Free IRS 1120-S PDF Template

Free IRS 1120-S PDF Template

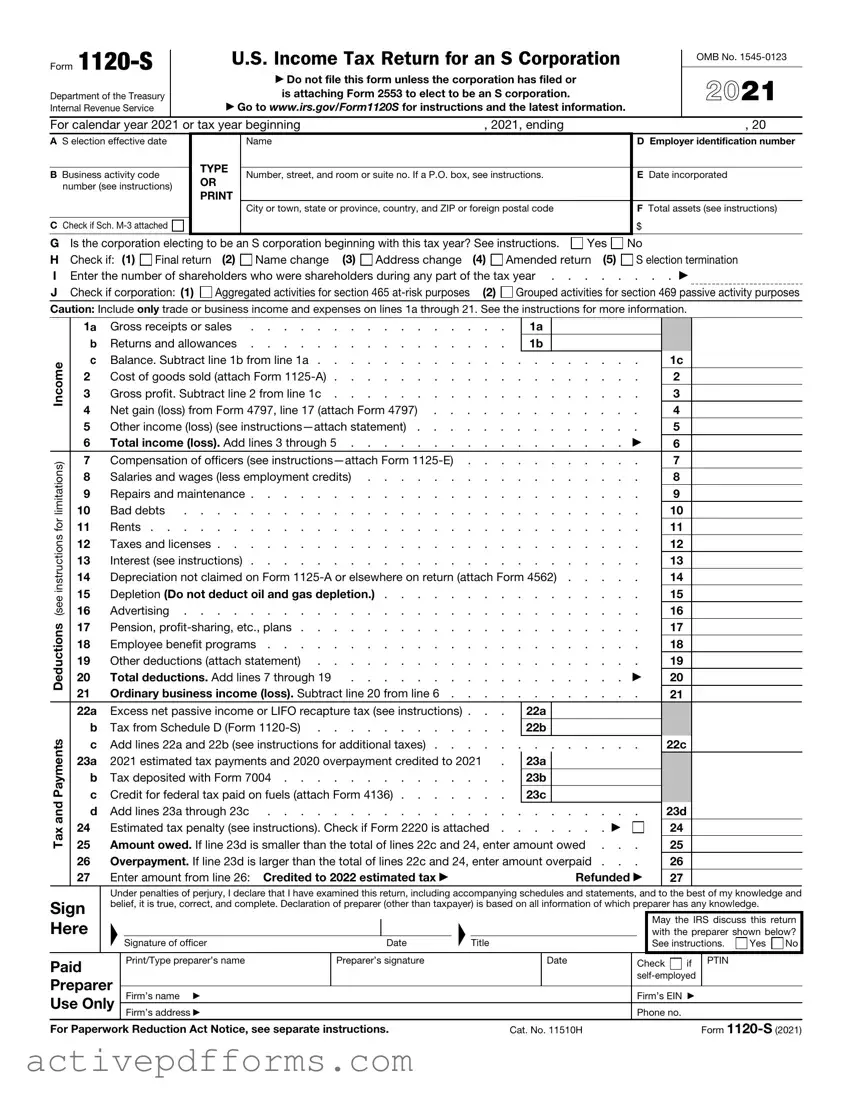

Many businesses in the United States operate as S corporations, a designation that affects how they report income, deductions, and credits to the Internal Revenue Service (IRS). Central to this process is the IRS Form 1120-S, which these corporations must complete annually. This form allows the IRS to assess the overall financial activity of an S corporation, ensuring that income is reported accurately and taxes are calculated correctly. With sections dedicated to income, deductions, and tax computations, the 1120-S form is intricate, requiring detailed attention to ensure all information is accurately reported. It serves not just as a means of tax reporting but also as a tool for S corporations to demonstrate their compliance with tax laws, making its accurate completion a critical aspect of a company's fiscal responsibilities. Understanding this form's major aspects is essential for anyone involved in the financial management of an S corporation, as mistakes can lead to audits, penalties, and interest charges, putting unnecessary strain on the business.

Form |

|

|

|

|

|

U.S. Income Tax Return for an S Corporation |

|

|

OMB No. |

||||

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ Do not file this form unless the corporation has filed or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2021 |

||

Department of the Treasury |

|

|

|

|

|

|

is attaching Form 2553 to elect to be an S corporation. |

|

|

|

|||

Internal Revenue Service |

|

|

|

|

|

▶ Go to www.irs.gov/Form1120S for instructions and the latest information. |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||||

For calendar year 2021 or tax year beginning |

, 2021, ending |

|

, 20 |

||||||||||

A S election effective date |

|

|

|

|

Name |

|

|

|

D Employer identification number |

||||

|

|

|

|

|

TYPE |

|

|

|

|

|

|

||

B |

Business activity code |

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

|

E Date incorporated |

|||||||

|

OR |

|

|

|

|||||||||

|

number (see instructions) |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

F Total assets (see instructions) |

||

|

|

|

|

|

|

|

|

|

|

|

|||

C Check if Sch. |

|

|

|

|

|

|

|

|

$ |

|

|||

G Is the corporation electing to be an S corporation beginning with this tax year? See instructions. |

Yes |

No |

|||||||||||

H |

Check if: (1) Final return |

|

(2) Name change (3) Address change |

(4) Amended return (5) |

|

S election termination |

|||||||

I |

Enter the number of shareholders who were shareholders during any part of the tax year |

|

. . . ▶ |

||||||||||

J |

Check if corporation: (1) |

|

Aggregated activities for section 465 |

(2) Grouped activities for section 469 passive activity purposes |

|||||||||

Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Tax and Payments Deductions (see instructions for limitations) Income

1a |

Gross receipts or sales |

|

1a |

|

|

|

|

|

|

b |

Returns and allowances |

|

1b |

|

|

|

|

|

|

c |

Balance. Subtract line 1b from line 1a |

. . . . . . . . |

1c |

|

|||||

2 |

Cost of goods sold (attach Form |

. . . . . . . . |

2 |

|

|||||

3 |

Gross profit. Subtract line 2 from line 1c |

. . . . . . . . |

3 |

|

|||||

4 |

Net gain (loss) from Form 4797, line 17 (attach Form 4797) |

. . . . . . . . |

4 |

|

|||||

5 |

Other income (loss) (see |

. . . . . . . . |

5 |

|

|||||

6 |

Total income (loss). Add lines 3 through 5 |

. . . . |

. |

. . |

▶ |

6 |

|

||

7 |

Compensation of officers (see |

. . . . . . . . |

7 |

|

|||||

8 |

Salaries and wages (less employment credits) |

. . . . . . . . |

8 |

|

|||||

9 |

Repairs and maintenance |

. . . . . . . . |

9 |

|

|||||

10 |

Bad debts |

. . . . . . . . |

10 |

|

|||||

11 |

Rents |

. . . . . . . . |

11 |

|

|||||

12 |

Taxes and licenses |

. . . . . . . . |

12 |

|

|||||

13 |

Interest (see instructions) |

. . . . . . . . |

13 |

|

|||||

14 |

Depreciation not claimed on Form |

14 |

|

||||||

15 |

Depletion (Do not deduct oil and gas depletion.) |

. . . . . . . . |

15 |

|

|||||

16 |

Advertising |

. . . . . . . . |

16 |

|

|||||

17 |

Pension, |

. . . . . . . . |

17 |

|

|||||

18 |

Employee benefit programs |

. . . . . . . . |

18 |

|

|||||

19 |

Other deductions (attach statement) |

. . . . . . . . |

19 |

|

|||||

20 |

Total deductions. Add lines 7 through 19 |

. . . . |

. |

. . |

▶ |

20 |

|

||

21 |

Ordinary business income (loss). Subtract line 20 from line 6 . . . . |

. . . . . . . . |

21 |

|

|||||

22a |

Excess net passive income or LIFO recapture tax (see instructions) . . . |

|

22a |

|

|

|

|

|

|

b |

Tax from Schedule D (Form |

|

22b |

|

|

|

|

|

|

c |

Add lines 22a and 22b (see instructions for additional taxes) |

. . . . . . . . |

22c |

|

|||||

23a |

2021 estimated tax payments and 2020 overpayment credited to 2021 . |

|

23a |

|

|

|

|

|

|

b |

Tax deposited with Form 7004 |

|

23b |

|

|

|

|

|

|

c |

Credit for federal tax paid on fuels (attach Form 4136) |

|

23c |

|

|

|

|

|

|

d |

Add lines 23a through 23c |

. . . . . . . . |

23d |

|

|||||

24 |

Estimated tax penalty (see instructions). Check if Form 2220 is attached . |

. . . . |

. |

. ▶ |

|

24 |

|

||

25 |

Amount owed. If line 23d is smaller than the total of lines 22c and 24, enter amount owed . . . |

25 |

|

||||||

26 |

Overpayment. If line 23d is larger than the total of lines 22c and 24, enter amount overpaid . . . |

26 |

|

||||||

27 |

Enter amount from line 26: Credited to 2022 estimated tax ▶ |

|

|

|

Refunded ▶ |

27 |

|

||

|

|

|

|

|

|

|

|

|

|

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

▲ |

|

|

▲ |

|

|

May the IRS discuss this return |

||

|

|

|

||||||

|

|

|

|

with the preparer shown below? |

||||

Signature of officer |

Date |

Title |

|

See instructions. |

Yes |

No |

||

|

|

|

|

|

|

|

|

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

Check |

if |

PTIN |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

||

Preparer |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Firm’s name ▶ |

|

|

|

Firm’s EIN ▶ |

|

|

||

Use Only |

|

|

|

|

|

|||

Firm’s address ▶ |

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

|

||

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11510H |

|

|

Form |

|

|||

Form |

Page 2 |

|

Schedule B |

|

Other Information (see instructions) |

1 Check accounting method: a |

Cash |

b |

Accrual |

c

Other (specify) ▶

Other (specify) ▶

2 See the instructions and enter the:

a Business activity ▶ |

b Product or service ▶ |

3At any time during the tax year, was any shareholder of the corporation a disregarded entity, a trust, an estate, or a nominee or similar person? If “Yes,” attach Schedule

4At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total stock issued and outstanding of any foreign or domestic corporation? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v)

below . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Yes No

(i)Name of Corporation

(ii)Employer Identification

Number (if any)

(iii)Country of Incorporation

(iv)Percentage of Stock Owned

(v)If Percentage in (iv) Is 100%, Enter the Date (if applicable) a Qualified Subchapter

S Subsidiary Election Was Made

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v) below . . . . . . .

(i)Name of Entity

(ii)Employer Identification

Number (if any)

(iii)Type of Entity

(iv)Country of Organization

(v)Maximum Percentage Owned in Profit, Loss, or Capital

5a At the end of the tax year, did the corporation have any outstanding shares of restricted stock? . . . . . . . .

If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of restricted stock |

▶ |

(ii) |

Total shares of |

▶ |

bAt the end of the tax year, did the corporation have any outstanding stock options, warrants, or similar instruments? . If “Yes,” complete lines (i) and (ii) below.

(i) |

Total shares of stock outstanding at the end of the tax year |

. ▶ |

(ii)Total shares of stock outstanding if all instruments were executed ▶

6Has this corporation filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide

|

information on any reportable transaction? |

. . . . . . . . . . . . . . . . . . . . . . . . |

7 |

Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . ▶ |

|

|

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount |

|

|

Instruments. |

|

8If the corporation (a) was a C corporation before it elected to be an S corporation or the corporation acquired an asset with a basis determined by reference to the basis of the asset (or the basis of any other property) in the hands of a C corporation, and

(b) has net unrealized

gain reduced by net recognized

9Did the corporation have an election under section 163(j) for any real property trade or business or any farming business

in effect during the tax year? See instructions . . . . . . . . . . . . . . . . . . . . . . . .

10 Does the corporation satisfy one or more of the following? See instructions . . . . . . . . . . . . . .

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense.

If “Yes,” complete and attach Form 8990.

11 Does the corporation satisfy both of the following conditions? . . . . . . . . . . . . . . . . . .

aThe corporation’s total receipts (see instructions) for the tax year were less than $250,000.

bThe corporation’s total assets at the end of the tax year were less than $250,000. If “Yes,” the corporation is not required to complete Schedules L and

Form

Form |

Page 3 |

|

Schedule B |

Other Information (see instructions) (continued) |

Yes No |

12During the tax year, did the corporation have any

terms modified so as to reduce the principal amount of the debt? . . . . . . . . . . . . . . . . .

If “Yes,” enter the amount of principal reduction . . . . . . . . . . . . . . ▶ $

13During the tax year, was a qualified subchapter S subsidiary election terminated or revoked? If “Yes,” see instructions .

14a Did the corporation make any payments in 2021 that would require it to file Form(s) 1099? |

|

|||||||||||

b |

If “Yes,” did the corporation file or will it file required Form(s) 1099? |

|

||||||||||

15 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|||||||||||

|

If “Yes,” enter the amount from Form 8996, line 15 |

. . . . ▶ $ |

|

|

|

|

||||||

Schedule K |

Shareholders’ Pro Rata Share Items |

|

|

|

|

|

|

|

Total amount |

|||

|

|

1 |

Ordinary business income (loss) (page 1, line 21) |

. . . . . . |

. . |

1 |

|

|

||||

|

|

2 |

Net rental real estate income (loss) (attach Form 8825) |

. . . . . . |

. . |

2 |

|

|

||||

|

|

3a |

Other gross rental income (loss) |

|

3a |

|

|

|

|

|

||

|

|

b |

Expenses from other rental activities (attach statement) |

. . . . |

|

3b |

|

|

|

|

|

|

|

|

c |

Other net rental income (loss). Subtract line 3b from line 3a . . . |

. . . . . . |

. . |

3c |

|

|||||

(Loss) |

|

4 |

Interest income |

. . . . . . |

. . |

4 |

|

|

||||

|

5 |

Dividends: a Ordinary dividends |

. . . . . . |

. . |

5a |

|

|

|||||

|

|

|

||||||||||

Income |

|

|

b Qualified dividends |

|

5b |

|

|

|

|

|

||

|

6 |

Royalties |

. . . . . . |

. . |

6 |

|

|

|||||

|

|

|

|

|||||||||

|

|

7 |

Net |

. . . . . . |

. . |

7 |

|

|

||||

|

|

8a |

Net |

. . . . . . |

. . |

8a |

|

|||||

|

|

b |

Collectibles (28%) gain (loss) |

|

8b |

|

|

|

|

|

||

|

|

c |

Unrecaptured section 1250 gain (attach statement) |

|

8c |

|

|

|

|

|

||

|

|

9 |

Net section 1231 gain (loss) (attach Form 4797) |

. . . . . . |

. . |

9 |

|

|

||||

|

|

10 |

Other income (loss) (see instructions) . . . |

Type ▶ |

|

|

|

|

|

10 |

|

|

Deductions |

|

11 |

Section 179 deduction (attach Form 4562) |

. . . . . . |

. . |

11 |

|

|

||||

|

12a |

Charitable contributions |

. . . . . . |

. . |

12a |

|

|

|||||

|

|

|

||||||||||

|

|

b |

Investment interest expense |

. . . . . . |

. . |

12b |

|

|||||

|

|

c |

Section 59(e)(2) expenditures |

Type ▶ |

|

|

|

|

|

12c |

|

|

|

|

d |

Other deductions (see instructions) . . . . |

Type ▶ |

|

|

|

|

|

12d |

|

|

|

|

13a |

. . . . . . |

. . |

13a |

|

||||||

|

|

b |

. . . . . . |

. . |

13b |

|

||||||

Credits |

|

c |

Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) |

. . |

13c |

|

||||||

|

d |

Other rental real estate credits (see instructions) |

Type ▶ |

|

|

|

|

|

13d |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

e |

Other rental credits (see instructions) . . . |

Type ▶ |

|

|

|

|

|

13e |

|

|

|

|

f |

Biofuel producer credit (attach Form 6478) |

. . . . . . |

. . |

13f |

|

|||||

|

|

g |

Other credits (see instructions) |

Type ▶ |

|

|

|

|

|

13g |

|

|

International Transactions |

|

14 |

Attach Schedule |

|

|

|

||||||

|

|

|

|

|

||||||||

|

|

|

check this box to indicate you are reporting items of international tax relevance . . . |

▶ |

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||

Alternative MinimumTax Items(AMT) |

15a |

. . . . . . |

. . |

15a |

|

|||||||

b |

Adjusted gain or loss |

. . . . . . |

. . |

15b |

|

|||||||

c |

Depletion (other than oil and gas) |

. . . . . . |

. . |

15c |

|

|

||||||

|

|

|

||||||||||

|

|

d |

Oil, gas, and geothermal |

. . . . . . |

. . |

15d |

|

|||||

|

|

e |

Oil, gas, and geothermal |

. . . . . . |

. . |

15e |

|

|||||

|

|

f |

Other AMT items (attach statement) |

. . . . . . |

. . |

15f |

|

|||||

ItemsAffecting ShareholderBasis |

|

16a |

. . . . . . |

. . |

16a |

|

||||||

|

f |

Foreign taxes paid or accrued |

. . . . . . |

. . |

16f |

|

||||||

|

|

b |

Other |

. . . . . . |

. . |

16b |

|

|||||

|

|

c |

Nondeductible expenses |

. . . . . . |

. . |

16c |

|

|||||

|

|

d |

Distributions (attach statement if required) (see instructions) . . . |

. . . . . . |

. . |

16d |

|

|||||

|

|

e |

Repayment of loans from shareholders |

. . . . . . |

. . |

16e |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

|

Form |

|

|

Page 4 |

|||

Schedule K |

|

Shareholders’ Pro Rata Share Items (continued) |

|

Total amount |

||

|

Information |

17a |

Investment income |

17a |

||

Other |

d |

Other items and amounts (attach statement) |

|

|

||

|

|

b |

Investment expenses |

17b |

||

|

|

c |

Dividend distributions paid from accumulated earnings and profits |

17c |

||

|

|

|

|

|

|

|

Recon- |

ciliation |

18 |

|

Income (loss) reconciliation. Combine the amounts on lines 1 through 10 in the far right |

|

|

|

|

|

|

|

||

|

|

|

|

column. From the result, subtract the sum of the amounts on lines 11 through 12d and 16f . |

18 |

|

Schedule L |

Balance Sheets per Books |

|

Beginning of tax year |

|

|

End of tax year |

|||||

|

|

Assets |

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less allowance for bad debts |

( |

|

) |

|

|

( |

) |

|

|

|

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|

4 |

U.S. government obligations |

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

||

6 |

Other current assets (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

10a |

Buildings and other depreciable assets . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated depreciation |

( |

|

) |

|

|

( |

) |

|

|

|

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated depletion |

( |

|

) |

|

|

( |

) |

|

|

|

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|

13a |

Intangible assets (amortizable only) . . . . |

|

|

|

|

|

|

|

|

|

|

b |

Less accumulated amortization |

( |

|

) |

|

|

( |

) |

|

|

|

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

22 |

Capital stock |

|

|

|

|

|

|

|

|

|

|

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

24 |

Retained earnings |

|

|

|

|

|

|

|

|

|

|

25 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

26 |

Less cost of treasury stock |

|

|

|

( |

) |

|

|

( |

) |

|

27 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Form |

Page 5 |

|

Schedule |

Reconciliation of Income (Loss) per Books With Income (Loss) per Return |

|

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books . . . . |

|

|

5 |

|

Income recorded on books this year |

|

|

|||

2 |

Income included on Schedule K, lines 1, 2, |

|

|

|

|

not included on Schedule K, lines 1 |

|

|

|||

|

|

|

|

through 10 (itemize): |

|

|

|

||||

|

3c, 4, 5a, 6, 7, 8a, 9, and 10, not recorded |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||

|

on books this year (itemize) |

|

|

a |

|

|

|

|

|||

3 |

Expenses recorded on books this year |

|

|

6 |

|

Deductions included on Schedule K, |

|

|

|||

|

|

|

|

|

|||||||

|

not included on Schedule K, lines 1 |

|

|

|

|

lines 1 through 12 and 16f, not charged |

|

|

|||

|

through 12 and 16f (itemize): |

|

|

|

|

against book income this year (itemize): |

|

|

|||

a |

Depreciation $ |

|

|

a |

|

Depreciation $ |

|

|

|

||

b |

Travel and entertainment $ |

|

|

7 |

|

Add lines 5 and 6 |

|

|

|||

|

|

|

|

|

|||||||

|

|

|

|

|

8 Income (loss) (Schedule K, line 18). |

|

|

||||

4 |

Add lines 1 through 3 |

|

|

|

|

Subtract line 7 from line 4 . . . . |

|

|

|||

Schedule |

Analysis of Accumulated Adjustments Account, Shareholders’ Undistributed Taxable Income |

|

|||||||||

|

|

Previously Taxed, Accumulated Earnings and Profits, and Other Adjustments Account |

|

||||||||

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Accumulated |

|

(b) Shareholders’ |

|

(c) Accumulated |

(d) Other adjustments |

|

|

|

|

|

|

adjustments account |

|

undistributed taxable |

|

earnings and profits |

account |

|

|

|

|

|

|

|

|

|

income previously taxed |

|

|

|

|

1 |

Balance at beginning of tax year |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

2 |

Ordinary income from page 1, line 21 . . . |

|

|

|

|

|

|

|

|

||

3 |

Other additions |

|

|

|

|

|

|

|

|

||

4 |

Loss from page 1, line 21 |

( |

|

) |

|

|

|

|

|

||

5 |

Other reductions |

( |

|

) |

|

|

|

( |

) |

||

6 |

Combine lines 1 through 5 |

|

|

|

|

|

|

|

|

||

7 |

Distributions |

|

|

|

|

|

|

|

|

||

8 |

Balance at end of tax year. Subtract line 7 from |

|

|

|

|

|

|

|

|

||

|

line 6 |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Form |

|

| Fact Name | Description |

|---|---|

| Purpose of Form 1120-S | Used by S corporations to report their income, gains, losses, deductions, credits, and other financial activities to the Internal Revenue Service (IRS). |

| Eligibility to File | Only corporations that have elected to be treated as S corporations for tax purposes are eligible to file Form 1120-S. |

| Due Date | The form is typically due on March 15th of each year for corporations operating on a calendar-year basis. For those on a fiscal-year basis, it is due the 15th day of the 3rd month after the end of their tax year. |

| Requirement for Shareholders | Each shareholder’s share of the corporation's income, deductions, and credits is reported on Schedule K-1 and must be included on their personal tax returns. |

| Pass-Through Taxation | S corporations benefit from pass-through taxation, where the income is taxed at the shareholder level, not at the corporate level. |

| State-Specific Forms | Some states require S corporations to file additional forms. The necessity and type of these forms depend on the state’s tax laws governing S corporations. |

| Penalties for Late Filing | Failure to file Form 1120-S by the due date may result in penalties, which accrue each month the return is late. |

| Electronic Filing | The IRS encourages the electronic filing of Form 1120-S, as it facilitates faster processing and reduces errors. |

Filing the IRS 1120-S form is a crucial step for S corporations in the United States. This form helps these businesses report their income, gains, losses, deductions, credits, and other financial information for the tax year. Correctly completing this document ensures compliance with tax obligations and avoids potential penalties. The process might seem overwhelming at first, but breaking it down into manageable steps can simplify it. Here's a concise guide to help you navigate through each section of the form methodically.

After submitting the IRS 1120-S form, the next steps will involve waiting for confirmation from the IRS that the form has been received and processed. This might include a notice of acceptance, a request for additional information, or a notification of any discrepancies that need to be addressed. It's important to respond promptly to any requests from the IRS to avoid delays in processing. Keeping a copy of the filled-out form and all supporting documents is advisable for record-keeping and future reference. Remember, staying organized and proactive with tax obligations is key to a smooth and compliant tax filing process.

What is the IRS 1120-S form?

The IRS 1120-S form is a tax document filed by S corporations for the purpose of reporting their annual income, deductions, gains, losses, etc. This form allows S corporations to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. The shareholders then report the income and losses on their own individual income tax returns. This process avoids double taxation, which is typical in traditional C corporations.

Who needs to file the IRS 1120-S form?

Any business entity that has elected to be treated as an S corporation by filing IRS Form 2553 and has received IRS approval must file the 1120-S form. This is a requirement for all S corporations, regardless of the level of their assets, receipts, or the number of shareholders. It is important for entities to file this form to maintain their S corporation status and comply with federal tax obligations.

When is the IRS 1120-S form due?

The filing deadline for the IRS 1120-S form is March 15 of the year following the reporting year. If March 15 falls on a weekend or a legal holiday, the deadline is extended to the next business day. It is crucial for S corporations to adhere to this deadline to avoid penalties and interest for late filing. An extension of time to file the IRS 1120-S form can be requested by filing IRS Form 7004 before the due date.

What are the penalties for not filing or late filing of the IRS 1120-S form?

It is in the best interest of an S corporation to file on time or request an extension if needed to mitigate possible penalties.

What are the main components of the IRS 1120-S form?

The IRS 1120-S form includes several parts that require detailed information about the S corporation's financial activities during the tax year. Key sections include:

Accuracy in compiling these components is critical to correctly calculate the tax responsibilities of the corporation and its shareholders.

How can an S corporation file the IRS 1120-S form?

S corporations can file the IRS 1120-S form either electronically through an IRS-authorized e-file provider or by mailing a paper return directly to the IRS. Electing to file electronically is often faster, safer, and ensures a quicker response from the IRS regarding the status of the submission. If mailing, it is important to use the correct address designated by the IRS for 1120-S filings, which can vary depending on the state in which the S corporation is located and whether a payment is being included with the return.

Filling out IRS Form 1120-S, which is the tax return document used by S corporations, requires careful attention to detail. Despite the best efforts of many, mistakes can happen, leading to delays or issues with the Internal Revenue Service (IRS). Below are nine common errors to watch out for when completing this important form:

Not checking the tax year box correctly - It's crucial to indicate the correct tax year for the return. A simple oversight here can lead to unnecessary confusion and correspondence with the IRS.

Failing to report all income - All income must be reported accurately. This includes both domestic and foreign income streams. Missing income can lead to penalties.

Mistakes in reporting shareholder compensation - Compensation paid to shareholders must be reported accurately. Both wages and distributions need careful calculation to avoid misrepresentation.

Incorrectly deducting expenses - Not all expenses a business incurs are deductible. It's critical to understand which expenses can be deducted to avoid potential issues with the IRS.

Forgetting to sign and date the form - An unsigned form is like an unsigned check – it's not valid. Ensure that the form is properly signed and dated before submission.

Miscalculating the tax due or refund - Errors in calculations can either lead to underpaying taxes and incurring penalties or overpaying and missing out on funds that could be utilized elsewhere in the business.

Omitting necessary schedules and attachments - The 1120-S form often requires additional schedules and attachments. Missing these can lead to incomplete filing and requests for further information from the IRS.

Using the wrong form version - Tax forms are updated periodically. Using an outdated version can result in the rejection of the submission.

Not keeping a copy of the filed return - Always keep a copy of the tax return and all supporting documents. This is crucial for future reference or in case of an IRS audit.

By avoiding these common mistakes, S corporations can ensure a smoother process when filing their IRS Form 1120-S. It's always recommended to consult with a tax professional to ensure accuracy and compliance with current tax laws and regulations.

When preparing and filing taxes, owners of S corporations utilize the IRS 1120-S form to report their income, gains, losses, deductions, credits, etc. However, this crucial form is often accompanied by additional documents that are necessary to provide a fuller picture of the corporation's financial activities throughout the fiscal year. Understanding these forms and documents can greatly simplify the tax preparation process, ensuring compliance and potentially optimizing the financial outcomes for both the corporation and its shareholders.

Overall, these forms and documents complement the IRS 1120-S form, each serving a unique purpose in the tax preparation and filing process. Properly managing and understanding these documents not only ensures compliance with tax laws but also helps in the strategic planning and financial management of an S corporation. Whether it's detailing income and expenses, reporting on specific tax situations, or providing necessary information for shareholder tax returns, these forms are integral to a thorough and accurate tax filing.

If you're navigating the world of business taxes, IRS Form 1120-S probably sounds familiar. It's the form used by S corporations to report their income, deductions, and credits to the Internal Revenue Service. However, it's not the only form on the block. There are several others, each serving its unique purpose. Here's a look at six documents similar to IRS 1120-S, shedding light on the tapestry of tax reporting forms.

Understanding these forms illuminates the diverse landscape of tax reporting for different types of entities. Whether operating as a partnership, corporation, nonprofit, homeowners' association, or a trust, there's a specific form that caters to each entity's unique fiscal responsibilities to the IRS.

Filing the IRS 1120-S form, which is essential for S corporations to submit their annual tax returns, requires careful attention to detail. To avoid common pitfalls and ensure the process is as smooth as possible, here are some dos and don'ts:

Do:Make sure your corporation qualifies as an S corporation under the IRS definitions before filing.

Use accurate and complete financial information from your company's records to fill out the form.

Double-check the corporation's EIN (Employer Identification Number) to ensure it's correctly entered.

List all shareholders and their correct proportion of shares to report income, deductions, and credits accordingly.

Take advantage of the IRS instructions for filling out the 1120-S form to clarify any confusion.

Ensure all necessary schedules and attachments are completed and included with your form.

Sign and date the form; an unsigned form is like not filing at all.

Keep a copy of the filed form and all relevant documents for your records.

Consider electronic filing for a faster and more secure submission process.

Consult with a tax professional if you encounter complex issues or have doubts about the correct procedure.

Don't file the form without first obtaining consent from all shareholders.

Don't leave any required fields blank; if something doesn't apply, enter "N/A" or "0" as appropriate.

Don't mix up personal finances with the corporation's finances.

Don't underestimate or overestimate income or deductions without proper documentation to back up your figures.

Don't forget to report all types of income, including ordinary business income, dividends, and interest.

Don't neglect state filing requirements, which may be different from federal requirements.

Don't miss the filing deadline to avoid penalties and interest.

Don't use outdated forms; always check that you are using the current year's form.

Don't attempt to hide or manipulate information to reduce tax liability. Such actions can lead to audits and penalties.

Don't hesitate to seek help from the IRS or a tax professional if you're unsure about any aspect of your filing.

Filing taxes can be daunting, especially for businesses that navigate the complex landscape of tax forms and regulations. The IRS Form 1120-S, used by S corporations, is no stranger to misconceptions. Let's address some common misunderstandings to clear up confusion and provide clarity for interested parties.

Only profits are reported: A common misconception is that the IRS Form 1120-S requires only the reporting of profits. However, both profits and losses must be reported on the form. This documentation helps the IRS understand the company's financial health and ensures accurate tax liability calculations.

It’s only for tax payments: Some believe this form is solely for making tax payments. In truth, the 1120-S form is mainly used to report the income, losses, deductions, and credits of an S corporation, distributing this information to the shareholders accordingly. The actual tax payments are typically made by the individual shareholders, not directly through this form.

Shareholder salaries are not reported: Another misunderstanding is that salaries paid to shareholders do not need to be reported on the 1120-S. Salaries paid to shareholders for services rendered are indeed reported on the form as part of the corporation's deductible business expenses.

Deadlines are the same for all corporations: The assumption that all corporations, including S corporations, face the same tax filing deadlines is incorrect. Specifically, S corporations must file Form 1120-S by the 15th day of the third month after the end of their tax year, which is March 15 for those on a calendar year — a month earlier than the deadline for C corporations.

State taxes don’t matter: Some might think that filing the 1120-S exempts them from state taxes. This misconception overlooks that while the 1120-S is a federal form, S corporations may still be liable for state taxes, and regulations vary by state. It’s crucial for S corporations to understand and comply with the specific tax obligations within their states.

Any business can file as an S corporation: It’s commonly misunderstood that any business can choose to file as an S corporation by simply submitting Form 1120-S. In reality, there are stringent eligibility criteria, including limits on the number and type of shareholders and the issuance of one class of stock, among others.

Income is taxed twice: A frequent misconception is that income reported on Form 1120-S is taxed twice. However, S corporations are pass-through entities, meaning the income is taxed only at the shareholder level, not at the corporate level. This structure avoids the double taxation commonly associated with C corporations.

Filing is optional for S corporations: Lastly, there's a belief that filing Form 1120-S is optional for S corporations. This assumption is false; once a corporation has elected S corporation status, it is required to file Form 1120-S annually, regardless of its income level, to maintain compliance with IRS regulations.

Understanding these misconceptions about the IRS Form 1120-S can demystify the process for S corporations, allowing for more accurate and compliant tax filings. It’s always recommendable to consult with a tax professional to navigate the specifics of corporate tax obligations.

Filing the IRS 1120-S form, required for S corporations, is a critical task that ensures these entities comply with U.S. tax laws. Understanding the key aspects of this form can help streamline the process, avoid common pitfalls, and take advantage of potential benefits. Here are four crucial takeaways anyone involved in this process should know:

How Much Does a 4 Point Inspection Cost in Florida - Inspection forms must be completed and signed by verifiable Florida-licensed professionals, underscoring the reliability and authority of the evaluation.

Tanzania Visum - Keep a copy of your completed form and any confirmation receipts, as you might need to present them upon arrival in Tanzania.

Il444-2790 - Vehicle use for business purposes is accommodated in the expenses section, allowing for a deduction based on percentage of business usage.