, or funds are provided only for a |

|

|

|

|

particular individual, your members, individuals who work for a particular employer, or graduates of a |

|

|

|

|

particular school. If “Yes,” explain the limitation and how recipients are selected for each program. |

|

|

|

|

|

|

|

|

3 |

Do any individuals who receive goods, services, or funds through your programs have a family or |

Yes |

No |

|

|

business relationship with any officer, director, trustee, or with any of your highest compensated |

|

|

|

|

employees or highest compensated independent contractors listed in Part V, lines 1a, 1b, and 1c? If |

|

|

|

|

“Yes,” explain how these related individuals are eligible for goods, services, or funds. |

|

|

|

|

|

|

|

|

Part VII |

Your History |

|

|

|

The following “Yes” or “No” questions relate to your history. See instructions.

1 |

Are you a successor to another organization? Answer “Yes,” if you have taken or will take over the |

Yes |

No |

||

|

|

activities of another organization; you took over 25% or more of the fair market value of the net assets of |

|

|

|

|

|

another organization; or you were established upon the conversion of an organization from |

|

|

|

|

|

nonprofit status. If “Yes,” complete Schedule G. |

|

|

|

|

|

|

|

||

|

2 |

Are you submitting this application more than 27 months after the end of the month in which you were |

Yes |

No |

|

|

|

legally formed? If “Yes,” complete Schedule E. |

|

|

|

|

|

|

|

|

|

|

Part VIII |

Your Specific Activities |

|

|

|

The following “Yes” or “No” questions relate to specific activities that you may conduct. Check the appropriate box. Your answers should pertain to past, present, and planned activities. See instructions.

1 Do you support or oppose candidates in political campaigns in any way? If “Yes,” explain. |

Yes |

No |

|

2 a |

Do you attempt to influence legislation? If “Yes,” explain how you attempt to influence legislation and |

Yes |

No |

|

complete line 2b. If “No,” go to line 3a. |

|

|

b |

Have you made or are you making an election to have your legislative activities measured by |

Yes |

No |

|

expenditures by filing Form 5768? If “Yes,” attach a copy of the Form 5768 that was already filed or |

|

|

|

attach a completed Form 5768 that you are filing with this application. If “No,” describe whether your |

|

|

|

attempts to influence legislation are a substantial part of your activities. Include the time and money |

|

|

|

spent on your attempts to influence legislation as compared to your total activities. |

|

|

3a Do you or will you operate bingo or gaming activities? If “Yes,” describe who conducts them, and list all revenue received or expected to be received and expenses paid or expected to be paid in operating these activities. Revenue and expenses should be provided for the time periods specified in Part IX, Financial Data.

bDo you or will you enter into contracts or other agreements with individuals or organizations to conduct bingo or gaming for you? If “Yes,” describe any written or oral arrangements that you made or intend to make, identify with whom you have or will have such arrangements, explain how the terms are or will be negotiated at arm’s length, and explain how you determine or will determine you pay no more than fair market value or you will be paid at least fair market value. Attach copies or any written contracts or other agreements relating to such arrangements.

cList the states and local jurisdictions, including Indian Reservations, in which you conduct or will conduct gaming or bingo.

Yes |

No |

Yes |

No |

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

|

Page 6 |

|

Part VIII |

Your Specific Activities (Continued) |

|

|

|

|

4 a Do |

you or will you undertake fundraising? If “Yes,” check all the fundraising programs you do or will |

Yes |

No |

||

conduct. See instructions. |

|

|

|

||

|

mail solicitations |

|

phone solicitations |

|

|

|

email solicitations |

|

accept donations on your website |

|

|

|

personal solicitations |

receive donations from another organization’s website |

|

||

|

vehicle, boat, plane, or similar donations |

government grant solicitations |

|

|

|

|

foundation grant solicitations |

Other |

|

|

|

Attach a description of each fundraising program.

b Do you or will you have written or oral contracts with any individuals or organizations to raise funds for |

Yes |

No |

you? If “Yes,” describe these activities. Include all revenue and expenses from these activities and state |

|

|

who conducts them. Revenue and expenses should be provided for the time periods specified in Part IX, |

|

|

Financial Data. Also, attach a copy of any contracts or agreements. |

|

|

c Do you or will you engage in fundraising activities for other organizations? If “Yes,” describe these |

Yes |

No |

arrangements. Include a description of the organizations for which you raise funds and attach copies of |

|

|

all contracts or agreements. |

|

|

dList all states and local jurisdictions in which you conduct fundraising. For each state or local jurisdiction listed, specify whether you fundraise for your own organization, you fundraise for another organization, or another organization fundraises for you.

e |

Do you or will you maintain separate accounts for any contributor under which the contributor has the |

Yes |

No |

|

right to advise on the use or distribution of funds? Answer “Yes” if the donor may provide advice on the |

|

|

|

types of investments, distributions from the types of investments, or the distribution from the donor’s |

|

|

|

contribution account. If “Yes,” describe this program, including the type of advice that may be provided |

|

|

|

and submit copies of any written materials provided to donors. |

|

|

|

|

|

|

5 |

Are you affiliated with a governmental unit? If “Yes,” explain. |

Yes |

No |

6a |

Do you or will you engage in economic development? If “Yes,” describe your program. |

Yes |

No |

bDescribe in full who benefits from your economic development activities and how the activities promote exempt purposes.

7a |

Do or will persons other than your employees or volunteers develop your facilities? If “Yes,” describe |

Yes |

No |

|

each facility, the role of the developer, and any business or family relationship(s) between the developer |

|

|

|

and your officers, directors, or trustees. |

|

|

b |

Do or will persons other than your employees or volunteers manage your activities or facilities? If “Yes,” |

Yes |

No |

|

describe each activity and facility, the role of the manager, and any business or family relationship(s) |

|

|

|

between the manager and your officers, directors, or trustees. |

|

|

cIf there is a business or family relationship between any manager or developer and your officers, directors, or trustees, identify the individuals, explain the relationship, describe how contracts are negotiated at arm’s length so that you pay no more than fair market value, and submit a copy of any contracts or other agreements.

8 Do you or will you enter into joint ventures, including partnerships or limited liability companies |

Yes |

No |

treated as partnerships, in which you share profits and losses with partners other than section 501(c)(3) |

|

|

organizations? If “Yes,” describe the activities of these joint ventures in which you participate. |

|

|

9a Are you applying for exemption as a childcare organization under section 501(k)? If “Yes,” answer lines 9b through 9d. If “No,” go to line 10.

bDo you provide childcare so that parents or caretakers of children you care for can be gainfully employed (see instructions)? If “No,” explain how you qualify as a childcare organization described in section 501(k).

Yes |

No |

Yes |

No |

cOf the children for whom you provide childcare, are 85% or more of them cared for by you to enable their parents or caretakers to be gainfully employed (see instructions)? If “No,” explain how you qualify as a childcare organization described in section 501(k).

dAre your services available to the general public? If “No,” describe the specific group of people for whom your activities are available. Also, see the instructions and explain how you qualify as a childcare organization described in section 501(k).

Yes |

No |

Yes |

No |

10 Do you or will you publish, own, or have rights in music, literature, tapes, artworks, choreography, |

Yes |

No |

scientific discoveries, or other intellectual property? If “Yes,” explain. Describe who owns or will own any copyrights, patents, or trademarks, whether fees are or will be charged, how the fees are determined, and how any items are or will be produced, distributed, and marketed.

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

|

Page 7 |

||

Part VIII |

Your Specific Activities (Continued) |

|

|

|

||

11 |

Do you or will you accept contributions of: real property; conservation easements; closely held |

Yes |

No |

|||

|

securities; intellectual property such as patents, trademarks, and copyrights; works of music or art; |

|

|

|||

|

licenses; royalties; automobiles, boats, planes, or other vehicles; or collectibles of any type? If “Yes,” |

|

|

|||

|

describe each type of contribution, any conditions imposed by the donor on the contribution, and any |

|

|

|||

|

agreements with the donor regarding the contribution. |

|

|

|

||

12 a |

Do you or will you operate in a foreign country or countries? If “Yes,” answer lines 12b through 12d. If |

Yes |

No |

|||

|

“No,” go to line 13a. |

|

|

|

|

|

b |

Name the foreign countries and regions within the countries in which you operate. |

|

|

|

||

c |

Describe your operations in each country and region in which you operate. |

|

|

|

||

d |

Describe how your operations in each country and region further your exempt purposes. |

|

|

|

||

|

|

|

|

|||

13a |

Do you or will you make grants, loans, or other distributions to organization(s)? If “Yes,” answer lines 13b |

Yes |

No |

|||

|

through 13g. If “No,” go to line 14a. |

|

|

|

||

bDescribe how your grants, loans, or other distributions to organizations further your exempt purposes.

c Do you have written contracts with each of these organizations? If “Yes,” attach a copy of each contract. |

Yes |

No |

dIdentify each recipient organization and any relationship between you and the recipient organization.

eDescribe the records you keep with respect to the grants, loans, or other distributions you make.

fDescribe your selection process, including whether you do any of the following.

(i) |

Do you require an application form? If “Yes,” attach a copy of the form. |

Yes |

No |

(ii) |

Do you require a grant proposal? If “Yes,” describe whether the grant proposal specifies your |

Yes |

No |

|

responsibilities and those of the grantee, obligates the grantee to use the grant funds only for the |

|

|

|

purposes for which the grant was made, provides for periodic written reports concerning the use of |

|

|

|

grant funds, requires a final written report and an accounting of how grant funds were used, and |

|

|

|

acknowledges your authority to withhold and/or recover grant funds in case such funds are, or appear |

|

|

|

to be, misused. |

|

|

gDescribe your procedures for oversight of distributions that assure you the resources are used to further your exempt purposes, including whether you require periodic and final reports on the use of resources.

14 a Do you or will you make grants, loans, or other distributions to foreign organizations? If “Yes,” answer lines 14b through 14f. If “No,” go to line 15.

bProvide the name of each foreign organization, the country and regions within a country in which each foreign organization operates, and describe any relationship you have with each foreign organization.

cDoes any foreign organization listed in line 14b accept contributions earmarked for a specific country or specific organization? If “Yes,” list all earmarked organizations or countries.

dDo your contributors know that you have ultimate authority to use contributions made to you at your discretion for purposes consistent with your exempt purposes? If “Yes,” describe how you relay this information to contributors.

eDo you or will you make

fDo you or will you use any additional procedures to ensure that your distributions to foreign organizations are used in furtherance of your exempt purposes? If “Yes,” describe these procedures, including site visits by your employees or compliance checks by impartial experts, to verify that grant funds are being used appropriately.

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Form 1023 (Rev.

|

Form 1023 (Rev. |

Name: |

EIN: |

|

Page 8 |

||

|

Part VIII |

Your Specific Activities (Continued) |

|

|

|

||

15 |

Do you have a close connection with any organizations? If “Yes,” explain. |

|

Yes |

No |

|||

|

16 |

Are you applying for exemption as a cooperative hospital service organization under section 501(e)? If |

Yes |

No |

|||

|

|

“Yes,” explain. |

|

|

|

|

|

|

|

|

|

|

|||

17 |

Are you applying for exemption as a cooperative service organization of operating educational |

Yes |

No |

||||

|

|

organizations under section 501(f)? If “Yes,” explain. |

|

|

|

||

|

|

|

|

||||

|

18 |

Are you applying for exemption as a charitable risk pool under section 501(n)? If “Yes,” explain. |

Yes |

No |

|||

|

19 |

Do you or will you operate a school? If “Yes,” complete Schedule B. Answer “Yes,” whether you operate |

Yes |

No |

|||

|

|

a school as your main function or as a secondary activity. |

|

|

|

||

|

|

|

|

||||

|

20 |

Is your main function to provide hospital or medical care? If “Yes,” complete Schedule C. |

Yes |

No |

|||

|

21 |

Do you or will you provide |

Yes |

No |

|||

|

|

complete Schedule F. |

|

|

|

|

|

|

|

|

|

|

|||

22 |

Do you or will you provide scholarships, fellowships, educational loans, or other educational grants to |

Yes |

No |

||||

|

|

individuals, including grants for travel, study, or other similar purposes? If “Yes,” complete |

Schedule H. |

|

|

||

Note: Private foundations may use Schedule H to request advance approval of individual grant procedures.

Form 1023 (Rev.

Form 1023 (Rev. |

Name: |

EIN: |

Page 9 |

|

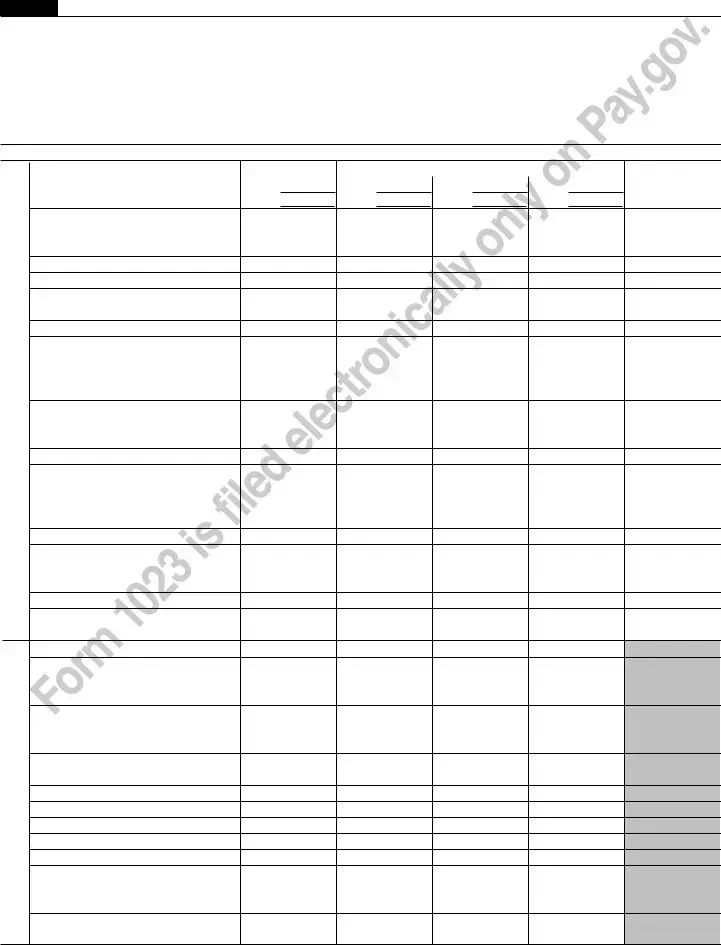

Part IX |

Financial Data |

|

|

|

For purposes of this schedule, years in existence refer to completed tax years.

1.If in existence less than 5 years, complete the statement for each year in existence and provide projections of your likely revenues and expenses based on a reasonable and good faith estimate of your future finances for a total of:

a.Three years of financial information if you have not completed one tax year, or

b.Four years of financial information if you have completed one tax year. See instructions.

2.If in existence 5 or more years, complete the schedule for the most recent 5 tax years. You will need to provide a separate statement that includes information about the most recent 5 tax years because the data table in Part IX has not been updated to provide for a 5th year. See instructions.

A.Statement of Revenues and Expenses

Revenues

Expenses

Type of revenue or expense |

Current tax year |

|

3 prior tax years or 2 succeeding tax years |

|

|

|

|

|

|

|

|

|

(a) From |

(b) From |

(c) From |

(d) From |

(e) Provide Total for |

|

To |

To |

To |

To |

(a) through (d) |

1Gifts, grants, and contributions received (do not include unusual grants)

2Membership fees received

3Gross investment income

4Net unrelated business income

5Taxes levied for your benefit

6Value of services or facilities furnished by a governmental unit without charge (not including the value of services generally furnished to the public without charge)

7Any revenue not otherwise listed above or in lines

8Total of lines 1 through 7

9Gross receipts from admissions, merchandise sold or services performed, or furnishing of facilities in any activity that is related to your exempt purposes (attach itemized list)

10Total of lines 8 and 9

11Net gain or loss on sale of capital assets (attach schedule and see instructions)

12Unusual grants

13Total Revenue

Add lines 10 through 12

14 Fundraising expenses

15Contributions, gifts, grants, and similar amounts paid out (attach an itemized list)

16Disbursements to or for the benefit of members (attach an itemized list)

17Compensation of officers, directors, and trustees

18 Other salaries and wages

19 Interest expense

20 Occupancy (rent, utilities, etc.)

21 Depreciation and depletion

22 Professional fees

23Any expense not otherwise classified, such as program services (attach itemized list)

24Total Expenses

Add lines 14 through 23

Form 1023 (Rev.

|

Form 1023 (Rev. |

Name: |

EIN: |

|

|

Page 10 |

||

|

Part IX |

Financial Data (Continued) |

|

|

|

|

||

|

|

|

|

B. Balance Sheet (for your most recently completed tax year) |

|

|

Year End: |

|

|

|

|

|

Assets |

|

|

(Whole dollars) |

|

1 |

Cash |

1 |

|

|

||||

2 |

Accounts receivable, net |

2 |

|

|

||||

3 |

Inventories |

3 |

|

|

||||

4 |

Bonds and notes receivable (attach an itemized list) |

4 |

|

|

||||

5 |

Corporate stocks (attach an itemized list) |

5 |

|

|

||||

6 |

Loans receivable (attach an itemized list) |

6 |

|

|

||||

7 |

Other investments (attach an itemized list) |

7 |

|

|

||||

8 |

Depreciable and depletable assets (attach an itemized list) |

8 |

|

|

||||

9 |

Land |

9 |

|

|

||||

10 |

Other assets (attach an itemized list) |

10 |

|

|

||||

11 |

Total Assets (add lines 1 through 10) |

11 |

|

|

||||

|

|

|

|

Liabilities |

|

|

|

|

12 |

Accounts payable |

12 |

|

|

||||

13 |

Contributions, gifts, grants, etc. payable |

13 |

|

|

||||

14 |

Mortgages and notes payable (attach an itemized list) |

14 |

|

|

||||

15 |

Other liabilities (attach an itemized list) |

15 |

|

|

||||

16 |

Total Liabilities (add lines 12 through 15) |

16 |

|

|

||||

|

|

|

|

Fund Balances or Net Assets |

|

|

|

|

17 |

Total fund balances or net assets |

17 |

|

|

||||

18 |

Total Liabilities and Fund Balances or Net Assets (add lines 16 and 17) |

18 |

|

|

||||

|

19 |

Have there been any substantial changes in your assets or liabilities since the end of the period |

|

Yes |

No |

|||

|

|

shown above? If “Yes,” explain. |

|

|

|

|

||

Part X Public Charity Status

Part X is designed to classify you as an organization that is either a private foundation or a public charity. Public charity status is a more favorable tax status than private foundation status. If you are a private foundation, Part X is designed to further determine whether you are a private operating foundation. See instructions.

|

1 a |

Are you a private foundation? If “Yes,” go to line 1b. If “No,” go to line 5 and proceed as instructed. If you |

Yes |

No |

|

|

are unsure, see the instructions. |

|

|

|

b |

As a private foundation, section 508(e) requires special provisions in your organizing document in |

|

|

|

|

addition to those that apply to all organizations described in section 501(c)(3). Check the box to confirm |

|

|

|

|

that your organizing document meets this requirement, whether by express provision or by reliance on |

|

|

|

|

operation of state law. Attach a statement that describes specifically where your organizing document |

|

|

|

|

meets this requirement, such as a reference to a particular article or section in your organizing document |

|

|

|

|

or by operation of state law. See the instructions, including Appendix B, for information about the special |

|

|

|

|

provisions that need to be contained in your organizing document. Go to line 2. |

|

|

|

|

|

|

|

|

2 |

Are you a private operating foundation? To be a private operating foundation you must engage directly in |

Yes |

No |

|

|

the active conduct of charitable, religious, educational, and similar activities, as opposed to indirectly |

|

|

|

|

carrying out these activities by providing grants to individuals or other organizations. If “Yes,” go to line 3. |

|

|

|

|

If “No,” go to the signature section of Part XI. |

|

|

|

|

|

|

|

3 |

Have you existed for one or more years? If “Yes,” attach financial information showing that you are a |

Yes |

No |

|

|

|

private operating foundation; go to the signature section of Part XI. If “No,” continue to line 4. |

|

|

|

|

|

|

|

|

4 |

Have you attached either (1) an affidavit or opinion of counsel, (including a written affidavit or opinion |

Yes |

No |

|

|

from a certified public accountant or accounting firm with expertise regarding this tax law matter), that |

|

|

|

|

sets forth facts concerning your operations and support to demonstrate that you are likely to satisfy the |

|

|

|

|

requirements to be classified as a private operating foundation; or (2) a statement describing your |

|

|

|

|

proposed operations as a private operating foundation? |

|

|

5If you answered “No” to line 1a, indicate the type of public charity status you are requesting by checking one of the choices below. You may check only one box.

The organization is not a private foundation because it is:

a 509(a)(1) and

c509(a)(1) and

d

Form 1023 (Rev.

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS 1023 form is used by nonprofit organizations to apply for tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. |

| Eligibility | Organizations that are organized and operated exclusively for religious, charitable, scientific, literary, or educational purposes may qualify. |

| Length of Process | The review process for the IRS 1023 form can take between 3 to 12 months, depending on the complexity of the application and the IRS's backlog. |

| User Fee | There is a user fee associated with the IRS 1023 form, which varies depending on the organization's gross receipts. Smaller organizations may qualify for a reduced fee by filing Form 1023-EZ. |

Filling out the IRS 1023 form is an important step for organizations seeking to gain tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. This process might seem complex at first, but breaking it down into manageable steps can help simplify it. It's not just about filling out the form; it's about understanding the implications of each answer and ensuring that your organization aligns with the IRS's requirements for exemption. Let's walk through the essential steps to complete the form accurately and effectively.

After submission, it’s a waiting game. The IRS will review your form, which can take several months. You might be contacted for more information or clarification on your submission. Once approved, you’ll receive a determination letter, which is your official document proving your tax-exempt status. Keep a close eye on your mailbox and be prepared to respond promptly to any inquiries from the IRS during the review process. This step towards achieving tax-exempt status is a pivotal one for your organization, laying the foundation for its fundraising and operational activities in the years to come.

What is the IRS 1023 form?

The IRS 1023 form, also known as the Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code, is a document that organizations must submit to the Internal Revenue Service (IRS) to obtain tax-exempt status. This designation allows charities, religious organizations, educational groups, and other eligible entities to be exempt from federal income tax. Completing this form accurately is a crucial step for organizations seeking to advance their missions through tax-exempt activities.

Who needs to file the IRS 1023 form?

Organizations seeking recognition of their tax-exempt status under Section 501(c)(3) of the Internal Revenue Code are required to file the IRS 1023 form. These include charitable organizations, religious groups, educational institutions, scientific organizations, literary societies, and other entities operating for exempt purposes. It is important for entities to assess their eligibility for 501(c)(3) status before embarking on the application process.

How long does it take to process the IRS 1023 form?

The processing time for the IRS 1023 form can vary significantly, usually ranging from 3 to 12 months, depending on the complexity of the application and the current backlog at the IRS. Organizations can expedite the process by ensuring that their application is complete and accurate, providing detailed descriptions of their activities, goals, and financial planning. The IRS may request additional information, which can extend the processing time. Timely responses to such requests can help reduce delays.

What information is required on the IRS 1023 form?

The IRS 1023 form requires comprehensive information about the applying organization, including its legal name, contact information, history, structure, detailed descriptions of its activities, financial data, and governance. The form also requires documentation supporting the entity's operational and financial practices, including bylaws, articles of incorporation, and financial statements. Clarity and accuracy in presenting this information are critical to the application's success.

Is there a filing fee for the IRS 1023 form?

Yes, there is a filing fee for the IRS 1023 form, and the amount depends on the organization's gross receipts. Smaller organizations with projected or actual annual gross receipts of $50,000 or less have a lower fee, while larger organizations with higher receipts face a higher fee. This fee is non-refundable and must accompany the application. Up-to-date fee information can be found on the IRS website, as these amounts can change.

Can the IRS 1023 form be filed electronically?

Yes, the IRS 1023 form can be filed electronically through the IRS website. The electronic filing option facilitates the submission process and may result in faster processing times. Electronic submissions require setting up an account on the IRS website. This method is recommended for its efficiency and convenience, and it allows applicants to track the status of their application online.

What happens after the IRS 1023 form is approved?

Upon approval of the IRS 1023 form, the organization will receive a determination letter from the IRS recognizing its tax-exempt status under Section 501(c)(3). This letter is essential for many aspects of the organization's operations, including eligibility for certain grants, tax-deductible contributions from donors, and exemption from federal income tax. The organization should maintain a copy of this letter for its records and provide copies to donors upon request.

Are there annual reporting requirements after receiving 501(c)(3) status?

Yes, organizations that have been granted 501(c)(3) status are required to file an annual informational return with the IRS, typically Form 990, 990-EZ, or 990-N (e-Postcard), depending on their gross receipts and assets. This filing requirement is crucial to maintain tax-exempt status and provides transparency regarding the organization's operations, finances, and adherence to its exempt purposes. Failure to file for three consecutive years results in automatic revocation of tax-exempt status.

Can tax-exempt status be revoked?

Yes, the IRS can revoke an organization's tax-exempt status if it fails to adhere to the operating constraints outlined in Section 501(c)(3), such as engaging in excessive political activities, failing to file required annual returns, or deviating from its exempt purpose. It is vital for organizations to comply with all legal requirements, report annual financial information accurately, and operate consistently with their stated exempt objectives to maintain their tax-exempt status.

Where can applicants find help with completing the IRS 1023 form?

Applicants can find assistance with the IRS 1023 form through various resources, including the IRS website, which offers instructions and tips for completing the form. Legal professionals specializing in nonprofit law can provide valuable guidance and ensure that the application meets all regulatory requirements. Additionally, nonprofit organizations and associations often offer workshops, webinars, and counseling services to help with the application process. Utilizing these resources can significantly enhance the likelihood of a successful application.

When organizations seek to secure 501(c)(3) status, completing the IRS 1023 form is a critical step. However, due to its complexity, people often make mistakes that can delay or affect their application. Understanding these common errors can guide organizations to better prepare their applications.

Not carefully reading the instructions: It is crucial to thoroughly review the form's instructions before starting the application process. Each section has specific requirements that need to be followed precisely.

Omitting necessary documents: The 1023 form requires various documents to be submitted alongside it, such as the organization's articles of incorporation and bylaws. Failure to include these can lead to processing delays.

Incorrectly classifying the organization: Organizations must correctly identify their classification based on their purpose and activities. Mistakes here can result in the application being processed under the wrong category.

Failing to describe activities in detail: The IRS requires detailed descriptions of current and planned activities. Vague or incomplete descriptions can raise questions about the organization's eligibility.

Not providing a detailed budget: A comprehensive budget, including projected revenues and expenses, is necessary. This allows the IRS to understand the financial planning and sustainability of the organization.

Forgetting to sign and date the form: Though it seems minor, forgetting to sign and date the application can result in it being returned.

Using outdated forms: The IRS periodically updates the 1023 form. Using an outdated version can lead to the rejection of the application.

Miscalculating the user fee: The IRS charges a user fee for processing the 1023 application. Incorrectly calculating or submitting the wrong fee amount can cause delays.

Avoiding these mistakes requires attention to detail, thorough preparation, and a clear understanding of the process. Organizations may benefit from consulting with professionals who specialize in nonprofit law to ensure their application is complete and accurate. By doing so, they can improve their chances of gaining 501(c)(3) status in a timely manner.

The IRS 1023 form is central for organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Alongside this primary document, several other forms and documents are frequently needed to ensure a comprehensive application process. These additional materials help illustrate the organization's structure, financial projections, operational practices, and compliance with legal requirements. Understanding each of these documents can significantly ease the application process for tax exemption.

In sum, while the IRS 1023 form is pivotal for nonprofits aiming to secure 501(c)(3) tax-exempt status, a thorough and valid application involves assembling additional documents. These documents, ranging from foundational organizational material to financial forecasts and operational policies, illustrate the organization's readiness and alignment with the exempt purposes as outlined by the IRS. By comprehensively preparing these forms and documents, organizations can navigate the application process more smoothly and favorably position themselves for gaining tax-exempt status.

IRS Form 1024: Just like IRS Form 1023, which organizations use to apply for recognition of exemption under section 501(c)(3) of the Internal Revenue Code, IRS Form 1024 is used by organizations seeking recognition of exemption under sections other than 501(c)(3). While Form 1023 is specific to charitable, religious, educational, and similar types of organizations, Form 1024 applies to a broader range of nonprofit entities, including social welfare organizations, business leagues, and fraternal societies.

IRS Form 990: IRS Form 990 is an annual information return that tax-exempt organizations are required to file. The similarity with the IRS Form 1023 lies in its focus on non-profit organizations. However, rather than being a form for applying for tax-exempt status, Form 990 provides the IRS and the public with financial information about the non-profit, including its income, expenses, and compensation of its highest-paid employees. It serves to ensure that the organization continues to operate in a manner consistent with its tax-exempt purposes.

IRS Form 8871: IRS Form 8871 is used by political organizations to notify the IRS of their intent to operate under section 527. It is similar to Form 1023 in that both forms are used by organizations seeking a specific tax status; however, Form 8871 is specifically for political organizations that wish to be recognized as exempt from federal income tax. Both forms require detailed information about the organization, its officers, and its specific activities.

IRS Form 8282: IRS Form 8282 is used by donee organizations to report information to the IRS about dispositions of certain charitable deduction property made within three years after the donor contributed the property. This form is somewhat similar to Form 1023 in its connection to charitable activities. Although Form 8282 deals with the reporting of post-donation activities rather than the application for tax-exempt status, it underscores the accountability and regulatory compliance expected of tax-exempt organizations.

Filling out the IRS 1023 form, an essential step in obtaining tax-exempt status under Section 501(c)(3) of the Internal Revenue Code, demands meticulous attention to detail and thoroughness. The following guide outlines best practices and common pitfalls to avoid, ensuring that the application process is as smooth and error-free as possible.

Do:

Don't:

The IRS Form 1023, pivotal for organizations seeking tax-exempt status under section 501(c)(3) of the Internal Revenue Code, is often misunderstood. Several misconceptions cloud its purpose, process, and requirements. This leads to confusion and potential mistakes in the application process. Here are six common myths, debunked to provide clarity:

Completing the Form 1023 is quick and easy. Many believe that filling out the IRS Form 1023 requires little effort and can be completed swiftly. However, the reality is that this form is comprehensive and requires detailed information about an organization's structure, activities, governance policies, and financial data. It demands thorough preparation and, quite often, advice or assistance from professionals experienced in tax law or nonprofit compliance.

The IRS Form 1023 only applies to large organizations. The truth is, the size of the organization does not exempt it from filing Form 1023 if it seeks 501(c)(3) status. While smaller entities may opt for Form 1023-EZ, a streamlined version, under certain criteria, the primary form is designed for all types of organizations, regardless of size, that wish to be recognized as tax-exempt under this specific section of the Tax Code.

Approval is guaranteed after submission. Some applicants assume that once Form 1023 is submitted, approval of their 501(c)(3) status is merely a formality. Nevertheless, the IRS reviews each application meticulously to ensure compliance with all requirements. Approval is not guaranteed, and organizations may be questioned further or even denied based on the information provided in their application.

Form 1023 affects only federal tax status. It's a common belief that Form 1023 relates solely to federal tax exemption. While it is true that its primary function is to establish an organization's status as tax-exempt at the federal level, this status often influences state tax obligations and eligibility for certain state benefits, including sales, property, and income tax exemptions. Therefore, the implications of Form 1023 extend beyond federal taxation.

Any organization can file Form 1023 at any time. This statement is not entirely accurate. Eligibility to file Form 1023 is contingent upon an organization's incorporation and nature of operations. Specifically, it must be a corporation, an unincorporated association, or a trust operating for exempt purposes as defined in section 501(c)(3). Moreover, it is recommended to file within 27 months from the end of the month in which the organization was established to ensure retroactive tax exemption from the date of formation.

Financial data provided in the form does not need to be precise. On the contrary, precision in presenting financial details is crucial. The IRS requires a reasonable estimation of an organization's finances for the current year and projections for the next two years. This includes revenue, expenses, and a breakdown of activities. Accuracy in these forecasts plays a critical role in the evaluation process, supporting the organization's planned operations and exempt purposes.

Understanding and dispelling these misconceptions about the IRS Form 1023 can significantly smooth the application process for tax-exempt status. Organizations are encouraged to approach the task with diligence and, when needed, seek knowledgeable support to navigate the complexities effectively.

The IRS 1023 form is essential for organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Approaching this document with clear understanding and meticulous attention to detail is crucial for a successful application. Below are key takeaways that can help you navigate the filling out and use of the IRS 1023 form effectively.

Successfully navigating the IRS 1023 form is a significant step towards achieving tax-exempt status for your organization. By understanding these key aspects, you'll be better positioned to complete and submit your application with confidence.

Idpfr - By integrating insurance information within the licensure process, the form streamlines administrative efficiency.

Roof Inspection Report Template - A roof certification document issued by XYZ Roofing Contractors, guaranteeing that the mentioned property's roof has been inspected, repaired as necessary, and is now certified as water-tight for a two-year period.

How to File a Construction Lien in Florida - Facilitates a dialogue between the contributor and property owner, underlined by the serious implication of lien filing for non-resolution of debts.