Free IRS 8862 PDF Template

Free IRS 8862 PDF Template

When diving into the world of taxes, certain forms become pivotal for individuals looking to navigate their financial responsibilities effectively. Among these, the IRS 8862 form holds significant importance, especially for those seeking to reclaim eligibility for certain tax credits that they may have previously lost due to a variety of reasons, such as inaccuracies or discrepancies in past filings. This form acts as a portal to requalify for these vital tax benefits, including the Earned Income Tax Credit (EITC), allowing taxpayers to present their case for eligibility once again. The process, while straightforward to those familiar with tax procedures, can present a series of questions and require detailed attention to ensure that all the necessary information is accurately reported. Understanding the conditions under which one needs to file Form 8862, the specific details required within the form, and the consequent steps to regain tax credits, is crucial for anyone looking to navigate this situation successfully.

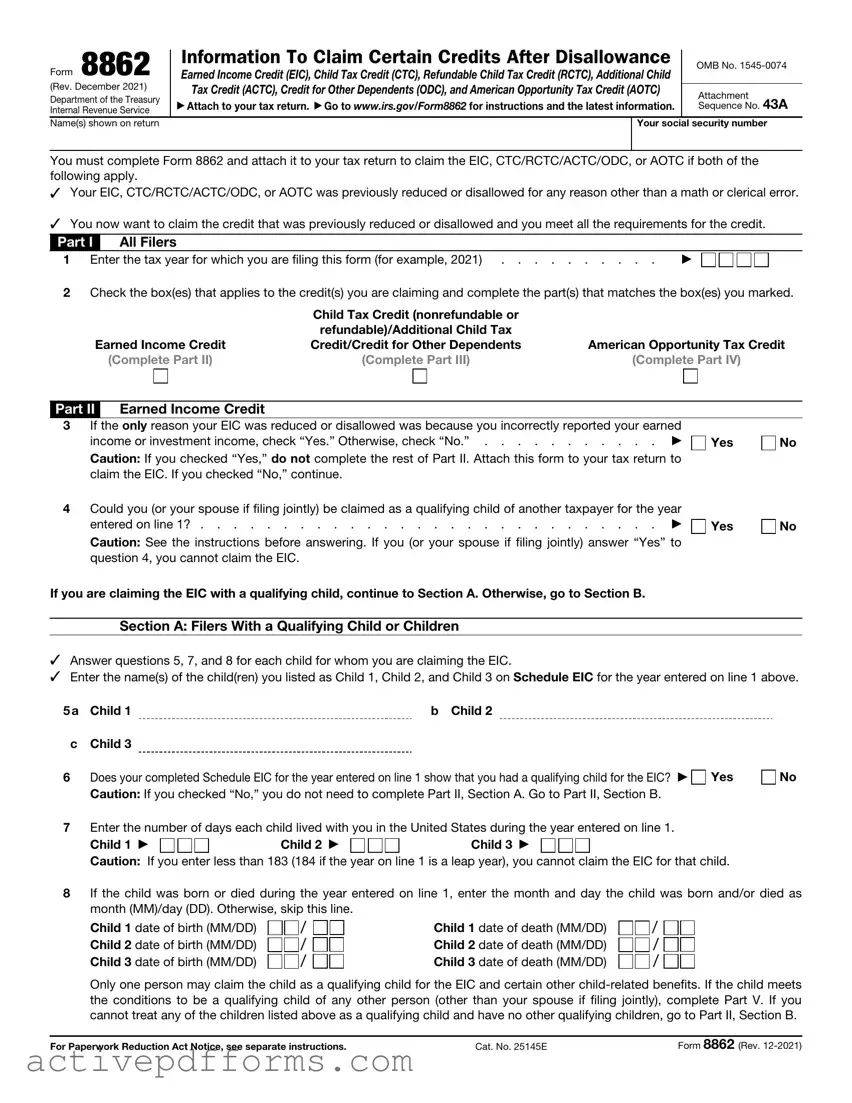

Form 8862 |

|

Information To Claim Certain Credits After Disallowance |

|

OMB No. |

|

|

|

||||

|

Earned Income Credit (EIC), Child Tax Credit (CTC), Refundable Child Tax Credit (RCTC), Additional Child |

|

|

||

(Rev. December 2021) |

|

Tax Credit (ACTC), Credit for Other Dependents (ODC), and American Opportunity Tax Credit (AOTC) |

|

|

|

|

|

Attachment |

|||

Department of the Treasury |

|

|

|

|

|

|

▶ Attach to your tax return. ▶ Go to www.irs.gov/Form8862 for instructions and the latest information. |

|

Sequence No. 43A |

||

Internal Revenue Service |

|

|

|||

|

|

|

|

|

|

Name(s) shown on return |

|

|

Your social security number |

||

|

|

|

|

|

|

You must complete Form 8862 and attach it to your tax return to claim the EIC, CTC/RCTC/ACTC/ODC, or AOTC if both of the following apply.

✓Your EIC, CTC/RCTC/ACTC/ODC, or AOTC was previously reduced or disallowed for any reason other than a math or clerical error.

✓You now want to claim the credit that was previously reduced or disallowed and you meet all the requirements for the credit.

Part I |

All Filers |

|

1 Enter the tax year for which you are filing this form (for example, 2021) |

▶ |

|

2Check the box(es) that applies to the credit(s) you are claiming and complete the part(s) that matches the box(es) you marked.

|

Child Tax Credit (nonrefundable or |

|

|

refundable)/Additional Child Tax |

|

Earned Income Credit |

Credit/Credit for Other Dependents |

American Opportunity Tax Credit |

(Complete Part II) |

(Complete Part III) |

(Complete Part IV) |

Part II Earned Income Credit

3If the only reason your EIC was reduced or disallowed was because you incorrectly reported your earned

income or investment income, check “Yes.” Otherwise, check “No.” . . . . . . . . . . . ▶ |

Yes |

No |

Caution: If you checked “Yes,” do not complete the rest of Part II. Attach this form to your tax return to |

|

|

claim the EIC. If you checked “No,” continue. |

|

|

4Could you (or your spouse if filing jointly) be claimed as a qualifying child of another taxpayer for the year

entered on line 1? . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ |

Yes |

No |

Caution: See the instructions before answering. If you (or your spouse if filing jointly) answer “Yes” to |

|

|

question 4, you cannot claim the EIC. |

|

|

If you are claiming the EIC with a qualifying child, continue to Section A. Otherwise, go to Section B. |

|

|

Section A: Filers With a Qualifying Child or Children

✓Answer questions 5, 7, and 8 for each child for whom you are claiming the EIC.

✓Enter the name(s) of the child(ren) you listed as Child 1, Child 2, and Child 3 on Schedule EIC for the year entered on line 1 above.

5a |

Child 1 |

b Child 2 |

|

|

c |

Child 3 |

|

|

|

6 |

Does your completed Schedule EIC for the year entered on line 1 show that you had a qualifying child for the EIC? ▶ |

Yes |

No |

|

|

Caution: If you checked “No,” you do not need to complete Part II, Section A. Go to Part II, Section B. |

|

|

|

7Enter the number of days each child lived with you in the United States during the year entered on line 1.

Child 1 ▶ |

Child 2 ▶ |

Child 3 ▶ |

Caution: If you enter less than 183 (184 if the year on line 1 is a leap year), you cannot claim the EIC for that child.

8If the child was born or died during the year entered on line 1, enter the month and day the child was born and/or died as month (MM)/day (DD). Otherwise, skip this line.

Child 1 date of birth (MM/DD) Child 2 date of birth (MM/DD) Child 3 date of birth (MM/DD)

/

/

/

/

/

/

Child 1 date of death (MM/DD) Child 2 date of death (MM/DD) Child 3 date of death (MM/DD)

/

/

/

/

/

/

Only one person may claim the child as a qualifying child for the EIC and certain other

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 25145E |

Form 8862 (Rev. |

Form 8862 (Rev. |

Page 2 |

Section B: Filers Without a Qualifying Child or Children |

|

9a Enter the number of days during the year entered on line 1 that your main home was in the United States . . |

. ▶ |

bIf married filing jointly, enter the number of days during the year entered on line 1 that your spouse’s main home was

|

in the United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ |

|

|

Caution: Members of the military stationed outside the United States during the year entered on line 1, see the instructions |

|

|

before answering. If you enter less than 183 (184 if the year on line 1 is a leap year) on either line 9a or 9b (if filing jointly), you |

|

|

cannot claim the EIC. |

|

10a |

Enter your age at the end of the year on line 1 |

|

b |

Enter your spouse’s age at the end of the year on line 1 |

|

|

Caution: If your spouse died during the year entered on line 1 or you are preparing a return for someone who died during the |

|

|

year entered on line 1, see the instructions before answering. If neither you (nor your spouse if filing jointly) met the applicable |

|

|

minimum or maximum age requirement at the end of the year on line 1, you cannot claim the EIC. See the Instructions for Form |

|

|

8862 for more information. |

|

11a Can you be claimed as a dependent on another taxpayer’s return? . . . . . . . . . . . . ▶

bCan your spouse (if filing jointly) be claimed as a dependent on another taxpayer’s return? . . . . ▶

Caution: If either you (or your spouse if filing jointly) answer “Yes” to question 11, you cannot claim the EIC.

Caution: If either you (or your spouse if filing jointly) answer “Yes” to question 11, you cannot claim the EIC.

Yes |

No |

Yes |

No |

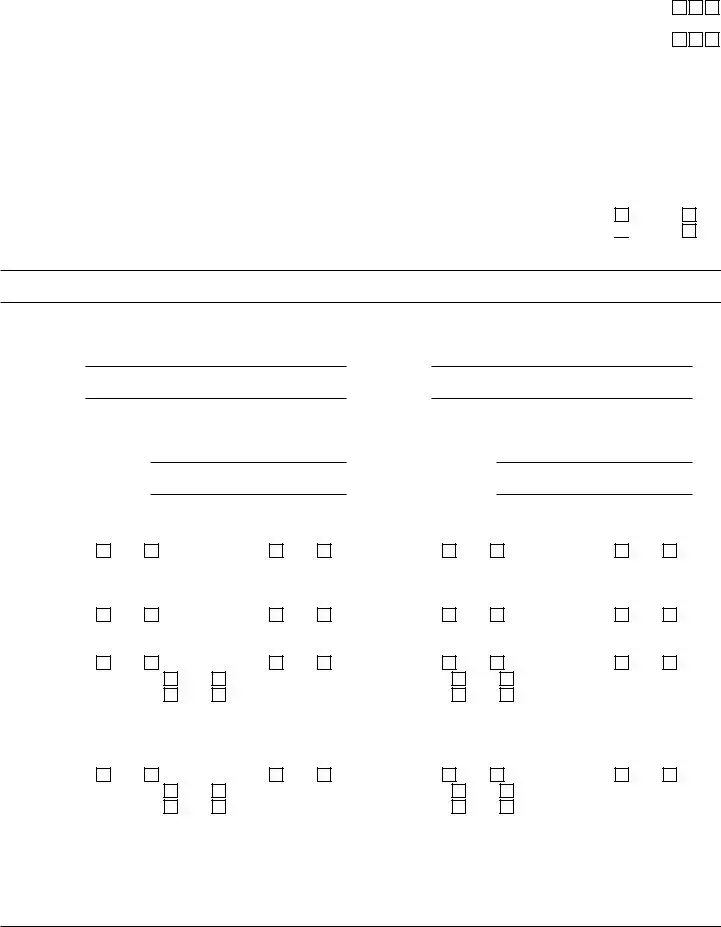

Part III Child Tax Credit (nonrefundable or refundable)/Additional Child Tax Credit/Credit for Other Dependents

12Enter the name(s) of each child for whom you are claiming the child tax credit/refundable child tax credit/additional child tax credit (CTC/RCTC/ACTC). If you are claiming the CTC/RCTC/ACTC for more than four qualifying children, attach a statement also answering questions 12 and

a |

Child 1 |

b |

Child 2 |

c |

Child 3 |

d |

Child 4 |

13Enter the name(s) of each person for whom you are claiming the credit for other dependents (ODC). If you are claiming the credit for more than four dependents, attach a statement answering questions 13, 16, and 17 for those dependents.

a |

Other dependent 1 |

b |

Other dependent 2 |

c |

Other dependent 3 |

d |

Other dependent 4 |

14For each child listed in response to question 12, did the child live with you for more than half of the year or meet an exception described in the instructions?

Child 1 |

Yes |

No |

Child 2 |

Yes |

No |

Child 3 |

Yes |

No |

Child 4 |

Yes |

No |

15For each child listed in response to question 12, did the child meet the requirements to be a qualifying child for the CTC/RCTC/ ACTC?

Child 1 |

Yes |

No |

Child 2 |

Yes |

No |

Child 3 |

Yes |

No |

Child 4 |

Yes |

No |

16For each person claimed as a qualifying child or other dependent for the CTC/RCTC/ACTC/ODC, is that person your dependent?

Child 1 |

Yes |

No |

|

Child 2 |

Yes |

No |

Child 3 |

Yes |

No |

Child 4 |

Yes |

No |

Other dependent 1 |

|

Yes |

No |

|

Other dependent 2 |

Yes |

No |

|

|

|

||

Other dependent 3 |

|

Yes |

No |

|

Other dependent 4 |

Yes |

No |

|

|

|

||

17For each person claimed as a qualifying child or other dependent for the CTC/RCTC/ACTC/ODC, is that person a citizen, national, or resident of the United States? See Pub. 519 for more information on when a person is a resident of the United States or is treated as a resident of the United States.

Child 1 |

Yes |

No |

|

Child 2 |

Yes |

No |

Child 3 |

Yes |

No |

Child 4 |

Yes |

No |

Other dependent 1 |

|

Yes |

No |

|

Other dependent 2 |

Yes |

No |

|

|

|

||

Other dependent 3 |

|

Yes |

No |

|

Other dependent 4 |

Yes |

No |

|

|

|

||

Caution: If the answer is “No” for questions 14, 15, 16, or 17, you cannot claim the CTC/RCTC/ACTC/ODC for that child or other dependent.

Only one person can claim the child as a qualifying child for the CTC/RCTC/ACTC/ODC. If the child meets the conditions to be a qualifying child of any other person (other than your spouse if filing jointly), complete Part V. If you cannot treat any of the children listed above as a qualifying child and have no other qualifying children, you cannot claim the CTC/RCTC/ACTC or the ODC based on having a qualifying child. If you are a noncustodial parent who is entitled to treat the child as a qualifying child, you do not need to complete Part V.

Form 8862 (Rev.

Form 8862 (Rev. |

Page 3 |

|

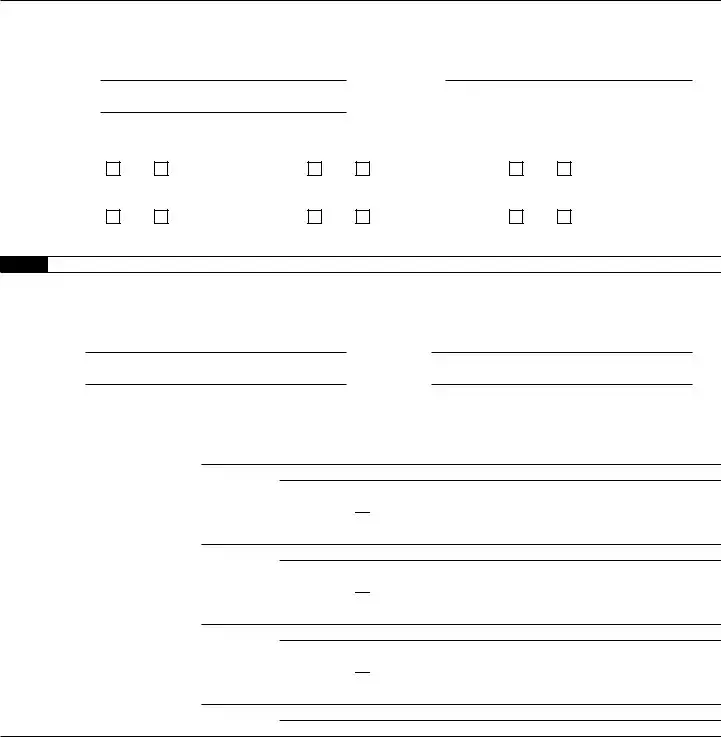

Part IV |

American Opportunity Tax Credit |

|

✓Answer the following questions for each student for whom you are claiming the AOTC. If you have more than three students, attach a statement also answering questions 18 and 19 for those students.

✓Enter the name(s) of the student(s) as listed on Form 8863.

18a |

Student 1 |

|

|

|

b |

Student 2 |

|

|

|

c |

Student 3 |

|

|

|

|

|

|

|

|

19a |

Did the student meet the requirements to be an eligible student for purposes of the AOTC for the year entered on line 1? See |

||||||||

|

Pub. 970 for more information. |

|

|

|

|

|

|

||

|

Student 1 |

Yes |

No |

Student 2 |

Yes |

No |

Student 3 |

Yes |

No |

bHas the Hope Scholarship Credit or AOTC been claimed for the student for any 4 tax years before the year entered on line 1?

Student 1 |

Yes |

No |

Student 2 |

Yes |

No |

Student 3 |

Yes |

No |

Caution: If you answered “No” to question 19a or “Yes” to question 19b, you cannot claim the credit for that student.

Part V Qualifying Child of More Than One Person

✓Answer the following questions for each child who meets the conditions to be a qualifying child of any other person (other than your spouse if filing jointly). If you have more than four qualifying children, attach a statement also answering questions

20a |

Child 1 |

b |

Child 2 |

c |

Child 3 |

d |

Child 4 |

21Enter the address where you and the child lived together during the year entered on line 1. If you lived with the child at more than one address during the year, attach a list of the addresses where you lived.

Child 1 ▶ Number and street

City or town, state, and ZIP code

Child 2 ▶ If same as shown for Child 1, check this box ▶

Number and street

City or town, state, and ZIP code

Child 3 ▶ If same as shown for Child 1, check this box ▶

Number and street

City or town, state, and ZIP code

Child 4 ▶ If same as shown for Child 1, check this box ▶

Number and street

City or town, state, and ZIP code

Otherwise, enter below.

Otherwise, enter below.

Otherwise, enter below.

Form 8862 (Rev.

Form 8862 (Rev. |

Page 4 |

|

Part V |

Qualifying Child of More Than One Person (continued) |

|

22Did any other person (except your spouse, if filing jointly, and your dependents claimed on your return)

live with Child 1, Child 2, Child 3, or Child 4 for more than half the year? |

Yes |

No |

If “Yes,” enter the relationship of each person to the child on the appropriate line below. |

|

|

Other person living with Child 1: Name

Relationship to Child 1

Other person living with Child 2: If same as shown for Child 1, check this box ▶

Name

Relationship to Child 2

Other person living with Child 3: If same as shown for Child 1, check this box ▶

Name

Relationship to Child 3

Other person living with Child 4: If same as shown for Child 1, check this box ▶

Name

Relationship to Child 4

Otherwise, enter below.

Otherwise, enter below.

Otherwise, enter below.

To determine which person can treat the child as a qualifying child for the EIC and CTC/RCTC/ACTC, see Qualifying Child of More Than One Person in Pub. 501.

Note: The IRS may ask you to provide additional information to verify your eligibility to claim each credit.

Form 8862 (Rev.

| Fact Number | Detail |

|---|---|

| 1 | The IRS 8862 form is officially titled "Information To Claim Earned Income Credit After Disallowance". |

| 2 | It is used by taxpayers who have had their Earned Income Credit (EIC) previously denied or reduced and wish to claim it again. |

| 3 | Filing this form is necessary if you are required to meet certain criteria to requalify for the EIC after disallowance. |

| 4 | The form is part of the process to prove to the IRS that you are eligible for the EIC for a subsequent tax year. |

| 5 | IRS 8862 must be filed with your tax return if your EIC was previously disallowed for reasons other than a mathematical or clerical error. |

| 6 | You do not need to file Form 8862 if your EIC claim was reduced or disallowed for reasons related solely to a math or clerical error on your part. |

| 7 | There are specific situations where you do not need to file Form 8862, such as if the IRS determines you fraudulently claimed the EIC in the past. |

| 8 | The form requires detailed information about your income, filing status, qualifying children, and other factors affecting your EIC eligibility. |

| 9 | While the IRS 8862 is a federal form, it does not require consideration of state-specific laws as it pertains solely to federal tax returns. |

Filling out the IRS Form 8862 is a necessary step for individuals whose Earned Income Tax Credit (EITC) was previously denied or reduced and who wish to claim it again. After completing this form, the next steps involve attaching it to your federal tax return before submission. This process helps the IRS determine your eligibility for the EITC in the current tax year. Ensure that you provide accurate information to avoid any delays or additional scrutiny from the IRS. Here are the detailed steps to fill out Form 8862 effectively.

Once the form is completed, attach it to your federal tax return. Double-check your return and Form 8862 for accuracy to prevent any processing issues. Submitting accurate and complete information will expedite the review process and increase the likelihood of your EITC claim being accepted.

What is IRS Form 8862?

IRS Form 8862, "Information To Claim Certain Credits After Disallowance," is a document taxpayers must file with the U.S. Internal Revenue Service (IRS) if they wish to reclaim eligibility for certain tax credits. These credits may have been previously disallowed or reduced in a prior tax year. Essentially, Form 8862 is used to inform the IRS that a taxpayer now meets the requirements for a credit they were previously denied.

Which credits does IRS Form 8862 relate to?

IRS Form 8862 is primarily associated with the Earned Income Credit (EIC). However, it may also pertain to other credits as specified by the IRS, such as the Child Tax Credit (CTC), Additional Child Tax Credit (ACTC), American Opportunity Tax Credit (AOTC), and the Premium Tax Credit (PTC) under certain circumstances.

When do I need to file Form 8862?

You must file Form 8862 if the IRS has previously disallowed or denied one of the relevant credits and you wish to claim the same credit or credits in a subsequent tax year. The requirement to file this form typically arises if you were found to have improperly claimed a credit due to an unintentional error or misunderstanding of tax law. Note that there are specific conditions under which you need not file Form 8862 again, such as after it has been accepted for a credit in a subsequent year.

How do I know if I'm eligible to file Form 8862?

Eligibility to file Form 8862 depends on receiving a notice from the IRS stating that your previous claim for a tax credit was disallowed and that you can re-qualify by meeting certain criteria. Additionally, you should not file Form 8862 if the disallowance was due to a determination of fraud or recklessness on your part.

What information do I need to provide on Form 8862?

On Form 8862, you'll need to provide detailed information about your tax and financial situation. This includes your filing status, number of qualifying children (if claiming credits related to dependents), total income, and other details specific to the credit you're claiming. The form will guide you through the required information based on the tax credit you wish to claim.

Can I file IRS Form 8862 electronically?

Yes, IRS Form 8862 can be filed electronically along with your tax return. Most modern tax preparation software supports electronic filing of this form. Filing electronically is generally faster and reduces the risk of errors compared to paper filing.

What happens after I file Form 8862?

After filing Form 8862, the IRS will review your submission as part of processing your tax return. If the form is properly completed and you meet all eligibility requirements, your previously disallowed credit may be reinstated. The IRS may also contact you for additional information or documentation to support your claim. It is crucial to respond promptly to any IRS inquiries to avoid delays in processing your credit.

Where can I get help with filling out Form 8862?

If you need assistance with Form 8862, several resources are available. The IRS website provides instructions and frequently asked questions about the form. Additionally, tax preparation software often offers guidance. For personalized help, consider consulting a tax professional or an accountant who can provide advice based on your specific situation.

Filling out IRS form 8862 is a critical step for individuals who are looking to claim certain credits after previously being disallowed. This form is used to ensure taxpayers can rightfully claim their Earned Income Credit, American Opportunity Credit, or other similar credits on their tax returns. However, mistakes can easily be made during this process, resulting in delays or the denial of these valuable credits. Here are seven common mistakes to avoid:

Not checking eligibility criteria before filling out the form. Taxpayers must meet specific requirements to claim credits, and failing to meet these criteria means the form is unnecessary.

Incorrectly reporting income or expenses. Accuracy is paramount when filling out any IRS form. Misreporting can lead to audits or penalties, in addition to delays in processing the form.

Omitting necessary documentation. Supporting documents, such as income statements or proof of expenses, are often required. Failure to attach these can result in the IRS being unable to verify claims on the form.

Entering incorrect tax year information. It's easy to mistakenly use information from the wrong year. This error can lead to considerable confusion and delay the acceptance of the form.

Failing to sign and date the form. An unsigned form is considered incomplete by the IRS and will not be processed.

Using outdated forms. Tax laws change, and so do IRS forms. Using an outdated form can mean that vital information is missing or improperly provided.

Not consulting a tax professional when necessary. Taxpayers who find the form confusing or intricate should seek assistance. A professional can provide clarity and ensure that the form is filled out correctly.

Ensuring accuracy and completeness when filling out IRS form 8862 is crucial for the timely processing of your tax return and the successful reclaiming of important tax credits. Avoiding these mistakes can save a lot of time and potential headaches, making the process smoother and more efficient.

When individuals find themselves needing to file the IRS 8862 form, which is typically used to claim the Earned Income Credit (EIC) after it was previously disallowed, there are various other forms and documents that often accompany it. The 8862 form serves as a crucial step for taxpayers to once again become eligible for the EIC, a significant tax credit for low-to-moderate-income working individuals and families. To ensure a comprehensive and compliant tax filing process, particularly concerning reclaiming eligibility for the EIC, understanding the associated documents that might need to be filed alongside the IRS 8862 form is beneficial.

Filing taxes accurately is a vital responsibility that requires careful attention to detail and thorough documentation. For taxpayers aiming to claim the Earned Income Credit after a disqualification, properly completing and submitting the IRS 8862 form along with the pertinent supplementary documents is crucial. This not only ensures compliance with tax laws but also facilitates the proper administration of tax benefits such as the EIC, fostering financial equity and support for eligible individuals and families.

The IRS Form 1040 is similar to the IRS 8862 form as both are integral to the individual income tax return process. The 1040 serves as the primary form that taxpayers use to file their annual income tax returns, detailing income, deductions, and credits. The similarity lies in their use for reporting critical tax information, although the 1040 encompasses a broader range of data.

The IRS Form W-2 also shares similarities with the 8862 form. The W-2 is issued by employers to employees, detailing the employee's annual wages and the amount of taxes withheld from their paycheck. Like the 8862, it provides specific, essential information required for accurately completing one’s tax obligations, although the W-2 focuses on income and tax withholding from employment.

IRS Form 1099 series, particularly the 1099-MISC, resemble the 8862 in their role in reporting specific types of income. The 1099 forms are used to report income from sources other than wages, salaries, and tips, such as freelance income, interest, and dividends. Both sets of forms are critical for ensuring that taxpayers account for all sources of income in their tax returns.

The IRS Form 8863, which is used to claim education credits, is similar to the 8862 in that both forms involve calculations to determine eligibility for certain tax benefits. They are specifically tailored to claim particular benefits, with the 8862 focused on earned income credits and the 8863 on education credits.

IRS Form 8857, used for requesting relief from joint tax liability under the Innocent Spouse Relief provisions, shares the concept of adjusting tax responsibility with the 8862. Both forms are used to modify an individual's tax obligations based on specific circumstances, although the contexts and reasons differ significantly.

The Schedule C (Form 1040) is akin to the 8862 as it pertains to reporting income or loss from a business operated or a profession practiced as a sole proprietor. Both documents are crucial for taxpayers who need to detail particular financial information that impacts their tax calculations and credits.

IRS Form 2441, Child and Dependent Care Expenses, is similar to the 8862 form in that it allows taxpayers to claim specific tax deductions or credits related to personal situations, in this case, expenses associated with child or dependent care. These forms cater to taxpayers looking to reduce their taxable income by reporting qualifying expenses or credits.

When completing the IRS Form 8862, it's essential to understand both what you should and shouldn't do to ensure the process is smooth and accurate. Below is a list of recommended practices to adopt, as well as common pitfalls to avoid.

Do:

Don't:

Understanding the IRS Form 8862 can be complex, leading to various misconceptions among taxpayers. The form, critical for those looking to claim certain credits after disallowance, is often misunderstood. Below are eight common misconceptions about the IRS Form 8862, which are imperative to clarify for accurate tax filing.

Form 8862 is only for Earned Income Credit (EIC) Filers: While it's commonly associated with the EIC, IRS Form 8862 must also be completed by individuals who are reclaiming the American Opportunity Credit, the Child Tax Credit, and other related credits after previously being denied these benefits.

Once Disallowed, Always Disallowed: Some believe that once their claim for a particular credit has been disallowed, they can never claim it again. However, Form 8862 serves precisely to allow taxpayers to reclaim these credits in future tax years, under certain conditions, once they fulfill the eligibility criteria.

Filing Form 8862 Automatically Qualifies You for the Credit: Filing this form does not guarantee that the credit will be granted. The IRS requires Form 8862 to reconsider eligibility, but all other qualifying criteria for the credit must still be met.

Form 8862 Needs to Be Filed Every Year: Many believe they need to file this form with their tax return every year to claim certain credits. However, it is typically only required once—the year following the IRS's disallowance of the credit—provided the taxpayer remains eligible for the credit(s) and the IRS does not require it to be filed again due to subsequent disallowances.

No Supporting Documentation is Needed: While the form itself is a statement of eligibility, it is often necessary to provide additional documentation or information to support the claim for the tax credits. This may include income statements or proof of residency, among others.

The Form Only Affects Federal Taxes: While it's true that IRS Form 8862 relates to federal income tax credits, the outcomes of these credits can influence state tax liabilities in states that base their tax calculations on federal taxable income or tax liability.

Form 8862 Must Be Submitted Separately: Some taxpayers mistakenly believe that Form 8862 should be submitted independently of their tax return. Actually, it should be attached to your federal income tax return during the year in which you are requesting the IRS to reconsider your eligibility for the credits.

Form 8862 is a Substitute for Legal Advice: No form can replace the value of personalized legal or tax advice. Misinterpreting the purpose of Form 8862 or how to correctly fill it out can lead to errors in tax filing. Consulting with a tax professional or legal advisor familiar with your specific situation is always recommended if there are uncertainties or specific circumstances that need attention.

Dispelling these misconceptions is essential for correct tax filing and to ensure taxpayers can rightfully claim the credits to which they are entitled. Awareness and understanding of IRS Form 8862's actual requirements and effects are crucial steps toward this goal.

The IRS Form 8862, "Information To Claim Certain Credits After Disallowance," is a crucial document for taxpayers who are looking to claim certain tax credits after a previous disallowance. Understanding the key aspects of this form can help individuals efficiently navigate potential hurdles in claiming deserved credits. Here are four key takeaways regarding the filling out and usage of the IRS 8862 form:

Filing Form 8862 can be a stepping stone to reclaiming valuable tax credits. Taxpayers should approach this process with thoroughness and attention to detail, ensuring that all the required information is correctly provided. This diligence will aid in the smooth processing of their claims and the successful reclaiming of credits that can make a significant difference in their tax returns.

Caqh System - Details on correcting entries online or via help desk to avoid application delays.

Da 7666 - The DA 7666 can also be a crucial piece of evidence in legal disputes involving the guardianship and rights over minors.