Free IRS Schedule E 1040 PDF Template

Free IRS Schedule E 1040 PDF Template

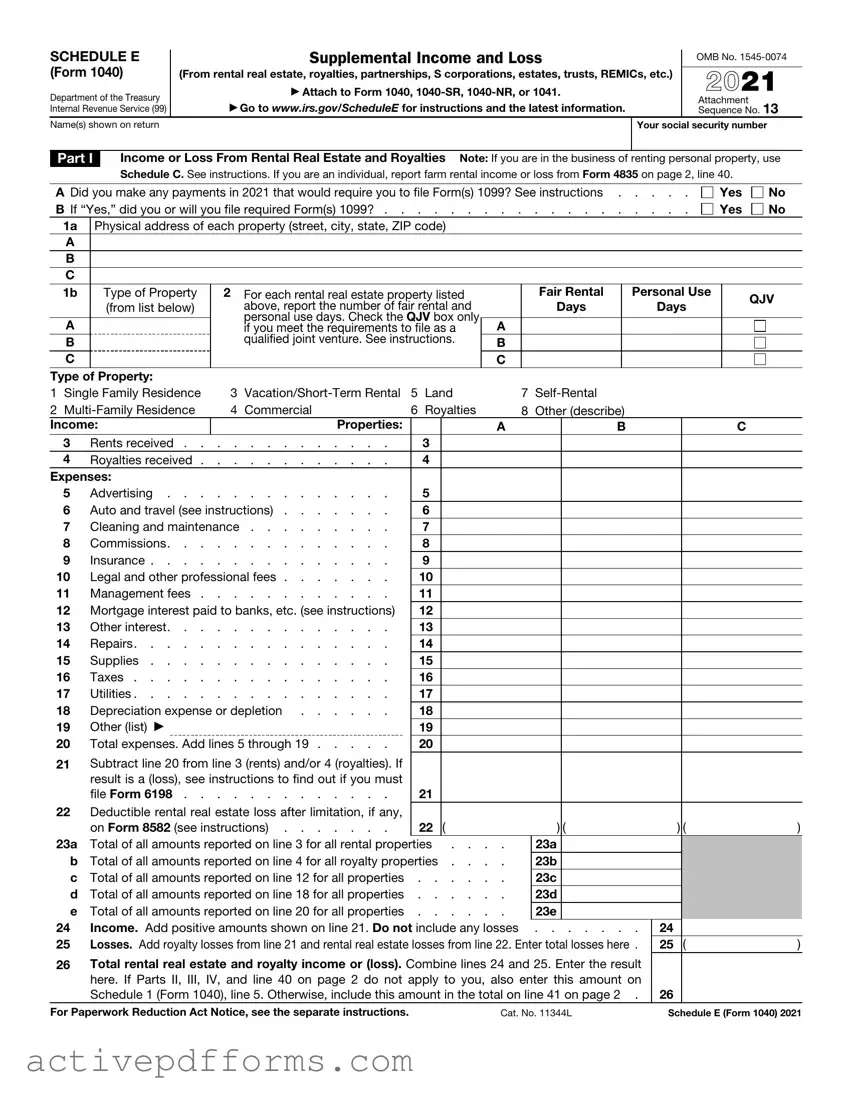

The tax landscape in the United States is complex, with numerous forms that filers must navigate during the tax season. One such form, the IRS Schedule E (Form 1040), is essential for individuals earning rental income, royalties, partnerships, S corporations, trusts, and estates, among other specialized sources of income. This form allows taxpayers to report supplemental income or loss from these ventures, which is a critical aspect of ensuring accurate tax liability calculation and compliance with IRS regulations. Not only does Schedule E serve as a pivotal tool for reporting non-employee income, but it also provides avenues for deductions related to these income sources, such as property maintenance for rentals or operational expenses for partnerships. Understanding and accurately completing this form is paramount for taxpayers looking to optimize their tax situations while adhering to the legal requirements set forth by the Internal Revenue Service. The nuances of Schedule E demand a thorough comprehension of its sections and the types of income each represents, ensuring that taxpayers can effectively report earnings and claim permissible deductions, ultimately shaping their financial responsibilities in the tax year.

SCHEDULE E |

|

|

|

Supplemental Income and Loss |

|

|

OMB No. |

|||||||||||||

|

|

|

|

|

||||||||||||||||

(Form 1040) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

(From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) |

|

2021 |

|||||||||||||||||

Department of the Treasury |

|

|

▶ Attach to Form 1040, |

|

|

|||||||||||||||

|

▶ Go to www.irs.gov/ScheduleE for instructions and the latest information. |

|

|

Attachment |

|

13 |

||||||||||||||

Internal Revenue Service (99) |

|

|

|

Sequence No. |

||||||||||||||||

Name(s) shown on return |

|

|

|

|

|

|

|

|

|

Your social security number |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Part I |

Income or Loss From Rental Real Estate and Royalties Note: If you are in the business of renting personal property, use |

||||||||||||||||||

|

|

|

Schedule C. See instructions. If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40. |

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A Did you make any payments in 2021 that would require you to file Form(s) 1099? See instructions . |

. . . . |

Yes |

|

No |

||||||||||||||||

B If “Yes,” did you or will you file required Form(s) 1099? . . |

. . . . . . . . . . . . . |

|

. . . . |

Yes |

|

No |

||||||||||||||

|

1a |

Physical address of each property (street, city, state, ZIP code) |

|

|

|

|

|

|

|

|

|

|

||||||||

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

Type of Property |

2 |

For each rental real estate property listed |

|

|

Fair Rental |

|

Personal Use |

|

QJV |

||||||||

|

|

|

(from list below) |

|

above, report the number of fair rental and |

|

|

Days |

|

Days |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

personal use days. Check the |

QJV box only |

|

|

|

|

|

|

|

|

|

|

||

|

A |

|

|

|

|

|

if you meet the requirements to file as a |

A |

|

|

|

|

|

|

|

|

|

|||

|

B |

|

|

|

|

|

qualified joint venture. See instructions. |

B |

|

|

|

|

|

|

|

|

|

|||

|

C |

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

Type of Property: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

1 |

Single Family Residence |

3 |

5 |

Land |

7 |

|

|

|

|

|

|

|||||||||

2 |

4 |

Commercial |

6 |

Royalties |

8 |

Other (describe) |

|

|

|

|

|

|

||||||||

Income: |

|

|

|

|

Properties: |

|

|

|

A |

B |

|

|

|

C |

|

|

||||

|

3 |

Rents received |

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|||||

|

4 |

Royalties received |

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|||||

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

5 |

Advertising |

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|||||

|

6 |

Auto and travel (see instructions) |

|

|

6 |

|

|

|

|

|

|

|

|

|

|

|||||

|

7 |

Cleaning and maintenance |

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|||||

|

8 |

Commissions |

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|||||

|

9 |

Insurance |

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|||||

10 |

Legal and other professional fees |

|

|

10 |

|

|

|

|

|

|

|

|

|

|

||||||

11 |

Management fees |

|

|

11 |

|

|

|

|

|

|

|

|

|

|

||||||

12 |

Mortgage interest paid to banks, etc. (see instructions) |

|

|

12 |

|

|

|

|

|

|

|

|

|

|

||||||

13 |

Other interest |

|

|

13 |

|

|

|

|

|

|

|

|

|

|

||||||

14 |

Repairs |

|

|

14 |

|

|

|

|

|

|

|

|

|

|

||||||

15 |

Supplies |

|

|

15 |

|

|

|

|

|

|

|

|

|

|

||||||

16 |

Taxes |

|

|

16 |

|

|

|

|

|

|

|

|

|

|

||||||

17 |

Utilities |

|

|

17 |

|

|

|

|

|

|

|

|

|

|

||||||

18 |

Depreciation expense or depletion |

|

|

18 |

|

|

|

|

|

|

|

|

|

|

||||||

19 |

Other (list) |

▶ |

|

|

|

|

19 |

|

|

|

|

|

|

|

|

|

|

|||

20 |

Total expenses. Add lines 5 through 19 |

|

|

20 |

|

|

|

|

|

|

|

|

|

|

||||||

21Subtract line 20 from line 3 (rents) and/or 4 (royalties). If result is a (loss), see instructions to find out if you must

file Form 6198 . . . . . . . . . . . . .

22Deductible rental real estate loss after limitation, if any,

|

on Form 8582 (see instructions) |

22 ( |

) ( |

|

) ( |

) |

23a |

Total of all amounts reported on line 3 for all rental properties . . . . |

23a |

|

|

|

|

b |

Total of all amounts reported on line 4 for all royalty properties . . . . |

23b |

|

|

|

|

c |

Total of all amounts reported on line 12 for all properties |

23c |

|

|

|

|

d |

Total of all amounts reported on line 18 for all properties |

23d |

|

|

|

|

e |

Total of all amounts reported on line 20 for all properties |

23e |

|

|

|

|

24 |

Income. Add positive amounts shown on line 21. Do not include any losses |

. . . . . . . |

24 |

|

|

|

25 |

Losses. Add royalty losses from line 21 and rental real estate losses from line 22. Enter total losses here . |

25 |

( |

) |

||

26 |

Total rental real estate and royalty income or (loss). Combine lines 24 and 25. Enter the result |

|

|

|

||

|

here. If Parts II, III, IV, and line 40 on page 2 do not apply to you, also enter this amount on |

|

|

|

||

|

Schedule 1 (Form 1040), line 5. Otherwise, include this amount in the total on line 41 on page 2 . |

26 |

|

|

||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11344L |

Schedule E (Form 1040) 2021 |

||||

Schedule E (Form 1040) 2021 |

Attachment Sequence No. 13 |

Page 2 |

Name(s) shown on return. Do not enter name and social security number if shown on other side.

Your social security number

Caution: The IRS compares amounts reported on your tax return with amounts shown on Schedule(s)

Part II Income or Loss From Partnerships and S Corporations — Note: If you report a loss, receive a distribution, dispose of stock, or receive a loan repayment from an S corporation, you must check the box in column (e) on line 28 and attach the required basis computation. If you report a loss from an

27Are you reporting any loss not allowed in a prior year due to the

|

|

|

see instructions before completing this section |

. . . . . . . |

. . . |

Yes |

No |

|||||||||||||||||

28 |

|

|

|

(a) Name |

|

|

|

(b) |

Enter P for |

|

(c) Check if |

|

|

(d) Employer |

|

(e) Check if |

|

|

(f) Check if |

|||||

|

|

|

|

|

|

partnership; S |

|

foreign |

|

|

identification |

basis computation |

|

any amount is |

||||||||||

|

|

|

|

|

|

|

|

|

for S corporation |

partnership |

|

|

|

number |

|

is required |

|

|

not at risk |

|||||

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Passive Income and Loss |

|

|

|

|

|

|

|

Nonpassive Income |

and Loss |

|

|

|||||||||

|

|

|

(g) Passive loss allowed |

|

|

(h) Passive income |

|

(i) Nonpassive loss allowed |

|

(j) Section 179 expense |

(k) Nonpassive income |

|||||||||||||

|

|

(attach Form 8582 if required) |

|

|

from Schedule |

|

|

(see Schedule |

|

|

deduction from Form 4562 |

from Schedule |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29a |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

b |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

|

Add columns (h) and (k) of line 29a |

. . . . . . . |

|

30 |

|

|

|

|

|||||||||||||||

31 |

|

Add columns (g), (i), and (j) of line 29b |

. . . . . . . |

|

31 |

( |

|

|

) |

|||||||||||||||

32 |

|

Total partnership and S corporation income or (loss). Combine lines 30 and 31 . . . . |

|

32 |

|

|

|

|

||||||||||||||||

Part III |

Income or Loss From Estates and Trusts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

33 |

|

|

|

|

|

|

|

(a) Name |

|

|

|

|

|

|

|

|

|

|

(b) Employer |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

identification number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Passive Income and Loss |

|

|

|

|

|

|

|

|

Nonpassive Income and Loss |

|

|

|||||||||

|

|

|

(c) Passive deduction or loss allowed |

|

|

(d) Passive income |

|

(e) Deduction or loss |

|

|

(f) Other income from |

|||||||||||||

|

|

|

(attach Form 8582 if required) |

|

|

|

from Schedule |

|

from Schedule |

|

|

Schedule |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34a |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

b |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

|

Add columns (d) and (f) of line 34a |

. . . . . . . |

|

35 |

|

|

|

|

|||||||||||||||

36 |

|

Add columns (c) and (e) of line 34b |

. . . . . . . |

|

36 |

( |

|

|

) |

|||||||||||||||

37 |

|

Total estate and trust income or (loss). Combine lines 35 and 36 . . . |

. . . . . . . |

|

37 |

|

|

|

|

|||||||||||||||

Part IV |

Income or Loss From Real Estate Mortgage Investment Conduits |

Holder |

||||||||||||||||||||||

38 |

|

|

|

|

|

(b) Employer identification |

(c) Excess inclusion from |

|

(d) Taxable income (net loss) |

(e) Income from |

||||||||||||||

|

|

|

(a) Name |

|

|

Schedules Q, line 2c |

|

|

||||||||||||||||

|

|

|

|

|

|

|

number |

|

|

|

(see instructions) |

|

|

from Schedules Q, line 1b |

Schedules Q, line 3b |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

39 |

|

Combine columns (d) and (e) only. Enter the result here and include in the total on line 41 below |

|

39 |

|

|

|

|

||||||||||||||||

Part V |

Summary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

40 |

|

Net farm rental income or (loss) from Form 4835. Also, complete line 42 below |

|

40 |

|

|

|

|

||||||||||||||||

41 |

|

Total income or (loss). Combine lines 26, 32, 37, 39, and 40. Enter the result here and on Schedule 1 (Form 1040), line 5 ▶ |

|

41 |

|

|

|

|

||||||||||||||||

42Reconciliation of farming and fishing income. Enter your gross farming and fishing income reported on Form 4835, line 7; Schedule

43Reconciliation for real estate professionals. If you were a real estate professional

(see instructions), enter the net income or (loss) you reported |

anywhere on Form |

|

|

1040, Form |

in which |

|

|

you materially participated under the passive activity loss rules |

. . . |

. . . |

43 |

Schedule E (Form 1040) 2021

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Schedule E (Form 1040) is used to report income and losses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. |

| Applicable Taxpayers | This form is for taxpayers who have earned income from the sources listed above and need to report these on their federal tax return. |

| Filing Requirements | Taxpayers must file Schedule E with their Form 1040 if they have received income or incurred losses from any of the specified sources during the tax year. |

| Passive Activity Limits | Income and losses reported on Schedule E could be subject to passive activity loss limitations, depending on the taxpayer's level of participation in the activity. |

| Supplemental Information | Schedule E must be accompanied by other forms or schedules if the income reported includes partnership or S corporation interests, or if special limitations apply. |

| State Specific Forms | Some states require taxpayers to complete additional forms or schedules similar to Schedule E to report the same income on their state tax returns. The requirements vary depending on the state's governing law. |

| Deadline for Filing | Schedule E must be filed by the tax return deadline, typically April 15th. If an extension is filed for the Form 1040, it also applies to Schedule E. |

To successfully fill out the IRS Schedule E (Form 1040), you will be reporting income or losses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. This form is a critical component of your tax return if any of these situations apply to you. Ensure you have all necessary information, including income statements, expense reports, and any relevant Partnership or S Corporation forms (Schedules K-1), before you begin. The following steps will guide you through completing the form accurately.

Once completed, attach Schedule E to your Form 1040 and submit it to the IRS by the tax filing deadline. If you need more time to prepare your return, remember to file an extension to avoid potential penalties. Ensure all entries are clear and readable to facilitate smooth processing of your tax return.

What is IRS Schedule E (Form 1040)?

IRS Schedule E (Form 1040) is used by taxpayers to report income and losses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in Real Estate Mortgage Investment Conduits (REMICs). This information is crucial for calculating the taxable income and understanding the tax responsibilities related to these sources.

Who needs to file Schedule E (Form 1040)?

Individuals who receive income or sustain losses from rental properties, royalties, or pass-through entities such as partnerships, S corporations, estates, and trusts, must complete and file Schedule E (Form 1040). This form helps in properly declaring and accounting for non-wage income.

Can I file Schedule E electronically?

Yes, you can file Schedule E electronically alongside your Form 1040 through IRS-approved tax software or with the help of a tax professional. Electronic filing (e-filing) is a convenient and secure way to submit your tax information and often results in faster processing of refunds.

What information do I need to fill out Schedule E?

This detailed information helps in accurately reporting income and deductions associated with property and royalty income.

How does Schedule E affect my taxes?

Schedule E influences your taxes by detailing passive income sources or losses, which are factored into your overall taxable income. Income from rental properties or royalties increases your taxable income, potentially raising your tax bill, while reported losses can reduce taxable income, potentially lowering your tax liability.

What are common mistakes to avoid when filling out Schedule E?

Ensuring the accuracy of entered information avoids processing delays, audits, and penalties.

Can I deduct rental property losses on Schedule E?

Yes, you can deduct losses on rental properties reported on Schedule E, but there are limits and rules. The IRS allows up to $25,000 in passive activity loss deductions for qualifying taxpayers, but this phases out when the taxpayer's adjusted gross income (AGI) is between $100,000 and $150,000. It's essential to understand these guidelines to fully benefit from potential deductions.

Do I need to file a separate Schedule E for each property?

No, you do not need to file a separate Schedule E for each rental property. Schedule E is designed to accommodate multiple properties. Each property’s income and expenses are reported in its own section on the form. This consolidation simplifies tax reporting for individuals with multiple rental incomes.

Where can I find more information about completing Schedule E?

More information about completing Schedule E can be found on the IRS’s official website. The website provides a detailed guide, including instructions for each part of the form and answers to frequently asked questions. For personalized assistance, consider consulting with a tax professional familiar with real estate and royalty income.

Filing taxes can be complicated, and it's easy to make mistakes, especially when dealing with the IRS Schedule E (Form 1040) for reporting rental income, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Here are ten common errors people make on this form:

Not reporting all income sources. Many people forget to include all the income they receive from rental properties, partnerships, or S corporations. This can lead to inaccuracies in their tax returns.

Incorrectly calculating expenses. It's important to accurately calculate and report expenses related to rental properties or other income sources on Schedule E. Overestimating expenses can raise red flags with the IRS.

Mixing up personal expenses with rental expenses. Some individuals mistakenly claim personal expenses as rental expenses. Only expenses directly tied to the rental activity can be deducted.

Failing to separate properties. If you own multiple rental properties, you need to report the income and expenses for each property separately on Schedule E.

Incorrectly reporting rental days. Mistakes often occur when taxpayers incorrectly count the number of days a property was rented out versus the number of days it was used for personal purposes.

Omitting carryover losses. If you have losses from previous years that are eligible to be carried over, failing to include them on your current Schedule E can result in a larger tax liability than necessary.

Misunderstanding passive activity loss rules. There are specific rules about when you can deduct passive activity losses, and misunderstanding these can lead to incorrect filings.

Incorrectly classifying rental properties. Sometimes, taxpayers incorrectly classify properties, not following the IRS guidelines, which can impact the tax treatment of income and expenses.

Forgetting to report supplemental income and loss. Supplemental income and losses, including that from rental real estate, must be reported on Schedule E and are often overlooked.

Using the wrong form. Occasionally, individuals use the wrong form entirely, filing out a Schedule C for business profit or loss, instead of a Schedule E for supplemental income and loss.

By paying close attention to these common pitfalls, individuals can avoid making these mistakes on their Schedule E forms. Ensuring accurate and complete information on your tax return helps to avoid the potential for audits and penalties from the IRS.

Preparing your tax returns involves more than just filling out the IRS Schedule E (Form 1040) for supplemental income and loss. This form is often just a part of a larger suite of documents and forms necessary for a comprehensive tax return, especially if you're dealing with rental properties, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Here, we'll explore a few key documents that are often used in conjunction with the Schedule E to ensure thorough and accurate tax filing.

Filing taxes can seem overwhelming, especially with the various forms and documents required to accurately report income, deductions, and credits. However, understanding how these forms work in conjunction with the IRS Schedule E becomes manageable with the right information and guidance. Each form serves its unique purpose, ensuring that individuals and entities accurately report their financial activities and adhere to tax regulations. By familiarizing oneself with these forms, taxpayers can navigate the complexities of the tax filing process more confidently and efficiently.

Schedule C (Form 1040): Similar to Schedule E, Schedule C is used by individuals to report income or losses from businesses they operated or professions they practiced as a sole proprietor. Both forms detail income and expenses related to the taxpayer's specific activities, but while Schedule E focuses on rental property, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs, Schedule C is concerned with profit or loss from a business.

Schedule D (Form 1040): This form is used to report capital gains or losses from transactions involving capital assets. Schedule D shares similarities with Schedule E in that both deal with the reporting of income, albeit different types. Schedule D's emphasis is on investments, whereas Schedule E is concerned with passive income sources like rents or partnerships.

Schedule F (Form 1040): Schedule F is for reporting income and expenses related to farming. Both this and Schedule E provide a framework for taxpayers to subtract their expenses from their income to determine their taxable income from specific activities (farming for Schedule F and rental, royalty, and pass-through entity income for Schedule E).

Form 8582 (Passive Activity Loss Limitations): This form is closely related to Schedule E because it is required when a taxpayer needs to report passive activity losses, which are common to those reporting on Schedule E. Form 8582 helps taxpayers calculate the allowable passive activity loss for the year, which can affect income reported on Schedule E.

Schedule K-1 (Form 1065): This form is used by partnerships to report the share of a partner's income, deductions, credits, etc. It is directly related to Schedule E in that the information from Schedule K-1 is needed by the partner to fill out Schedule E, showing how pass-through entity income affects their personal tax obligations.

Schedule K-1 (Form 1120-S): Similar to the Schedule K-1 for Form 1065, this version is for shareholders of S corporations. It provides details on the shareholder’s share of income, losses, deductions, and credits. Again, like the partnership K-1, it is essential for completing Schedule E for those individuals who need to report income from S corporations.

Form 8825 (Rental Real Estate Income and Expenses of a Partnership or an S Corporation): Form 8825 is used by partnerships and S corporations to report income and expenses from rental real estate. It is akin to Schedule E in its focus on rental income and expenses, but it is specifically for entities rather than individuals. The information from Form 8825 can feed into Schedule E through Schedule K-1, aligning both forms in the process of reporting rental income on individual returns.

Filling out the IRS Schedule E (Form 1040) involves reporting income or loss from rental real estate, royalties, partnerships, S corporations, trusts, and more. It's essential to approach this task carefully to ensure accuracy and compliance with tax laws. Here's a straightforward list of dos and don'ts to help guide you through the process.

Do:When it comes to filing taxes, particularly for those who need to include additional schedules like the IRS Schedule E (Form 1040), there are several misconceptions that can confuse taxpayers. Let's dispel some common myths to help clarify the process:

All rental income is taxed the same. This isn't true. The IRS distinguishes between short-term and long-term rentals, which can affect your tax responsibilities. For example, if you rent out your property for less than 14 days a year, that income may not be taxable. However, the specifics can get complex, so understanding the nuances of rental income on Schedule E is crucial.

Personal use of rental doesn’t impact taxes. Actually, how often you use your rental property for personal reasons can significantly affect your tax deductions. If you use the property yourself for more than 14 days or more than 10% of the total days it is rented, deductions may be limited. Tracking and reporting personal use accurately is vital.

You can only deduct losses from real estate activities. While it's common to use Schedule E for reporting losses from real estate, it's not limited to that. Taxpayers can also report losses from partnerships, S Corporations, trusts, and more. Understanding the breadth of what Schedule E encompasses can open up additional tax strategies.

Passive activity losses are not deductible. This is a complex area, but not entirely true. Generally, losses from passive activities can't offset other types of income. However, there are exceptions, especially for real estate professionals or when a taxpayer actively participates in rental activities, allowing some or all of those losses to be deducted. Navigating these rules is essential for maximizing your tax benefits.

Filing a Schedule E is only for the wealthy. This notion might deter some from taking advantage of potential tax benefits. In reality, anyone who receives rental income or income from any entity reported on Schedule E should file it, regardless of their overall income level. It's about properly reporting your income and expenses, not your wealth.

Once filed, the information on Schedule E cannot be amended. Mistakes happen and circumstances change, which is why the IRS allows amendments to previously filed returns. If you need to correct or update information on your Schedule E, you can file an amended tax return using Form 1040-X. This flexibility helps ensure your tax filings accurately reflect your financial picture.

Tax laws can be intricate, and the misconceptions around the IRS Schedule E (Form 1040) illustrate just how easily taxpayers can be led astray. Understanding the specifics can save you a lot of time and potentially money, making it worth getting to know the ins and outs of filing your taxes properly.

The IRS Schedule E 1040 form is a crucial document for taxpayers who need to report income and expenses from rental properties, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Understanding how to properly complete and utilize this form is vital for accurately filing your taxes and ensuring compliance with IRS regulations. Here are ten key takeaways to guide you:

By keeping these key points in mind, taxpayers can better navigate the complexities of Schedule E of Form 1040, ensuring they correctly report their income and expenses while adhering to IRS regulations.

Lash Extension Consent Form - A step-by-step guide that walks you through what to expect during your eyelash extension appointment, ensuring a smooth and enjoyable experience.

Usps Separation Letter - For employees pondering retirement, this form is not applicable, highlighting the focus on resignations and inter-agency transfers.