Free IRS Schedule A 990 or 990-EZ PDF Template

Free IRS Schedule A 990 or 990-EZ PDF Template

Navigating the intricacies of nonprofit tax requirements demands a clear understanding, especially when dealing with the IRS Schedule A (Form 990 or 990-EZ). This form stands as a vital component for most tax-exempt organizations, helping them showcase their public charity status and validate their compliance with federal tax obligations. Designed to be attached to the broader Form 990 or 990-EZ, Schedule A requires detailed information about the organization's revenues, activities, and public support over the tax year. It scrutinizes the organization's adherence to public charity standards by examining its sources of income, thereby distinguishing it from a private foundation. Filling out this form accurately is crucial, as it not only affects an organization's tax-exempt status but also its public image and eligibility for future funding. Thus, understanding its requirements, the nuances of its sections, and how it fits into the larger tax reporting landscape is essential for any nonprofit seeking to maintain its standing and ensure compliance.

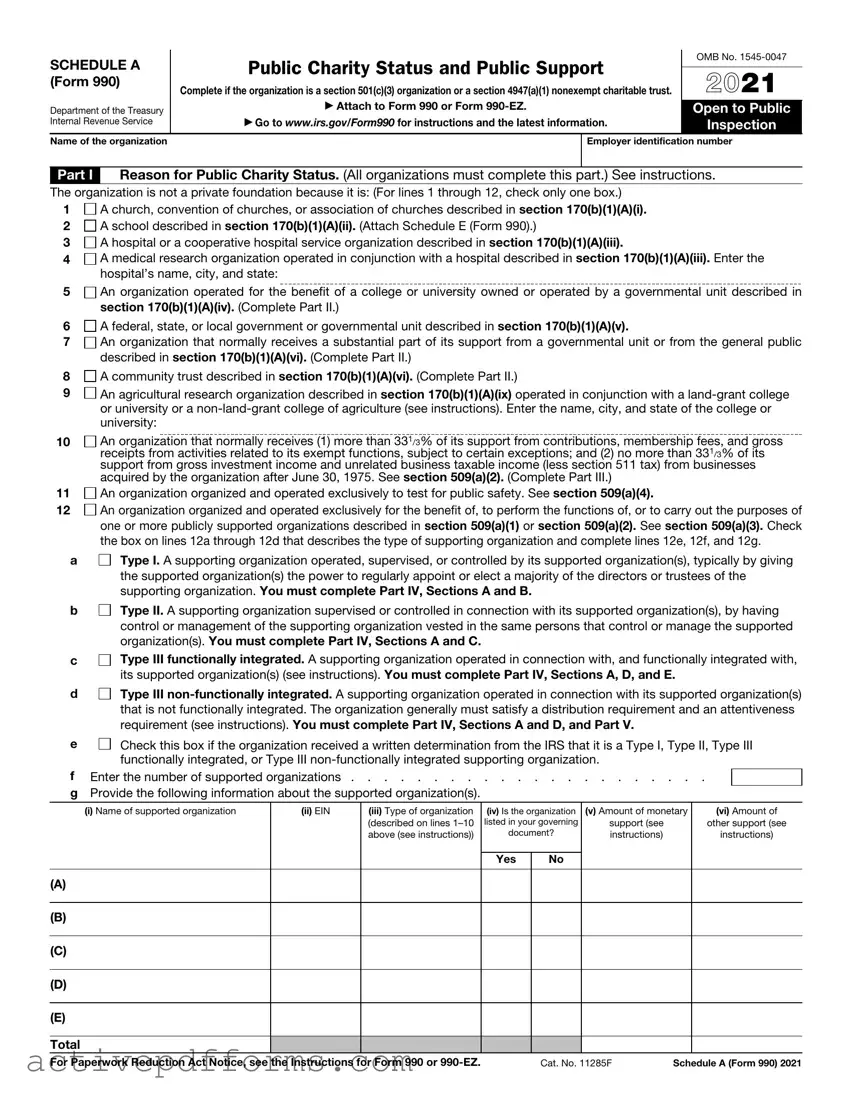

SCHEDULE A |

Public Charity Status and Public Support |

OMB No. |

|

|

|||

2021 |

|||

(Form 990) |

Complete if the organization is a section 501(c)(3) organization or a section 4947(a)(1) nonexempt charitable trust. |

||

|

|||

Department of the Treasury |

▶ Attach to Form 990 or Form |

Open to Public |

|

Internal Revenue Service |

▶ Go to www.irs.gov/Form990 for instructions and the latest information. |

Inspection |

|

Name of the organization |

Employer identification number |

||

Part I Reason for Public Charity Status. (All organizations must complete this part.) See instructions.

The organization is not a private foundation because it is: (For lines 1 through 12, check only one box.)

1 A church, convention of churches, or association of churches described in section 170(b)(1)(A)(i).

A church, convention of churches, or association of churches described in section 170(b)(1)(A)(i).

2 A school described in section 170(b)(1)(A)(ii). (Attach Schedule E (Form 990).)

A school described in section 170(b)(1)(A)(ii). (Attach Schedule E (Form 990).)

3 A hospital or a cooperative hospital service organization described in section 170(b)(1)(A)(iii).

A hospital or a cooperative hospital service organization described in section 170(b)(1)(A)(iii).

4 A medical research organization operated in conjunction with a hospital described in section 170(b)(1)(A)(iii). Enter the hospital’s name, city, and state:

A medical research organization operated in conjunction with a hospital described in section 170(b)(1)(A)(iii). Enter the hospital’s name, city, and state:

5 An organization operated for the benefit of a college or university owned or operated by a governmental unit described in section 170(b)(1)(A)(iv). (Complete Part II.)

An organization operated for the benefit of a college or university owned or operated by a governmental unit described in section 170(b)(1)(A)(iv). (Complete Part II.)

6 A federal, state, or local government or governmental unit described in section 170(b)(1)(A)(v).

A federal, state, or local government or governmental unit described in section 170(b)(1)(A)(v).

7 An organization that normally receives a substantial part of its support from a governmental unit or from the general public described in section 170(b)(1)(A)(vi). (Complete Part II.)

An organization that normally receives a substantial part of its support from a governmental unit or from the general public described in section 170(b)(1)(A)(vi). (Complete Part II.)

8 A community trust described in section 170(b)(1)(A)(vi). (Complete Part II.)

A community trust described in section 170(b)(1)(A)(vi). (Complete Part II.)

9 An agricultural research organization described in section 170(b)(1)(A)(ix) operated in conjunction with a

An agricultural research organization described in section 170(b)(1)(A)(ix) operated in conjunction with a

10

11

12

An organization that normally receives (1) more than 331/3% of its support from contributions, membership fees, and gross receipts from activities related to its exempt functions, subject to certain exceptions; and (2) no more than 331/3% of its support from gross investment income and unrelated business taxable income (less section 511 tax) from businesses acquired by the organization after June 30, 1975. See section 509(a)(2). (Complete Part III.)

An organization organized and operated exclusively to test for public safety. See section 509(a)(4).

An organization organized and operated exclusively to test for public safety. See section 509(a)(4).

An organization organized and operated exclusively for the benefit of, to perform the functions of, or to carry out the purposes of one or more publicly supported organizations described in section 509(a)(1) or section 509(a)(2). See section 509(a)(3). Check the box on lines 12a through 12d that describes the type of supporting organization and complete lines 12e, 12f, and 12g.

An organization organized and operated exclusively for the benefit of, to perform the functions of, or to carry out the purposes of one or more publicly supported organizations described in section 509(a)(1) or section 509(a)(2). See section 509(a)(3). Check the box on lines 12a through 12d that describes the type of supporting organization and complete lines 12e, 12f, and 12g.

a

Type I. A supporting organization operated, supervised, or controlled by its supported organization(s), typically by giving the supported organization(s) the power to regularly appoint or elect a majority of the directors or trustees of the supporting organization. You must complete Part IV, Sections A and B.

b

c

d

Type II. A supporting organization supervised or controlled in connection with its supported organization(s), by having control or management of the supporting organization vested in the same persons that control or manage the supported organization(s). You must complete Part IV, Sections A and C.

Type III functionally integrated. A supporting organization operated in connection with, and functionally integrated with, its supported organization(s) (see instructions). You must complete Part IV, Sections A, D, and E.

Type III

e Check this box if the organization received a written determination from the IRS that it is a Type I, Type II, Type III functionally integrated, or Type III

Check this box if the organization received a written determination from the IRS that it is a Type I, Type II, Type III functionally integrated, or Type III

f Enter the number of supported organizations . . . . . . . . . . . . . . . . . . . . . .

gProvide the following information about the supported organization(s).

(i) Name of supported organization |

(ii) EIN |

(iii) Type of organization |

(iv) Is the organization |

(v) Amount of monetary |

(vi) Amount of |

|

|

|

(described on lines |

listed in your governing |

support (see |

other support (see |

|

|

|

above (see instructions)) |

document? |

instructions) |

instructions) |

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

|

(A)

(B)

(C)

(D)

(E)

Total

For Paperwork Reduction Act Notice, see the Instructions for Form 990 or |

Cat. No. 11285F |

Schedule A (Form 990) 2021 |

Schedule A (Form 990) 2021 |

Page 2 |

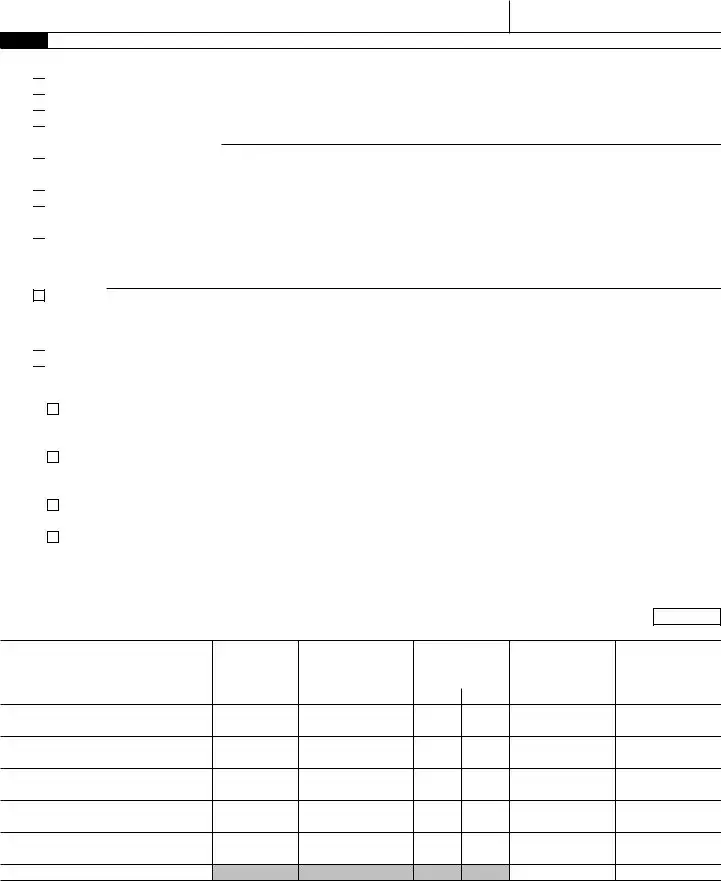

Part II Support Schedule for Organizations Described in Sections 170(b)(1)(A)(iv) and 170(b)(1)(A)(vi) (Complete only if you checked the box on line 5, 7, or 8 of Part I or if the organization failed to qualify under Part III. If the organization fails to qualify under the tests listed below, please complete Part III.)

Section A. Public Support

Calendar year (or fiscal year beginning in) ▶

1Gifts, grants, contributions, and membership fees received. (Do not include any “unusual grants.”) . . .

2Tax revenues levied for the organization’s benefit and either paid to

or expended on its behalf . . . .

3The value of services or facilities furnished by a governmental unit to the organization without charge . . . .

4Total. Add lines 1 through 3 . . . .

5The portion of total contributions by each person (other than a governmental unit or publicly supported organization) included on line 1 that exceeds 2% of the amount shown on line 11, column (f) . . . .

6Public support. Subtract line 5 from line 4

Section B. Total Support

(a)2017

(b)2018

(c)2019

(d)2020

(e)2021

(f)Total

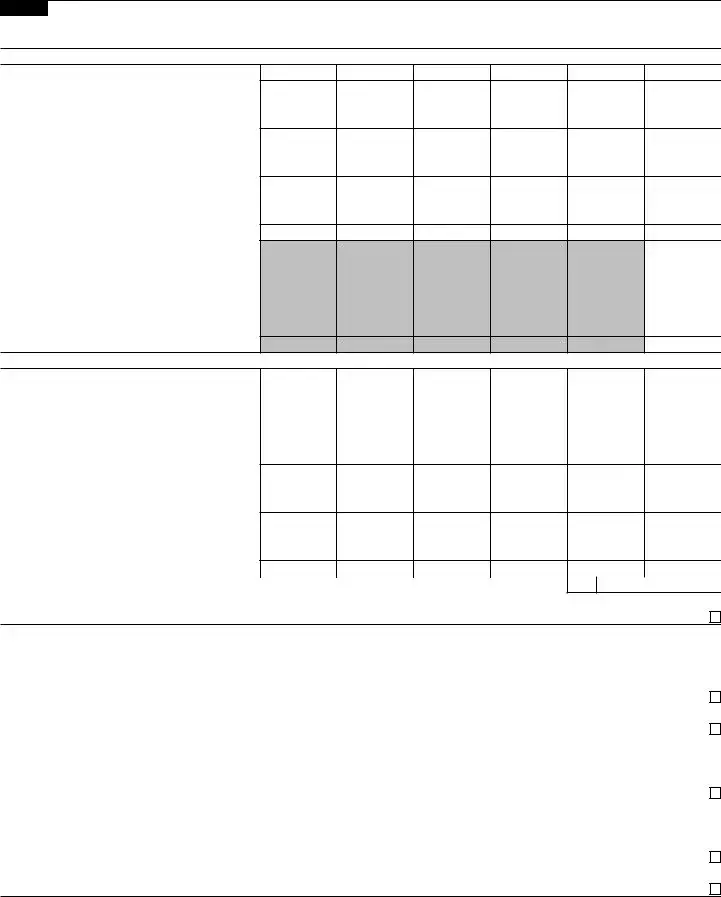

Calendar year (or fiscal year beginning in) ▶ |

(a) 2017 |

(b) 2018 |

(c) 2019 |

(d) 2020 |

(e) 2021 |

(f) Total |

|

7 |

Amounts from line 4 |

|

|

|

|

|

|

8 |

Gross income from interest, dividends, |

|

|

|

|

|

|

|

payments received on securities loans, |

|

|

|

|

|

|

|

rents, royalties, and income from |

|

|

|

|

|

|

|

similar sources |

|

|

|

|

|

|

9Net income from unrelated business activities, whether or not the business is regularly carried on . . . . . .

10Other income. Do not include gain or loss from the sale of capital assets (Explain in Part VI.) . . . . . . .

11 |

Total support. Add lines 7 through 10 |

|

|

|

|

12 |

Gross receipts from related activities, etc. |

|

(see instructions) |

12 |

|

13First 5 years. If the Form 990 is for the organization’s first, second, third, fourth, or fifth tax year as a section 501(c)(3) organization, check this box and stop here . . . . . . . . . . . . . . . . . . . . . . . . . ▶

Section C. Computation of Public Support Percentage

14 |

Public support percentage for 2021 (line 6, column (f), divided by line 11, column (f)) . . . . |

14 |

|

% |

15 |

Public support percentage from 2020 Schedule A, Part II, line 14 |

15 |

|

% |

16a |

331/3% support |

1/3% or more, check this |

||

|

box and stop here. The organization qualifies as a publicly supported organization |

▶ |

||

b331/3% support

17a

b

organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

18Private foundation. If the organization did not check a box on line 13, 16a, 16b, 17a, or 17b, check this box and see

instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021 |

Page 3 |

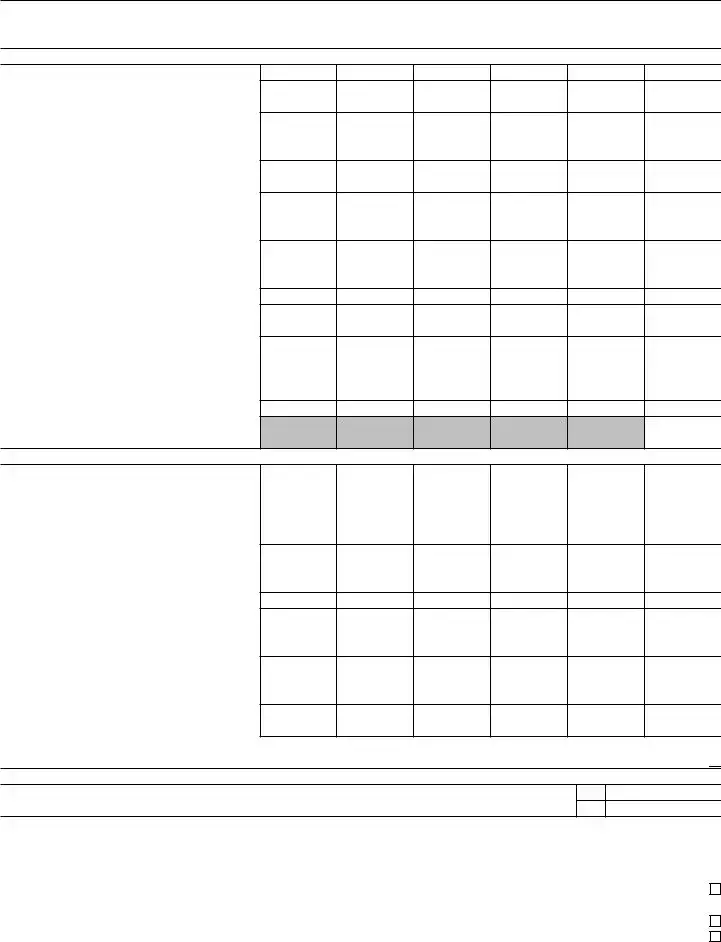

Part III Support Schedule for Organizations Described in Section 509(a)(2)

(Complete only if you checked the box on line 10 of Part I or if the organization failed to qualify under Part II. If the organization fails to qualify under the tests listed below, please complete Part II.)

Section A. Public Support

Calendar year (or fiscal year beginning in) ▶

1Gifts, grants, contributions, and membership fees received. (Do not include any “unusual grants.”)

2Gross receipts from admissions, merchandise sold or services performed, or facilities furnished in any activity that is related to the organization’s

3Gross receipts from activities that are not an unrelated trade or business under section 513

4Tax revenues levied for the

organization’s benefit and either paid to or expended on its behalf . . . .

5The value of services or facilities furnished by a governmental unit to the organization without charge . . . .

6Total. Add lines 1 through 5 . . . .

7a Amounts included on lines 1, 2, and 3

received from disqualified persons .

bAmounts included on lines 2 and 3 received from other than disqualified persons that exceed the greater of $5,000 or 1% of the amount on line 13 for the year

c Add lines 7a and 7b . . . . . .

8Public support. (Subtract line 7c from line 6.) . . . . . . . . . . .

Section B. Total Support

(a)2017

(b)2018

(c)2019

(d)2020

(e)2021

(f)Total

Calendar year (or fiscal year beginning in) ▶ |

(a) 2017 |

(b) 2018 |

(c) 2019 |

(d) 2020 |

(e) 2021 |

(f) Total |

|

9 |

Amounts from line 6 |

|

|

|

|

|

|

10a |

Gross income from interest, dividends, |

|

|

|

|

|

|

|

payments received on securities loans, rents, |

|

|

|

|

|

|

|

royalties, and income from similar sources . |

|

|

|

|

|

|

bUnrelated business taxable income (less section 511 taxes) from businesses acquired after June 30, 1975 . . . .

c Add lines 10a and 10b . . . . .

11Net income from unrelated business activities not included on line 10b, whether or not the business is regularly carried on

12Other income. Do not include gain or loss from the sale of capital assets (Explain in Part VI.) . . . . . . .

13Total support. (Add lines 9, 10c, 11, and 12.) . . . . . . . . . .

14First 5 years. If the Form 990 is for the organization’s first, second, third, fourth, or fifth tax year as a section 501(c)(3) organization, check this box and stop here . . . . . . . . . . . . . . . . . . . . . . . . . ▶

Section C. Computation of Public Support Percentage

15 |

Public support percentage for 2021 (line 8, column (f), divided by line 13, column (f)) |

16 |

Public support percentage from 2020 Schedule A, Part III, line 15 |

Section D. Computation of Investment Income Percentage

15

16

%

%

17 |

Investment income percentage for 2021 (line 10c, column (f), divided by line 13, column (f)) . . . |

17 |

|

% |

18 |

Investment income percentage from 2020 Schedule A, Part III, line 17 |

18 |

|

% |

19a |

331/3% support |

|||

|

17 is not more than 331/3%, check this box and stop here. The organization qualifies as a publicly supported organization . |

▶ |

||

b331/3% support

line 18 is not more than 331/3%, check this box and stop here. The organization qualifies as a publicly supported organization |

▶ |

20 Private foundation. If the organization did not check a box on line 14, 19a, or 19b, check this box and see instructions |

▶ |

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021Page 4

Part IV Supporting Organizations

(Complete only if you checked a box in line 12 on Part I. If you checked box 12a, Part I, complete Sections A and B. If you checked box 12b, Part I, complete Sections A and C. If you checked box 12c, Part I, complete Sections A, D, and E. If you checked box 12d, Part I, complete Sections A and D, and complete Part V.)

Section A. All Supporting Organizations

1Are all of the organization’s supported organizations listed by name in the organization’s governing documents? If “No,” describe in Part VI how the supported organizations are designated. If designated by class or purpose, describe the designation. If historic and continuing relationship, explain.

2Did the organization have any supported organization that does not have an IRS determination of status under section 509(a)(1) or (2)? If “Yes,” explain in Part VI how the organization determined that the supported organization was described in section 509(a)(1) or (2).

3a Did the organization have a supported organization described in section 501(c)(4), (5), or (6)? If “Yes,” answer lines 3b and 3c below.

bDid the organization confirm that each supported organization qualified under section 501(c)(4), (5), or (6) and satisfied the public support tests under section 509(a)(2)? If “Yes,” describe in Part VI when and how the organization made the determination.

cDid the organization ensure that all support to such organizations was used exclusively for section 170(c)(2)(B) purposes? If “Yes,” explain in Part VI what controls the organization put in place to ensure such use.

4a Was any supported organization not organized in the United States (“foreign supported organization”)? If “Yes,” and if you checked box 12a or 12b in Part I, answer lines 4b and 4c below.

bDid the organization have ultimate control and discretion in deciding whether to make grants to the foreign supported organization? If “Yes,” describe in Part VI how the organization had such control and discretion despite being controlled or supervised by or in connection with its supported organizations.

cDid the organization support any foreign supported organization that does not have an IRS determination under sections 501(c)(3) and 509(a)(1) or (2)? If “Yes,” explain in Part VI what controls the organization used to ensure that all support to the foreign supported organization was used exclusively for section 170(c)(2)(B) purposes.

5a Did the organization add, substitute, or remove any supported organizations during the tax year? If “Yes,” answer lines 5b and 5c below (if applicable). Also, provide detail in Part VI, including (i) the names and EIN numbers of the supported organizations added, substituted, or removed; (ii) the reasons for each such action;

(iii)the authority under the organization’s organizing document authorizing such action; and (iv) how the action was accomplished (such as by amendment to the organizing document).

bType I or Type II only. Was any added or substituted supported organization part of a class already designated in the organization’s organizing document?

cSubstitutions only. Was the substitution the result of an event beyond the organization’s control?

6Did the organization provide support (whether in the form of grants or the provision of services or facilities) to anyone other than (i) its supported organizations, (ii) individuals that are part of the charitable class benefited by one or more of its supported organizations, or (iii) other supporting organizations that also support or benefit one or more of the filing organization’s supported organizations? If “Yes,” provide detail in Part VI.

7Did the organization provide a grant, loan, compensation, or other similar payment to a substantial contributor (as defined in section 4958(c)(3)(C)), a family member of a substantial contributor, or a 35% controlled entity with regard to a substantial contributor? If “Yes,” complete Part I of Schedule L (Form 990).

8Did the organization make a loan to a disqualified person (as defined in section 4958) not described on line 7? If “Yes,” complete Part I of Schedule L (Form 990).

9a Was the organization controlled directly or indirectly at any time during the tax year by one or more disqualified persons, as defined in section 4946 (other than foundation managers and organizations described in section 509(a)(1) or (2))? If “Yes,” provide detail in Part VI.

bDid one or more disqualified persons (as defined on line 9a) hold a controlling interest in any entity in which the supporting organization had an interest? If “Yes,” provide detail in Part VI.

cDid a disqualified person (as defined on line 9a) have an ownership interest in, or derive any personal benefit from, assets in which the supporting organization also had an interest? If “Yes,” provide detail in Part VI.

10a Was the organization subject to the excess business holdings rules of section 4943 because of section 4943(f) (regarding certain Type II supporting organizations, and all Type III

bDid the organization have any excess business holdings in the tax year? (Use Schedule C, Form 4720, to determine whether the organization had excess business holdings.)

Yes No

1 |

2 |

3a

3b

3c

4a

4b

4c

5a

5b

5c

6

7

8

9a

9b

9c

10a

10b

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021 |

Page 5 |

|

Part IV |

Supporting Organizations (continued) |

|

11Has the organization accepted a gift or contribution from any of the following persons?

aA person who directly or indirectly controls, either alone or together with persons described on lines 11b and 11c below, the governing body of a supported organization?

bA family member of a person described on line 11a above?

cA 35% controlled entity of a person described on line 11a or 11b above? If “Yes” to line 11a, 11b, or 11c, provide detail in Part VI.

Section B. Type I Supporting Organizations

Yes No

11a

11b

11c

1Did the governing body, members of the governing body, officers acting in their official capacity, or membership of one or more supported organizations have the power to regularly appoint or elect at least a majority of the organization’s officers, directors, or trustees at all times during the tax year? If “No,” describe in Part VI how the supported organization(s) effectively operated, supervised, or controlled the organization’s activities. If the organization had more than one supported organization, describe how the powers to appoint and/or remove officers, directors, or trustees were allocated among the supported organizations and what conditions or restrictions, if any, applied to such powers during the tax year.

2Did the organization operate for the benefit of any supported organization other than the supported organization(s) that operated, supervised, or controlled the supporting organization? If “Yes,” explain in Part VI how providing such benefit carried out the purposes of the supported organization(s) that operated, supervised, or controlled the supporting organization.

Section C. Type II Supporting Organizations

Yes No

1

2

1Were a majority of the organization’s directors or trustees during the tax year also a majority of the directors or trustees of each of the organization’s supported organization(s)? If “No,” describe in Part VI how control or management of the supporting organization was vested in the same persons that controlled or managed the supported organization(s).

Section D. All Type III Supporting Organizations

Yes No

1

1Did the organization provide to each of its supported organizations, by the last day of the fifth month of the organization’s tax year, (i) a written notice describing the type and amount of support provided during the prior tax year, (ii) a copy of the Form 990 that was most recently filed as of the date of notification, and (iii) copies of the organization’s governing documents in effect on the date of notification, to the extent not previously provided?

2Were any of the organization’s officers, directors, or trustees either (i) appointed or elected by the supported organization(s) or (ii) serving on the governing body of a supported organization? If “No,” explain in Part VI how the organization maintained a close and continuous working relationship with the supported organization(s).

3By reason of the relationship described on line 2, above, did the organization’s supported organizations have a significant voice in the organization’s investment policies and in directing the use of the organization’s income or assets at all times during the tax year? If “Yes,” describe in Part VI the role the organization’s supported organizations played in this regard.

Section E. Type III Functionally Integrated Supporting Organizations

Yes No

1

2

3

1Check the box next to the method that the organization used to satisfy the Integral Part Test during the year (see instructions).

a The organization satisfied the Activities Test. Complete line 2 below.

The organization satisfied the Activities Test. Complete line 2 below.

b The organization is the parent of each of its supported organizations. Complete line 3 below.

The organization is the parent of each of its supported organizations. Complete line 3 below.

c The organization supported a governmental entity. Describe in Part VI how you supported a governmental entity (see instructions).

The organization supported a governmental entity. Describe in Part VI how you supported a governmental entity (see instructions).

2 Activities Test. Answer lines 2a and 2b below. |

Yes No |

aDid substantially all of the organization’s activities during the tax year directly further the exempt purposes of the supported organization(s) to which the organization was responsive? If “Yes,” then in Part VI identify those supported organizations and explain how these activities directly furthered their exempt purposes, how the organization was responsive to those supported organizations, and how the organization determined

that these activities constituted substantially all of its activities.

bDid the activities described on line 2a, above, constitute activities that, but for the organization’s involvement, one or more of the organization’s supported organization(s) would have been engaged in? If “Yes,” explain in Part VI the reasons for the organization’s position that its supported organization(s) would

have engaged in these activities but for the organization’s involvement.

3Parent of Supported Organizations. Answer lines 3a and 3b below.

aDid the organization have the power to regularly appoint or elect a majority of the officers, directors, or

trustees of each of the supported organizations? If “Yes” or “No,” provide details in Part VI. |

3a |

|

b Did the organization exercise a substantial degree of direction over the policies, programs, and activities of each |

|

|

of its supported organizations? If “Yes,” describe in Part VI the role played by the organization in this regard. |

3b |

|

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021 |

Page 6 |

|

Part V |

Type III |

|

1 Check here if the organization satisfied the Integral Part Test as a qualifying trust on Nov. 20, 1970 (explain in Part VI). See instructions. All other Type III

Check here if the organization satisfied the Integral Part Test as a qualifying trust on Nov. 20, 1970 (explain in Part VI). See instructions. All other Type III

Section |

(A) Prior Year |

(B) Current Year |

||

(optional) |

||||

|

|

|

||

|

|

|

|

|

1 |

Net |

1 |

|

|

2 |

Recoveries of |

2 |

|

|

3 |

Other gross income (see instructions) |

3 |

|

|

4 |

Add lines 1 through 3. |

4 |

|

|

5 |

Depreciation and depletion |

5 |

|

|

6Portion of operating expenses paid or incurred for production or collection of gross income or for management, conservation, or maintenance of

|

property held for production of income (see instructions) |

6 |

|

|

7 |

Other expenses (see instructions) |

7 |

|

|

8 |

Adjusted Net Income (subtract lines 5, 6, and 7 from line 4) |

8 |

|

|

Section |

(A) Prior Year |

(B) Current Year |

||

(optional) |

||||

|

|

|

||

1Aggregate fair market value of all

a |

Average monthly value of securities |

1a |

b Average monthly cash balances |

1b |

|

c |

Fair market value of other |

1c |

d Total (add lines 1a, 1b, and 1c) |

1d |

|

eDiscount claimed for blockage or other factors (explain in detail in Part VI):

2 |

Acquisition indebtedness applicable to |

2 |

3 |

Subtract line 2 from line 1d. |

3 |

4Cash deemed held for exempt use. Enter 0.015 of line 3 (for greater amount,

|

see instructions). |

4 |

|

|

5 |

Net value of |

5 |

|

|

6 |

Multiply line 5 by 0.035. |

6 |

|

|

7 |

Recoveries of |

7 |

|

|

8 |

Minimum Asset Amount (add line 7 to line 6) |

8 |

|

|

Section |

|

|

Current Year |

|

|

|

|

|

|

1 |

Adjusted net income for prior year (from Section A, line 8, column A) |

1 |

|

|

2 |

Enter 0.85 of line 1. |

2 |

|

|

3 |

Minimum asset amount for prior year (from Section B, line 8, column A) |

3 |

|

|

4 |

Enter greater of line 2 or line 3. |

4 |

|

|

5 |

Income tax imposed in prior year |

5 |

|

|

6Distributable Amount. Subtract line 5 from line 4, unless subject to

emergency temporary reduction (see instructions). |

6 |

7 Check here if the current year is the organization’s first as a

Check here if the current year is the organization’s first as a

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021 |

|

|

|

|

Page 7 |

|||

Part V |

Type III |

|

||||||

Section |

|

|

|

|

Current Year |

|||

|

|

|

|

|

|

|||

1 |

Amounts paid to supported organizations to accomplish exempt purposes |

|

1 |

|

||||

2 |

Amounts paid to perform activity that directly furthers exempt purposes of supported |

|

|

|||||

|

organizations, in excess of income from activity |

|

|

2 |

|

|||

3 |

Administrative expenses paid to accomplish exempt purposes of supported organizations |

3 |

|

|||||

4 |

Amounts paid to acquire |

|

|

4 |

|

|||

5 |

Qualified |

5 |

|

|||||

6 |

Other distributions (describe in Part VI). See instructions. |

|

|

6 |

|

|||

7 |

Total annual distributions. Add lines 1 through 6. |

|

|

7 |

|

|||

8 |

Distributions to attentive supported organizations to which the organization is responsive |

|

|

|||||

|

(provide details in Part VI). See instructions. |

|

|

8 |

|

|||

9 |

Distributable amount for 2021 from Section C, line 6 |

|

|

9 |

|

|||

10 |

Line 8 amount divided by line 9 amount |

|

|

10 |

|

|||

|

|

|

|

(i) |

(ii) |

|

(iii) |

|

Section |

(see instructions) |

Underdistributions |

Distributable |

|||||

Excess Distributions |

||||||||

|

|

|

|

|

|

Amount for 2021 |

||

1 |

Distributable amount for 2021 from Section C, line 6 |

|

|

|

|

|||

2 |

Underdistributions, if any, for years prior to 2021 |

|

|

|

|

|||

|

(reasonable cause |

|

|

|

|

|||

|

instructions. |

|

|

|

|

|

||

3 |

Excess distributions carryover, if any, to 2021 |

|

|

|

|

|||

a |

From 2016 |

|

|

|

|

|

||

b |

From 2017 |

|

|

|

|

|

||

c |

From 2018 |

|

|

|

|

|

||

d |

From 2019 |

|

|

|

|

|

||

e |

From 2020 |

|

|

|

|

|

||

f |

Total of lines 3a through 3e |

|

|

|

|

|

||

g |

Applied to underdistributions of prior years |

|

|

|

|

|||

h |

Applied to 2021 distributable amount |

|

|

|

|

|||

i |

Carryover from 2016 not applied (see instructions) |

|

|

|

|

|||

j |

Remainder. Subtract lines 3g, 3h, and 3i from line 3f. |

|

|

|

|

|||

4 |

Distributions for 2021 from |

|

|

|

|

|

||

|

Section D, line 7: |

$ |

|

|

|

|

||

a |

Applied to underdistributions of prior years |

|

|

|

|

|||

b |

Applied to 2021 distributable amount |

|

|

|

|

|||

c |

Remainder. Subtract lines 4a and 4b from line 4. |

|

|

|

|

|||

5 |

Remaining underdistributions for years prior to 2021, if |

|

|

|

|

|||

|

any. Subtract lines 3g and 4a from line 2. For result |

|

|

|

|

|||

|

greater than zero, explain in Part VI. See instructions. |

|

|

|

|

|||

6 |

Remaining underdistributions for 2021. Subtract lines 3h |

|

|

|

|

|||

|

and 4b from line 1. For result greater than zero, explain in |

|

|

|

|

|||

|

Part VI. See instructions. |

|

|

|

|

|

||

7 |

Excess distributions carryover to 2022. Add lines 3j |

|

|

|

|

|||

|

and 4c. |

|

|

|

|

|

||

8 |

Breakdown of line 7: |

|

|

|

|

|

||

a |

Excess from 2017 . . . |

|

|

|

|

|

||

b |

Excess from 2018 . . . |

|

|

|

|

|

||

c |

Excess from 2019 . . . |

|

|

|

|

|

||

d |

Excess from 2020 . . . |

|

|

|

|

|

||

e |

Excess from 2021 . . . |

|

|

|

|

|

||

Schedule A (Form 990) 2021

Schedule A (Form 990) 2021 |

Page 8 |

|

Part VI |

Supplemental Information. Provide the explanations required by Part II, line 10; Part II, line 17a or 17b; Part |

|

|

III, line 12; Part IV, Section A, lines 1, 2, 3b, 3c, 4b, 4c, 5a, 6, 9a, 9b, 9c, 11a, 11b, and 11c; Part IV, Section |

|

|

B, lines 1 and 2; Part IV, Section C, line 1; Part IV, Section D, lines 2 and 3; Part IV, Section E, lines 1c, 2a, 2b, |

|

|

3a, and 3b; Part V, line 1; Part V, Section B, line 1e; Part V, Section D, lines 5, 6, and 8; and Part V, Section E, |

|

|

lines 2, 5, and 6. Also complete this part for any additional information. (See instructions.) |

|

|

|

|

Schedule A (Form 990) 2021

| Fact Name | Description |

|---|---|

| Purpose of Schedule A | Schedule A of form 990 or 990-EZ is primarily used by organizations to report information about their public charity status and public support. It ensures that they meet the public support test over a five-year period, crucial for maintaining their tax-exempt status. |

| Required Filers | Organizations that have filed for tax-exempt status under Section 501(c)(3) of the Internal Revenue Code are required to complete and attach Schedule A to their Form 990 or 990-EZ annually. |

| Public Inspection | Schedule A, like Form 990 or 990-EZ, is open to public inspection. This transparency allows the public to see how the organization is supported financially, ensuring it adheres to its mission and public charity status requirements. |

| Governing Laws | Under the Internal Revenue Code (IRC) Section 501(c)(3), along with the regulations and guidelines provided by the Internal Revenue Service (IRS), organizations must adhere to specific requirements to maintain their tax-exempt status, which includes the filing of Schedule A with their Form 990 or 990-EZ. |

Filing the IRS Schedule A (990 or 990-EZ) is an essential task for many non-profit organizations, ensuring their compliance with tax regulations and maintaining their tax-exempt status. This document, part of the broader 990 and 990-EZ forms, focuses specifically on public charity status and public support. Its accurate completion helps the IRS determine an organization's compliance with its mission and financial responsibilities. The steps outlined below aim to simplify the process, making it manageable for those tasked with this important duty.

Successfully completing and submitting Schedule A (990 or 990-EZ) is crucial for non-profit organizations seeking to maintain their tax-exempt status. While the process may seem daunting, careful attention to detail and adherence to IRS instructions can make it a manageable task. Should questions or uncertainties arise, consulting with a tax professional experienced in non-profit tax law is advisable. This ensures not only compliance but also peace of mind for those responsible for the organization's financial integrity.

What is IRS Schedule A (Form 990 or 990-EZ)?

Schedule A (Form 990 or 990-EZ) is a required tax document for organizations that claim tax-exempt status under Section 501(c)(3). This form helps the IRS assess the public support percentage of these organizations, ensuring they meet the public support criteria set forth for maintaining their tax-exempt status.

Who needs to file Schedule A (Form 990 or 990-EZ)?

All organizations that are exempt from federal income tax under Section 501(c)(3), including charities, educational institutions, and religious organizations, must file Schedule A along with their Form 990 or 990-EZ. This schedule provides details on the organization's revenue sources, which is critical for proving public support.

What information do I need to complete Schedule A?

To fill out Schedule A, organizations need detailed records of their income, including donations, grants, and other sources of revenue over the reporting period. It is also necessary to compile information on any gifts or contributions received, details on fundraising activities, and an understanding of how the organization meets the IRS's public support criteria.

How does the IRS determine if an organization meets the public support criteria?

The IRS uses Schedule A to evaluate an organization's support over a five-year period. To classify as publicly supported, an organization must demonstrate that a substantial portion of its financial support comes from the general public, government agencies, or other public sources rather than a limited number of donors. This ensures the organization is not privately funded or controlled.

Can I file Schedule A electronically?

Yes, organizations can file Schedule A (Form 990 or 990-EZ) electronically through an IRS-authorized e-file provider. Electronic filing is not only convenient but also faster and can help reduce the risk of errors by providing immediate feedback.

What happens if my organization fails to file Schedule A?

Failing to file Schedule A along with Form 990 or 990-EZ can lead to penalties and may jeopardize an organization's tax-exempt status. It's crucial to file all required forms accurately and on time to maintain compliance with IRS regulations.

Where can I get help with completing Schedule A?

There are numerous resources available for organizations needing assistance with Schedule A. The IRS website offers comprehensive guides and the full text of the form instructions. Additionally, tax professionals and nonprofit organizations specializing in tax issues can provide valuable advice and support. It's advisable to seek help well before the deadline to ensure accurate and timely filing.

When is Schedule A due?

Schedule A is due at the same time as Form 990 or 990-EZ. This deadline typically falls on the 15th day of the 5th month after the organization's fiscal year ends. Organizations can request a 6-month extension to file by submitting Form 8868 before the original due date.

Filling out the IRS Schedule A for Form 990 or 990-EZ is a detailed process that often leads to common mistakes. Both forms are essential for tax-exempt organizations, ensuring they meet public charity status requirements. Being aware of these errors can help organizations complete the form more accurately.

Not verifying the organization's public charity status every year. Tax laws and organizational financials can change, potentially affecting status.

Omitting necessary schedules or documentation. Each part of Schedule A asks for different information, and failing to provide all required details can lead to further scrutiny from the IRS.

Incorrectly calculating public support percentage. This is crucial for demonstrating compliance with public charity status requirements.

Failing to report all sources of revenue, including donations, grants, and other forms of financial support. This can misrepresent an organization's financial health and public support level.

Misunderstanding the difference between direct and indirect public support, which can affect the accuracy of the support calculation.

Not listing all substantial contributors. Organizations must report donors who contribute a significant portion of the total donations.

Overlooking the need to update information about officers, directors, trustees, and key employees. This information is critical for transparency and compliance.

Forgetting to sign and date the form. An unsigned form is considered incomplete and can lead to processing delays.

Avoiding these mistakes not only helps in staying compliant with IRS requirements but also in maintaining the organization's reputation and ability to serve the community. For those who are unsure about any part of the process, seeking advice from a tax professional is always a wise decision.

When preparing the IRS Schedule A (990 or 990-EZ), organizations are often required to provide additional documents to support their tax-exempt status and financial activities throughout the year. These documents play a crucial role in ensuring compliance with federal regulations and support the information provided in the main tax forms. Each document addresses different components of an organization's operations, from financial transactions to governance practices.

Together, these documents provide a comprehensive overview of a nonprofit organization's financial health, activities, and governance. They are essential for maintaining transparency, complying with tax laws, and ensuring the organization's ongoing eligibility for tax-exempt status. By carefully preparing and submitting these forms, organizations can demonstrate their commitment to responsible financial management and regulatory compliance.

Form 1023: This document, utilized by organizations seeking tax-exempt status under IRS Section 501(c)(3), shares a resemblance to the IRS Schedule A 990 or 990-EZ. Both require detailed information about the organization's activities, financials, and governance practices to ensure compliance with federal tax regulations.

Form 990-N (e-Postcard): Aimed at small tax-exempt organizations, this form is a simplified annual notification. It parallels the Schedule A 990 or 990-EZ in its purpose to report to the IRS, albeit with significantly less detail required, making it suitable for organizations with annual receipts of $50,000 or less.

Form 990-PF: Used by private foundations, irrespective of their financial status, this form resembles Schedule A 990 or 990-EZ through its comprehensive reporting requirements. Both documents necessitate detailed financial data, activities, and operational insights to maintain tax-exempt status and public accountability.

Form 8868: Serving as an application for extension of time to file an exempt organization return, this document shares the premise of compliance with filing requirements, akin to Schedule A 990 or 990-EZ. It’s utilized when an organization needs additional time to compile the thorough information required for their annual reporting.

State Charity Registration Forms: Many states require annual or periodic filings similar to the IRS forms for tax-exempt organizations, including the Schedule A 990 or 990-EZ. These state-specific documents often request comparable information about activities, finances, and governance to ensure compliance with state laws governing charitable organizations.

Form 1065: While primarily used by partnerships for tax reporting, this form overlaps with the Schedule A 990 or 990-EZ in its detailed financial reporting requirements. Nonprofit organizations that partake in partnerships may find similarities in the financial detail and accountability these forms demand.

Form 1120: Corporations use this form to report their income, gains, losses, deductions, and credits to the IRS. The link to Schedule A 990 or 990-EZ lies in their shared objective of detailed financial reporting. Although aimed at for-profit entities, the depth of financial disclosure required presents parallels to the nonprofit filings.

Filling out the IRS Schedule A (Form 990 or 990-EZ) can be a daunting process for many non-profit organizations. This form is designed to provide the IRS with information about the public charity status and public support. To ensure that your organization accurately completes this form and avoids common pitfalls, here are seven do's and don'ts to follow:

Filing IRS Schedule A (Form 990 or 990-EZ) for public charities and certain other non-profits can sometimes be confusing. It's easy to fall into misconceptions regarding how it should be filed, who should file it, and what information it should contain. Here, we clarify some common misconceptions about these forms.

Filling out the IRS Schedule A 990 or 990-EZ form is a key part of complying with IRS requirements for tax-exempt organizations. While the process may seem complicated, understanding a few critical components can streamline the task and ensure that organizations maintain their tax-exempt status without running into preventable issues. Below are four essential takeaways for handling this important document:

By understanding these key points, organizations can better navigate the complexities of the IRS Schedule A 990 or 990-EZ form, ensuring they remain compliant and in good standing with the IRS. Remember, when in doubt, consulting with a tax professional familiar with nonprofit tax requirements can provide valuable guidance and peace of mind.

Fillable W-9 Form 2023 - Designed to keep real estate agents financially informed, this form includes specifics on asset acquisitions and their associated costs.

Handicap Placard Replacement Pa - Emphasizes that each placard type, whether permanent, temporary, or veteran-specific, requires certain sections of the form to be completed.