Free IRS 1120 PDF Template

Free IRS 1120 PDF Template

Navigating the intricate landscape of corporate taxation requires a solid understanding of various IRS forms, among which the IRS 1120 form stands out as a crucial document for corporations. This form serves as the foundation for reporting income, gains, losses, deductions, and credits, thereby determining the income tax liability of a corporation. It is essential for both domestic and foreign corporations operating in the United States to familiarize themselves with the requirements and intricacies of the IRS 1120, ensuring compliance and optimizing tax obligations. Completing this form accurately is not only a matter of legal compliance but also an opportunity to avail oneself of beneficial tax provisions, making it imperative for corporations to understand every aspect of it. As we delve into the major aspects of the IRS 1120 form, it's important to keep in mind the implications it has on a corporation's financial health and its standing with the IRS.

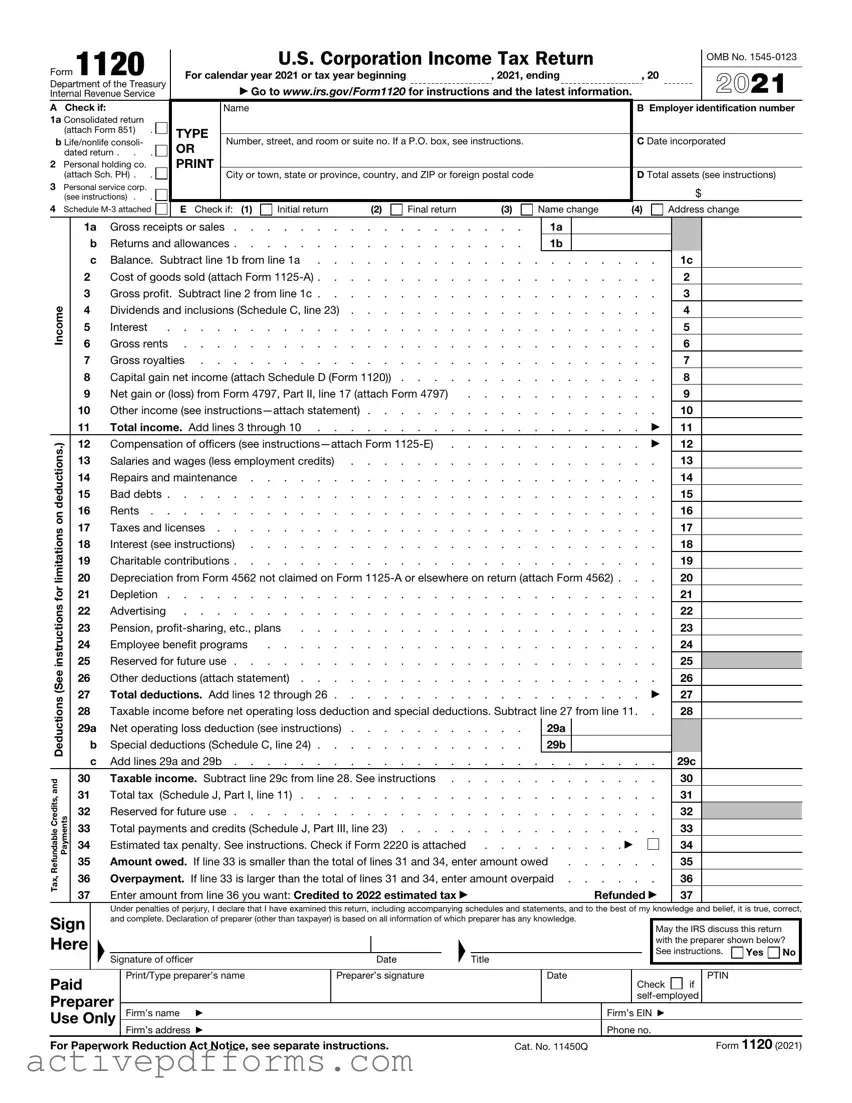

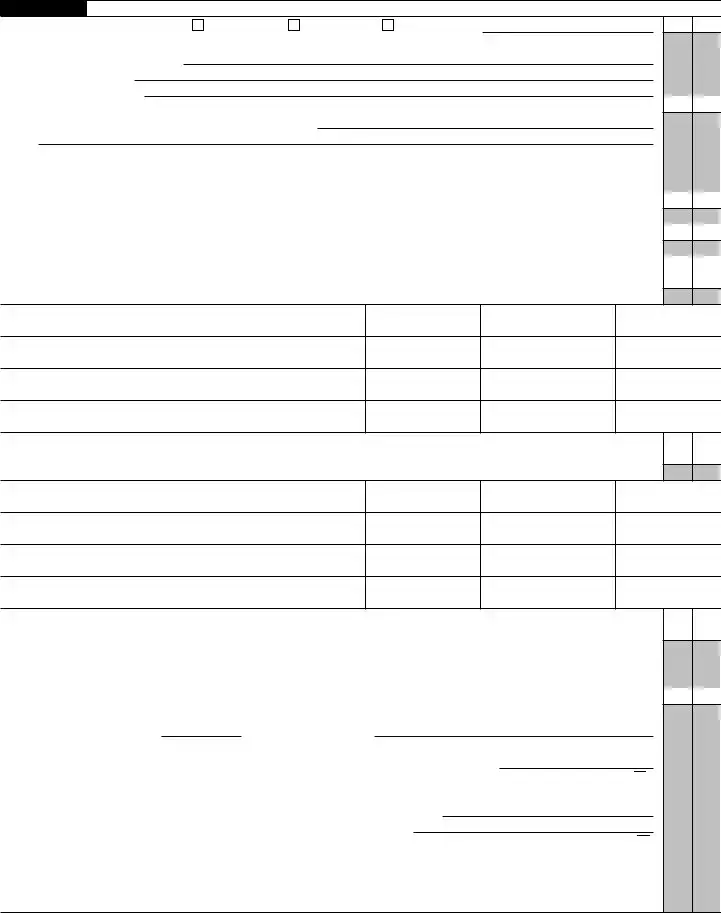

Form 1120

Department of the Treasury

Internal Revenue Service

A Check if:

1a Consolidated return (attach Form 851) .

b Life/nonlife consoli- dated return . . .

2Personal holding co. (attach Sch. PH) . .

3Personal service corp. (see instructions) . .

4 Schedule

|

|

U.S. Corporation Income Tax Return |

|

|

OMB No. |

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

For calendar year 2021 or tax year beginning |

|

, 2021, ending |

, 20 |

|

2021 |

||||

|

▶ Go to www.irs.gov/Form1120 for instructions and the latest information. |

|

|||||||

|

Name |

|

|

|

|

|

B Employer identification number |

||

TYPE |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

C Date incorporated |

|||||||

OR |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

D Total assets (see instructions) |

|||||||

|

|

||||||||

|

|

|

|

|

|

|

|

$ |

|

E Check if: (1) |

Initial return |

(2) |

Final return |

(3) |

Name change |

(4) |

Address change |

||

|

1a |

|

Gross receipts or sales |

|

. . . |

. |

|

1a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Returns and allowances |

|

. . . |

. |

|

1b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Balance. Subtract line 1b from line 1a |

|

. . . . . . . . . . . . |

1c |

|

|

||||||||||||||||||||

|

2 |

|

|

Cost of goods sold (attach Form |

|

. . . . . . . . . . . . |

2 |

|

|

|

|||||||||||||||||||

|

3 |

|

|

Gross profit. Subtract line 2 from line 1c |

|

. . . . . . . . . . . . |

3 |

|

|

|

|||||||||||||||||||

Income |

4 |

|

|

Dividends and inclusions (Schedule C, line 23) |

|

. . . . . . . . . . . . |

4 |

|

|

|

|||||||||||||||||||

5 |

|

|

Interest |

. . . . . . . . . . . . . . . . . . |

|

. . . . . . . . . . . . |

5 |

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

6 |

|

|

Gross rents |

|

. . . . . . . . . . . . |

6 |

|

|

|

|||||||||||||||||||

|

7 |

|

|

Gross royalties |

|

. . . . . . . . . . . . |

7 |

|

|

|

|||||||||||||||||||

|

8 |

|

|

Capital gain net income (attach Schedule D (Form 1120)) . . . . |

|

. . . . . . . . . . . . |

8 |

|

|

|

|||||||||||||||||||

|

9 |

|

|

Net gain or (loss) from Form 4797, Part II, line 17 (attach Form 4797) |

|

. . . . . . . . . . . . |

9 |

|

|

|

|||||||||||||||||||

|

10 |

|

|

Other income (see |

|

. . . . . . . . . . . . |

10 |

|

|

|

|||||||||||||||||||

|

11 |

|

|

Total income. Add lines 3 through 10 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

11 |

|

|

|

|||||||||||

deductions.) |

12 |

|

|

Compensation of officers (see |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

12 |

|

|

|

|||||||||||

13 |

|

|

Salaries and wages (less employment credits) |

|

. . . . . . . . . . . . |

13 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

14 |

|

|

Repairs and maintenance |

|

. . . . . . . . . . . . |

14 |

|

|

|

|||||||||||||||||||

|

15 |

|

|

Bad debts |

|

. . . . . . . . . . . . |

15 |

|

|

|

|||||||||||||||||||

on |

16 |

|

|

Rents |

|

. . . . . . . . . . . . |

16 |

|

|

|

|||||||||||||||||||

17 |

|

|

Taxes and licenses |

|

. . . . . . . . . . . . |

17 |

|

|

|

||||||||||||||||||||

limitations |

|

|

|

|

|

|

|||||||||||||||||||||||

20 |

|

|

Depreciation from Form 4562 not claimed on Form |

20 |

|

|

|

||||||||||||||||||||||

|

18 |

|

|

Interest (see instructions) |

|

. . . . . . . . . . . . |

18 |

|

|

|

|||||||||||||||||||

|

19 |

|

|

Charitable contributions |

|

. . . . . . . . . . . . |

19 |

|

|

|

|||||||||||||||||||

for |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

21 |

|

|

Depletion |

|

. . . . . . . . . . . . |

21 |

|

|

|

||||||||||||||||||||

instructions |

25 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

25 |

|

|

|

|||||||||||||||||||

|

22 |

|

|

Advertising |

|

. . . . . . . . . . . . |

22 |

|

|

|

|||||||||||||||||||

|

23 |

|

|

Pension, |

. . . . . . . . . . |

|

. . . . . . . . . . . . |

23 |

|

|

|

||||||||||||||||||

|

24 |

|

|

Employee benefit programs |

. . . . . . . . . . . . |

|

. . . . . . . . . . . . |

24 |

|

|

|

||||||||||||||||||

(See |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

|

|

Other deductions (attach statement) |

|

. . . . . . . . . . . . |

26 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

Deductions |

27 |

|

|

Total deductions. Add lines 12 through 26 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

27 |

|

|

|

|||||||||||

28 |

|

|

Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11. . |

28 |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

29a |

|

Net operating loss deduction (see instructions) |

|

. . . |

. |

|

29a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Special deductions (Schedule C, line 24) |

|

. . . |

. |

|

29b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Add lines 29a and 29b |

|

. . . . . . . . . . . . |

29c |

|

|

||||||||||||||||||||

and |

30 |

|

|

Taxable income. Subtract line 29c from line 28. See instructions . |

|

. . . . . . . . . . . . |

30 |

|

|

|

|||||||||||||||||||

31 |

|

|

Total tax |

(Schedule J, Part I, line 11) |

|

. . . . . . . . . . . . |

31 |

|

|

|

|||||||||||||||||||

Credits,Refundable Payments |

|

|

|

|

|

|

|||||||||||||||||||||||

32 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

32 |

|

|

|

||||||||||||||||||||

|

33 |

|

|

Total payments and credits (Schedule J, Part III, line 23) . . . . |

|

. . . . . . . . . . . . |

33 |

|

|

|

|||||||||||||||||||

|

34 |

|

|

Estimated tax penalty. See instructions. Check if Form 2220 is attached |

. . |

. |

. . |

. . |

. |

. ▶ |

|

|

|

34 |

|

|

|

||||||||||||

|

35 |

|

|

Amount owed. If line 33 is smaller than the total of lines 31 and 34, enter amount owed |

. . . . . . |

35 |

|

|

|

||||||||||||||||||||

Tax, |

36 |

|

|

Overpayment. If line 33 is larger than the total of lines 31 and 34, enter amount overpaid |

36 |

|

|

|

|||||||||||||||||||||

37 |

|

|

Enter amount from line 36 you want: Credited to 2022 estimated tax ▶ |

|

|

|

|

|

|

|

Refunded ▶ |

37 |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Sign |

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, |

||||||||||||||||||||||||||

|

|

and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|

|

|

May the IRS discuss this return |

|

||||||||||||||||||||

Here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

with the preparer shown below? |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions. |

Yes |

No |

||

|

|

|

▲Signature of officer |

|

|

|

Date |

▲ |

|

Title |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

|

Print/Type preparer’s name |

|

|

Preparer’s signature |

|

|

|

|

|

Date |

|

|

|

|

|

Check |

if |

PTIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Firm’s name ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

|

|||||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Firm’s address ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone no. |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

|

|

Cat. No. 11450Q |

|

|

|

|

|

|

|

Form 1120 (2021) |

|||||||||||||||||

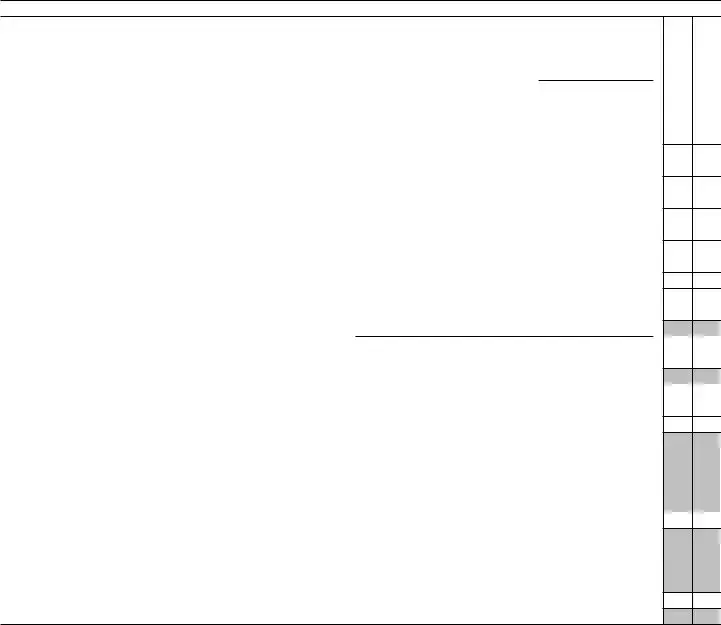

Form 1120 (2021) |

|

|

Page 2 |

|

Schedule C |

Dividends, Inclusions, and Special Deductions (see |

(a) Dividends and |

(b) % |

(c) Special deductions |

|

instructions) |

inclusions |

(a) × (b) |

|

|

|

|||

1Dividends from

stock) |

50 |

2Dividends from

|

stock) |

65 |

|

|

See |

3 |

Dividends on certain |

instructions |

4 |

Dividends on certain preferred stock of |

23.3 |

5 |

Dividends on certain preferred stock of |

26.7 |

6 |

Dividends from |

50 |

7 |

Dividends from |

65 |

8 |

Dividends from wholly owned foreign subsidiaries |

100 |

|

|

See |

9 |

Subtotal. Add lines 1 through 8. See instructions for limitations |

instructions |

10Dividends from domestic corporations received by a small business investment

|

company operating under the Small Business Investment Act of 1958 |

100 |

11 |

Dividends from affiliated group members |

100 |

12 |

Dividends from certain FSCs |

100 |

13

|

corporation (excluding hybrid dividends) (see instructions) |

|

100 |

|

|

14 |

Dividends from foreign corporations not included on line 3, 6, 7, 8, 11, 12, or 13 |

|

|

||

|

(including any hybrid dividends) |

|

|

|

|

15 |

Reserved for future use |

|

|

|

|

16a |

Subpart F inclusions derived from the sale by a controlled foreign corporation (CFC) of |

|

|

||

|

the stock of a |

100 |

|

||

|

(see instructions) |

|

|

||

b |

Subpart F inclusions derived from hybrid dividends of tiered corporations (attach Form(s) |

|

|

||

|

5471) (see instructions) |

|

|

|

|

c |

Other inclusions from CFCs under subpart F not included on line 16a, 16b, or 17 (attach |

|

|

||

|

Form(s) 5471) (see instructions) |

|

|

||

17 |

Global Intangible |

18 |

|

19 |

|

20 |

Other dividends |

21 |

Deduction for dividends paid on certain preferred stock of public utilities . . . . |

22 |

Section 250 deduction (attach Form 8993) |

23Total dividends and inclusions. Add column (a), lines 9 through 20. Enter here and on page 1, line 4 . . . . . . . . . . . . . . . . . . . . . .

24 |

Total special deductions. Add column (c), lines 9 through 22. Enter here and on page 1, line 29b |

Form 1120 (2021)

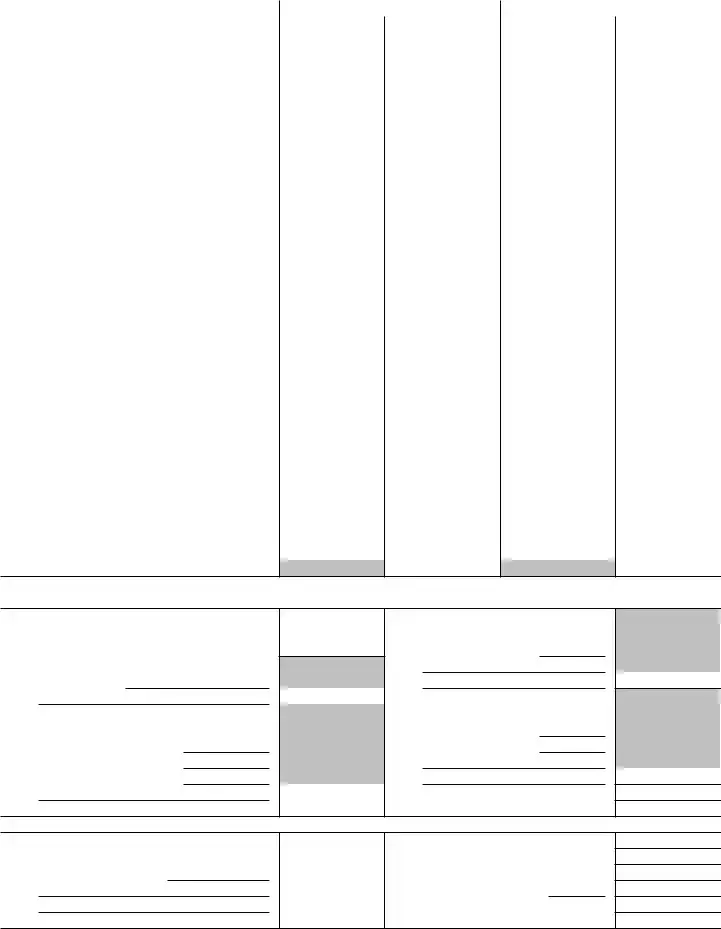

Form 1120 (2021) |

|

|

|

|

|

Page 3 |

|

Schedule J |

Tax Computation and Payment (see instructions) |

|

|

|

|

|

|

Part |

|

|

|

|

|

||

1 |

Check if the corporation is a member of a controlled group (attach Schedule O (Form 1120)). See instructions |

▶ |

|

|

|||

2 |

Income tax. See instructions |

. . . . |

. . . |

2 |

|

||

3 |

Base erosion minimum tax amount (attach Form 8991) |

. . . . |

. . . |

3 |

|

||

4 |

Add lines 2 and 3 |

. . . . |

. . . |

4 |

|

||

5a |

Foreign tax credit (attach Form 1118) |

5a |

|

|

|

|

|

b |

Credit from Form 8834 (see instructions) |

5b |

|

|

|

|

|

c |

General business credit (attach Form 3800) |

5c |

|

|

|

|

|

d |

Credit for prior year minimum tax (attach Form 8827) |

5d |

|

|

|

|

|

e |

Bond credits from Form 8912 |

5e |

|

|

|

|

|

6 |

Total credits. Add lines 5a through 5e |

. . . . |

. . . |

6 |

|

||

7 |

Subtract line 6 from line 4 |

. . . . |

. . . |

7 |

|

||

8 |

Personal holding company tax (attach Schedule PH (Form 1120)) |

. . . . |

. . . |

8 |

|

||

9a |

Recapture of investment credit (attach Form 4255) |

9a |

|

|

|

|

|

b |

Recapture of |

9b |

|

|

|

|

|

c |

Interest due under the |

|

|

|

|

|

|

|

Form 8697) |

9c |

|

|

|

|

|

d |

Interest due under the |

9d |

|

|

|

|

|

e |

Alternative tax on qualifying shipping activities (attach Form 8902) |

9e |

|

|

|

|

|

f |

Interest/tax due under section 453A(c) and/or section 453(l) |

9f |

|

|

|

|

|

g |

Other (see |

9g |

|

|

|

|

|

10 |

Total. Add lines 9a through 9g |

. . . . |

. . . |

10 |

|

||

11 |

Total tax. Add lines 7, 8, and 10. Enter here and on page 1, line 31 |

. . . . |

. . . |

11 |

|

||

Part

12 Reserved for future use . . . . . . . . . . . . . . . . . . . . . . . . . . .

12

Part

13 |

2020 overpayment credited to 2021 |

. . . . . . . . |

13 |

|

|

||

14 |

2021 estimated tax payments |

. . . . . . . . |

14 |

|

|

||

15 |

2021 refund applied for on Form 4466 |

. . . . . . . . |

15 |

( |

) |

||

16 |

Combine lines 13, 14, and 15 |

. . . . . . . . |

16 |

|

|

||

17 |

Tax deposited with Form 7004 |

. . . . . . . . |

17 |

|

|

||

18 |

Withholding (see instructions) |

. . . . . . . . |

18 |

|

|

||

19 |

Total payments. Add lines 16, 17, and 18 |

. . . . . . . . |

19 |

|

|

||

20 |

Refundable credits from: |

|

|

|

|

|

|

a |

Form 2439 |

|

20a |

|

|

|

|

b |

Form 4136 |

|

20b |

|

|

|

|

c |

Reserved for future use |

|

20c |

|

|

|

|

d |

Other (attach |

|

20d |

|

|

|

|

21 |

Total credits. Add lines 20a through 20d |

. . . . . . . . |

21 |

|

|

||

22 |

Reserved for future use |

. . . . . . . . |

22 |

|

|

||

23 |

Total payments and credits. Add lines 19 and 21. Enter here and on page 1, line 33 . |

. . . . . . . . |

23 |

|

|

||

|

|

|

|

|

|

|

Form 1120 (2021) |

Form 1120 (2021) |

Page 4 |

Schedule K Other Information (see instructions)

1 |

Check accounting method: a |

Cash |

b |

Accrual |

c |

Other (specify) ▶ |

2See the instructions and enter the: a Business activity code no. ▶

b Business activity ▶ c Product or service ▶

3 Is the corporation a subsidiary in an affiliated group or a

If “Yes,” enter name and EIN of the parent corporation ▶

4At the end of the tax year:

aDid any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or

corporation’s stock entitled to vote? If “Yes,” complete Part I of Schedule G (Form 1120) (attach Schedule G) . . . . . .

bDid any individual or estate own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all

classes of the corporation’s stock entitled to vote? If “Yes,” complete Part II of Schedule G (Form 1120) (attach Schedule G) .

5At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote of any foreign or domestic corporation not included on Form 851, Affiliations Schedule? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

Yes No

(i)Name of Corporation

(ii)Employer

Identification Number

(if any)

(iii)Country of Incorporation

(iv)Percentage Owned in Voting

Stock

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

(i)Name of Entity

(ii)Employer

Identification Number

(if any)

(iii)Country of Organization

(iv)Maximum

Percentage Owned in Profit, Loss, or Capital

6During this tax year, did the corporation pay dividends (other than stock dividends and distributions in exchange for stock) in

excess of the corporation’s current and accumulated earnings and profits? See sections 301 and 316 . . . . . . . .

If “Yes,” file Form 5452, Corporate Report of Nondividend Distributions. See the instructions for Form 5452. If this is a consolidated return, answer here for the parent corporation and on Form 851 for each subsidiary.

7At any time during the tax year, did one foreign person own, directly or indirectly, at least 25% of the total voting power of all classes of the corporation’s stock entitled to vote or at least 25% of the total value of all classes of the corporation’s stock? .

For rules of attribution, see section 318. If “Yes,” enter:

(a) Percentage owned ▶ |

and (b) Owner’s country ▶ |

(c)The corporation may have to file Form 5472, Information Return of a 25%

8 Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . . . ▶

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

9Enter the amount of

10Enter the number of shareholders at the end of the tax year (if 100 or fewer) ▶

11If the corporation has an NOL for the tax year and is electing to forego the carryback period, check here (see instructions) ▶

If the corporation is filing a consolidated return, the statement required by Regulations section

12Enter the available NOL carryover from prior tax years (do not reduce it by any deduction reported on

page 1, line 29a.) . . . . . . . . . . . . . . . . . . . . . . . . . ▶ $

Form 1120 (2021)

Form 1120 (2021) |

Page 5 |

Schedule K Other Information (continued from page 4)

13 |

Are the corporation’s total receipts (page 1, line 1a, plus lines 4 through 10) for the tax year and its total assets at the end of the |

Yes No |

|

||

|

tax year less than $250,000? |

|

|

If “Yes,” the corporation is not required to complete Schedules L, |

|

|

distributions and the book value of property distributions (other than cash) made during the tax year ▶ $ |

|

14 |

Is the corporation required to file Schedule UTP (Form 1120), Uncertain Tax Position Statement? See instructions . . . . |

|

|

If “Yes,” complete and attach Schedule UTP. |

|

15a |

Did the corporation make any payments in 2021 that would require it to file Form(s) 1099? |

|

b |

If “Yes,” did or will the corporation file required Form(s) 1099? |

|

16During this tax year, did the corporation have an

own stock? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17During or subsequent to this tax year, but before the filing of this return, did the corporation dispose of more than 65% (by value)

of its assets in a taxable,

18Did the corporation receive assets in a section 351 transfer in which any of the transferred assets had a fair market basis or fair

market value of more than $1 million? . . . . . . . . . . . . . . . . . . . . . . . . . . .

19During the corporation’s tax year, did the corporation make any payments that would require it to file Forms 1042 and

20 Is the corporation operating on a cooperative basis?. . . . . . . . . . . . . . . . . . . . . . .

21During the tax year, did the corporation pay or accrue any interest or royalty for which the deduction is not allowed under section

267A? See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” enter the total amount of the disallowed deductions ▶ $

22Does the corporation have gross receipts of at least $500 million in any of the 3 preceding tax years? (See sections 59A(e)(2)

and (3)) . |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

If “Yes,” complete and attach Form 8991.

23Did the corporation have an election under section 163(j) for any real property trade or business or any farming business in effect

|

during the tax year? See instructions |

24 |

Does the corporation satisfy one or more of the following? See instructions |

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense. If “Yes,” complete and attach Form 8990.

25 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|

If “Yes,” enter amount from Form 8996, line 15 . . . . ▶ $ |

26Since December 22, 2017, did a foreign corporation directly or indirectly acquire substantially all of the properties held directly or indirectly by the corporation, and was the ownership percentage (by vote or value) for purposes of section 7874 greater than 50% (for example, the shareholders held more than 50% of the stock of the foreign corporation)? If “Yes,” list the ownership

percentage by vote and by value. See instructions . . . . . . . . . . . . . . . . . . . . . . .

Percentage: By Vote |

By Value |

Form 1120 (2021)

Form 1120 (2021) |

|

|

|

|

|

|

|

|

|

|

|

|

Page 6 |

||

Schedule L |

|

Balance Sheets per Books |

|

|

Beginning of tax year |

|

|

End of tax year |

|

||||||

|

|

|

Assets |

|

|

|

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

||||

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less allowance for bad debts . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|||||

4 |

U.S. government obligations |

. . . . . |

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

|

|

|

|

|

|

|

|

|

|||||

6 |

Other current assets (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

||||

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

||||

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

||||

10a |

Buildings and other depreciable assets . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depreciation . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depletion . . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|||||

13a |

Intangible assets (amortizable only) |

. . . |

|

|

|

|

|

|

|

|

|

|

|||

b |

Less accumulated amortization . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|||||

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|||||

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

||||

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

||||

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

||||

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

||||

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

||||

22 |

Capital stock: |

a Preferred stock . . . . |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

b Common stock . . . . |

|

|

|

|

|

|

|

|

|

|

||

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

||||

24 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

25 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

26 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

27 |

Less cost of treasury stock |

|

|

|

|

( |

) |

|

|

( |

) |

||||

28 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|||||

Schedule

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books |

7 |

Income recorded on books this year |

|

2 |

Federal income tax per books |

|

|

not included on this return (itemize): |

3 |

Excess of capital losses over capital gains . |

|

|

|

4Income subject to tax not recorded on books this year (itemize):

|

|

|

8 |

|

Deductions on this return not charged |

5 |

Expenses recorded on books this year not |

|

against book income this year (itemize): |

||

|

deducted on this return (itemize): |

a |

Depreciation . . $ |

||

a |

Depreciation . . . . $ |

b |

Charitable contributions $ |

||

bCharitable contributions . $

cTravel and entertainment . $

|

|

|

9 |

Add lines 7 and 8 |

6 |

Add lines 1 through 5 |

10 |

Income (page 1, line |

|

Schedule

1 |

Balance at beginning of year |

5 |

Distributions: a Cash |

||

2 |

Net income (loss) per books |

|

|

|

b Stock . . . . |

3 |

Other increases (itemize): |

|

|

|

c Property . . . . |

|

|

|

6 |

Other decreases (itemize): |

|

|

|

|

7 |

Add lines 5 and 6 |

|

4 |

Add lines 1, 2, and 3 |

8 |

Balance at end of year (line 4 less line 7) |

||

Form 1120 (2021)

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Form 1120 is used by U.S. corporations to report their income, gains, losses, deductions, and to calculate their federal income tax liability. |

| Filing Requirement | All domestic corporations must file Form 1120, unless they are exempt under the Internal Revenue Code. |

| Due Date | For corporations operating on a calendar year, Form 1120 is due by April 15. For those on a fiscal year, it's due the 15th day of the 4th month after the end of their fiscal year. |

| Extension Option | Corporations can request a six-month extension to file Form 1120 by submitting Form 7004 before the original due date. |

| Electronic Filing | Most corporations can file Form 1120 electronically through the IRS e-file system. |

| State-Specific Versions | Some states require corporations to file state-specific versions of Form 1120. The requirements and laws governing these forms vary by state. |

Filing out the IRS 1120 form is a necessary step for corporations in the United States to report their income, gains, losses, deductions, and credits. This process helps to determine the amount of tax the corporation owes or the refund it may be entitled to. For those who may feel overwhelmed by the form, the following steps are designed to provide a straightforward guide. Being meticulous and following each step carefully are key to ensuring the accuracy of the information submitted.

Completing the IRS 1120 form is a critical task that requires attention to detail and understanding of the corporation's financial activities throughout the year. By following these steps methodically, corporations can accurately report their financial status and comply with federal tax obligations, helping avoid potential penalties for incorrect or late submissions.

What is an IRS 1120 form?

The IRS 1120 form, known as the U.S. Corporation Income Tax Return, is a document that must be filed by corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). It is used to determine the income tax liability of a corporation.

Who needs to file an IRS 1120 form?

All corporations that operate in the United States and are required to pay federal income taxes must file Form 1120. S corporations, however, file a different form, known as Form 1120S, due to their special tax status which allows them to pass income directly to shareholders to be taxed at individual rates.

When is the IRS 1120 form due?

The deadline for filing Form 1120 is typically the 15th day of the fourth month following the end of the corporation's tax year. For corporations operating on a calendar year, the due date is April 15th. If the due date falls on a weekend or legal holiday, the deadline is extended to the next business day. Corporations can request a six-month extension to file by submitting Form 7004 before the original due date.

What information is required to complete Form 1120?

Corporations must provide a comprehensive range of information when filing Form 1120, including but not limited to:

What happens if you file IRS 1120 late or fail to file?

Filing Form 1120 late or failing to file can result in penalties. The IRS may impose a penalty of 5% of the unpaid taxes for each month or part of a month that the return is late, up to a maximum of 25%. If the return is filed more than 60 days after the due date, the minimum penalty is either $435 or the balance of the tax due on the return, whichever is smaller (as of the last known update in 2023). Interest is also charged on any unpaid taxes.

Can you e-file IRS Form 1120?

Yes, corporations can e-file Form 1120. The IRS encourages electronic filing due to its faster processing time, convenience, and reduced errors compared to paper filing. E-filing can be done through IRS-authorized e-filing providers.

Are there any changes to the IRS 1120 form for the current tax year?

The IRS may make changes to the Form 1120 from year to year to reflect updates in tax laws and regulations. It is important for corporations to refer to the latest version of the form and its instructions, available on the IRS website, to ensure compliance with current tax filing requirements.

Can a corporation receive a refund if they overpay their taxes on Form 1120?

Yes, if a corporation overpays their taxes as reported on Form 1120, they are entitled to receive a refund. The overpayment may be applied to the next year’s estimated tax or refunded directly to the corporation. This choice is made at the time of filing.

How can a corporation amend a previously filed IRS 1120 form?

If a corporation needs to correct or amend a previously filed Form 1120, they should file an amended return using Form 1120X, Amended U.S. Corporation Income Tax Return. This form must be filed within three years from the date the original return was filed, or within two years from the date the tax was paid, whichever is later. It is important to provide a complete explanation of the changes and attach any necessary documentation.

Filling out the IRS 1120 form, which corporations use to report their income, gains, losses, deductions, and credits to the Internal Revenue Service, often involves navigating complex rules and calculations. People tend to make several common mistakes during this process. Recognizing and avoiding these errors can save time, reduce the potential for an audit, and ensure that the company pays the correct amount of taxes.

Not verifying the corporation's information: It is crucial to double-check the accuracy of the corporation's name, address, Employer Identification Number (EIN), and the tax year. Incorrect or outdated information can lead to processing delays or misdirected correspondence.

Incorrectly reporting income: Corporations sometimes make errors by reporting income under the wrong categories or failing to report certain types of income altogether. This mistake can result in inaccurate tax liability calculations.

Failing to document and deduct all allowable expenses: Many corporations miss out on reducing their taxable income because they do not keep thorough records of their expenses or do not know which expenses are deductible.

Miscalculating deductions and credits: Deductions and credits are meant to reduce a corporation’s tax liability. However, errors in calculation or misunderstanding eligibility criteria can lead to missed opportunities for savings or penalties for overstating deductions.

Incorrectly calculating tax due: The tax calculation process involves understanding various tax rates and how they apply to the corporation's income. Mistakes here can either result in overpaying or underpaying taxes.

Not correctly identifying or separating permanent and temporary differences in tax reporting: This affects the corporation’s effective tax rate and deferred tax balances. Misunderstanding these concepts can affect financial statements and future tax liabilities.

Omitting attachments or schedules: The IRS requires certain attachments and schedules for specific deductions, credits, or aspects of income. Failing to include these can result in an incomplete return, requiring further action to rectify.

Not seeking professional advice when needed: Tax laws and regulations are complex and constantly changing. Without specialized knowledge, it’s easy to overlook opportunities or make costly mistakes. Consulting with a tax professional can provide clarity and assurance.

Avoiding these mistakes requires careful attention to detail, a thorough understanding of tax laws relevant to corporations, and, when in doubt, seeking advice from qualified professionals. By doing so, corporations can ensure they meet their legal obligations while optimizing their tax positions.

Businesses operating in the United States use a variety of forms and documents to comply with tax regulations, one of which is the IRS 1120 form. This form is specifically designed for corporations to report their income, gains, losses, deductions, and credits and to figure out their federal income tax liability. Alongside this form, several other documents are often necessary to provide a complete financial picture of the corporation and ensure compliance with tax laws.

Preparing and forwarding these documents with the IRS 1120 form can be quite a task for any business. Each document serves a specific purpose, contributing to a comprehensive assessment of a corporation's financial activities and tax responsibilities. Staying informed and up-to-date with these requirements is essential for businesses to maintain good standing with the IRS and avoid penalties for non-compliance.

IRS 1120-S Form: This document is tailored for S corporations, allowing them to pass income directly to shareholders to avoid double taxation. It's similar to the IRS 1120 form, which is used by C corporations, in that both require detailed income, loss, and tax information. However, the 1120-S includes a schedule for reporting income allocations to shareholders.

IRS 1065 Form: Used by partnerships for tax reporting, this form closely resembles the IRS 1120 in its requirement for detailing income, expenses, and profit distribution. The key difference lies in its design for partnerships, which, like S corporations, pass profits directly to owners, thereby avoiding the corporate tax level.

IRS 1040 Schedule C: Sole proprietors use this form to report business income and expenses. It aligns with the IRS 1120 form in its purpose to detail a business's financial activity. The distinction is that it's for individuals running a business alone, consolidating business and personal taxes into one return.

IRS 990 Form: This is for nonprofit organizations to report their income, expenses, and operational activities. Its similarity with the IRS 1120 form lies in its comprehensive coverage of an organization's financial health. Unlike the 1120, however, it serves nonprofits and includes sections on program service accomplishments and compliance with public charity status.

IRS 1041 Form: Used by estates and trusts, this form reports income, deductions, and beneficiary distributions. It mirrors the financial detail requirement seen in IRS 1120, but is applied to the fiduciary activities of legal entities managing estate or trust resources, including distributions made to beneficiaries.

IRS 8832 Form: This form is for businesses electing their classification for federal tax purposes. While not a tax return like the IRS 1120, it's related in that it can determine how a business entity is taxed—potentially affecting whether the 1120 or another form is relevant for that business's tax responsibilities.

State Corporate Income Tax Returns: Nearly every state requires corporations to file an income tax return. These forms resemble the IRS 1120 as they gather details on income, deductions, and tax liabilities at the state level. The specific form and its contents vary by state, but the overall purpose aligns closely with the federal 1120's objectives of documenting a corporation's financial activities and calculating its tax dues.

Filing your corporation's taxes involves filling out Form 1120 with the Internal Revenue Service (IRS). To ensure accuracy and avoid common pitfalls, here are several do's and don'ts to keep in mind:

Filling out Form 1120 with care and thoroughness can prevent errors and possible audits. Always consider seeking professional advice to ensure your corporation's tax filing is compliant and optimized for your financial situation.

The IRS Form 1120 is the U.S. Corporation Income Tax Return that many corporations are required to file annually. However, there are several misconceptions surrounding this form that may lead to confusion. Clearing up these misunderstandings can help ensure that fields are filled out correctly and that all obligations to the Internal Revenue Service (IRS) are met accurately.

Only Large Corporations Need to File Form 1120: Many small business owners think that IRS Form 1120 is only for large corporations. However, most corporations, regardless of size, are required to file Form 1120 if they are registered as C corporations under United States law.

Filing Form 1120 Grants Automatic Taxation Benefits: Simply filing Form 1120 does not automatically grant corporations taxation benefits. The benefits depend on the specific deductions and credits for which the corporation is eligible and claims on the form.

Form 1120 Is Only for Reporting Income: While reporting income is one of the primary purposes of Form 1120, this form also includes sections for deductions, credits, and other vital tax information. It serves as a comprehensive report on the corporation's taxable activities over the fiscal year.

S Corporations Must File Form 1120: This is a common misconception. S corporations actually file Form 1120S, not Form 1120, which is specifically for C corporations. Choosing the correct form is crucial for compliance with IRS guidelines.

Form 1120 Can Be Filed at Any Time During the Year: The IRS has specific deadlines for when Form 1120 must be filed, usually the 15th day of the fourth month after the end of the company's fiscal year. Extensions are available, but they must be filed timely.

All Corporations Pay the Same Rate on Taxable Income: The federal corporate tax rate may be uniform, but effective tax rates can vary significantly from one corporation to another based on eligible deductions and credits.

Electronic Filing Isn't Necessary: For most corporations, especially those with assets of $10 million or more and that file at least 250 returns annually, electronic filing is required. Smaller corporations are strongly encouraged to file electronically for efficiency and accuracy.

Every Corporation Can Delay Filing Form 1120 Without Penalties: Automatic extensions are available but must be formally requested using Form 7004. Filing late without an extension can result in penalties.

Personal and Business Expenses Are Interchangeable on Form 1120: It's vital to distinguish personal expenses from business expenses clearly. Form 1120 is strictly for business-related financial activities, and blending personal expenses can lead to IRS scrutiny and potential penalties.

Understanding these misconceptions regarding IRS Form 1120 can help corporations navigate their tax obligations more effectively, ensuring compliance and taking advantage of all applicable tax benefits.

Filing an IRS 1120 form is essential for corporations to accurately report their income, gains, losses, deductions, and credits for the tax year. Understanding the key takeaways can make filling out the form a smoother process and help ensure compliance with tax regulations. Here are some crucial points to remember:

By keeping these key points in mind, corporations can navigate the complexities of tax reporting with more confidence. Always consult with a tax professional if there are uncertainties about how to fill out the form or about specific tax situations.

Certificate to Return to Work - Encourages a collaborative approach between employees, health care providers, and employers for a successful work re-entry.

Eagle Project Rules - Preparation of this form often begins well before the actual submission, with Scouts planning their path to Eagle Scout from early on.

Scoring Sheet Basketball - Enables schools to uphold a standardized approach to recording basketball game statistics.