Free IRS 1042-S PDF Template

Free IRS 1042-S PDF Template

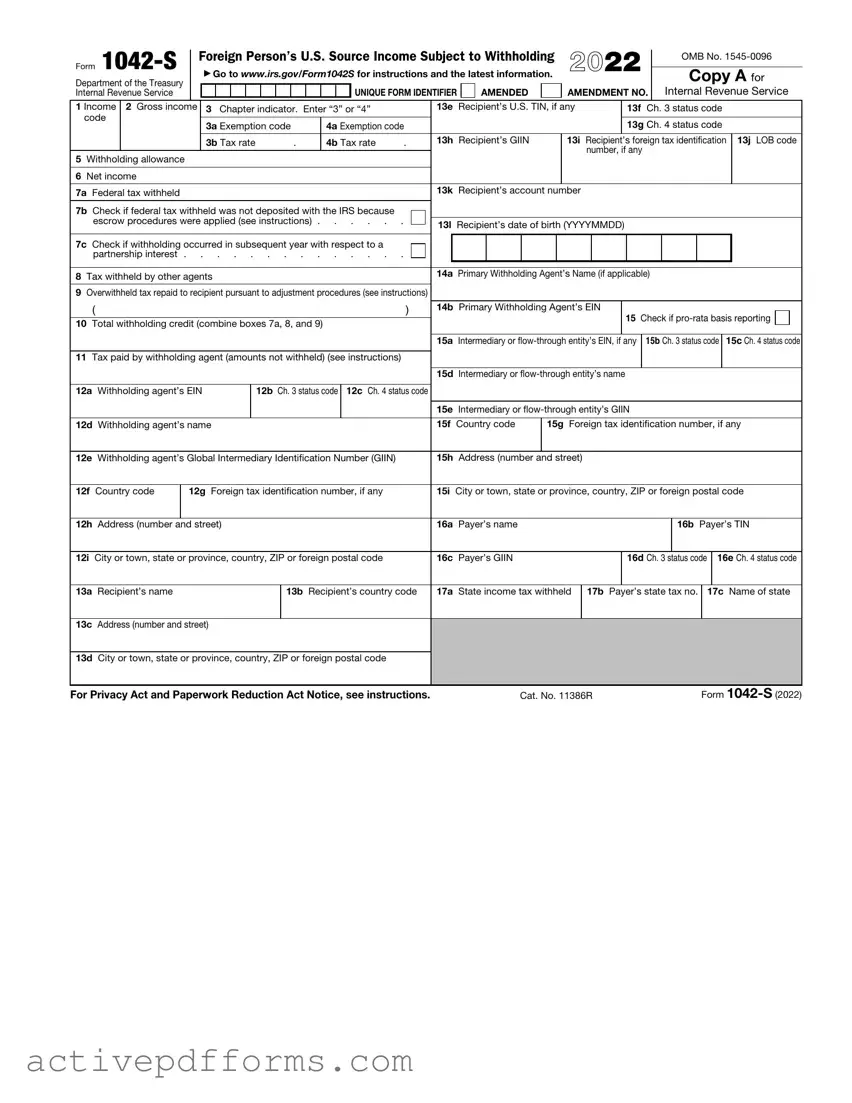

The labyrinth of tax forms in the United States includes some that are more cryptic than others, and nestled among them is the IRS 1042-S form. This document plays a pivotal role in the financial interactions between the U.S. and persons or entities beyond its borders. It serves as a critical mechanism for reporting income paid to foreign individuals, whether they are students, employees, or contractors, and on investments held by non-U.S. residents. The form captures a wide array of income types, from scholarships and royalties to interest and dividends, essentially any payment that could be subject to U.S. income tax withholding. Moreover, the 1042-S form is not just about reporting amounts paid; it also details the taxes withheld on these payments, ensuring compliance with tax treaties and U.S. tax laws. This information provides the Internal Revenue Service (IRS) with the means to ensure that the appropriate taxes are collected, and it gives foreign individuals and entities the data needed to navigate their tax obligations within their own countries, perhaps claiming a credit for taxes paid in the U.S. Given its multifaceted purposes and the complexities that can arise in cross-border taxation scenarios, understanding the intricacies of the 1042-S form is paramount for those navigating the international aspects of U.S. tax law.

|

|

|

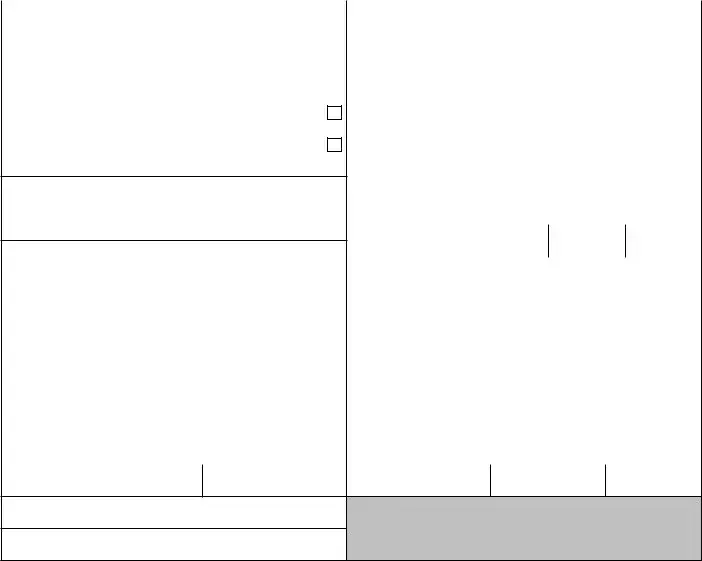

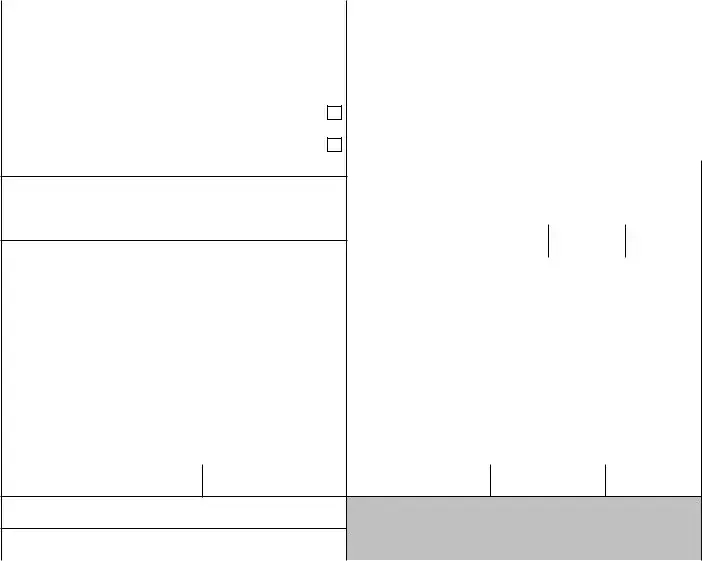

Foreign Person’s U.S. Source Income Subject to Withholding |

2022 |

|

OMB No. |

|||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||

Department of the Treasury |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Copy A for |

|||||||||

Form |

|

▶ Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

|

|

|||||||||||||||||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

AMENDED |

|

|

AMENDMENT NO. |

|

Internal Revenue Service |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 Income |

2 Gross income |

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13e |

Recipient’s U.S. TIN, if any |

|

|

|

13f Ch. 3 status code |

||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13h |

Recipient’s GIIN |

13i Recipient’s foreign tax identification |

13j LOB code |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

13k |

Recipient’s account number |

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

escrow procedures were applied (see instructions) |

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

partnership interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

8 Tax withheld by other agents |

|

|

|

|

|

|

|

14a |

Primary Withholding Agent’s Name (if applicable) |

|

|

|

|

||||||||||||||||||

9Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions)

( |

) |

|

14b Primary Withholding Agent’s EIN |

15 Check if |

|

|

|

|

|

||||

10 Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a Intermediary or |

|||

11Tax paid by withholding agent (amounts not withheld) (see instructions)

|

|

|

|

|

|

|

15d Intermediary or |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a |

Withholding agent’s EIN |

|

12b Ch. 3 status code |

12c Ch. 4 status code |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15e |

Intermediary or |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

12d Withholding agent’s name |

15f Country code |

15g Foreign tax identification number, if any |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

12e |

Withholding agent’s Global Intermediary Identification Number (GIIN) |

15h |

Address (number and street) |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12f |

Country code |

12g |

Foreign tax identification number, if any |

15i |

City or town, state or province, country, ZIP or foreign postal code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12h |

Address (number and street) |

16a |

Payer’s name |

|

|

|

16b Payer’s TIN |

|||||||

|

|

|

|

|

|

|

|

|

||||||

12i City or town, state or province, country, ZIP or foreign postal code |

16c |

Payer’s GIIN |

|

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

13a |

Recipient’s name |

|

|

13b Recipient’s country code |

17a |

State income tax withheld |

17b Payer’s state tax no. |

17c Name of state |

||||||

13c Address (number and street)

13d City or town, state or province, country, ZIP or foreign postal code

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Cat. No. 11386R |

Form |

Form |

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2022 |

|

|

OMB No. |

|||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

▶ Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

|

Copy B |

||||||||||||||||||||||||||||

Department of the Treasury |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

AMENDED |

|

|

AMENDMENT NO. |

|

|

for Recipient |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 Income |

2 Gross income |

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13e |

Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

|||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13h |

Recipient’s GIIN |

|

13i Recipient’s foreign tax identification |

13j LOB code |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

13k |

Recipient’s account number |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

escrow procedures were applied (see instructions) |

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

partnership interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

8 Tax withheld by other agents |

|

|

|

|

|

|

|

14a |

Primary Withholding Agent’s Name (if applicable) |

||||||||||||||||||||||||

9Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions)

( |

) |

|

14b Primary Withholding Agent’s EIN |

15 Check if |

|

|

|

|

|

||||

10 Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a Intermediary or |

|||

11Tax paid by withholding agent (amounts not withheld) (see instructions)

|

|

|

|

|

|

|

15d Intermediary or |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a |

Withholding agent’s EIN |

|

12b Ch. 3 status code |

12c Ch. 4 status code |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15e |

Intermediary or |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

12d Withholding agent’s name |

15f Country code |

15g Foreign tax identification number, if any |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

12e |

Withholding agent’s Global Intermediary Identification Number (GIIN) |

15h |

Address (number and street) |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12f |

Country code |

12g |

Foreign tax identification number, if any |

15i |

City or town, state or province, country, ZIP or foreign postal code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12h |

Address (number and street) |

16a |

Payer’s name |

|

|

|

16b Payer’s TIN |

|||||||

|

|

|

|

|

|

|

|

|

||||||

12i City or town, state or province, country, ZIP or foreign postal code |

16c |

Payer’s GIIN |

|

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

13a |

Recipient’s name |

|

|

13b Recipient’s country code |

17a |

State income tax withheld |

17b Payer’s state tax no. |

17c Name of state |

||||||

13c Address (number and street)

13d City or town, state or province, country, ZIP or foreign postal code

(keep for your records) |

Form |

U.S. Income Tax Filing Requirements

Generally, every nonresident alien individual, nonresident alien fiduciary, and foreign corporation with U.S. income, including income that is effectively connected with the conduct of a trade or business in the United States, must file a U.S. income tax return. However, no return is required to be filed by a nonresident alien individual, nonresident alien fiduciary, or foreign corporation if such person was not engaged in a trade or business in the United States at any time during the tax year and if the tax liability of such person was fully satisfied by the withholding of U.S. tax at the source. Corporations file Form

En règle générale, tout étranger

àIRS.gov et dans toutes les ambassades et tous les consulats des

Explanation of Codes

Box 1. Income Code.

Code |

Types of Income |

01Interest paid by U.S.

02Interest paid on real property mortgages

03Interest paid to controlling foreign corporations

04Interest paid by foreign corporations

05Interest on

|

22 |

Interest paid on deposit with a foreign branch of a domestic |

|

Interest |

30 |

corporation or partnership |

|

Original issue discount (OID) |

|||

|

29 |

Deposit interest |

|

|

31 |

||

|

33 |

Substitute |

|

|

51 |

Interest paid on certain actively traded or publicly offered |

|

|

|

securities1 |

|

|

54 |

Substitute |

|

|

|

or publicly offered securities1 |

|

Dividend |

06 |

Dividends paid by U.S. |

|

07 |

Dividends qualifying for direct dividend rate |

||

|

|||

|

08 |

Dividends paid by foreign corporations |

Por regla general, todo extranjero no residente, todo organismo fideicomisario extranjero no residente y toda sociedad anónima extranjera que reciba ingresos en los Estados Unidos, incluyendo ingresos relacionados con la conducción de un negocio o comercio dentro de los Estados Unidos, deberá presentar una declaración estadounidense de impuestos sobre el ingreso. Sin embargo, no se requiere declaración alguna a un individuo extranjero, una sociedad anónima extranjera u organismo fideicomisario extranjero no residente, si tal persona no ha efectuado comercio o negocio en los Estados Unidos durante el año fiscal y si la responsabilidad con los impuestos de tal persona ha sido satisfecha plenamente mediante retención del impuesto de los Estados Unidos en la fuente. Las sociedades anónimas envían el Formulario

Im allgemeinen muss jede ausländische Einzelperson, jeder ausländische Bevollmächtigte und jede ausländische Gesellschaft mit Einkommen in den Vereinigten Staaten, einschliesslich des Einkommens, welches direkt mit der Ausübung von Handel oder Gewerbe innerhalb der Staaten verbunden ist, eine Einkommensteuererklärung der Vereinigten Staaten abgeben. Eine Erklärung, muss jedoch nicht von Ausländern, ausländischen Bevollmächtigten oder ausländischen Gesellschaften in den Vereinigten Staaten eingereicht werden, falls eine solche Person während des Steuerjahres kein Gewerbe oder Handel in den Vereinigten Staaten ausgeübt hat und die Steuerschuld durch Einbehaltung der Steuern der Vereinigten Staaten durch die Einkommensquelle abgegolten ist. Gesellschaften reichen den Vordruck

|

34 |

Substitute |

|

40 |

Other dividend equivalents under IRC section 871(m) |

Dividend |

52 |

Dividends paid on certain actively traded or publicly offered |

|

securities1 |

|

|

|

|

|

53 |

Substitute |

|

|

publicly offered securities1 |

|

56 |

Dividend equivalents under IRC section 871(m) as a result of |

|

|

applying the combined transaction rules |

|

|

|

|

09 |

Capital gains |

|

10 |

Industrial royalties |

|

11 |

Motion picture or television copyright royalties |

|

12 |

Other royalties (for example, copyright, software, |

|

|

broadcasting, endorsement payments) |

Other |

13 |

Royalties paid on certain publicly offered securities1 |

14 |

Real property income and natural resources royalties |

|

|

15 |

Pensions, annuities, alimony, and/or insurance premiums |

|

16 |

Scholarship or fellowship grants |

|

17 |

Compensation for independent personal services2 |

|

18 |

Compensation for dependent personal services2 |

|

19 |

Compensation for teaching2 |

See back of Copy C for additional codes

1This code should only be used if the income paid is described in Regulations section

2If compensation that otherwise would be covered under Income Codes 17 through 20 is directly attributable to the recipient’s occupation as an artist or athlete, use Income Code 42 or 43 instead.

Form |

|

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2022 |

|

|

OMB No. |

|||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Department of the Treasury |

|

|

▶ Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

Copy C for Recipient |

||||||||||||||||||||||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

|

|

AMENDED |

|

|

AMENDMENT NO. |

|

Attach to any Federal tax return you file |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 Income |

2 Gross income |

|

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13e |

Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

|||||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13h |

Recipient’s GIIN |

|

13i Recipient’s foreign tax identification |

13j LOB code |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

13k |

Recipient’s account number |

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

escrow procedures were applied (see instructions) |

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

partnership interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

8 Tax withheld by other agents |

|

|

|

|

|

|

|

14a |

Primary Withholding Agent’s Name (if applicable) |

|||||||||||||||||||||||||||

9Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions)

( |

) |

|

14b Primary Withholding Agent’s EIN |

15 Check if |

|

|

|

|

|

||||

10 Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a Intermediary or |

|||

11Tax paid by withholding agent (amounts not withheld) (see instructions)

|

|

|

|

|

|

|

15d Intermediary or |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a |

Withholding agent’s EIN |

|

12b Ch. 3 status code |

12c Ch. 4 status code |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15e |

Intermediary or |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

12d Withholding agent’s name |

15f Country code |

15g Foreign tax identification number, if any |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

12e |

Withholding agent’s Global Intermediary Identification Number (GIIN) |

15h |

Address (number and street) |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12f |

Country code |

12g |

Foreign tax identification number, if any |

15i |

City or town, state or province, country, ZIP or foreign postal code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12h |

Address (number and street) |

16a |

Payer’s name |

|

|

|

16b Payer’s TIN |

|||||||

|

|

|

|

|

|

|

|

|

||||||

12i City or town, state or province, country, ZIP or foreign postal code |

16c |

Payer’s GIIN |

|

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

13a |

Recipient’s name |

|

|

13b Recipient’s country code |

17a |

State income tax withheld |

17b Payer’s state tax no. |

17c Name of state |

||||||

13c Address (number and street)

13d City or town, state or province, country, ZIP or foreign postal code

Form

Explanation of Codes (continued)

|

20 |

Compensation during studying and training2 |

|

|

23 |

Other income |

|

|

24 |

Qualified investment entity (QIE) distributions of capital |

|

|

|

gains |

|

|

25 |

Trust distributions subject to IRC section 1445 |

|

|

26 |

Unsevered growing crops and timber distributions by a trust |

|

|

|

subject to IRC section 1445 |

|

|

27 |

Publicly traded partnership distributions subject to IRC |

|

|

|

section 1446 |

|

|

28 |

Gambling winnings3 |

|

|

32 |

Notional principal contract income4 |

|

Other |

35 |

Substitute |

|

36 |

Capital gains distributions |

||

|

|||

|

37 |

Return of capital |

|

|

38 |

Eligible deferred compensation items subject to IRC section |

|

|

|

877A(d)(1) |

|

|

39 |

Distributions from a nongrantor trust subject to IRC section |

|

|

|

877A(f)(1) |

41Guarantee of indebtedness

42Earnings as an artist or

43Earnings as an artist or

44Specified federal procurement payments

50Income previously reported under escrow procedure6

55Taxable death benefits on life insurance contracts

57Amount realized under IRC section 1446(f)

Boxes 3a and 4a. Exemption Code (applies if the tax rate entered in box 3b or 4b is 00.00).

CodeAuthority for Exemption Chapter 3

01Effectively connected income

02Exempt under IRC7

03Income is not from U.S. sources

04Exempt under tax treaty

05Portfolio interest exempt under IRC

06QI that assumes primary withholding responsibility

07WFP or WFT

08U.S. branch treated as U.S. Person

09Territory FI treated as U.S. Person

10QI represents that income is exempt

11QSL that assumes primary withholding responsibility

12Payee subjected to chapter 4 withholding

22QDD that assumes primary withholding responsibility

23Exempt under section 897(l)

24Exempt under section 892

Chapter 4

13Grandfathered payment

14Effectively connected income

15Payee not subject to chapter 4 withholding

16Excluded nonfinancial payment

17Foreign Entity that assumes primary withholding responsibility

18U.S.

19Exempt from withholding under IGA8

20Dormant account9

21

Boxes 12b, 12c, 13f, 13g, 15b, 15c, 16d, and 16e. Withholding Agent, Recipient, Intermediary, and Payer Chapter 3 and Chapter 4 Status Codes.

Type of Recipient, Withholding Agent, Payer, or Intermediary Code

Chapter 3 Status Codes

03Territory

04Territory

05U.S.

06U.S.

07U.S.

08Partnership other than Withholding Foreign Partnership or Publicly Traded Partnership

09Withholding Foreign Partnership

See back of Copy D for additional codes

2If compensation that otherwise would be covered under Income Codes 17 through 20 is directly attributable to the recipient’s occupation as an artist or athlete, use Income Code 42 or 43 instead.

3Subject to 30% withholding rate unless the recipient is from one of the treaty countries listed under Gambling winnings (Income Code 28) in Pub. 515.

4Use appropriate Interest Income Code for embedded interest in a notional principal contract.

5Income Code 43 should only be used if Letter 4492, Venue Notification, has been issued by the Internal Revenue Service (otherwise, use Income Code 42 for earnings as an artist or athlete). If Income Code 42 or 43 is used, Recipient Code 22 (artist or athlete) should be used instead of Recipient Code 16 (individual), 15 (corporation), or 08 (partnership other than withholding foreign partnership).

6Use only to report gross income the tax for which is being deposited in the current year because such tax was previously escrowed for chapters 3 and 4 and the withholding agent previously reported the gross income in a prior year and checked the box to report the tax as not deposited under the escrow procedure. See the instructions to this form for further explanation.

7This code should only be used if no other specific chapter 3 exemption code applies.

8Use only to report a U.S. reportable account or nonconsenting U.S. account that is receiving a payment subject to chapter 3 withholding.

9Use only if applying the escrow procedure for dormant accounts under Regulations section

Form |

|

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2022 |

|

|

OMB No. |

|||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Department of the Treasury |

|

|

▶ Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

Copy D for Recipient |

||||||||||||||||||||||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

|

|

AMENDED |

|

|

AMENDMENT NO. |

|

|

Attach to any state tax return you file |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 Income |

2 Gross income |

|

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13e |

Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

|||||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13h |

Recipient’s GIIN |

|

13i Recipient’s foreign tax identification |

13j LOB code |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

13k |

Recipient’s account number |

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

escrow procedures were applied (see instructions) |

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

partnership interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

8 Tax withheld by other agents |

|

|

|

|

|

|

|

14a |

Primary Withholding Agent’s Name (if applicable) |

|||||||||||||||||||||||||||

9Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions)

( |

) |

|

14b Primary Withholding Agent’s EIN |

15 Check if |

|

|

|

|

|

||||

10 Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a Intermediary or |

|||

11Tax paid by withholding agent (amounts not withheld) (see instructions)

|

|

|

|

|

|

|

15d Intermediary or |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a |

Withholding agent’s EIN |

|

12b Ch. 3 status code |

12c Ch. 4 status code |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15e |

Intermediary or |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

12d Withholding agent’s name |

15f Country code |

15g Foreign tax identification number, if any |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

12e |

Withholding agent’s Global Intermediary Identification Number (GIIN) |

15h |

Address (number and street) |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12f |

Country code |

12g |

Foreign tax identification number, if any |

15i |

City or town, state or province, country, ZIP or foreign postal code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12h |

Address (number and street) |

16a |

Payer’s name |

|

|

|

16b Payer’s TIN |

|||||||

|

|

|

|

|

|

|

|

|

||||||

12i City or town, state or province, country, ZIP or foreign postal code |

16c |

Payer’s GIIN |

|

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

13a |

Recipient’s name |

|

|

13b Recipient’s country code |

17a |

State income tax withheld |

17b Payer’s state tax no. |

17c Name of state |

||||||

13c Address (number and street)

13d City or town, state or province, country, ZIP or foreign postal code

Form

Explanation of Codes (continued)

10Trust other than Withholding Foreign Trust

11Withholding Foreign Trust

12Qualified Intermediary

13Qualified Securities

14Qualified Securities

15Corporation

16Individual

17Estate

18Private Foundation

19International Organization

20Tax Exempt Organization (Section 501(c) entities)

21Unknown Recipient

22Artist or Athlete

23Pension

24Foreign Central Bank of Issue

25Nonqualified Intermediary

26Hybrid entity making Treaty Claim

35Qualified Derivatives Dealer

36Foreign

37Foreign

38Publicly Traded Partnership

Pooled Reporting Codes10

27Withholding Rate

28Withholding Rate

29PAI Withholding Rate

30PAI Withholding Rate

31Agency Withholding Rate

32Agency Withholding Rate

Chapter 4 Status Codes

01U.S. Withholding

02U.S. Withholding

03Territory

04Territory

05Participating

06Participating

07Registered

08Registered

09Registered

10Certified

11Certified

12Certified

13Certified

14Certified

15Nonparticipating FFI

16

17U.S.

18U.S.

19Passive NFFE identifying Substantial U.S. Owners

20Passive NFFE with no Substantial U.S. Owners

21Publicly Traded NFFE or Affiliate of Publicly Traded NFFE

22Active NFFE

23Individual

24Section 501(c) Entities

25Excepted Territory NFFE

26Excepted

27Exempt Beneficial Owner

28Entity Wholly Owned by Exempt Beneficial Owners

29Unknown Recipient

30Recalcitrant Account Holder

31Nonreporting IGA FFI

32Direct reporting NFFE

33U.S. reportable account

34Nonconsenting U.S. account

35Sponsored direct reporting NFFE

36Excepted

37Undocumented Preexisting Obligation

38U.S.

39Account Holder of Excluded Financial Account11

40Passive NFFE reported by FFI12

41NFFE subject to 1472 withholding

50U.S. Withholding

Pooled Reporting Codes

42Recalcitrant

43Recalcitrant

44Recalcitrant

45Recalcitrant

46Recalcitrant

47Nonparticipating FFI Pool

48U.S. Payees Pool

49

Box 13j. LOB Code (enter the code that best describes the applicable limitation on benefits (LOB) category that qualifies the taxpayer for the requested treaty benefits).

LOB Code |

LOB Treaty Category |

02Government – contracting state/political subdivision/local authority

03Tax exempt pension trust/Pension fund

04Tax exempt/Charitable organization

05Publicly traded corporation

06Subsidiary of publicly traded corporation

07Company that meets the ownership and base erosion test

08Company that meets the derivative benefits test

09Company with an item of income that meets the active trade or business test

10Discretionary determination

11Other

12No LOB article in treaty

10Codes 27 through 32 should only be used by a QI, QSL, WP, or WT. A QI acting as a QDD may use only code 27 or 28.

11This code should only be used if income is paid to an account that is excluded from the definition of financial account under Regulations section

12This code should only be used when the withholding agent has received a certification on the FFI withholding statement of a participating FFI or registered deemed- compliant FFI that maintains the account that the FFI has reported the account held by the passive NFFE as a U.S. account (or U.S. reportable account) under its FATCA requirements. The withholding agent must report the name and GIIN of such FFI in boxes 15d and 15e.

13This code should only be used by a withholding agent that is reporting a payment (or portion of a payment) made to a QI with respect to the QI’s recalcitrant account holders.

Form |

|

Foreign Person’s U.S. Source Income Subject to Withholding |

2022 |

|

|

OMB No. |

|||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

▶ Go to www.irs.gov/Form1042S for instructions and the latest information. |

|

|

|

Copy E |

||||||||||||||||||||||||||||||

Department of the Treasury |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

UNIQUE FORM IDENTIFIER |

|

AMENDED |

|

|

AMENDMENT NO. |

|

|

for Withholding Agent |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 Income |

2 Gross income |

|

3 Chapter indicator. Enter “3” or “4” |

|

|

13e Recipient’s U.S. TIN, if any |

|

|

|

13f |

Ch. 3 status code |

||||||||||||||||||||||||

code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3a Exemption code |

|

|

4a Exemption code |

|

|

|

|

|

|

|

|

|

|

|

|

|

13g Ch. 4 status code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

3b Tax rate |

. |

|

4b Tax rate |

. |

|

13h Recipient’s GIIN |

|

13i Recipient’s foreign tax identification |

13j LOB code |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

number, if any |

|

|

|

|

|

|

|||

5 Withholding allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6 Net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

7a Federal tax withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

13k Recipient’s account number |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7b Check if federal tax withheld was not deposited with the IRS because |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

escrow procedures were applied (see instructions) |

|

|

13l Recipient’s date of birth (YYYYMMDD) |

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7c Check if withholding occurred in subsequent year with respect to a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

partnership interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

8 Tax withheld by other agents |

|

|

|

|

|

|

|

14a Primary Withholding Agent’s Name (if applicable) |

|||||||||||||||||||||||||||

9Overwithheld tax repaid to recipient pursuant to adjustment procedures (see instructions)

( |

) |

|

14b Primary Withholding Agent’s EIN |

15 Check if |

|

|

|

|

|

||||

10 Total withholding credit (combine boxes 7a, 8, and 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a Intermediary or |

|||

11Tax paid by withholding agent (amounts not withheld) (see instructions)

|

|

|

|

|

|

|

15d Intermediary or |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a |

Withholding agent’s EIN |

|

12b Ch. 3 status code |

12c Ch. 4 status code |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15e |

Intermediary or |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

12d Withholding agent’s name |

15f Country code |

15g Foreign tax identification number, if any |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||

12e |

Withholding agent’s Global Intermediary Identification Number (GIIN) |

15h |

Address (number and street) |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12f |

Country code |

12g |

Foreign tax identification number, if any |

15i |

City or town, state or province, country, ZIP or foreign postal code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

12h |

Address (number and street) |

16a |

Payer’s name |

|

|

|

16b Payer’s TIN |

|||||||

|

|

|

|

|

|

|

|

|

||||||

12i City or town, state or province, country, ZIP or foreign postal code |

16c |

Payer’s GIIN |

|

|

16d Ch. 3 status code |

|

16e Ch. 4 status code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

||||

13a |

Recipient’s name |

|

|

13b Recipient’s country code |

17a |

State income tax withheld |

17b Payer’s state tax no. |

17c Name of state |

||||||

13c Address (number and street)

13d City or town, state or province, country, ZIP or foreign postal code

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Form |

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Form 1042-S is used to report income paid to a non-resident of the United States that is subject to income tax withholding. |

| Who Files It | This form is typically filed by a U.S. or foreign payer who pays a foreign person that includes individuals, corporations, partnerships, trusts, estates, consortia, or any other entity. |

| Types of Income Reported | Form 1042-S covers various types of income such as salaries, scholarships, dividends, royalties, rentals, commissions, and any other compensation or income paid to a non-resident alien. |

| Reporting and Withholding Compliance | The form helps ensure compliance with the withholding tax requirements under chapters 3 and 4 of the Internal Revenue Code, helping institutions to report amounts paid, taxes withheld, and to ensure the proper taxation of non-resident aliens. |

Filing the IRS 1042-S form is a crucial step for entities making payments of certain U.S. source income to foreign persons, including individuals, corporations, partnerships, trusts, estates, or any foreign persons that are subject to U.S. tax withholding. It requires precision and attention to detail. To ensure compliance with the IRS requirements, follow these step-by-step instructions to accurately complete and submit the form. Remember, this process helps in maintaining the integrity of the financial system while adhering to the tax laws in place for foreign entities and individuals.

After submission, keep a copy of the 1042-S form and any supporting documentation for your records. This provides evidence of compliance with IRS regulations and can be invaluable in the event of queries or audits. Staying organized and maintaining clear records simplifies future tax filings and supports accurate reporting for both the entity and the recipient.

What is an IRS 1042-S form and who needs to file it?

The IRS 1042-S form, formally known as the Foreign Person's U.S. Source Income Subject to Withholding, is a tax document used to report amounts paid to foreign persons (including individuals, corporations, partnerships, or non-resident alien individuals) by United States-based entities. This form is critical for income types such as dividends, interest, royalties, and compensation for services performed in the U.S., among others, when these amounts are subject to income tax withholding. Academic institutions, investment entities, and businesses that engage with foreign contractors or partners often find themselves required to file this form.

What types of income are reported on the 1042-S form?

Income reported on the 1042-S form spans various categories, reflecting the diverse nature of payments that U.S. sources might make to foreign entities. Key categories include, but are not limited to, earned income, such as wages or compensation for services; passive income, such as interest, dividends, and royalties; and gambling winnings. Each type of income necessitates careful documentation and accurate reporting to ensure compliance with U.S. tax laws and treaty agreements.

When is the deadline to file the 1042-S form?

The IRS mandates that the 1042-S form be filed by March 15th following the close of the calendar year in which the income was paid to the foreign person. Filers should be aware of this deadline to avoid penalties associated with late submissions. For those requiring more time, the IRS does offer an extension to file the form; however, an official request must be submitted to obtain this extension.

How does one obtain an extension to file the 1042-S form?

To secure an extension for filing the 1042-S form, the filer must submit a formal request to the IRS before the original due date of March 15th. This involves filing Form 8809, Application for Extension of Time to File Information Returns. It is important to note that this extension will grant additional time to file the form, not an extension to pay any due taxes. Accurate estimation and payment of taxes are expected by the original due date to avoid penalties.

Are there penalties for failing to file the 1042-S form?

Yes, failure to file the 1042-S form can result in significant penalties. These penalties are tiered based on the delay in filing. The initial penalty is imposed if the form is not filed by the due date (including extensions), with additional charges accruing the longer the form remains unfiled. These penalties underscore the importance of timely and accurate filing, not only to remain compliant with U.S. tax regulations but also to avoid needless financial costs.

Filling out the IRS 1042-S form can often feel like navigating through a maze. Mistakes are easy to make but can lead to headaches down the road. Here are four common missteps:

Not reporting all relevant sources of income. It might be tempting to include only your primary sources of income, but every payment that falls under the scope of the 1042-S form must be reported. This includes, but is not limited to, scholarships, grants, and compensation for services.

Using incorrect recipient codes. Each type of income and recipient has a specific code, and using the wrong one can throw a wrench into the processing of your form. Always double-check these codes to ensure they match the nature of your income and your status.

Forgetting to include complete payer information. The entity or person paying the income must be fully identified on the form. This means providing not just a name, but also a complete address and tax identification number. Incomplete information may cause delays or result in the form being sent back for correction.

Misunderstanding tax treaty benefits. If a tax treaty between the United States and your home country applies to you, understanding the specifics is crucial. Incorrectly applied benefits can lead to underpayment or overpayment of taxes, each with its own set of complications.

Keeping these points in mind will help smooth the filing process, ensuring accuracy and timeliness in your dealings with the IRS.

When dealing with tax reporting and compliance in the United States, especially in regards to payments made to foreign persons, the IRS Form 1042-S plays a crucial role. Beyond this form, several other documents and forms often play supportive or complementary roles in ensuring thorough compliance and reporting. These documents vary in purpose, from declaring tax treaty benefits to reporting income not subject to withholding. Whether you're an individual navigating the complexities of U.S. tax law for the first time, or a seasoned professional looking for a refresher, understanding these forms can provide clarity and ensure you meet all necessary tax obligations.

Understanding and properly utilizing these forms can significantly ease the process of compliance with U.S. tax laws. Entities and individuals engaged in cross-border payments should ensure they are familiar with the requirements of each relevant form to avoid penalties and maximize their benefit under the law. Consulting with a tax professional can provide personalized guidance and additional assurance that one's tax affairs are handled correctly.

The W-2 Form is similar to the IRS 1042-S form in that it reports income. While the 1042-S is for foreign persons' U.S. source income subject to withholding, the W-2 is used for reporting wages, tips, and other compensation paid to an employee and the taxes withheld from them in the U.S.

The 1099 Series of forms, especially the 1099-MISC and 1099-NEC, show similarities as they are used to report various types of income other than wages, salaries, and tips. These forms cater to U.S. citizens and residents, unlike the 1042-S which is specifically for the reporting of non-U.S. persons’ income.

The W-8BEN Form relates closely to the IRS 1042-S because it is also tied to foreign individuals. However, the W-8BEN is used by the individuals to certify their foreign status and claim benefits under the income tax treaty, rather than report income.

W-9 Form draws a parallel by being a request for taxpayer identification number and certification. Unlike the 1042-S which reports income paid to foreign persons, the W-9 is utilized to provide information directly by U.S. persons or resident aliens usually for real estate transactions, or other scenarios not involving employment.

The 1040 Form, used by individuals to file annual income tax returns in the U.S., shares similarities with the 1042-S as both deal with the reporting of income and taxes. However, the 1040 is much broader, covering all types of income earned by U.S. taxpayers.

Form 8966, the FATCA Report, is akin to the 1042-S as it deals with foreign financial information. The 8966 is part of the U.S. Foreign Account Tax Compliance Act (FATCA), requiring foreign financial institutions (FFIs) and certain other non-financial foreign entities to report on the foreign assets held by U.S. account holders.

Form 8804/8805/8813, related to Partnership Withholding Tax, have connections as they involve non-U.S. partners. These forms are used to report and pay the withholding tax due on effectively connected income allocable to the foreign partners, similar to how the 1042-S is used to report income paid to foreign individuals.

The IRS 1042-S form, also known as the Foreign Person's U.S. Source Income Subject to Withholding form, is an essential document for reporting amounts paid to foreign persons, including non-resident aliens, foreign corporations, and international organizations. Properly filling out this form is critical to ensure compliance with U.S. tax laws. Below are key dos and don'ts to consider when completing the IRS 1042-S form:

Do:When dealing with the IRS 1042-S form, many people have misconceptions. This form is pivotal for reporting income paid to a non-resident, including wages, scholarships, and compensation for services. Let's debunk some common misunderstandings about it.

Only applicable to employment income: A common myth is that Form 1042-S is only for reporting wages paid to non-resident aliens. In truth, it covers a broader range of payments including scholarships, grants, and royalties.

Only for large businesses: Some believe that only large corporations need to file Form 1042-S. However, any entity making payments subject to reporting to non-residents, regardless of its size, must file this form.