Free IRS 8283 PDF Template

Free IRS 8283 PDF Template

Navigating the complexities of tax deductions related to non-cash charitable contributions involves understanding and correctly utilizing IRS Form 8283. This crucial document is pivotal for taxpayers who wish to gain the benefits associated with donating property other than cash to qualified organizations. The significance of this form stems from its role in providing the IRS with detailed information about the donated property, ensuring donors comply with tax laws while optimizing their deductions. Specific sections of the form cater to different types of donations and their respective values, thus requiring careful evaluation and completion by the donor. Whether it’s a piece of art, a vehicle, or stocks, accurately reporting on Form 8283 can potentially enhance an individual's tax-saving strategy. However, with the potential for scrutiny from the IRS, it’s essential for individuals to precisely assess the value of their donations and maintain thorough documentation supporting their claims. The necessity of obtaining professional appraisals for items of substantial value adds an additional layer of complexity to the process, underscoring the importance of attention to detail and proper adherence to the relevant guidelines.

Form 8283 |

|

Noncash Charitable Contributions |

|

OMB No. |

|

|

|||

|

▶ Attach one or more Forms 8283 to your tax return if you claimed a total deduction |

|

|

|

(Rev. December 2021) |

|

of over $500 for all contributed property. |

|

Attachment |

Department of the Treasury |

|

|

||

|

|

|

||

|

▶ Go to www.irs.gov/Form8283 for instructions and the latest information. |

|

Sequence No. 155 |

|

Internal Revenue Service |

|

|

||

Name(s) shown on your income tax return |

|

Identifying number |

||

|

|

|

|

|

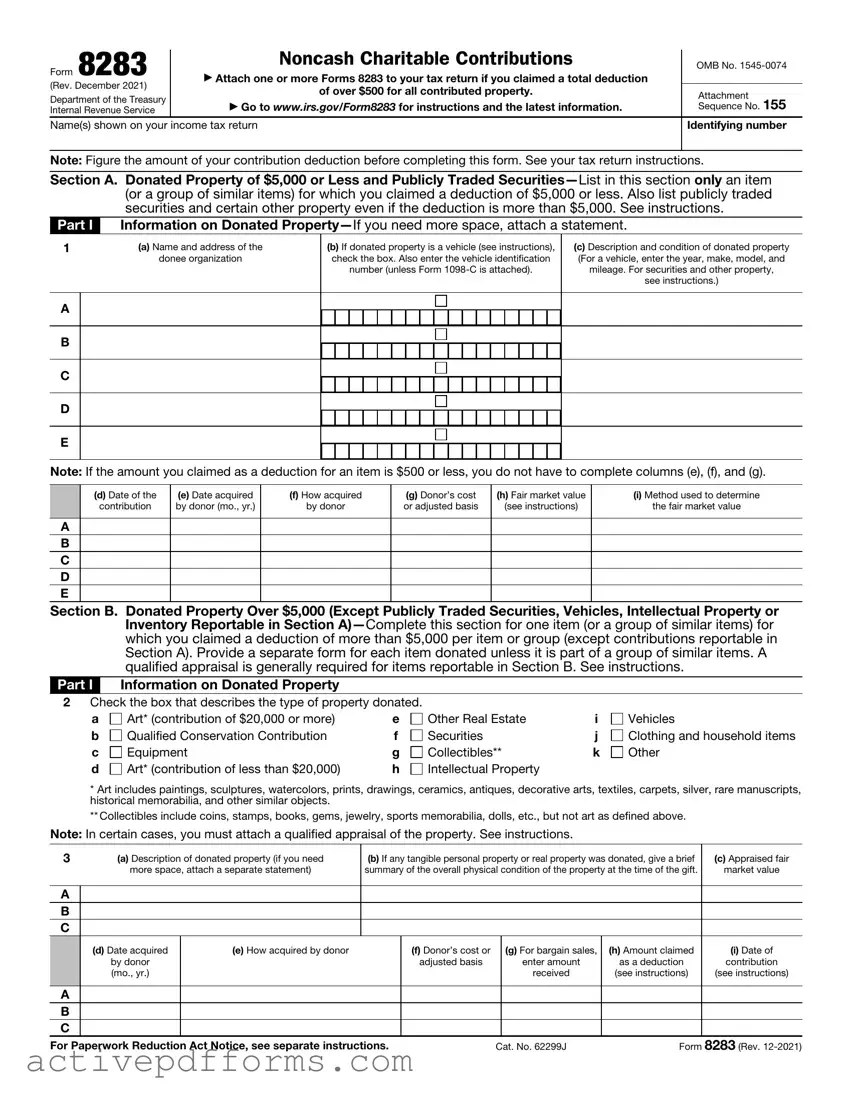

Note: Figure the amount of your contribution deduction before completing this form. See your tax return instructions.

Section A. Donated Property of $5,000 or Less and Publicly Traded

Part I |

Information on Donated |

|||||||||||||||||||

1 |

|

(a) Name and address of the |

(b) If donated property is a vehicle (see instructions), |

(c) Description and condition of donated property |

||||||||||||||||

|

|

donee organization |

check the box. Also enter the vehicle identification |

(For a vehicle, enter the year, make, model, and |

||||||||||||||||

|

|

|

|

|

number (unless Form |

mileage. For securities and other property, |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

see instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: If the amount you claimed as a deduction for an item is $500 or less, you do not have to complete columns (e), (f), and (g).

|

(d) Date of the |

(e) Date acquired |

(f) How acquired |

(g) Donor’s cost |

(h) Fair market value |

(i) Method used to determine |

|

contribution |

by donor (mo., yr.) |

by donor |

or adjusted basis |

(see instructions) |

the fair market value |

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

B |

|

|

|

|

|

|

C |

|

|

|

|

|

|

D |

|

|

|

|

|

|

E |

|

|

|

|

|

|

Section B. Donated Property Over $5,000 (Except Publicly Traded Securities, Vehicles, Intellectual Property or Inventory Reportable in Section

Part I Information on Donated Property

2Check the box that describes the type of property donated.

a |

Art* (contribution of $20,000 or more) |

e |

Other Real Estate |

i |

Vehicles |

b |

Qualified Conservation Contribution |

f |

Securities |

j |

Clothing and household items |

c |

Equipment |

g |

Collectibles** |

k |

Other |

d |

Art* (contribution of less than $20,000) |

h |

Intellectual Property |

|

|

*Art includes paintings, sculptures, watercolors, prints, drawings, ceramics, antiques, decorative arts, textiles, carpets, silver, rare manuscripts, historical memorabilia, and other similar objects.

**Collectibles include coins, stamps, books, gems, jewelry, sports memorabilia, dolls, etc., but not art as defined above.

Note: In certain cases, you must attach a qualified appraisal of the property. See instructions.

3 |

(a) Description of donated property (if you need |

(b) If any tangible personal property or real property was donated, give a brief |

(c) Appraised fair |

|||||

|

more space, attach a separate statement) |

summary of the overall physical condition of the property at the time of the gift. |

market value |

|||||

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

(d) Date acquired |

(e) How acquired by donor |

|

(f) Donor’s cost or |

|

(g) For bargain sales, |

(h) Amount claimed |

(i) Date of |

|

by donor |

|

|

adjusted basis |

|

enter amount |

as a deduction |

contribution |

|

(mo., yr.) |

|

|

|

|

received |

(see instructions) |

(see instructions) |

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 62299J |

Form |

8283 (Rev. |

|||||

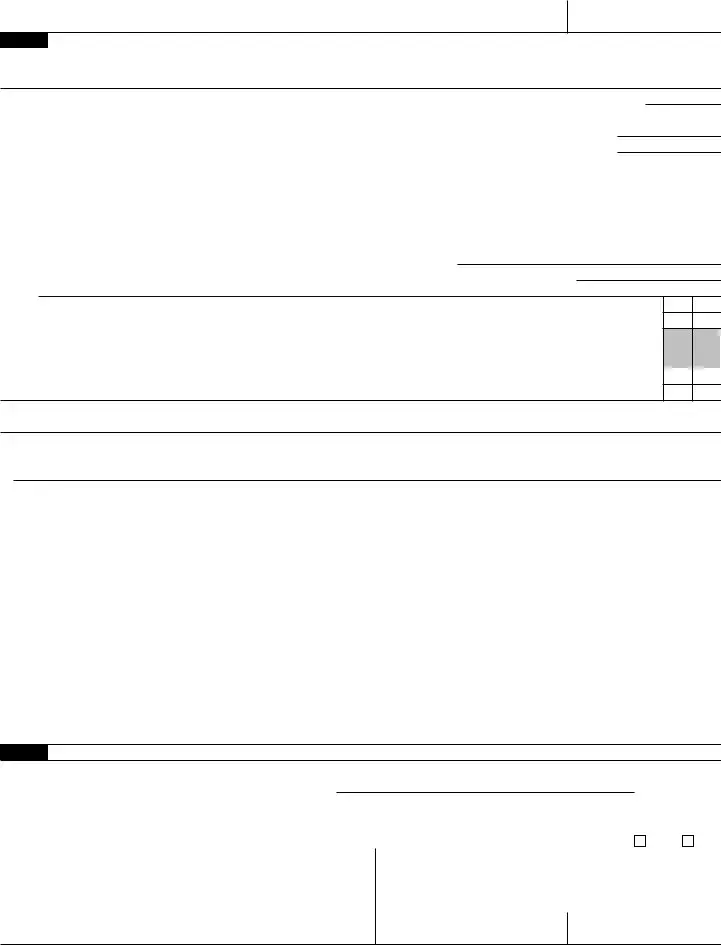

Form 8283 (Rev. |

Page 2 |

Name(s) shown on your income tax return |

Identifying number |

Part II Partial Interests and Restricted Use Property (Other Than Qualified Conservation Contributions)— Complete lines 4a through 4e if you gave less than an entire interest in a property listed in Section B, Part I. Complete lines 5a through 5c if conditions were placed on a contribution listed in Section B, Part I; also attach the required statement. See instructions.

4a Enter the letter from Section B, Part I that identifies the property for which you gave less than an entire interest ▶ If Section B, Part II applies to more than one property, attach a separate statement.

b Total amount claimed as a deduction for the property listed in Section B, Part I: (1) |

For this tax year . . ▶ |

(2) |

For any prior tax years ▶ |

cName and address of each organization to which any such contribution was made in a prior year (complete only if different from the donee organization in Section B, Part V, below):

Name of charitable organization (donee)

Address (number, street, and room or suite no.) |

City or town, state, and ZIP code |

|

|

dFor tangible property, enter the place where the property is located or kept ▶

eName of any person, other than the donee organization, having actual possession of the property ▶

Yes No

5a Is there a restriction, either temporary or permanent, on the donee’s right to use or dispose of the donated property?

bDid you give to anyone (other than the donee organization or another organization participating with the donee

organization in cooperative fundraising) the right to the income from the donated property or to the possession of the property, including the right to vote donated securities, to acquire the property by purchase or otherwise, or to designate the person having such income, possession, or right to acquire? . . . . . . . . . . . . .

cIs there a restriction limiting the donated property for a particular use? . . . . . . . . . . . . . .

Part III Taxpayer (Donor)

I declare that the following item(s) included in Section B, Part I above has to the best of my knowledge and belief an appraised value of not more than $500 (per item). Enter identifying letter from Section B, Part I and describe the specific item. See instructions.

▶

Signature of |

|

|

|

taxpayer (donor) ▶ |

Date ▶ |

||

Part IV |

|

Declaration of Appraiser |

|

I declare that I am not the donor, the donee, a party to the transaction in which the donor acquired the property, employed by, or related to any of the foregoing persons, or married to any person who is related to any of the foregoing persons. And, if regularly used by the donor, donee, or party to the transaction, I performed the majority of my appraisals during my tax year for other persons.

Also, I declare that I perform appraisals on a regular basis; and that because of my qualifications as described in the appraisal, I am qualified to make appraisals of the type of property being valued. I certify that the appraisal fees were not based on a percentage of the appraised property value. Furthermore, I understand that a false or fraudulent overstatement of the property value as described in the qualified appraisal or this Form 8283 may subject me to the penalty under section 6701(a) (aiding and abetting the understatement of tax liability). I understand that my appraisal will be used in connection with a return or claim for refund. I also understand that, if there is a substantial or gross valuation misstatement of the value of the property claimed on the return or claim for refund that is based on my appraisal, I may be subject to a penalty under section 6695A of the Internal Revenue Code, as well as other applicable penalties. I affirm that I have not been at any time in the

Sign |

Appraiser signature ▶ |

|

Date ▶ |

Here |

|

||

Appraiser name ▶ |

Title ▶ |

||

Business address (including room or suite no.) |

|

Identifying number |

|

|

|

|

|

City or town, state, and ZIP code

Part V Donee Acknowledgment

This charitable organization acknowledges that it is a qualified organization under section 170(c) and that it received the donated property as described in Section B, Part I, above on the following date ▶

Furthermore, this organization affirms that in the event it sells, exchanges, or otherwise disposes of the property described in Section B, Part I (or any portion thereof) within 3 years after the date of receipt, it will file Form 8282, Donee Information Return, with the IRS and give the donor a copy of that form. This acknowledgment does not represent agreement with the claimed fair market value.

Does the organization intend to use the property for an unrelated use? |

. . . . . . . . . . . |

. . . ▶ |

Yes |

No |

Name of charitable organization (donee) |

Employer identification number |

|

|

|

|

|

|

|

|

Address (number, street, and room or suite no.) |

City or town, state, and ZIP code |

|

|

|

|

|

|

|

|

Authorized signature |

Title |

Date |

|

|

Form 8283 (Rev.

| Fact Number | Description |

|---|---|

| 1 | The IRS Form 8283 is used to report information about non-cash charitable contributions. |

| 2 | This form is required for donations valued over $500. |

| 3 | Form 8283 is divided into two sections: Section A for items valued at $5,000 or less, and Section B for items valued more than $5,000. |

| 4 | For donations in Section B, a qualified appraisal must be attached to the form if the total deduction for all non-cash gifts is over $5,000. |

| 5 | Taxpayers must include the fair market value of the items at the time of the donation. |

| 6 | The form should be filed with your annual tax return to the IRS. |

| 7 | If you donate a single item or a group of similar items with a value of more than $500, detailed information about the donation must be provided, including how the value was determined. |

| 8 | The governing law for the IRS Form 8283 is the Internal Revenue Code, specifically sections related to charitable contributions and deductions. |

Filling out the IRS Form 8283 is necessary for anyone who has made a non-cash charitable contribution valued over $500. This form helps to report the value of your contribution to the IRS, ensuring that your charitable donation is accurately reflected in your tax obligations. The process involves several steps, from describing the donated property to acknowledging the receiving organization. Following these steps methodically will aid in completing the form correctly and efficiently.

After successfully completing and attaching the IRS Form 8283 to your tax return, the next steps involve waiting for acknowledgment from the IRS. This acknowledgment, often received with the processing of your tax return, officially recognizes your non-cash charitable contributions. Keeping a copy of the form for your records is wise, alongside any correspondence or receipt from the charity. These documents can be crucial for any future inquiries regarding your donation or tax return.

What is IRS Form 8283 and who needs to file it?

IRS Form 8283, Noncash Charitable Contributions, is a document that taxpayers in the United States must file if they claim a deduction for a charitable donation of property worth more than $500. This form documents the information about the donated property and the organizations receiving the donations. It is necessary for taxpayers who donate noncash items and want to reduce their taxable income through charitable giving.

What types of donations require Form 8283 to be filled out?

Donations that require Form 8283 include a wide range of noncash items such as vehicles, artwork, equipment, stocks that are not publicly traded, real estate, and other types of personal property. If the total value of all donated items exceeds $500 for the year, this form is necessary.

How do I determine the value of the items I donated?

The value of donated items should reflect their fair market value at the time of the donation. Fair market value is the price at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts. Taxpayers may need to consult appraisals for high-value items or use guidance from charities and tax professionals for more common items.

Are there any particular sections of Form 8283 that are more important?

All parts of Form 8283 are important; however, sections A and B have different requirements based on the value of the donated property. Section A is for items or groups of similar items valued at $500 to $5,000. Section B is for items over $5,000 and requires a qualified appraisal for each item listed, along with the signature of the appraiser and, in some cases, the charity receiving the donation.

Can I file Form 8283 electronically with my tax return?

Yes, Form 8283 can be filed electronically as part of your tax return if you are e-filing. The IRS accepts this form alongside your tax return through most tax preparation software. It is important to ensure that all required documentation, particularly for donations listed in Section B, is kept on file in case of an IRS audit.

What happens if I forget to include Form 8283 with my tax return?

If you forget to include Form 8283 with your tax return, it may result in the IRS disallowing your deduction for the noncash charitable contributions. If the omission was unintentional, you could be given the opportunity to correct the mistake by filing an amended return with the missing form. However, this depends on the IRS's discretion and the specific circumstances surrounding the oversight.

Is there a deadline for filing Form 8283?

Form 8283 should be filed with your annual tax return by the tax filing deadline, which is typically April 15 for most taxpayers. If you receive an extension to file your tax return, the same extended deadline applies to Form 8283. It is critical to adhere to these deadlines to benefit from the deduction for your noncash charitable contributions.

The IRS 8283 form is an essential document for those who have donated property valued at more than $500. It serves a critical function in ensuring donors receive the charity deduction they are entitled to on their tax returns. However, it's notoriously easy to trip up on the finer details. Let’s explore some common mistakes made when filling out this form:

Not Including All Required Information: Failure to fill in every necessary field can lead to the rejection of the form. This includes forgetting to list details such as the charity’s name, address, and a thorough description of the donated property.

Omitting the Date of Contribution: Each item or batch of items donated needs a corresponding date of contribution. This oversight can confuse the timeline of donations.

Incorrect Valuation of Donated Items: Many filers estimate the value of their donation inaccurately. Whether by overvaluation or undervaluation, this mistake can either diminish the rightful deduction or provoke scrutiny from the IRS.

Lack of Proper Documentation for Valuations Over $5000: For donated items or groups of similar items valued over $5000, an appraisal is required. Not attaching this appraisal is a common oversight.

Forgetting to Sign the Declaration of Appraiser: The form includes a section for the appraiser’s declaration that must be signed, certifying the appraisal’s accuracy. Overlooking this step can invalidate the necessary documentation.

Misunderstanding the Good Used Condition Requirement: The IRS mandates that clothing and household items be in good used condition or better to be deductible. Misinterpreting what qualifies can lead to errors in filing.

Failure to Report Carry-Over Contributions: Donors often miss reporting donations from previous years that were too large to fully deduct. This continuation, or carry-over, needs proper acknowledgment on the form.

Avoiding these mistakes requires careful attention to detail and a solid understanding of the form’s requirements. Below are some tips to help ensure a smooth process:

Review the IRS guidelines for non-cash charitable contributions before starting.

Keep detailed records of all donations, including receipts, appraisals, and a log of donated items.

Consider consulting a tax professional for high-value donations, especially if an appraisal is needed.

Double-check your form for accuracy and completeness before submission.

By familiarizing oneself with these common pitfalls and following these practical tips, donors can navigate the IRS 8283 form more effectively, ensuring their generous contributions are accurately reflected in their tax deductions.

When preparing and submitting the IRS Form 8283 for noncash charitable contributions, individuals often find it necessary to include additional documentation to fully comply with tax regulations and to support the claims made on this form. Understanding the various forms and documents that frequently accompany Form 8283 can simplify the filing process and help ensure accuracy and compliance.

Together, these forms and documents play a crucial role in the tax filing process, ensuring that charitable contributions are accurately reported and properly substantiated. It's important for donors to gather and organize these materials well in advance of tax deadlines to avoid any delays or issues with their tax returns.

IRS Form 1040, Schedule A: Similar to Form 8283, Schedule A of Form 1040 is used for itemizing deductions that taxpayers claim on their income tax returns, including charitable donations. However, Form 8283 is specifically for non-cash charitable contributions, detailing the donated property's condition and its fair market value.

IRS Form 1098-C: This form is closely related to Form 8283 as it pertains to donations of vehicles, boats, and airplanes. The donor needs to attach Form 1098-C to Form 8283 when a vehicle, boat, or airplane is donated, and the claimed value exceeds $500. It provides detailed information about the donation.

IRS Form 8282: Form 8282 is filed by organizations that receive charitable donations worth more than $5,000 and then sell, exchange, or otherwise dispose of the property within three years after receiving it. This form complements Form 8283 by disclosing the disposition of donated property, ensuring transparency and compliance.

IRS Form 8863: Although focused on education credits rather than charitable contributions, Form 8863 is similar to Form 8283 as it pertains to deductions and tax credits. Taxpayers use Form 8863 to claim education credits for qualified expenses, which, like charitable donations, can reduce taxable income.

IRS Form 8949: This form is used to report sales and other dispositions of capital assets, which may include assets that were once charitable contributions. Like Form 8283, which details non-cash charitable contributions, Form 8949 captures details that affect tax liability regarding the disposition of assets.

IRS Form 5695: Similar to Form 8283's purpose of reporting specific deductions to reduce tax liability, Form 5695 is used for claiming residential energy credits. Taxpayers fill out this form to claim credits for energy-saving improvements to their homes, akin to claiming deductions for charitable contributions.

IRS Form 2106: While Form 8283 is for non-cash charitable contributions, Form 2106 is used by employees to itemize job-related expenses. Both forms facilitate deductions that can lower the taxpayer's overall taxable income, although they focus on different types of deductions.

Filing out the IRS Form 8283, which is necessary for individuals who are claiming a deduction for a noncash charitable contribution, requires attention to detail and an understanding of the required information. Below are essential tips to ensure accuracy and compliance with the IRS rules.

Things You Should Do

Thoroughly document the donated property's condition, as this can significantly impact the value of your contribution and, consequently, the amount of your deduction.

Obtain a qualified appraisal for the donated items if their value exceeds $5,000, excluding stock. It's crucial to adhere to this requirement to validate your claim.

Ensure that the organization to which you’re donating is recognized as a tax-exempt charity by the IRS, enabling your contributions to be tax-deductible.

Include all required attachments, such as the qualified appraisal, with your Form 8283 if applicable based on the value of your donation.

Accurately describe the donated property on Section A or Section B of the form, depending on the value of the donation, to provide clear evidence of the donation's nature and value.

Sign and date the declaration on the form to attest to the accuracy of the information provided.

Keep a copy of the completed Form 8283 and all relevant documentation for your records, as these documents are crucial should the IRS have any questions or if an audit is conducted.

Things You Shouldn't Do

Do not underestimate the value of donated property, as doing so can lead to missed tax deduction opportunities. Conversely, overvaluing items can result in penalties and audits.

Avoid neglecting to secure a qualified appraisal when required. This oversight can invalidate your deduction for higher-value donations.

Do not donate to organizations without verifying their eligibility for tax-deductible contributions. Donations to ineligible entities cannot be deducted.

Refrain from submitting the form without proper verification and signatures from the donee organization, as this confirms receipt and acceptance of the donated property.

Avoid leaving sections blank or providing incomplete descriptions of the donated items. Inadequate information can lead to processing delays or the IRS questioning the validity of your donation.

Do not ignore IRS deadlines for filing Form 8283. Submitting the form late can jeopardize your ability to claim the deduction for the applicable tax year.

Avoid failing to consult with a tax professional if you're unsure about the form's requirements or your eligibility for claiming a deduction. This can prevent potential errors and ensure compliance with tax laws.

Understanding the IRS 8283 form is crucial for taxpayers who make non-cash charitable contributions. However, there are several misconceptions about this form that can lead to mistakes or confusion. Let's clear up some of the most common misunderstandings:

By understanding these misconceptions and the realities behind the IRS 8283 form, donors can navigate their charitable contributions more effectively and ensure compliance with IRS requirements.

The IRS 8283 form is required for individuals who make non-cash donations worth more than $500 in a given tax year. Understanding how to correctly fill out and use this form is crucial in ensuring compliance with IRS regulations and maximizing potential tax deductions. Here are key takeaways regarding this process:

Correctly filling out and using Form 8283 is essential for taxpayers making non-cash charitable contributions. By following these guidelines, individuals can ensure they receive the appropriate tax benefits while adhering to federal tax laws.

Flea Tick Certificate - Falsification of this certificate can lead to severe legal consequences, emphasizing the form's role in maintaining integrity in animal transportation.

Exit Interview Survey - Enables exploration of reasons behind employee disengagement and dissatisfaction.