Free IRS Schedule B 941 PDF Template

Free IRS Schedule B 941 PDF Template

Navigating the intricacies of tax documentation is a task that many businesses find challenging, yet it remains a crucial aspect of fiscal responsibility. Among the myriad forms that need to be mastered, the IRS Schedule B (Form 941) stands out as particularly significant for employers who are required to report taxes withheld from employees' wages, as well as their own portion of social security and Medicare taxes. This form plays a pivotal role in ensuring that businesses remain compliant with the Internal Revenue Service's regulations, acting as a detailed record of tax liabilities throughout the quarter. Its primary function is to provide a snapshot of when these liabilities were accrued, thus offering a straightforward way to monitor and meet tax obligations in a timely manner. The importance of accurately completing IRS Schedule B cannot be overstated, as it affects not only a business's compliance status but also its financial health.

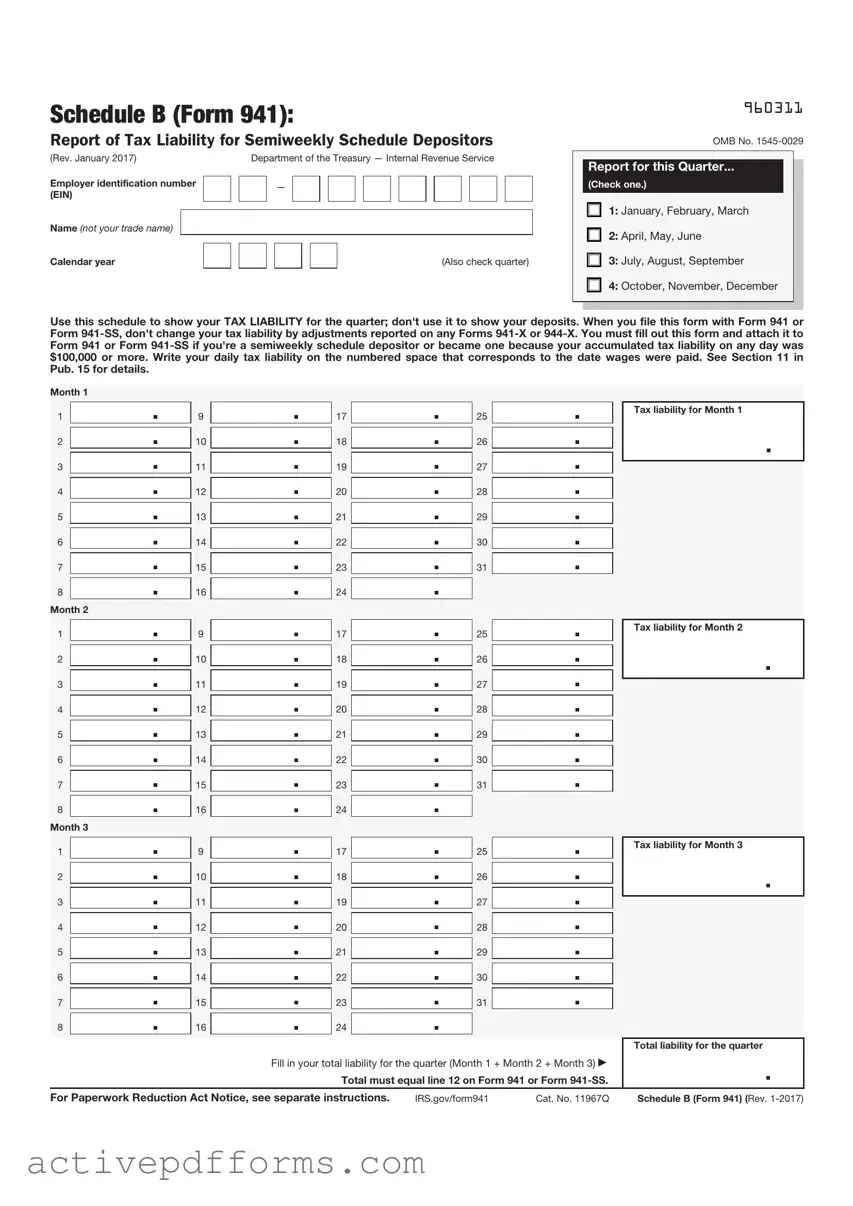

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. January 2017) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don't use it to show your deposits. When you file this form with Form 941 or Form

Month 1

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 2

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 3

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

Tax liability for Month 1

.

Tax liability for Month 2

.

1 |

|

. |

9 |

|

. |

17 |

|

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

18 |

|

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

19 |

|

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

20 |

|

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

21 |

|

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

22 |

|

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

23 |

|

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

24 |

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3) |

. |

|||||||||

|

|

|

|

|

|

Total must equal line 12 on Form 941 or Form |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

IRS.gov/form941 |

Cat. No. 11967Q |

Schedule B (Form 941) (Rev. |

|||||||||||

| Fact Number | Fact Description |

|---|---|

| 1 | IRS Schedule B (Form 941) is primarily used by employers to report tax liability for social security, Medicare, and withheld income taxes on a semi-weekly schedule. |

| 2 | Employers are required to fill out Schedule B (Form 941) if they reported more than $50,000 in taxes during the lookback period or accumulated a tax liability of $100,000 or more on any given day during the current or prior tax year. |

| 3 | Schedule B does not determine the amount of tax owed; rather, it schedules when these liabilities are due to be paid during the quarter. |

| 4 | This form must be filed quarterly with the IRS, attached to Form 941, Employer's Quarterly Federal Tax Return. |

| 5 | Penalties for late or incorrect filings of Schedule B can result in fines and interest charges. Timeliness and accuracy are paramount in avoiding these penalties. |

| 6 | Schedule B is not typically filed by employers who deposit their taxes monthly, unless specifically directed to do so by the IRS. |

| 7 | Each line of Schedule B represents a pay period within the quarter. Employers must report their tax liabilities according to the specific dates wages were paid. |

| 8 | For states with specific employment tax requirements, employers must also comply with state-level filing requirements. However, Schedule B (Form 941) is a federal form, and state specifics may vary. |

| 9 | The form is available for download on the IRS website, and can be filed electronically or by mail alongside Form 941. |

Filling out IRS Schedule B for Form 941 is a crucial step in reporting your business's payroll tax liabilities accurately. This process requires attention to detail and an understanding of your payroll cycles. The aim is to ensure that your business complies with federal tax obligations in a timely and correct manner. By following the set steps, you can complete the Schedule B form confidently, contributing to the smooth operation of your business's financial responsibilities.

Once you have completed all steps and submitted your Schedule B alongside Form 941, your next actions depend on the regular operation of your payroll. It's important to continue monitoring your payroll amounts and tax liabilities for each subsequent quarter, preparing to fill out and submit a new Schedule B form as necessary. Staying organized and keeping accurate records throughout the year will simplify this process for each tax period.

What is the IRS Schedule B (Form 941), and who needs to file it?

The IRS Schedule B (Form 941) is a tax document required from employers who withhold income tax, social security tax, or Medicare tax from their employees' paychecks. Employers who make these withholdings must report them quarterly using Form 941, and Schedule B is a more detailed report showing the tax amounts they've withheld for each pay period within the quarter. It's mainly required for employers who are on a semi-weekly schedule for depositing these withholdings.

How do I know if I need to file Schedule B with my Form 941?

If you're an employer who deposits employment taxes on a semi-weekly schedule, you'll need to file Schedule B. Generally, this applies to employers who have accumulated $50,000 or more in employment taxes in the lookback period, which is the four-quarter period ending on June 30 of the prior year. However, if you're a monthly depositor or did not reach this threshold, you likely do not need to file Schedule B.

What information is required on Schedule B?

Schedule B asks for detailed information about the taxes an employer has withheld during each pay period within a quarter. This includes the date of each payroll, the total taxes withheld for that pay period, and the quarter's cumulative total. It's essential to be precise with the dates and amounts to ensure compliance with IRS requirements.

Can I file Schedule B electronically?

Yes, the IRS encourages employers to file Schedule B electronically for convenience and efficiency. Filing electronically also reduces the risk of errors and faster processing times. Employers can use various IRS-approved e-file providers to complete and submit their Schedule B and Form 941.

When is Schedule B due?

Schedule B is due at the same time as Form 941. Generally, this is the last day of the month that follows the end of the quarter. Specifically, the due dates are April 30 for the first quarter, July 31 for the second quarter, October 31 for the third quarter, and January 31 for the fourth quarter. If the due date falls on a weekend or holiday, it is extended to the next business day.

What happens if I file Schedule B late?

Filing Schedule B late can result in penalties and interest charges from the IRS. The penalty for late filing of Schedule B can vary, depending on how late the form is filed and the amount of taxes due. It's important to file on time to avoid these additional costs.

Do I need to attach payment when filing Schedule B?

Schedule B itself does not require a payment when filed. However, it accompanies Form 941, which does generally require a payment if taxes are owed. The payment should match the total tax liability reported for the quarter on Form 941 and Schedule B.

Can I correct a mistake on Schedule B after I've filed it?

If you discover an error on a filed Schedule B, you can correct it by filing a corrected Schedule B along with Form 941-X, Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund. This form is used to make corrections to previously filed Form 941 and Schedule B documents. It's important to correct mistakes as soon as they're discovered to avoid potential penalties.

Is there a penalty for over-reporting on Schedule B?

While the IRS primarily concerns itself with under-reporting of taxes, over-reporting can also cause issues. If you over-report, it might affect the amount of taxes you owe or result in a larger refund than you're entitled to. If the IRS discovers the over-reporting, especially if it seems intentional, it could lead to scrutiny or an audit. Corrections should be made using Form 941-X.

Where can I get help with my Schedule B?

There are several resources available for employers who need help with Schedule B. These include the official IRS website, which has guides and resources available free of charge. Additionally, tax professionals and IRS-approved electronic filing services can provide assistance and ensure that your Schedule B and Form 941 are filed correctly and on time.

When filling out the IRS Schedule B for Form 941, individuals often encounter certain common pitfalls. Being aware of these can save a lot of time and prevent unnecessary stress. Here is a comprehensive look at five mistakes frequently made during this process:

Not Matching the Total Taxes Reported to Form 941: Every entry in Schedule B must equal the total taxes reported in Form 941, line 12. A mismatch between these figures is a common error that can lead to audits or questions from the IRS.

Incorrectly Reporting the Tax Liability Period: Schedule B requires taxpayers to report their tax liability for each semi-weekly period, not the deposit dates. Misunderstanding this requirement can lead to inaccuracies in how and when liabilities are reported.

Omitting Information or Details: Sometimes, entries are incomplete or information is unintentionally left out. Every field that requires an entry should be filled in to avoid processing delays or the IRS seeking clarifications.

Mathematical Errors: Simple arithmetic mistakes can cause big problems with the IRS. Double-checking the math to ensure that all totals add up correctly is crucial in avoiding unnecessary corrections later.

Failing to Sign and Date the Form: An unsigned or undated form is considered incomplete by the IRS. Always ensure that the Schedule B is signed and dated before submission to demonstrate that the information provided is confirmed to the best of the signer's knowledge.

Attention to detail and a thorough review of the Schedule B Form 941 can significantly reduce the risk of these mistakes. Additionally, seeking guidance from a tax professional is advisable for individuals who are unsure about how to correctly complete this form.

When businesses tackle their payroll tax responsibilities, the IRS Schedule B (Form 941), "Report of Tax Liability for Semiweekly Schedule Depositors," often comes into play. This form allows employers who deposit payroll taxes on a semiweekly schedule to report their tax liabilities. However, it is rarely the only document needed during this process. Several other forms and documents are commonly required to ensure compliance with tax regulations and to streamline payroll reporting and payments.

Together with Schedule B (Form 941), these forms create a comprehensive framework for managing and reporting a business's payroll taxes. Accurately completing and timely submitting these documents is critical to maintaining compliance with tax laws and avoiding any potential penalties or fines. Understanding each form's role in the payroll process can help employers navigate their tax obligations more effectively.

Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return: Similar to Schedule B (Form 941), Form 940 is used by employers to report their annual Federal Unemployment Tax Act (FUTA) tax. Both forms require employers to calculate taxes based on employee wages and report annually or quarterly, respectively.

Form 944, Employer’s Annual Federal Tax Return: This form is for smaller employers to report Social Security, Medicare, and withheld income tax annually. It's similar to Schedule B (Form 941) in that it deals with reporting employer tax obligations, but it's for those with smaller tax liabilities.

Form W-2, Wage and Tax Statement: Employers use Form W-2 to report wages, tips, and other compensation paid to an employee. Like Schedule B (Form 941), this form is integral to reporting employee compensation and taxes withheld, albeit on an individual basis.

Form W-3, Transmittal of Wage and Tax Statements: This form accompanies Form W-2 submissions to the Social Security Administration. It summarizes employee earnings, Social Security, and Medicare taxes withheld, echoing Schedule B (Form 941)'s function of summarizing payroll tax liabilities.

Form 1099-MISC, Miscellaneous Income: Used to report payments made in the course of a business to a person who's not an employee, such as independent contractors. Relevant to employers, it complements Schedule B (Form 941) by covering non-employee compensation, highlighting another aspect of tax reporting.

Form 1099-NEC, Nonemployee Compensation: Starting in 2020, this form replaces Form 1099-MISC for reporting nonemployee compensation. While Schedule B (Form 941) focuses on employee taxes, Form 1099-NEC addresses payments to individuals not classified as employees, emphasizing the breadth of payroll tax reporting obligations.

Form 945, Annual Return of Withheld Federal Income Tax: Form 945 is used to report federal income tax withheld from nonpayroll payments, including gambling winnings, pensions, and IRAs. It parallels Schedule B (Form 941) in its focus on withholding taxes, though 945 is for nonpayroll withholdings.

Form W-4, Employee’s Withholding Certificate: Employees use Form W-4 to determine the amount of federal income tax to withhold from their paychecks. While not a reporting form like Schedule B (Form 941), it directly influences the calculation of taxes reported by employers, underscoring its pivotal role in payroll tax processes.

Filling out the IRS Schedule B for Form 941 correctly is crucial for employers who report payroll taxes. To ensure accuracy and compliance with IRS requirements, here are key dos and don'ts to keep in mind:

Do:

Don't:

When navigating the intricacies of the IRS Schedule B for Form 941, several misconceptions commonly arise. Understanding these can help ensure accurate payroll reporting and compliance. Below are four of the most prevalent misunderstandings:

By dispelling these misconceptions, employers can better navigate their responsibilities and avoid common pitfalls associated with IRS Schedule B for Form 941. This ensures more accurate reporting, timely deposits, and reduces the risk of penalties, contributing to a smoother operational process for both the employer and the IRS.

The IRS Schedule B (Form 941) is a critical document for businesses that report taxes withheld from employees' wages. Understanding how to accurately complete and use this form is vital for compliance with IRS regulations. Here are nine key takeaways to guide you through this process:

The IRS Schedule B (Form 941) is used by employers to report the tax liability for Medicare, Social Security, and withheld federal income tax. It's meant for businesses that pay wages subject to these taxes.

Employers need to file this form on a quarterly basis, even if there are no taxes to report for a particular period. This ensures compliance and avoids potential penalties.

Accuracy is crucial when filling out Schedule B to avoid underpayment or overpayment of taxes. Employers should carefully calculate the total taxes for each quarter.

The form requires employers to declare their total tax liability for each month in the quarter. This breaks down the quarterly liability into more manageable monthly figures.

Employers must use their employment tax liability, not the deposits made, when completing Schedule B. This distinction is important for accurately reporting liabilities vs. actual payments.

If an employer's tax liability reaches $100,000 or more on any day during a monthly or semi-weekly deposit period, they must switch to the next-day deposit schedule. This shift impacts how tax liabilities are reported on the Schedule B.

Accuracy in reporting and timeliness of filing Schedule B can affect an employer's ability to claim tax credits and deductions. Proper completion of the form can lead to significant benefits.

It's important for employers to retain copies of filed Schedule B forms and all relevant employment tax records for at least four years after the filing date or the date the tax was paid, whichever is later.

Employers unsure about how to fill out or file Schedule B should seek advice from a tax professional or the IRS. Guidance is available to help navigate the complexities of tax reporting.

By adhering to these guidelines, employers can ensure they meet their tax reporting responsibilities effectively and efficiently. Proper management of the IRS Schedule B (Form 941) is essential for maintaining compliance and minimizing the risk of encountering issues with the IRS.

I 130 Approval Time - Oftentimes accompanied by additional forms and evidence, such as proof of the petitioner's U.S. citizenship or permanent residence.

Imm 1344 Printable - Part 1 of the form focuses on the eligibility and personal details of the sponsor.

Filing a Motion in Family Court - A resourceful packet for initiating family court motions related to modifications, enforcement, or other related actions post-judgment.