Free IRS 8233 PDF Template

Free IRS 8233 PDF Template

Navigating the complexities of tax obligations in the United States can be a daunting task, especially for individuals who are not citizens but are earning income within the country's borders. Amidst the plethora of forms and documents, the IRS 8233 form stands out for those who find themselves in such a situation. This particular form plays a pivotal role in ensuring the correct application of treaty benefits, potentially reducing the amount of taxes required to be withheld from income earned in the U.S. It is specifically designed for nonresident aliens and others who receive compensation for personal services performed in the United States. The form allows these individuals to claim exemption from withholding on compensation due to tax treaty benefits. Additionally, the 8233 form demands a detailed declaration of the recipient’s personal and income details, alongside their claim for exemption. This makes the understanding and accurate completion of the form crucial, as it directly impacts the treatment of one’s income and the subsequent tax implications. Essential for both the income earner and the withholding agent, this form ensures compliance with U.S. tax laws while acknowledging the tax treaty positions that can alleviate the tax burdens for those qualified under specific agreements between the United States and their country of residence.

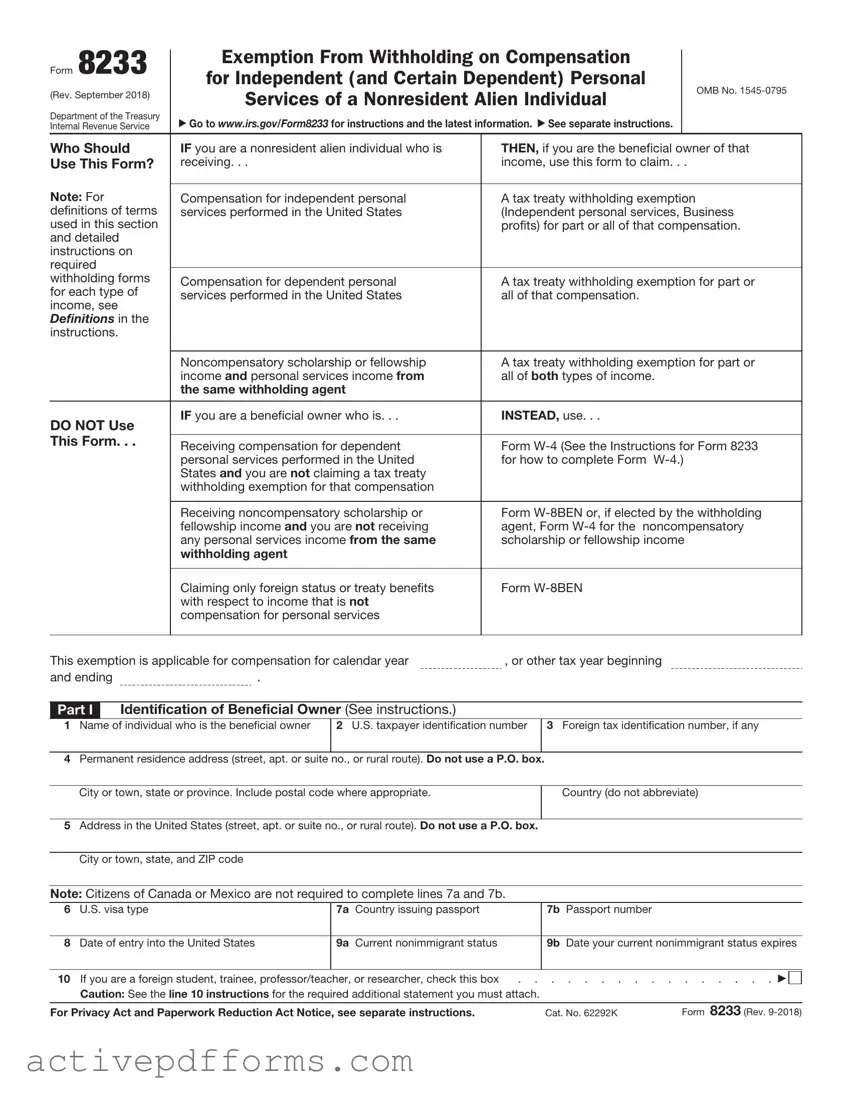

Form 8233

(Rev. September 2018)

Department of the Treasury Internal Revenue Service

Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual

Go to www.irs.gov/Form8233 for instructions and the latest information. See separate instructions.

OMB No.

Who Should |

IF you are a nonresident alien individual who is |

THEN, if you are the beneficial owner of that |

Use This Form? |

receiving. . . |

income, use this form to claim. . . |

Note: For |

|

|

Compensation for independent personal |

A tax treaty withholding exemption |

|

definitions of terms |

services performed in the United States |

(Independent personal services, Business |

used in this section |

|

profits) for part or all of that compensation. |

and detailed |

|

|

instructions on |

|

|

required |

|

|

|

|

|

withholding forms |

Compensation for dependent personal |

A tax treaty withholding exemption for part or |

for each type of |

services performed in the United States |

all of that compensation. |

income, see |

|

|

Definitions in the |

|

|

instructions. |

|

|

|

|

|

|

Noncompensatory scholarship or fellowship |

A tax treaty withholding exemption for part or |

|

income and personal services income from |

all of both types of income. |

|

the same withholding agent |

|

|

|

|

DO NOT Use |

IF you are a beneficial owner who is. . . |

INSTEAD, use. . . |

|

|

|

This Form. . . |

Receiving compensation for dependent |

Form |

|

||

|

personal services performed in the United |

for how to complete Form |

|

States and you are not claiming a tax treaty |

|

|

withholding exemption for that compensation |

|

|

|

|

|

Receiving noncompensatory scholarship or |

Form |

|

fellowship income and you are not receiving |

agent, Form |

|

any personal services income from the same |

scholarship or fellowship income |

|

withholding agent |

|

|

|

|

|

Claiming only foreign status or treaty benefits |

Form |

|

with respect to income that is not |

|

|

compensation for personal services |

|

|

|

|

This exemption is applicable for compensation for calendar year |

, or other tax year beginning |

|

and ending |

. |

|

Part I Identification of Beneficial Owner (See instructions.)

1Name of individual who is the beneficial owner

2U.S. taxpayer identification number

3Foreign tax identification number, if any

4Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box.

City or town, state or province. Include postal code where appropriate.

Country (do not abbreviate)

5Address in the United States (street, apt. or suite no., or rural route). Do not use a P.O. box.

City or town, state, and ZIP code

Note: Citizens of Canada or Mexico are not required to complete lines 7a and 7b.

6U.S. visa type

7a Country issuing passport

7b Passport number

8Date of entry into the United States

9a Current nonimmigrant status

9b Date your current nonimmigrant status expires

10 If you are a foreign student, trainee, professor/teacher, or researcher, check this box |

. . . . . . . . . . . . . . . . |

|

Caution: See the line 10 instructions for the required additional statement you must attach. |

|

|

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 62292K |

Form 8233 (Rev. |

Form 8233 (Rev. |

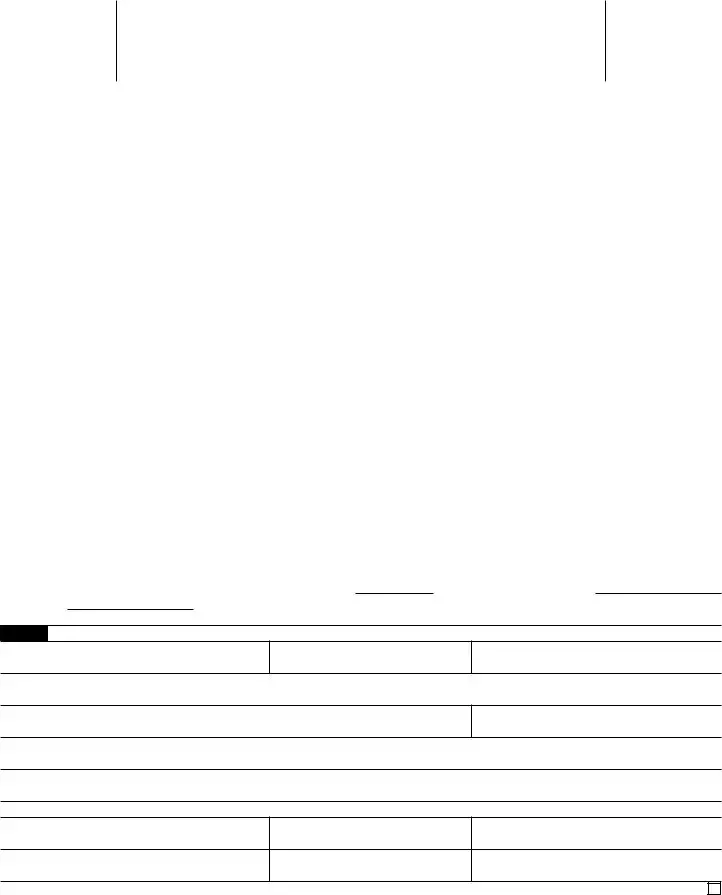

Page 2 |

|

Part II |

Claim for Tax Treaty Withholding Exemption |

|

11Compensation for independent (and certain dependent) personal services: a Description of personal services you are providing

b Total compensation you expect to be paid for these services in this calendar or tax year $

12If compensation is exempt from withholding based on a tax treaty benefit, provide: a Tax treaty on which you are basing exemption from withholding

b Treaty article on which you are basing exemption from withholding

c Total compensation listed on line 11b above that is exempt from tax under this treaty $ d Country of residence

Note: Do not complete lines 13a through 13d unless you also received compensation for personal services from the same withholding agent.

13Noncompensatory scholarship or fellowship income:

aAmount $

bTax treaty on which you are basing exemption from withholding

cTreaty article on which you are basing exemption from withholding

dTotal income listed on line 13a above that is exempt from tax under this treaty $

14Sufficient facts to justify the exemption from withholding claimed on line 12 and/or line 13 (see instructions)

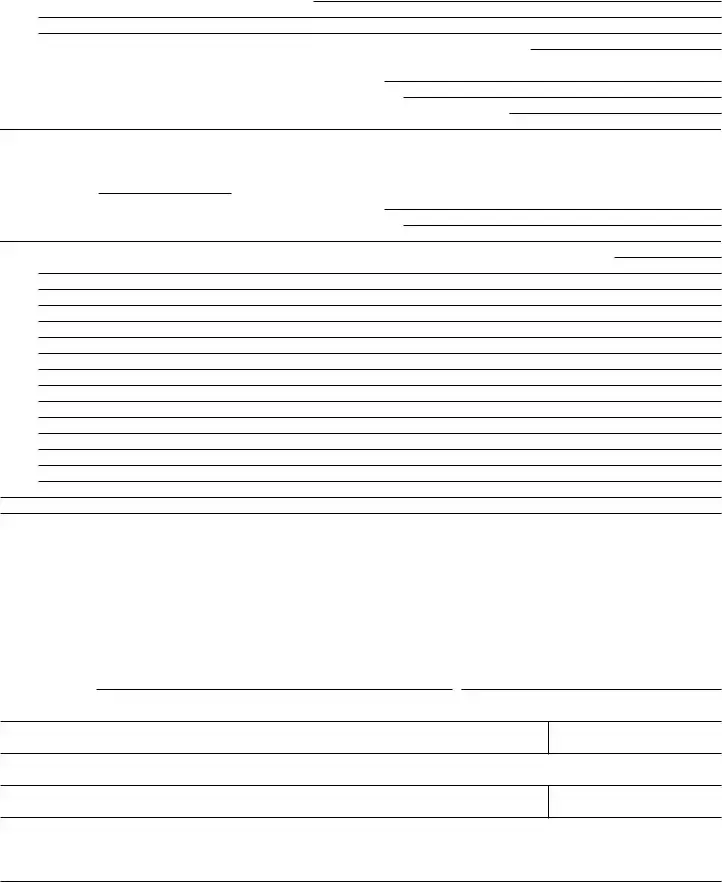

Part III Certification

Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that:

•I am the beneficial owner (or am authorized to sign for the beneficial owner) of all the income to which this form relates.

•The beneficial owner is not a U.S. person.

•The beneficial owner is a resident of the treaty country listed on line 12a and/or 13b above within the meaning of the income tax treaty

between the United States and that country, or was a resident of the treaty country listed on line 12a and/or 13b above at the time of, or immediately prior to, entry into the United States, as required by the treaty.

Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner.

Sign Here |

▶ Signature of beneficial owner (or individual authorized to sign for beneficial owner) |

Date |

|

|

|

|

|

Part IV |

|

Withholding Agent Acceptance and Certification |

|

Name

Employer identification number

Address (number and street) (Include apt. or suite no. or P.O. box, if applicable.)

City, state, and ZIP code

Telephone number

Under penalties of perjury, I certify that I have examined this form and any accompanying statements, that I am satisfied that an exemption from withholding is warranted, and that I do not know or have reason to know that the nonresident alien individual is not entitled to the exemption or that the nonresident alien’s eligibility for the exemption cannot be readily determined.

Signature of withholding agent |

Date |

Form 8233 (Rev.

| Fact Name | Description |

|---|---|

| Purpose of Form 8233 | This form is designed to allow non-resident aliens to claim exemption from withholding on compensation for independent personal services and certain other income. |

| Required Filers | Non-resident alien individuals, who are receiving compensation for services performed in the United States and claiming a tax treaty benefit, are required to file Form 8233. |

| Submission Process | After completing Form 8233, the individual must submit it to their payer, who then forwards it to the Internal Revenue Service (IRS) for approval. |

| Governing Tax Treaties | The eligibility to claim exemption based on a tax treaty benefit is governed by the specific tax treaty between the United States and the non-resident alien's country of residence. |

Filing the IRS Form 8233 is an essential process for individuals who are claiming exemption from withholding on income from the United States due to tax treaties. This procedure can seem intricate, but breaking it down into manageable steps makes it more approachable. It's crucial to pay close attention to each part of the form to ensure accuracy and compliance with the tax laws. The following steps are designed to guide you through filling out the form with ease.

Once submitted, the process on the payer’s part involves assessing the form for completeness and accuracy before sending it to the IRS. The IRS will then review the form to determine if the tax exemption is justified based on the tax treaty. Remember, it's important to retain copies of all documents submitted for your records. Approaching this process with patience and attention to detail will ensure a smoother path to claiming your tax treaty benefits.

The Internal Revenue Service (IRS) Form 8233, titled "Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual," is a document utilized in the United States to claim exemption from withholding of federal income tax for certain types of income received by nonresident aliens. This form plays a pivotal role for individuals in specific circumstances and understanding its implications, the process of filing, and its requirements is crucial for compliance and benefiting from potential exemptions.

What is the purpose of IRS Form 8233?

IRS Form 8233 is designed to enable nonresident alien individuals to claim exemptions from withholding on compensation related to personal services within the United States, under a tax treaty between the United States and the individual's country of tax residence. By accurately completing and submitting this form, taxpayers can assert their right to partial or full exemption from U.S. federal income tax on certain earnings, reflecting the provisions of the applicable tax treaty.

Who needs to file Form 8233?

Form 8233 must be filed by nonresident alien individuals who receive compensation for independent or certain dependent personal services performed in the United States and who claim exemption from withholding of federal income tax. These individuals typically include independent contractors, scholars, researchers, and employees of foreign governments, among others, whose compensation may qualify for reduced taxation under a treaty.

What types of income are eligible for exemption using Form 8233?

The types of income that can be exempted from withholding upon the filing of Form 8233 are generally limited to compensation for personal services. This encompasses wages, salaries, honoraria, fellowship stipends, and certain scholarships. It's essential to consult the specific tax treaty between the U.S. and the taxpayer's country of residence to determine the eligibility and extent of such exemptions.

How does one file Form 8233, and what documents are required?

To file Form 8233, the individual must complete it in full and provide all necessary documentation. This includes a Taxpayer Identification Number (TIN), typically in the form of a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). Additionally, documentation substantiating residency in a treaty country and details regarding the nature of the services and compensation must be furnished. The completed form and supporting documents should be submitted to the withholding agent, not directly to the IRS, unless specifically instructed.

What are the implications of incorrectly filing Form 8233?

Incorrectly filing Form 8233 can lead to several adverse outcomes, including the denial of the treaty benefits claimed, imposition of withholding at the statutory rate, and potential penalties and interest on underpaid taxes. Accuracy and completeness in filing are paramount to avoid these consequences. In cases where uncertainties or questions arise, it may be beneficial to seek guidance from a tax professional or the IRS.

How often must Form 8233 be filed?

Form 8233 must be filed for each tax year in which an individual claims exemption from withholding under a tax treaty. Thus, it is not a one-time filing but requires annual renewal as long as the conditions for the exemption persist. Furthermore, any change in circumstances that affects the individual's eligibility for the tax treaty benefits necessitates a reevaluation of the need to file Form 8233.

Understanding and utilizing IRS Form 8233 can significantly benefit nonresident alien individuals eligible for tax treaty benefits. However, the complexities of tax treaties and the specifics of individual circumstances underscore the importance of thoroughness and possibly, professional tax advice in navigating these issues.

Filling out IRS forms can often feel like navigating a maze without a map. The IRS 8233 form, in particular, demands careful attention. Primarily used by nonresident aliens to claim a tax treaty benefit or exemption from withholding on income effectively connected with the conduct of a trade or business in the United States, inaccuracies in completing this form can lead to unexpected tax liabilities or processing delays. Here are some commonly observed mistakes to avoid:

Not fully understanding the treaty benefits – Without a clear grasp of the specifics of the tax treaty between the United States and one's country of residence, individuals often miss the benefits they're entitled to or apply them incorrectly.

Failing to correctly identify the type of income – Misclassifying income can lead to incorrect withholding and reporting, impacting one's tax obligations.

Omitting personal information – Every field related to personal information, including taxpayer identification numbers and addresses, must be accurately filled out to avoid processing delays.

Overlooking the necessity for a Taxpayer Identification Number (TIN) – A common error is to submit the form without a TIN, which is mandatory for processing the form.

Inaccurate claim of benefit eligibility – Claiming treaty benefits without meeting the eligibility criteria can lead to rejection of the form or a request for additional documentation.

Misunderstanding the scope of exemption – Individuals sometimes mistakenly believe they are exempt from all US taxes, when in reality, the exemption might only apply to certain types of income.

Not attaching required additional documentation – Ignoring the requirement to attach additional documentation, such as a residency certificate, can result in the denial of treaty benefits.

Forgetting to sign and date the form – This simple oversight can invalidate the entire submission, necessitating a resubmission and further delaying processing.

Remember, accurate completion of the IRS 8233 form is crucial for nonresident aliens seeking to utilize treaty benefits. Ensuring all information is precise and up-to-date can save individuals from unnecessary headaches. When in doubt, consulting with a tax professional or legal consultant familiar with international tax obligations can provide clarity and peace of mind. Taking the time to thoroughly review and understand the form before submission is an investment in one’s financial well-being.

The IRS Form 8233, Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual, is an important document for nonresident aliens providing services in the United States. It allows individuals to claim exemption from withholding on income related to personal services. To accurately process and understand this claim for exemption, several other forms and documents may frequently be used in conjunction with IRS Form 8233. Understanding these additional documents can provide a clearer picture of the tax obligations and entitlements of a nonresident alien in the U.S.

While this list is not exhaustive, these documents are prominently associated with the IRS Form 8233. They serve as foundational pieces in the broader context of U.S. tax compliance for nonresident aliens. Proper completion and submission of these forms help ensure compliance with U.S. tax laws and can prevent potential legal and financial complications. Individuals unsure about their tax status or the appropriate forms to file should consider consulting with a tax preparer or attorney specialized in international tax law.

IRS Form W-8BEN: This document, much like the IRS 8233 form, is used by foreign individuals to claim exemption from certain U.S. withholdings on income. The primary purpose of Form W-8BEN is to establish the non-U.S. status of the beneficiary, thus helping reduce the tax burden under the provisions of international treaties. Both forms serve as crucial tools for non-residents to navigate U.S. tax laws but target slightly different circumstances and benefits.

IRS Form W-9: Although designed primarily for U.S. persons (including residents and entities), the IRS Form W-9 shares a common goal with the 8233 form: providing taxpayer identification information to entities that will pay them income. Where the 8233 form targets non-resident aliens and foreign entities for specific exemptions, the W-9 collects information to report income paid to the IRS, ensuring compliance with U.S. tax laws.

IRS Form 1040-NR: This form is another document closely related to the IRS 8233 form, yet it serves a broader purpose. Nonresident aliens utilize the IRS Form 1040-NR to file their U.S. income tax returns. While the 8233 is specifically for claiming exemption from withholding on compensation for independent personal services, the 1040-NR provides a comprehensive declaration of all taxable income earned in the U.S. Both are vital for non-residents to fulfill their tax obligations and claim eligible benefits.

IRS Form 8288-B: This form is used by foreign persons to apply for a withholding certificate for dispositions by foreign persons of U.S. real property interests. Its connection to the IRS 8233 form lies in its similar function of allowing non-U.S. persons to reduce or eliminate withholding requirements, albeit in the specific context of real estate transactions. Both forms play a critical role in managing the tax implications for foreign individuals and entities involved in U.S. financial activities.

IRS Form 8805: Pertinent to foreign partners of U.S. partnerships, IRS Form 8805 is utilized to report the share of income effectively connected with the U.S. trade or business. Like the IRS 8233 form, it relates to the withholding tax and international tax treaty benefits. However, the 8805 form specifically deals with income allocations to foreign partners, ensuring that the appropriate taxes are withheld and reported correctly to the IRS, thereby facilitating compliance with U.S. tax laws.

Filling out the IRS 8233 form, which pertains to Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual, requires attention to detail and an understanding of your tax situation. Here's a clear guide to what you should and shouldn't do to navigate this process smoothly.

Do:Read the instructions provided by the IRS carefully before you start filling out the form. Understanding the requirements can save you from making mistakes.

Verify your tax treaty benefits eligibility. If a tax treaty between the United States and your country of tax residency exists, determine if it applies to your situation.

Provide accurate personal information, including your name, address, and SSN or ITIN. Mistakes here can lead to processing delays.

Include details about the compensator, such as the employer or entity paying for your services. This information is crucial for the IRS to process your form.

Fill out the form in English and use USD for any monetary amounts. Ensuring clarity in communication aids in the smooth processing of your paperwork.

Attach a statement to the form if additional space is needed or to provide further explanation about your tax situation, as required.

Review the form for errors before submitting it. A second look can catch mistakes you may have overlooked initially.

Keep a copy of the filled-out form for your records. This helps you stay organized and prepared for any future inquiries.

Submit the form before the deadline. Late submissions can result in delayed processing or complications with your tax withholding.

Seek guidance from a tax professional if you're unsure about any part of the form. Professional advice can prevent costly errors.

Don’t overlook the importance of checking for updates to the form or related tax treaty benefits. Tax laws and forms can change, and staying current is essential.

Don’t use pencil or non-permanent ink when filling out the form. Use black ink to ensure all information remains legible and permanent.

Don’t leave any required fields blank. If a section does not apply, indicate with “N/A” (not applicable) or “0” if it refers to amounts.

Don’t guess on details. If you're unsure about something, it’s better to seek clarification rather than risk submitting incorrect information.

Don’t forget to sign and date the form. An unsigned form is considered incomplete and will not be processed.

Don’t submit the form without ensuring all necessary documentation is included. Missing documents can delay the process.

Don’t ignore IRS requests for additional information. Respond promptly to any inquiries to avoid processing delays.

Don’t discard evidence of mailing the form to the IRS. Keeping proof can be useful if there are any disputes about whether you submitted the form on time.

Don’t underestimate the impact of tax treaties. They can significantly affect your withholding rates, so familiarize yourself with any that apply.

Don’t hesitate to update the form if your circumstances change. Keeping your information current helps avoid potential issues with tax withholding.

The Internal Revenue Service (IRS) Form 8233, "Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual," often stirs confusion and misconceptions. Let’s debunk some common misunderstandings to foster a clearer perspective on its importance and usage.

Understanding these misconceptions about Form 8233 can alleviate unnecessary stress and ensure compliance with U.S. tax laws, while possibly benefiting from specific exemptions and treaty provisions designed for nonresident aliens.

The IRS 8233 form is essential for individuals who are claiming exemption from withholding on income from the United States due to a tax treaty between the U.S. and their country of residence. Understanding how to properly fill out and use this form is crucial for ensuring compliance with tax obligations and taking advantage of treaty benefits. Below are five key takeaways regarding the IRS 8233 form.

Properly completing and using the IRS 8233 form can significantly impact an individual's tax obligations in the United States. Comprehending these key points ensures individuals correctly claim treaty benefits, thereby potentially reducing their tax burden.

Where to Get Official Transcripts - Effortlessly plan for your future with the Bauder College Transcript Request Form, which provides a detailed procedure for obtaining your academic transcript, including the payment process.

Daycare Receipt Template - A structured receipt showcasing the specifics of child care service payment, including the care period and parties involved.

Vendor Additional Insured - Limits of coverage for vendors are dictated by law and any applicable contractual requirements.