Free IRS Power of Attorney ( 2848) PDF Template

Free IRS Power of Attorney ( 2848) PDF Template

When it comes to dealing with the IRS, the thought can be daunting for many. Tax matters often involve complex rules and regulations, making it challenging for individuals to navigate the process on their own. Recognizing this, the IRS allows taxpayers to designate a representative to act on their behalf through the IRS Power of Attorney (POA) form, officially known as Form 2848. This key document enables tax professionals, such as attorneys, certified public accountants, or other individuals authorized to practice before the IRS, to receive confidential tax information and advocate for taxpayers. The form facilitates a smoother interaction with the IRS, allowing representatives to perform a variety of tasks such as negotiating payment plans, resolving tax disputes, and attending meetings. Its versatility makes it an essential tool for anyone seeking professional assistance with tax matters, providing peace of mind by ensuring they are well-represented in dealings with one of the government's most formidable agencies.

Check Form for Common Errors & Reminders

Form 2848 |

|

Power of Attorney |

For IRS Use Only |

|||||

|

|

|

|

OMB No. |

||||

(Rev. January 2021) |

and Declaration of Representative |

|

|

|

|

|

||

Received by: |

|

|||||||

Department of the Treasury |

|

|

|

|||||

▶ Go to www.irs.gov/Form2848 for instructions and the latest information. |

|

|

|

|

|

|||

Internal Revenue Service |

Name |

|

|

|||||

|

|

|

||||||

Part I |

Power of Attorney |

Telephone |

|

|

||||

|

Caution: A separate Form 2848 must be completed for each taxpayer. Form 2848 will not be honored |

Function |

|

|

||||

|

for any purpose other than representation before the IRS. |

Date |

/ / |

|||||

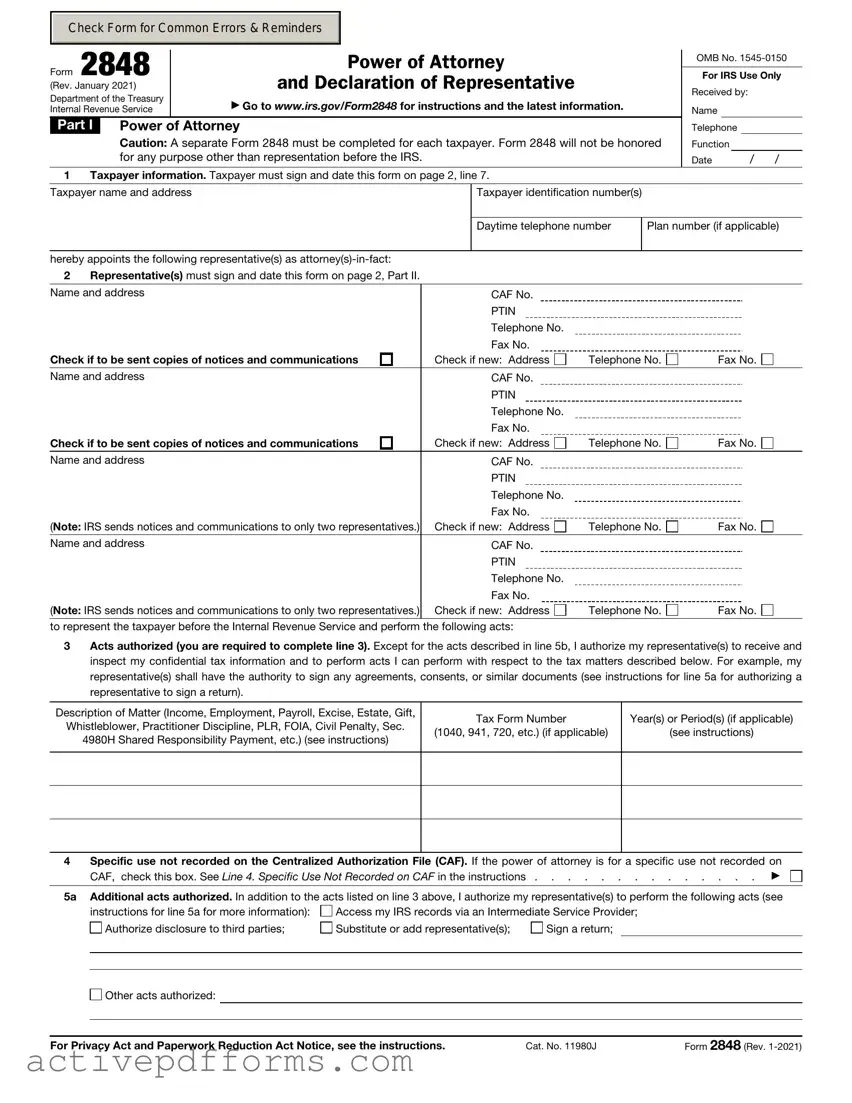

1Taxpayer information. Taxpayer must sign and date this form on page 2, line 7.

Taxpayer name and address |

Taxpayer identification number(s) |

Daytime telephone number

Plan number (if applicable)

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

to represent the taxpayer before the Internal Revenue Service and perform the following acts:

3Acts authorized (you are required to complete line 3). Except for the acts described in line 5b, I authorize my representative(s) to receive and inspect my confidential tax information and to perform acts I can perform with respect to the tax matters described below. For example, my representative(s) shall have the authority to sign any agreements, consents, or similar documents (see instructions for line 5a for authorizing a representative to sign a return).

Description of Matter (Income, Employment, Payroll, Excise, Estate, Gift, |

Tax Form Number |

Year(s) or Period(s) (if applicable) |

|

Whistleblower, Practitioner Discipline, PLR, FOIA, Civil Penalty, Sec. |

|||

(1040, 941, 720, etc.) (if applicable) |

(see instructions) |

||

4980H Shared Responsibility Payment, etc.) (see instructions) |

|||

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Specific use not recorded on the Centralized Authorization File (CAF). If the power of attorney is for a specific use not recorded on |

|||

|

CAF, check this box. See Line 4. Specific Use Not Recorded on CAF in the instructions . |

. . . . . . . . . . . . . ▶ |

||

|

|

|

||

5a |

Additional acts authorized. In addition to the acts listed on line 3 above, I authorize my representative(s) to perform the following acts (see |

|||

|

instructions for line 5a for more information): |

Access my IRS records via an Intermediate Service Provider; |

||

|

Authorize disclosure to third parties; |

Substitute or add representative(s); |

Sign a return; |

|

|

|

|

|

|

|

|

|

|

|

Other acts authorized:

For Privacy Act and Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 11980J |

Form 2848 (Rev. |

Form 2848 (Rev. |

Page 2 |

bSpecific acts not authorized. My representative(s) is (are) not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative(s) or any firm or other entity with whom the representative(s) is (are) associated) issued by the government in respect of a federal tax liability.

List any other specific deletions to the acts otherwise authorized in this power of attorney (see instructions for line 5b):

6Retention/revocation of prior power(s) of attorney. The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Internal Revenue Service for the same matters and years or periods covered by this form. If you do not want to

revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7Taxpayer declaration and signature. If a tax matter concerns a year in which a joint return was filed, each spouse must file a separate power of attorney even if they are appointing the same representative(s). If signed by a corporate officer, partner, guardian, tax matters partner, partnership representative (or designated individual, if applicable), executor, receiver, administrator, trustee, or individual other than the taxpayer, I certify I have the legal authority to execute this form on behalf of the taxpayer.

▶ IF NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THIS POWER OF ATTORNEY TO THE TAXPAYER.

Signature |

Date |

Title (if applicable) |

Print name |

|

Print name of taxpayer from line 1 if other than individual |

Part II Declaration of Representative

Under penalties of perjury, by my signature below I declare that:

•I am not currently suspended or disbarred from practice, or ineligible for practice, before the Internal Revenue Service;

•I am subject to regulations in Circular 230 (31 CFR, Subtitle A, Part 10), as amended, governing practice before the Internal Revenue Service;

•I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

•I am one of the following:

a

bCertified Public

cEnrolled

d

e

fFamily

gEnrolled

hUnenrolled Return

kQualifying Student or Law

rEnrolled Retirement Plan

▶IF THIS DECLARATION OF REPRESENTATIVE IS NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THE POWER OF ATTORNEY. REPRESENTATIVES MUST SIGN IN THE ORDER LISTED IN PART I, LINE 2.

Note: For designations

Designation—

Insert above

letter

Licensing jurisdiction

(State) or other

licensing authority

(if applicable)

Bar, license, certification, registration, or enrollment number (if applicable)

Signature

Date

Form 2848 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Power of Attorney (Form 2848) allows a taxpayer to grant authority to an individual, often a tax professional, to represent them before the IRS. |

| Eligibility for Representatives | Representatives must be eligible to practice before the IRS, including attorneys, CPAs, and enrolled agents. |

| Scope of Authority | This form specifies the tax matters and years or periods for which representation is authorized. |

| Execution Requirements | The taxpayer and their chosen representative must both sign and date the form for it to be valid. |

| Filing Method | The completed Form 2848 can be mailed or faxed to the IRS, depending on the taxpayer's location and the specifics of their request. |

| Duration of Authority | Authority granted on Form 2848 generally remains in effect until it is revoked by the taxpayer or the representative, or it expires under IRS rules. |

| Revocation Process | To revoke the authority, the taxpayer must send a written notice to the IRS, specifying the revocation of power of attorney. |

| State-Specific Forms | Some states require their own form instead of, or in addition to, Form 2848 for state tax matters, governed by individual state laws. |

| Legal Significance | Signing Form 2848 legally allows the representative to receive confidential tax information and act on the taxpayer's behalf in matters with the IRS. |

The IRS Power of Attorney (Form 2848) plays a significant role for individuals or entities who wish to authorize someone else to represent them before the IRS. Filling out this form correctly is paramount to ensure that the designated representative can perform necessary actions such as receiving confidential tax information and making agreements with the IRS on the taxpayer’s behalf. Below is a systematic guide to help you through the process of completing the form.

Upon completing these steps, review the form thoroughly for any errors or omissions. An accurately completed Form 2848 is essential for seamless processing by the IRS. Once the form is filled out and verified for completeness and correctness, it should be mailed or faxed to the IRS office designated for the taxpayer’s location, as per the instructions provided with the form. This step is crucial for the authorization to be recognized and for the representative to begin acting on the taxpayer's behalf in dealings with the IRS.

What is the IRS Power of Attorney (Form 2848) and when is it used?

The IRS Power of Attorney (Form 2848) is a legal document that allows individuals to authorize someone else, typically a tax professional, to represent them before the Internal Revenue Service (IRS). This representation may include receiving confidential tax information and acting on the taxpayer's behalf in matters such as audits, appeals, and tax collection issues. The form is used when taxpayers need professional assistance with their taxes and wish to grant specific powers to their chosen representatives to handle tax matters directly with the IRS.

Who can be designated as a representative on Form 2848?

On Form 2848, taxpayers can designate individuals who are eligible to practice before the IRS. This includes attorneys, certified public accountants (CPAs), enrolled agents, enrolled actuaries, enrolled retirement plan agents, and certain other individuals who are in good standing with the IRS. The representative must have a Preparer Tax Identification Number (PTIN) to be listed on the form. It’s important to choose a representative who is competent and trustworthy, as they will have access to sensitive tax information and the ability to make decisions on the taxpayer’s behalf.

How do you file Form 2848 with the IRS?

Form 2848 can be filed through mail or fax, depending on the taxpayer’s preference and the IRS guidelines. The completed form must include the taxpayer’s name, social security number or taxpayer identification number, and the specific tax matters and years or periods for which authorization is granted. The designated representative’s declaration of eligibility and signature are also required. Once the form is completed and signed, it should be sent to the IRS office designated for the taxpayer’s location, as specified in the form’s instructions.

Does Form 2848 need to be renewed, and if so, how often?

Form 2848 remains in effect until it is revoked by the taxpayer, the authorization naturally expires, or the representation ends due to completion of the tax matters for which it was granted. There is no set renewal period; however, if the taxpayer needs to extend the time or scope of representation, they must submit a new Form 2848. Additionally, if the taxpayer wishes to change representatives, they must file a new form indicating the new representative’s information and revoke the previous authorization if necessary.

Can a taxpayer revoke a Power of Attorney granted through Form 2848?

Yes, a taxpayer can revoke a Power of Attorney granted through Form 2848 at any time. To do so, the taxpayer must provide written notice to the IRS, specifying that the power of attorney is being revoked. Another method is filing a new Form 2848 with a different representative listed, which automatically revokes the prior authorization. It is recommended to notify the previous representative of the revocation in writing for clarity and record-keeping purposes.

Are there any special considerations when completing Form 2848?

Yes, there are several important considerations when completing Form 2848. Taxpayers should be precise about the tax forms, years, and types of tax matters they are authorizing their representative to handle. Specifying these details limits the representative's authority to those specifically designated matters. If a taxpayer wishes to grant broad powers to the representative, they must clearly indicate this on the form. Additionally, ensuring that the form is signed and dated by both the taxpayer and the representative is crucial for validity. Careful attention to these details ensures that the Power of Attorney will be processed smoothly by the IRS and that the taxpayer’s interests are adequately protected.

Navigating tax matters can sometimes feel like trekking through a labyrinth. One of the tools designed to help taxpayers through this complex journey is IRS Form 2848, the Power of Attorney (POA). However, while it’s meant to grant someone else the authority to speak or act on your behalf with the IRS, filling out this form incorrectly can lead to complications. Here are four common mistakes people make when completing IRS Form 2848.

Not Providing Complete Information

Accuracy and completeness are paramount when filling out IRS Form 2848. A common pitfall is leaving certain fields blank or providing incomplete information about the taxpayer or the representative. The IRS requires full names, addresses, and taxpayer identification numbers—such as SSNs (Social Security Numbers) or EINs (Employer Identification Numbers)—for processing. Omissions can result in the IRS rejecting the form, delaying crucial actions on your tax matters.

Listing Multiple Representatives Incorrectly

Sometimes, a taxpayer needs to appoint more than one representative. Form 2848 has the space to list multiple representatives, but the details need to be aligned with the IRS’s requirements. Each representative's name, address, and phone number must be listed correctly. Additionally, if you're authorizing these representatives to receive notices and communications from the IRS independently of each other, this needs to be specified by checking the box on line 5a. Failure to do so can lead to miscommunications and possibly delay or invalidate the POA.

Forgetting to Specify the Tax Matters

Another common mistake is not being specific about the tax form and year or years for which the POA is granted. The form requires you to identify the type of tax, tax form number, and the year(s) or period(s) involved. Vague or incorrect information in this section can significantly limit the representative’s ability to effectively handle your tax matters, as the IRS will only grant them authority for the details listed.

Not Signing or Dating the Form

It might sound simple, but an astonishing number of forms are submitted to the IRS without the taxpayer’s signature and/or date. This simple oversight renders the POA invalid. The IRS cannot process an unsigned or undated Form 2848, since the signature and date verify the taxpayer’s consent to grant the powers outlined in the form to the designated representative. Always double-check that these critical pieces of information are included before submission.

In ensuring that Form 2848 is filled out accurately and completely, taxpayers can avoid unnecessary delays and ensure their representatives are fully empowered to act on their behalf in dealings with the IRS. Attention to detail can make all the difference in smoothing the tax negotiation and resolution process.

When dealing with tax matters, it's common for individuals or businesses to use the IRS Power of Attorney (Form 2848) to authorize someone else to represent them before the IRS. However, Form 2848 often works in conjunction with other documents to ensure comprehensive handling of tax-related responsibilities. Below is a list of documents frequently used alongside Form 2848, each playing a crucial role in tax representation, preparation, and compliance.

Together, these forms enable a tax representative armed with a Power of Attorney to accurately assess, report, and address a wide array of tax-related issues and submissions. Understanding and utilizing these forms appropriately can significantly impact the management and resolution of tax affairs.

Healthcare Proxy or Medical Power of Attorney: This document allows individuals to appoint someone else to make healthcare decisions on their behalf if they are unable to do so themselves. It's similar to the IRS Power of Attorney (Form 2848) in that both appoint a representative to act on the individual's behalf, though the scope of authority differs substantially, with one focusing on medical decisions and the other on tax matters.

Durable Power of Attorney for Finances: This legal document grants a designated person the authority to manage the financial affairs of the individual. Like the IRS Power of Attorney, it allows someone else to act on your behalf, but it covers a broader range of financial decisions, not just tax issues.

General Power of Attorney: A general power of attorney provides broad powers to a proxy to act on the individual's behalf, including handling financial matters, making business transactions, and dealing with personal affairs. It is similar to the IRS Power of Attorney in its function of designating an agent but is more expansive in its application.

Limited Power of Attorney: This document grants limited authority to an agent for specific tasks or under certain conditions, which could include tax matters. Similar to Form 2848, a Limited Power of Attorney specifies what the agent is allowed to do, but it's applied in a broader array of contexts, not limited to dealing with the IRS.

Springing Power of Attorney: A springing power of attorney becomes effective under circumstances outlined in the document, such as the incapacity of the principal. While its applicability can be broad, including financial decisions and healthcare directives, it shares the trait of conditional activation with the tax-specific IRS Power of Attorney.

Advance Healthcare Directive: Often combined with a healthcare proxy, this document outlines an individual's healthcare preferences in advance, including end-of-life care and interventions. Although focused on healthcare, not taxes, it's similar to the IRS Power of Attorney in enabling individuals to make critical decisions in advance, thereby guiding actions on their behalf when they're not able to do so.

Guardianship or Conservatorship Arrangements: These legal processes appoint someone to make decisions for another person, typically in cases of incapacity. While these are court-ordered and can cover a wide range of decision-making powers, from healthcare to finances, they share the concept of representation with the IRS Power of Attorney.

Business Power of Attorney: This document, also known as a Commercial Power of Attorney, allows businesses to appoint agents to carry out specific business-related tasks. While distinct in its focus on business actions, it is similar to the IRS Power of Attorney in that it allows for the delegation of decision-making authority and actions to another party.

Filling out the IRS Power of Attorney (Form 2848) accurately is crucial because it grants another person the authority to handle your tax matters. To ensure you complete the form correctly and avoid any potential problems, here are some essential do's and don'ts to keep in mind:

Following these guidelines will help ensure that the Power of Attorney process is smooth and effective, allowing your representative to act on your behalf without any unnecessary complications.

The IRS Power of Attorney (POA) Form 2848 is a vital document that allows individuals to grant others the authority to represent them before the U.S. Internal Revenue Service (IRS). However, several misconceptions exist regarding its use, purpose, and limitations. Understanding these misconceptions is crucial for effectively managing and executing one's tax matters. Below are six common misconceptions about the IRS Power of Attorney (Form 2848) and explanations that aim to clarify these misunderstandings.

Clarifying these misconceptions about the IRS Power of Attorney (Form 2848) is important for taxpayers and their representatives to navigate the complexities of tax representation effectively. Proper understanding and application of this authority ensure that tax matters are handled accurately and efficiently, promoting compliance and minimizing errors.

The Internal Revenue Service (IRS) Form 2848, Power of Attorney and Declaration of Representative, is a crucial document that allows you to grant authority to an individual, known as your representative, to receive your confidential tax information and to deal with the IRS on your behalf. Understanding the correct way to fill out and use this form is vital. Here are seven key takeaways:

Correctly completing and using the IRS Form 2848 ensures that your representative has the authority needed to assist you with your tax matters efficiently and legally. Always keep a copy of the form for your records and stay informed about any changes in your representation or tax situation that might necessitate an adjustment to your power of attorney.

Bill of Lading Form - This document is an Ocean Bill of Lading, serving as a legal agreement for the shipment of goods by sea, detailing the exporter's information, the consignee, and the transit specifics.

Toyota Payoff - Details the process for Toyota vehicle owners or lessees to receive their certificate of title after financial settlement.

Par Q Form - Participants are asked about any current medications, allergies, and recent hospitalizations.