Free IRS 433-A PDF Template

Free IRS 433-A PDF Template

When individuals find themselves in a situation where they owe more taxes than they can afford to pay, navigating the solution can be a daunting task. The IRS understands that circumstances such as this can arise, which is why the IRS 433-A form exists. This critical document plays a pivotal role for taxpayers seeking to establish payment plans or achieve an offer in compromise with the IRS. Essentially, it provides the IRS with detailed information about the taxpayer's financial situation, including income, expenses, and asset information. This comprehensive financial snapshot allows the IRS to assess the taxpayer's ability to pay their debt. The form is designed to be thorough, ensuring that the IRS can make an informed decision regarding payment arrangements that are both fair and manageable for the taxpayer. Understanding the major aspects of this form is the first step towards resolving tax debt in a manner that considers the taxpayer's financial reality.

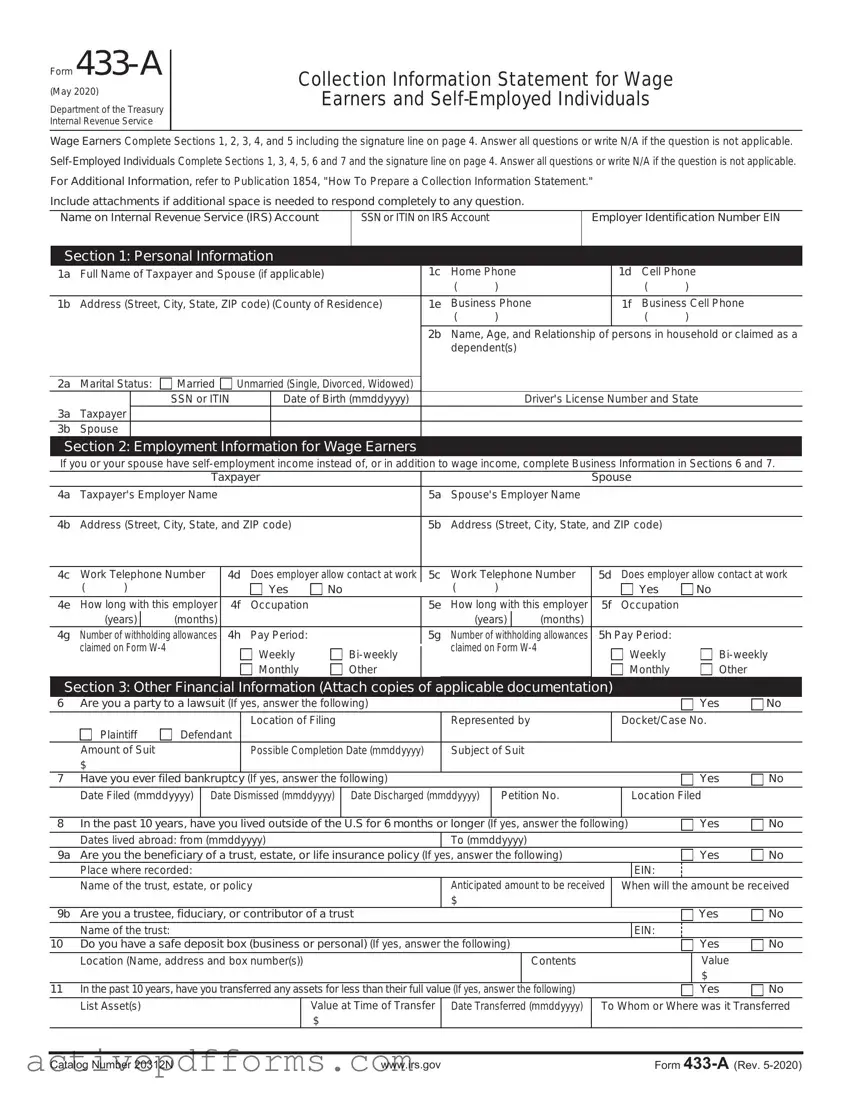

Form

(May 2020)

Department of the Treasury Internal Revenue Service

Collection Information Statement for Wage

Earners and

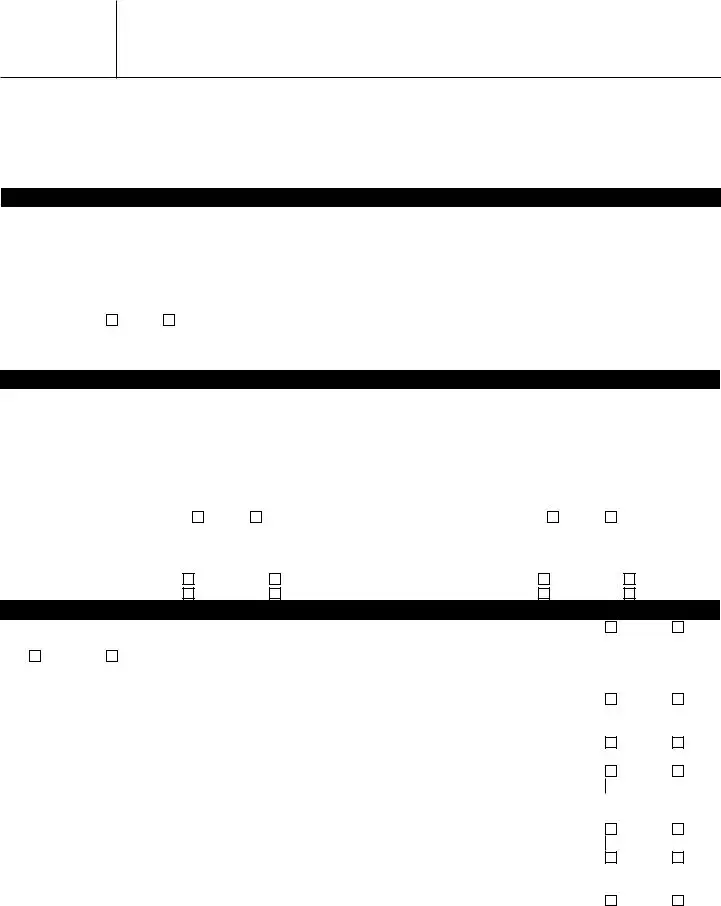

Wage Earners Complete Sections 1, 2, 3, 4, and 5 including the signature line on page 4. Answer all questions or write N/A if the question is not applicable.

For Additional Information, refer to Publication 1854, "How To Prepare a Collection Information Statement."

Include attachments if additional space is needed to respond completely to any question.

Name on Internal Revenue Service (IRS) Account |

SSN or ITIN on IRS Account |

Employer Identification Number EIN |

|

|

|

Section 1: Personal Information

1a |

Full Name of Taxpayer and Spouse (if applicable) |

1c |

Home Phone |

1d |

Cell Phone |

|||||||

|

|

|

|

|

|

|

( |

) |

|

( |

) |

|

1b |

Address (Street, City, State, ZIP code) (County of Residence) |

1e |

Business Phone |

1f |

Business Cell Phone |

|||||||

|

|

|

|

|

|

|

( |

) |

|

( |

) |

|

|

|

|

|

|

|

2b |

Name, Age, and Relationship of |

persons in household or claimed as a |

|

|||

|

|

|

|

|

|

|

dependent(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2a |

Marital Status: |

Married |

Unmarried (Single, Divorced, Widowed) |

|

|

|

|

|

|

|

||

3a |

Taxpayer |

|

SSN or ITIN |

|

Date of Birth (mmddyyyy) |

|

|

Driver's License Number and State |

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

3b |

Spouse |

|

|

|

|

|

|

|

|

|

|

|

Section 2: Employment Information for Wage Earners

If you or your spouse have

|

|

|

|

Taxpayer |

|

|

|

|

|

|

|

Spouse |

|

|

||

4a |

Taxpayer's Employer Name |

|

|

|

5a |

Spouse's Employer Name |

|

|

|

|||||||

|

|

|

|

|

|

|

||||||||||

4b |

Address (Street, City, State, and ZIP code) |

|

5b |

Address (Street, City, State, and ZIP code) |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

||||||||

4c |

Work Telephone Number |

4d |

Does employer allow contact at work |

5c |

Work Telephone Number |

5d Does employer allow contact at work |

|

|||||||||

|

( |

) |

|

|

|

Yes |

No |

|

|

( |

) |

|

|

Yes |

No |

|

4e |

How long with this employer |

4f |

Occupation |

|

5e |

How long with this employer |

5f Occupation |

|

|

|||||||

|

|

(years) |

|

(months) |

|

|

|

|

|

|

(years) |

|

(months) |

|

|

|

4g |

Number of withholding allowances |

4h |

Pay Period: |

|

5g |

Number of withholding allowances |

5h Pay Period: |

|

|

|||||||

|

claimed on Form |

|

|

Weekly |

|

|

claimed on Form |

|

Weekly |

|||||||

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

Monthly |

Other |

|

|

|

|

|

|

Monthly |

Other |

|

Section 3: Other Financial Information (Attach copies of applicable documentation)

6 |

Are you a party to a lawsuit (If yes, answer the following) |

|

|

|

|

|

|

|

Yes |

No |

||||||

|

Plaintiff |

Defendant |

Location of Filing |

Represented by |

|

|

Docket/Case No. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Amount of Suit |

|

|

Possible Completion Date (mmddyyyy) |

Subject of Suit |

|

|

|

|

|

|

|

||||

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Have you ever filed bankruptcy |

(If yes, answer the following) |

|

|

|

|

|

|

|

Yes |

No |

|||||

|

Date Filed (mmddyyyy) |

Date Dismissed (mmddyyyy) |

Date Discharged (mmddyyyy) |

Petition No. |

|

|

|

Location Filed |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

8 |

In the past 10 years, have you lived outside of the U.S for 6 months or longer (If yes, answer the following) |

|

Yes |

No |

||||||||||||

|

Dates lived abroad: from (mmddyyyy) |

To (mmddyyyy) |

|

|

|

|

|

|

|

|||||||

9a |

Are you the beneficiary of a trust, estate, or life insurance policy (If yes, answer the following) |

|

|

|

|

Yes |

No |

|||||||||

|

Place where recorded: |

|

|

|

|

|

|

|

|

|

|

EIN: |

|

|

||

|

Name of the trust, estate, or policy |

Anticipated amount to be received |

|

When will the amount be received |

||||||||||||

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

9b |

Are you a trustee, fiduciary, or contributor of a trust |

|

|

|

|

|

|

|

Yes |

No |

||||||

|

Name of the trust: |

|

|

|

|

|

|

|

|

|

|

|

EIN: |

|

|

|

10 |

Do you have a safe deposit box (business or personal) (If yes, answer the following) |

|

|

|

|

Yes |

No |

|||||||||

|

Location (Name, address and box number(s)) |

|

|

Contents |

|

|

|

|

Value |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

11 |

In the past 10 years, have you transferred any assets for less than their full value (If yes, answer the following) |

|

|

|

|

Yes |

No |

|||||||||

|

List Asset(s) |

|

|

|

Value at Time of Transfer |

Date Transferred (mmddyyyy) |

To Whom or Where was it Transferred |

|||||||||

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Catalog Number 20312N |

|

|

|

|

www.irs.gov |

|

|

|

|

|

|

Form |

|

|||

Form |

Page 2 |

Section 4: Personal Asset Information for all Individuals (Foreign and Domestic)

12 CASH ON HAND Include cash that is not in a bank |

Total Cash on Hand |

$

PERSONAL BANK ACCOUNTS Include all checking, online and mobile (e.g., PayPal etc.) accounts, money market accounts, savings accounts, and stored value cards (e.g., payroll cards, government benefit cards, etc.).

|

Type of Account |

Full Name & Address (Street, City, State, ZIP code) of Bank, |

Account Number |

Account Balance |

||

|

As of |

|

|

|||

|

Savings & Loan, Credit Union, or Financial Institution |

|

|

|||

|

mmddyyyy |

|||||

|

|

|

|

|

||

13a |

|

|

|

$ |

|

|

13b |

|

|

|

$ |

|

|

13c |

Total Cash (Add lines 13a, 13b, and amounts from any attachments) |

|

$ |

|

|

|

INVESTMENTS Include stocks, bonds, mutual funds, stock options, certificates of deposit, and retirement assets such as IRAs, Keogh, 401(k) plans and commodities (e.g., gold, silver, copper, etc.). Include all corporations, partnerships, limited liability companies, or other business entities in which you are an officer, director, owner, member, or otherwise have a financial interest. Include attachment(s) if additional space is needed to respond.

Type of Investment |

Full Name & Address |

Current Value |

Loan Balance (if applicable) |

Equity |

|||

As of |

|||||||

or Financial Interest |

(Street, City, State, ZIP code) of Company |

Value minus Loan |

|||||

|

|

|

|

mmddyyyy |

|

|

|

14a |

|

|

|

|

|

|

|

|

Phone |

$ |

$ |

|

|

$ |

|

14b |

|

|

|

|

|

|

|

Phone

$

$

$

VIRTUAL CURRENCY (CRYPTOCURRENCY) List all virtual currency you own or in which you have a financial interest. (e.g., Bitcoin, Ethereum, Litecoin, Ripple, etc.) If applicable, attach a statement with each virtual currency’s public key.

|

|

|

|

Name of Virtual Currency Wallet, |

Email Address Used to |

Location(s) of Virtual Currency |

Virtual Currency |

|||||||||||

Type of Virtual Currency |

|

Amount and Value in |

||||||||||||||||

|

Exchange or Digital Currency |

With the Virtual Currency |

(Mobile Wallet, Online, and/or |

US dollars as of |

||||||||||||||

|

|

|

|

|

Exchange (DCE) |

Exchange or DCE |

|

External Hardware storage) |

today (e.g., 10 Bitcoins |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$64,600.00 USD) |

||

14c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14e |

Total Equity (Add lines 14a through 14d and amounts from any attachments) |

|

|

|

|

|

|

$ |

|

|

||||||||

AVAILABLE CREDIT Include all lines of credit and bank issued credit cards. |

|

|

|

|

|

|

|

|

|

|||||||||

|

Full Name & Address (Street, City, State, ZIP code) of Credit Institution |

|

Credit Limit |

|

Amount Owed |

Available Credit |

||||||||||||

|

|

|

As of |

As of |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

mmddyyyy |

|

|

mmddyyyy |

|

15a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Acct. No |

|

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

15b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Acct. No |

|

|

|

|

|

|

|

|

$ |

|

|

$ |

|

|

$ |

|

|

15c |

Total Available Credit (Add lines 15a, 15b and amounts from any attachments) |

|

|

|

|

|

|

$ |

|

|

||||||||

16a |

LIFE INSURANCE Do you own or have any interest in any life insurance policies with cash value (Term Life insurance does |

not have a cash value) |

||||||||||||||||

|

Yes |

No |

|

If yes, complete blocks 16b through 16f for each policy. |

|

|

|

|

|

|

|

|

||||||

16b |

Name and Address of Insurance |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Company(ies): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16c |

Policy Number(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16d |

Owner of Policy |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16e |

Current Cash Value |

|

|

|

|

$ |

|

$ |

|

|

|

|

|

$ |

|

|

|

|

16f |

Outstanding Loan Balance |

|

$ |

|

$ |

|

|

|

|

|

$ |

|

|

|

|

|||

16g |

Total Available Cash (Subtract amounts on line 16f from line 16e and include amounts from any attachments) |

$ |

|

|

||||||||||||||

Catalog Number 20312N |

www.irs.gov |

Form |

Form |

|

|

|

|

|

|

|

|

|

Page 3 |

||

REAL PROPERTY Include all real property owned or being purchased |

|

|

|

|

|

|||||||

|

|

|

|

Purchase Date |

|

Current Fair |

Current Loan |

Amount of |

Date of Final |

Equity |

||

|

|

|

|

(mmddyyyy) |

|

Market Value |

Balance |

Monthly Payment |

Payment |

FMV Minus Loan |

||

|

|

|

|

|

(FMV) |

(mmddyyyy) |

||||||

17a |

Property Description |

|

$ |

|

|

$ |

$ |

|

|

$ |

||

|

|

|

|

|

|

|

|

|

||||

|

Location (Street, City, State, ZIP code) and County |

|

Lender/Contract Holder Name, Address (Street, City, State, ZIP code), and Phone |

|||||||||

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

17b |

Property Description |

|

$ |

|

|

$ |

$ |

|

|

$ |

||

|

|

|

|

|

|

|

|

|

||||

|

Location (Street, City, State, ZIP code) and County |

|

Lender/Contract Holder Name, Address (Street, City, State, ZIP code), and Phone |

|||||||||

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

17c Total Equity (Add lines 17a, 17b and amounts from any attachments) |

|

|

|

$ |

|

|||||||

PERSONAL VEHICLES LEASED AND PURCHASED Include boats, RVs, motorcycles, |

||||||||||||

Description (Year, Mileage, Make/Model, |

Purchase/ |

|

Current Fair |

Current Loan |

Amount of |

Date of Final |

Equity |

|||||

Lease Date |

|

Market Value |

Payment |

|||||||||

Tag Number, Vehicle Identification Number) |

(mmddyyyy) |

|

(FMV) |

Balance |

Monthly Payment |

(mmddyyyy) |

FMV Minus Loan |

|||||

18a Year |

|

Make/Model |

|

$ |

|

|

$ |

$ |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

||||

|

Mileage |

|

License/Tag Number |

Lender/Lessor |

Name, Address |

(Street, City, State, |

ZIP code), and Phone |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle Identification Number |

|

|

|

|

|

Phone |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

18b Year |

|

Make/Model |

|

$ |

|

|

$ |

$ |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

||||

|

Mileage |

|

License/Tag Number |

Lender/Lessor |

Name, Address |

(Street, City, State, |

ZIP code), and Phone |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vehicle Identification Number |

|

|

|

|

|

Phone |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

18c Total Equity (Add lines 18a, 18b and amounts from any attachments)

$

PERSONAL ASSETS Include all furniture, personal effects, artwork, jewelry, collections (coins, guns, etc.), antiques or other assets. Include intangible assets such as licenses, domain names, patents, copyrights, mining claims, etc.

|

Purchase/ |

|

Current Fair |

Current Loan |

Amount of |

Date of Final |

Equity |

|||

|

Lease Date |

|

Market Value |

Payment |

||||||

|

(mmddyyyy) |

|

(FMV) |

Balance |

Monthly Payment |

(mmddyyyy) |

FMV Minus Loan |

|||

19a Property Description |

|

|

$ |

|

|

$ |

$ |

|

|

$ |

|

|

|

|

|

|

|

||||

Location (Street, City, State, ZIP code) and County |

|

Lender/Lessor Name, Address (Street, City, State, ZIP code), and Phone |

||||||||

|

|

|

|

|

|

|

Phone |

|

|

|

19b Property Description |

|

|

$ |

|

|

$ |

$ |

|

|

$ |

|

|

|

|

|

|

|

||||

Location (Street, City, State, ZIP code) and County |

|

Lender/Lessor Name, Address (Street, City, State, ZIP code), and Phone |

||||||||

|

|

|

|

|

|

|

Phone |

|

|

|

19c Total Equity (Add lines 19a, 19b and amounts from any attachments) |

|

|

|

$ |

|

|||||

Catalog Number 20312N |

www.irs.gov |

Form |

Form |

Page 4 |

|

If you are |

Section 5: Monthly Income and Expenses

Monthly Income/Expense Statement (For additional information, refer to Publication 1854.)

|

Total Income |

|

|

|

Total Living Expenses |

|

IRS USE ONLY |

|

Source |

|

Gross Monthly |

|

Expense Items 6 |

Actual Monthly |

Allowable Expenses |

20 |

Wages (Taxpayer) 1 |

$ |

|

35 |

Food, Clothing and Misc. 7 |

$ |

|

21 |

Wages (Spouse) 1 |

$ |

|

36 |

Housing and Utilities 8 |

$ |

|

22 |

Interest - Dividends |

$ |

|

37 |

Vehicle Ownership Costs 9 |

$ |

|

23 |

Net Business Income 2 |

$ |

|

38 |

Vehicle Operating Costs 10 |

$ |

|

24 |

Net Rental Income 3 |

$ |

|

39 |

Public Transportation 11 |

$ |

|

25 |

Distributions |

$ |

|

40 |

Health Insurance |

$ |

|

26 |

Pension (Taxpayer) |

$ |

|

41 |

Out of Pocket Health Care Costs 12 |

$ |

|

27 |

Pension (Spouse) |

$ |

|

42 |

Court Ordered Payments |

$ |

|

28 |

Social Security (Taxpayer) |

$ |

|

43 |

Child/Dependent Care |

$ |

|

29 |

Social Security (Spouse) |

$ |

|

44 |

Life Insurance |

$ |

|

30 |

Child Support |

$ |

|

45 |

Current year taxes (Income/FICA) 13 |

$ |

|

31 |

Alimony |

$ |

|

46 |

Secured Debts (Attach list) |

$ |

|

|

Other Income (Specify below) 5 |

|

|

47 |

Delinquent State or Local Taxes |

$ |

|

32 |

|

$ |

|

48 |

Other Expenses (Attach list) |

$ |

|

33 |

|

$ |

|

49 |

Total Living Expenses (add lines |

$ |

|

34 |

Total Income (add lines |

$ |

|

50 |

Net difference (Line 34 minus 49) |

$ |

|

1Wages, salaries, pensions, and social security: Enter gross monthly wages and/or salaries. Do not deduct tax withholding or allotments taken out of pay, such as insurance payments, credit union deductions, car payments, etc. To calculate the gross monthly wages and/or salaries:

If paid weekly - multiply weekly gross wages by 4.3. Example: $425.89 x 4.3 = $1,831.33

If paid biweekly (every 2 weeks) - multiply biweekly gross wages by 2.17. Example: $972.45 x 2.17 = $2,110.22

If paid semimonthly (twice each month) - multiply semimonthly gross wages by 2. Example: $856.23 x 2 = $1,712.46

2Net Income from Business: Enter monthly net business income. This is the amount earned after ordinary and necessary monthly business expenses are paid. This figure is the amount from page 6, line 89. If the net business income is a loss, enter “0”. Do not enter a negative number. If this amount is more or less than previous years, attach an explanation.

3Net Rental Income: Enter monthly net rental income. This is the amount earned after ordinary and necessary monthly rental expenses are paid. Do not include deductions for depreciation or depletion. If the net rental income is a loss, enter “0.” Do not enter a negative number.

4Distributions: Enter the total distributions from partnerships and subchapter S corporations reported on Schedule

5Other Income: Include agricultural subsidies, unemployment compensation, gambling income, oil credits, rent subsidies, sharing economy income from providing

6Expenses not generally allowed: We generally do not allow tuition for private schools, public or private college expenses, charitable contributions, voluntary retirement contributions or payments on unsecured debts. However, we may allow the expenses if proven that they are necessary for the health and welfare of the individual or family or the production of income. See Publication 1854 for exceptions.

7Food, Clothing and Miscellaneous: Total of food, clothing, housekeeping supplies, and personal care products for one month. The miscellaneous allowance is for expenses incurred that are not included in any other allowable living expense items. Examples are credit card payments, bank fees and charges, reading material, and school supplies.

8Housing and Utilities: For principal residence: Total of rent or mortgage payment. Add the average monthly expenses for the following: property taxes, homeowner’s or renter’s insurance, maintenance, dues, fees, and utilities. Utilities include gas, electricity, water, fuel, oil, other fuels, trash collection, telephone, cell phone, cable television and internet services.

9Vehicle Ownership Costs: Total of monthly lease or purchase/loan payments.

10Vehicle Operating Costs: Total of maintenance, repairs, insurance, fuel, registrations, licenses, inspections, parking, and tolls for one month.

11Public Transportation: Total of monthly fares for mass transit (e.g., bus, train, ferry, taxi, etc.)

12Out of Pocket Health Care Costs: Monthly total of medical services, prescription drugs and medical supplies (e.g., eyeglasses, hearing aids, etc.)

13Current Year Taxes: Include state and Federal taxes withheld from salary or wages, or paid as estimated taxes.

Certification: Under penalties of perjury, I declare that to the best of my knowledge and belief this statement of assets, liabilities, and other information is true, correct, and complete.

Taxpayer's Signature

Spouse's signature

Date

After we review the completed Form

IRS USE ONLY (Notes)

Catalog Number 20312N |

www.irs.gov |

Form |

Form |

|

Page 5 |

Sections 6 and 7 must be completed only if you are |

||

Section 6: Business Information |

|

|

51 Is the business a sole proprietorship (filing Schedule C) |

Yes, Continue with Sections 6 and 7. |

No, Complete Form |

All other business entities, including limited liability companies, partnerships or corporations, must complete Form

52Business Name & Address (if different than 1b)

53 |

Employer Identification Number |

54 Type of Business |

|

|

55 |

Is the business a |

Yes |

No |

|

|

|

|

|

|

Federal Contractor |

||

56 |

Business Website (web address) |

57 |

Total Number of Employees |

58 |

Average Gross Monthly Payroll |

|

||

|

|

|

|

|

|

|

||

59 |

Frequency of Tax Deposits |

60 |

Does the business engage in |

Yes |

No |

|||

|

|

|

|

(Internet sales) If yes, complete lines 61a and 61b |

||||

PAYMENT PROCESSOR (e.g., PayPal, Authorize.net, Google Checkout, etc.) Include virtual currency wallet, exchange or digital currency exchange.

Name & Address (Street, City, State, ZIP code). Name & Address (Street, City, State, ZIP code) |

Payment Processor Account Number |

61a

61b

CREDIT CARDS ACCEPTED BY THE BUSINESS

Credit Card

Merchant Account Number

Issuing Bank Name & Address (Street, City, State, ZIP code)

62a

62b

62c

63 BUSINESS CASH ON HAND Include cash that is not in a bank. |

Total Cash on Hand |

$ |

BUSINESS BANK ACCOUNTS Include checking accounts, online and mobile (e.g., PayPal) accounts, money market accounts, savings accounts, and stored value cards (e.g., payroll cards, government benefit cards, etc.). Report Personal Accounts in Section 4.

|

Type of Account |

Full name & Address (Street, City, State, ZIP code) |

Account Number |

Account Balance |

||

|

As of |

|

|

|||

|

of Bank,Savings & Loan, Credit Union or Financial Institution. |

|

|

|||

|

mmddyyyy |

|||||

|

|

|

|

|

||

64a |

|

|

|

$ |

|

|

64b |

|

|

|

$ |

|

|

64c |

Total Cash in Banks (Add lines 64a, 64b and amounts from any attachments) |

|

$ |

|

|

|

ACCOUNTS/NOTES RECEIVABLE Include

Accounts/Notes Receivable & Address (Street, City, State, ZIP code) |

Status (e.g., age, |

Date Due |

Invoice Number or Government |

Amount Due |

factored, other) |

(mmddyyyy) |

Grant or Contract Number |

||

65a |

|

|

|

$ |

65b |

|

|

|

$ |

65c |

|

|

|

$ |

65d |

|

|

|

$ |

65e |

|

|

|

$ |

65f Total Outstanding Balance (Add lines 65a through 65e and amounts from any attachments) |

|

$ |

||

Catalog Number 20312N |

www.irs.gov |

Form |

Form |

Page 6 |

BUSINESS ASSETS Include all tools, books, machinery, equipment, inventory or other assets used in trade or business. Include a list and show the value of all intangible assets such as licenses, patents, domain names, copyrights, trademarks, mining claims, etc.

|

|

Purchase/ |

|

Current Fair |

Current Loan |

Amount of |

Date of Final |

Equity |

|

|

|

Lease Date |

|

Market Value |

Payment |

||||

|

|

(mmddyyyy) |

|

(FMV) |

Balance |

Monthly Payment |

(mmddyyyy) |

FMV Minus Loan |

|

66a |

Property Description |

|

$ |

|

|

$ |

$ |

|

$ |

|

|

|

|

|

|

||||

|

Location (Street, City, State, ZIP code) and Country |

|

|

Lender/Lessor/Landlord |

Name, Address (Street, |

City, State, ZIP code), and Phone |

|||

|

|

|

|

|

|

|

Phone |

|

|

66b |

Property Description |

|

$ |

|

|

$ |

$ |

|

$ |

|

|

|

|

|

|

||||

Location (Street, City, State, ZIP code) and Country

Lender/Lessor/Landlord Name, Address (Street, City, State, ZIP code), and Phone

Phone

66c Total Equity (Add lines 66a, 66b and amounts from any attachments)

$

Section 7 should be completed only if you are

Section 7: Sole Proprietorship Information (lines 67 through 87 should reconcile with business Profit and Loss Statement)

Accounting Method Used:

Cash

Accrual

Use the prior 3, 6, 9 or 12 month period to determine your typical business income and expenses.

Income and Expenses during the period (mmddyyyy) |

|

|

to (mmddyyyy) |

|

||

Provide a breakdown below of your average monthly income and expenses, based on the period |

of time used above. |

|

||||

|

Total Monthly Business Income |

|

Total Monthly Business Expenses (Use attachments as needed) |

|||

|

Source |

Gross Monthly |

|

Expense Items |

Actual Monthly |

|

67 |

Gross Receipts |

$ |

77 |

Materials Purchased 1 |

$ |

|

68 |

Gross Rental Income |

$ |

78 |

Inventory Purchased 2 |

$ |

|

69 |

Interest |

$ |

79 |

Gross Wages & Salaries |

$ |

|

70 |

Dividends |

$ |

80 |

Rent |

$ |

|

71 |

Cash Receipts not included in lines |

$ |

81 |

Supplies 3 |

$ |

|

|

Other Income (Specify below) |

|

82 |

Utilities/Telephone 4 |

$ |

|

72 |

|

$ |

83 |

Vehicle Gasoline/Oil |

$ |

|

73 |

|

$ |

84 |

Repairs & Maintenance |

$ |

|

74 |

|

$ |

85 |

Insurance |

$ |

|

75 |

|

$ |

86 |

Current Taxes 5 |

$ |

|

76 |

Total Income (Add lines 67 through 75) |

$ |

87 |

Other Expenses, including installment payments |

$ |

|

|

(Specify) |

|||||

|

|

|

88 |

Total Expenses (Add lines 77 through 87) |

$ |

|

|

|

|

89 |

Net Business Income (Line 76 minus 88) 6 |

$ |

|

Enter the monthly net income amount from line 89 on line 23, section 5. If line 89 is a loss, enter "0" on line 23, section 5.

1Materials Purchased: Materials are items directly related to the production of a product or service.

2Inventory Purchased: Goods bought for resale.

3Supplies: Supplies are items used in the business that are consumed or used up within one year. This could be the cost of books, office supplies, professional equipment, etc.

4Utilities/Telephone: Utilities include gas, electricity, water, oil, other fuels, trash collection, telephone, cell phone and business internet.

5Current Taxes: Real estate, excise, franchise, occupational, personal property, sales and employer’s portion of employment taxes.

6Net Business Income: Net profit from Form 1040, Schedule C may be used if duplicated deductions are eliminated (e.g., expenses for business use of home already included in housing and utility expenses on page 4). Deductions for depreciation and depletion on Schedule C are not cash expenses and must be added back to the net income figure. In addition, interest cannot be deducted if it is already included in any other installment payments allowed.

IRS USE ONLY (Notes)

Privacy Act: The information requested on this Form is covered under Privacy Acts and Paperwork Reduction Notices which have already been provided to the taxpayer.

Catalog Number 20312N |

www.irs.gov |

Form |

| Fact Name | Detail |

|---|---|

| Purpose | The IRS Form 433-A is used to collect financial information from individuals to determine their ability to pay outstanding tax debts. |

| Who Must File | Individuals who are unable to pay their tax debt in full and are seeking a payment plan or compromise with the IRS are required to submit Form 433-A. |

| Sections Covered | The form includes sections on personal information, employment details, bank accounts, assets, credit card information, and monthly living expenses. |

| Impact on Payment Plans | The information provided on Form 433-A helps the IRS to determine eligibility for payment plans and to set payment amounts based on the individual's financial situation. |

| State-Specific Versions | While Form 433-A is a federal form, some states may require similar forms for state tax debt issues. These forms and their requirements are governed by the respective state's laws. |

After filling out the IRS 433-A form, the information you provide will be used to evaluate your financial situation. This evaluation will determine your ability to pay outstanding taxes. It's crucial to approach this document with thoroughness, providing accurate and updated information to ensure the IRS can make a fair assessment of your financial condition.

After completing the form, you will submit it to the IRS either via mail or electronically, as directed in the form's instructions. Ensure you keep a copy of the filled form and any accompanying documents for your records. The IRS will then process your form, which could lead to further communications about your financial situation and proposed steps to address your tax obligations.

What is the IRS Form 433-A and who should use it?

The IRS Form 433-A is a detailed form used by individuals to provide the Internal Revenue Service (IRS) with information about their financial situation. This form is particularly used to set up payment plans or to settle tax debts under conditions where the taxpayer demonstrates an inability to make a full payment immediately. It's meant for individuals who owe income tax, self-employed individuals, and those who are responsible for a household's financial decisions.

What kind of information do I need to complete Form 433-A?

To accurately complete Form 433-A, you will need comprehensive details about your financial situation. This includes, but is not limited to, your employment information, bank accounts, real estate, other personal assets, credit cards, loans, monthly living expenses, and any other form of income or expenses. It’s essential to provide detailed and accurate information to ensure a fair assessment by the IRS.

How can I obtain Form 433-A?

Form 433-A can be downloaded directly from the IRS website. Alternatively, you can also request a paper copy by calling the IRS. It’s important to ensure you are using the most recent version of the form to avoid any processing delays.

Is there a deadline for submitting Form 433-A?

There is no specific deadline for submitting Form 433-A itself. However, it is typically requested by the IRS during the process of arranging a payment plan or negotiating a settlement. Once requested by the IRS, it is crucial to submit it as promptly as possible to avoid potential penalties or further enforcement actions.

Can I submit Form 433-A electronically?

Currently, Form 433-A must be printed and mailed to the IRS. Electronic submission is not an option. It is essential to send it to the appropriate address provided by the IRS to ensure it is processed efficiently.

What happens after I submit Form 433-A?

After submitting Form 433-A, the IRS will review your financial information to determine your ability to pay your tax debt. They may propose a payment plan that reflects your financial situation, offer a settlement, or suggest other resolutions depending on your unique circumstances. The IRS may also request additional information or documentation to verify the details provided in your form.

How can I ensure my Form 433-A is processed smoothly?

To facilitate a smooth processing of your Form 433-A, ensure that all information is complete, accurate, and truthful. Attach all required documentation and proof for assets, income, and expenses as specified in the form instructions. Additionally, making sure your contact information is up to date will help avoid any delays in communication.

What if I need help filling out Form 433-A?

If you find the process of filling out Form 433-A overwhelming, consider seeking assistance from a tax professional. Tax attorneys, certified public accountants (CPAs), and enrolled agents who specialize in tax issues can provide valuable guidance and ensure that the form is filled out correctly and your rights are protected.

Can changes be made to Form 433-A after it has been submitted?

If your financial situation changes significantly after you have submitted Form 433-A, you should inform the IRS as soon as possible. Depending on the circumstances, the IRS may allow you to submit a revised form or provide updated information to reflect your current financial status.

When dealing with the Internal Revenue Service (IRS) 433-A form, which is essential for individuals who are setting up a payment plan or an offer in compromise due to tax debt, accuracy and thoroughness cannot be overstated. However, mistakes are common, and they can complicate or delay the resolution of tax issues. Here are nine of the most common mistakes people make.

Not providing all required information: Filling out the IRS 433-A form partially or leaving out essential details can lead to processing delays or rejections. Every piece of requested information must be furnished accurately.

Using outdated forms: Tax laws and forms are updated regularly. Using an outdated version of Form 433-A may result in errors or require resubmission with the current form, causing unnecessary delays.

Underestimating expenses: Some individuals minimize their monthly expenses in the belief that it makes them look more financially capable of settling their tax debt. This can backfire, as the IRS has standards for allowable living expenses, and underreporting can lead to unrealistic payment plans.

Overestimating expenses: Conversely, inflating expenses to appear unable to pay can also create issues. The IRS verifies expense claims against national and local standards, and discrepancies can lead to skepticism about the accuracy of the entire form.

Failing to include all sources of income: All income must be reported on the Form 433-A. This includes wages, dividends, business income, rental income, and any other sources. Omission of any income source can be seen as an attempt to deceive.

Not accurately reporting assets: Assets such as real estate, vehicles, life insurance, and retirement accounts must be accurately reported on the form. Overlooking or undervaluing assets can lead to allegations of fraud.

Math errors: Simple math errors can lead to an incorrect representation of financial status. Always double-check calculations to ensure accuracy.

Failure to sign and date the form: An unsigned or undated form is not valid and will not be processed. This mistake can delay resolution efforts significantly.

Not consulting with a tax professional: Given the complexities of tax laws and the potential for mistakes, failing to seek professional advice can be a critical oversight. A tax professional can help ensure that the Form 433-A is filled out correctly and that all options for resolving tax debt are considered.

Avoiding these mistakes can help individuals navigate the challenges of resolving tax issues with the IRS more smoothly and efficiently.

When dealing with tax issues, particularly those involving payment plans or negotiations with the IRS, the Form 433-A (OIC) – an individual or self-employed person's Collection Information Statement for Wage Earners and Self-Employed Individuals – becomes central. Its completion and submission can rarely be done in isolation. Typically, several additional documents and forms are required to provide a comprehensive view of an individual's financial situation. Below, we list and briefly describe other forms and documents often used alongside the IRS 433-A Form.

Completing the IRS 433-A form requires a thorough documentation process. Each document plays a crucial role in creating a comprehensive picture of the taxpayer's financial state, allowing for accurate and fair negotiations with the IRS. Always ensure that documents are current and accurately reflect your financial situation to streamline the process and achieve a favorable outcome.

The IRS 433-F, also known as the Collection Information Statement, is akin to the 433-A as both forms are used by individuals to provide financial information to the IRS. This outlines the taxpayer's ability to pay outstanding tax debts, but the 433-F is a shorter and less detailed form than the 433-A.

The IRS Form 1040, the U.S. individual income tax return, shares similarities with the IRS 433-A in that it requires detailed financial information from the taxpayer. However, while the 1040 focuses on calculating tax liabilities based on income, deductions, and credits, the 433-A seeks information to assess payment plans for existing tax debts.

Form 9465, the Installment Agreement Request, is used to request a payment plan for paying off a tax debt. It works in conjunction with the IRS 433-A, which provides the IRS with the necessary financial information to determine the feasibility and terms of the payment plan.

The IRS Form 656, Offer in Compromise, allows taxpayers to settle their tax liabilities for less than the full amount owed. The IRS 433-A provides the detailed financial information that supports the taxpayer's offer by demonstrating their inability to fully pay the tax debt.

Form W-2, Wage and Tax Statement, and the IRS 433-A both require individual income information. The W-2 form is provided by employers to employees, showing the annual wages and taxes withheld. In contrast, the 433-A collects information on wages among various other financial details directly from taxpayers to assess their financial situation.

The Schedule C (Form 1040), Profit or Loss From Business, and the IRS 433-A are related through their collection of financial details related to individual business activities. Schedule C is used by sole proprietors to report how much their business made or lost in a year, while the 433-A might include similar information as part of its comprehensive financial disclosure for tax resolution purposes.

Form 1120, U.S. Corporation Income Tax Return, while primarily for corporations, intersects with the information sought in IRS 433-A for individuals who own businesses. The 433-A form may require details about the individual's business income and financial situation, which could also be reflected in a corporation's 1120 form filings.

IRS Form 433-B, Collection Information Statement for Businesses, parallels the 433-A in purpose and content but is specifically designed for businesses. Both forms gather financial information to negotiate tax payment terms, with the 433-B focusing on the business entity's financial capacity.

The Bankruptcy Forms, particularly the Statement of Financial Affairs for Individuals Filing for Bankruptcy, share the purpose of providing a comprehensive view of an individual's financial situation. Like the IRS 433-A, these forms require detailed disclosure of income, assets, and liabilities, but for the purpose of bankruptcy proceedings rather than tax resolution.

Form SSA-632, Request for Waiver of Overpayment Recovery or Change in Repayment Rate, is used by the Social Security Administration to assess an individual's ability to repay overpaid benefits. Similar to the IRS 433-A, it gathers comprehensive financial information to evaluate a person's capacity to make payments, albeit in the context of Social Security benefits.

Filling out IRS Form 433-A, a detailed form used to collect financial information from individuals to determine their ability to pay off tax debt, requires careful attention. Here are five essential practices to follow and avoid for a smoother process.

Do:

Don't:

The IRS Form 433-A, often required during the process of setting up a payment plan or offering in compromise with the IRS, is subject to several misconceptions. Understanding these misconceptions is pivotal for individuals attempting to navigate their financial obligations to the federal government accurately.

The form is only for businesses: A common misunderstanding is that IRS Form 433-A is solely for businesses. In reality, this form is intended for individuals or sole proprietors to provide detailed information about their financial situation. This includes income, expenses, and assets, which helps the IRS determine an individual's ability to pay back taxes.

Filling out the form guarantees a payment plan: Another misconception is that completion and submission of the form guarantee the approval of a payment plan or offer in compromise. While it is a crucial step in the application process, approval is based on a thorough review of the submitted information, and the IRS's decision takes into account the individual's full financial situation and compliance history.

The information requested is optional: Some might believe that the information requested on the form is optional or that not all sections need to be completed. This belief can lead to the submission of an incomplete form, which can delay the process. It is essential to complete every section of the form that applies to your situation, providing detailed and accurate information to avoid processing delays or rejection.

You can negotiate your own terms: There is a belief that individuals can negotiate the terms of their payment plan directly by using the information provided in Form 433-A. While the form does help outline an individual's financial situation, the IRS has specific guidelines and formulas to determine payment terms. These calculations are made based on the information provided in the form, along with IRS policies and the individual's ability to pay.

The IRS Form 433-A is a critical document used by the Internal Revenue Service (IRS) to gather financial information from individuals who are seeking to set up a payment plan or settle a tax debt. Understanding how to properly fill out and utilize this form can significantly impact an individual's financial responsibilities to the government. Below are key takeaways to consider when dealing with the IRS Form 433-A:

In summary, the IRS Form 433-A is a powerful tool in managing or negotiating your tax obligations. Taking the time to accurately and thoroughly complete this document can significantly affect your financial engagements with the IRS. Whether you're applying for a payment plan or trying to reduce your tax liabilities, the details you provide on this form play a critical role in determining the outcome.

Free Coaching Templates Pdf - Streamlines the process of documenting and addressing work-related concerns, making it manageable and consistent.

Mobile Home Listing Agreement - By defining the authority of the listing agent, the agreement solidifies the agent’s role and efforts to sell the mobile home within the agreed period.

Where to Mail Form 3911 - IRS Form 3911 is the prescribed method for taxpayers to initiate a trace of their federal tax refund with the IRS.