Free IRS W-2 PDF Template

Free IRS W-2 PDF Template

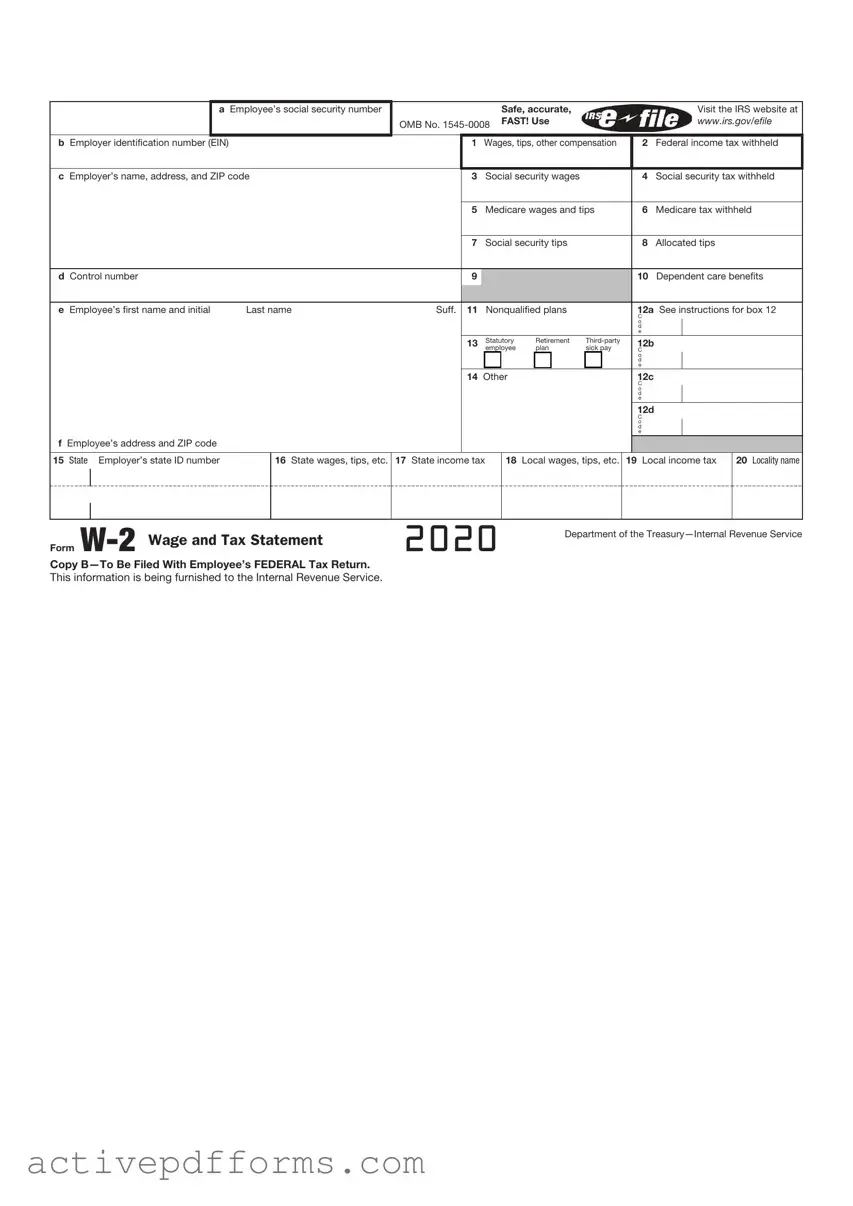

Every year, employees across the United States anxiously await the arrival of a crucial document that plays a pivotal role in their financial affairs - the W-2 form. As the primary reporting document for wage and salary information for employees, its arrival kickstarts the annual ritual of tax preparation and filing. The Internal Revenue Service (IRS) mandates that employers must furnish this form, which details not just wages paid but also taxes withheld from an employee's paycheck over the calendar year. This includes federal, state, and other taxes, making the W-2 an essential piece of the puzzle in accurately fulfilling one’s tax obligations. Furthermore, the form accounts for other contributions such as those toward retirement plans and health insurance. Given its significance in the financial lives of millions, understanding the nuances and ensuring its accurate completion is paramount for both employers and employees. It doesn't only serve as a record of earnings but also affects tax refund calculations and potential liabilities, thereby holding a significant influence on one's financial health.

Attention:

You may file Forms

Note: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file Copy A downloaded from this website with the SSA; a penalty may be imposed for filing forms that can’t be scanned. See the penalties section in the current General Instructions for Forms

Please note that Copy B and other copies of this form, which appear in black, may be downloaded, filled in, and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns such as Forms

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22222 |

VOID |

|

|

a |

Employee’s social security number |

For Official Use Only ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

OMB No. |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

b Employer identification number (EIN) |

|

|

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

d Control number |

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

|

Last name |

|

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

15 State Employer’s state ID number |

|

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

|

20 Locality name |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

||||||||||||||||||||||

|

|

|

|

|

For Privacy Act and Paperwork Reduction |

||||||||||||||||||||||

|

Copy |

|

|

|

|

|

Act Notice, see the separate instructions. |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Form |

|

|

|

|

|

|

|

|

|

|

Cat. No. 10134D |

|||||||||||||||

Do Not Cut, Fold, or Staple Forms on This Page

22222 |

a Employee’s social security number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

OMB No. |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b Employer identification number (EIN) |

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

15 State Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

Copy

|

|

a |

Employee’s social security number |

|

|

|

Safe, accurate, |

|

|

|

|

|

Visit the IRS website at |

|

|||||

|

|

|

|

|

OMB No. |

FAST! Use |

|

|

|

|

|

www.irs.gov/efile |

|

||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

b Employer identification number (EIN) |

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

|

|

||||

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

15 State Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Copy

This information is being furnished to the Internal Revenue Service.

Notice to Employee

Do you have to file? Refer to the Instructions for Forms 1040 and

Earned income credit (EIC). You may be able to take the EIC for 2021 if your adjusted gross income (AGI) is less than a certain amount. The amount of the credit is based on income and family size. Workers without children could qualify for a smaller credit. You and any qualifying children must have valid social security numbers (SSNs). You can’t take the EIC if your investment income is more than the specified amount for 2021 or if income is earned for services provided while you were an inmate at a penal institution. For 2021 income limits and more information, visit www.irs.gov/EITC. See also Pub. 596, Earned Income Credit. Any EIC that is more than your tax liability is refunded to you, but only if you file a tax return.

Employee’s social security number (SSN). For your protection, this form may show only the last four digits of your SSN. However, your employer has reported your complete SSN to the IRS and SSA.

Clergy and religious workers. If you aren’t subject to social security and Medicare taxes, see Pub. 517, Social Security and Other Information for Members of the Clergy and Religious Workers.

Corrections. If your name, SSN, or address is incorrect, correct Copies B, C, and 2 and ask your employer to correct your employment record. Be sure to ask the employer to file Form

Cost of

Credit for excess taxes. If you had more than one employer in 2021 and more than $8,853.60 in social security and/or Tier 1 railroad retirement (RRTA) taxes were withheld, you may be able to claim a credit for the excess against your federal income tax. If you had more than one railroad employer and more than $5,203.80 in Tier 2 RRTA tax was withheld, you may also be able to claim a credit. See the Instructions for Forms 1040 and

(See also Instructions for Employee on the back of Copy C.)

aEmployee’s social security number

|

This information is being furnished to the Internal Revenue Service. If you |

|

OMB No. |

are required to file a tax return, a negligence penalty or other sanction |

|

may be imposed on you if this income is taxable and you fail to report it. |

||

|

b Employer identification number (EIN) |

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 State Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

||||||||||||

|

|

|

|

Safe, accurate, |

|

|||||||||||

Copy |

|

|

|

|

|

|

|

FAST! Use |

|

|||||||

(See Notice to Employee on the back of Copy B.)

Instructions for Employee

(See also Notice to Employee on the back of Copy B.)

Box 1. Enter this amount on the wages line of your tax return.

Box 2. Enter this amount on the federal income tax withheld line of your tax return.

Box 5. You may be required to report this amount on Form 8959, Additional Medicare Tax. See the Instructions for Forms 1040 and

Box 6. This amount includes the 1.45% Medicare Tax withheld on all Medicare wages and tips shown in box 5, as well as the 0.9% Additional Medicare Tax on any of those Medicare wages and tips above $200,000.

Box 8. This amount is not included in box 1, 3, 5, or 7. For information on how to report tips on your tax return, see the Instructions for Forms 1040 and

You must file Form 4137, Social Security and Medicare Tax on Unreported Tip Income, with your income tax return to report at least the allocated tip amount unless you can prove with adequate records that you received a smaller amount. If you have records that show the actual amount of tips you received, report that amount even if it is more or less than the allocated tips. Use Form 4137 to figure the social security and Medicare tax owed on tips you didn’t report to your employer. Enter this amount on the wages line of your tax return. By filing Form 4137, your social security tips will be credited to your social security record (used to figure your benefits).

Box 10. This amount includes the total dependent care benefits that your employer paid to you or incurred on your behalf (including amounts from a section 125 (cafeteria) plan). Any amount over $5,000 is also included in box 1. Complete Form 2441, Child and Dependent Care Expenses, to figure any taxable and nontaxable amounts.

Box 11. This amount is (a) reported in box 1 if it is a distribution made to you from a nonqualified deferred compensation or nongovernmental section 457(b) plan, or (b) included in box 3 and/or box 5 if it is a prior year deferral under a nonqualified or section 457(b) plan that became taxable for social security and Medicare taxes this year because there is no longer a substantial risk of forfeiture of your right to the deferred amount. This box shouldn’t be used if you had a deferral and a

distribution in the same calendar year. If you made a deferral and received a distribution in the same calendar year, and you are or will be age 62 by the end of the calendar year, your employer should file Form

Box 12. The following list explains the codes shown in box 12. You may need this information to complete your tax return. Elective deferrals (codes D, E, F, and S) and designated Roth contributions (codes AA, BB, and EE) under all plans are generally limited to a total of $19,500 ($13,500 if you only have SIMPLE plans; $22,500 for section 403(b) plans if you qualify for the

However, if you were at least age 50 in 2021, your employer may have allowed an additional deferral of up to $6,500 ($3,000 for section 401(k)(11) and 408(p) SIMPLE plans). This additional deferral amount is not subject to the overall limit on elective deferrals. For code G, the limit on elective deferrals may be higher for the last 3 years before you reach retirement age. Contact your plan administrator for more information. Amounts in excess of the overall elective deferral limit must be included in income. See the Instructions for Forms 1040 and

Note: If a year follows code D through H, S, Y, AA, BB, or EE, you made a

(continued on back of Copy 2)

|

|

a Employee’s social security number |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

OMB No. |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b Employer identification number (EIN) |

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

15 State Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

Copy

Income Tax Return

Instructions for Employee (continued from back of

Copy C)

Box 12 (continued)

Box 13. If the “Retirement plan” box is checked, special limits may apply to the amount of traditional IRA contributions you may deduct. See Pub.

Box 14. Employers may use this box to report information such as state disability insurance taxes withheld, union dues, uniform payments, health insurance premiums deducted, nontaxable income, educational assistance payments, or a member of the clergy’s parsonage allowance and utilities. Railroad employers use this box to report railroad retirement (RRTA) compensation, Tier 1 tax, Tier 2 tax, Medicare tax, and Additional Medicare Tax. Include tips reported by the employee to the employer in railroad retirement (RRTA) compensation.

Note: Keep Copy C of Form

|

VOID |

|

|

a Employee’s social security number |

OMB No. |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

b Employer identification number (EIN) |

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

15 State Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2021 |

|

|

Department of the |

|||||||||||||||

|

|

|

|

For Privacy Act and Paperwork Reduction |

|||||||||||||||

Copy |

|

|

|

|

|

|

|

|

|

|

Act Notice, see separate instructions. |

||||||||

| Fact Name | Description |

|---|---|

| Purpose of the W-2 Form | This form is utilized by employers to report an employee's annual earnings and the amount of taxes withheld from their paycheck to the Internal Revenue Service (IRS). |

| Deadline for Distribution | Employers must send out the W-2 form to their employees by January 31st following the end of the tax year, to ensure employees have sufficient time to file their income taxes. |

| Electronic Accessibility | While physical copies are traditionally mailed, employees also have the option to receive their W-2 form electronically, provided they consent to this method. |

| State-Specific Forms and Laws | Some states may require additional state-specific tax forms in addition to the federal W-2 form. Laws regarding these forms vary by state, reflecting the state's tax regulations and requirements. |

Filling out an IRS W-2 form is an essential task for employers as it involves reporting the income, tax withholdings, and other financial information of their employees for the tax year. It is important to complete this form accurately to ensure that employees have the information they need to file their tax returns. The process may seem complex initially but can be made straightforward by following a step-by-step approach. Below are the steps to accurately fill out the W-2 form:

Once the W-2 form is filled out completely and accurately, the next steps involve distributing the forms and filing them with the Social Security Administration (SSA). Employers must provide copies to their employees by January 31st of the year following the tax year reported, ensuring employees have ample time to file their tax returns. Additionally, employers are required to submit Copy A of all W-2 forms, along with a W-3 form which summarizes the W-2 information, to the SSA by the last day of February (if filing by paper) or the end of March (if filing electronically). Adhering to these guidelines will assist in maintaining compliance with IRS regulations and ensuring the timely processing of tax-related information.

What is a W-2 form?

The W-2 form, also known as the Wage and Tax Statement, is a document that employers must send to their employees and the Internal Revenue Service (IRS) at the end of each year. It reports the employee's annual wages and the amount of taxes withheld from their paycheck. This form is essential for employees to prepare their annual tax returns, as it provides critical information regarding their income and taxes paid throughout the year.

When should I receive my W-2 form?

Employers are required to provide you with your W-2 form by January 31st of the year following the reported earnings. If this date falls on a weekend or holiday, the deadline is extended to the next business day. This allows employees ample time to file their taxes accurately and promptly.

What should I do if I haven’t received my W-2?

If you do not receive your W-2 form by the middle of February, it's advisable to take the following steps:

Can I file my taxes without a W-2?

While it's crucial to have your W-2 form to file your taxes accurately, the IRS does allow you to file without it if you haven't received the form by the tax filing deadline. In such cases, you can use Form 4852, Substitute for Form W-2, Wage and Tax Statement. You will need to estimate your income and withholding taxes as accurately as possible. It's important to note that filing with an estimated W-2 may delay the processing of your tax return.

What if the information on my W-2 is incorrect?

If you discover any discrepancies on your W-2 form, you should promptly contact your employer to issue a corrected W-2, known as a W-2c. Common errors might include incorrect wage, tax withholding amounts, or personal information. It is essential to wait for the corrected W-2 before filing your taxes to ensure that your tax return is accurate.

Can I access my W-2 online?

Many employers offer the option to access your W-2 electronically. Opting in usually requires you to give your consent to receive the form electronically instead of by mail. Accessing your W-2 online can be faster and more secure, and this method also helps in reducing paper waste.

What if I worked for multiple employers?

If you worked for multiple employers during the year, you should receive a W-2 form from each employer. It's your responsibility to ensure you have received all your W-2 forms before filing your taxes. If you’re missing a W-2 from any employer, follow the steps outlined above to obtain the missing form. Combining information from all your W-2 forms is crucial for accurately filing your tax return and calculating your total income and tax liability.

When completing the IRS W-2 form, individuals often make errors that can lead to delays in processing or even penalties. It's crucial to approach this task carefully to ensure accuracy. Below are seven common mistakes encountered:

Incorrectly reporting names or Social Security numbers. It's imperative that the names and Social Security numbers on the W-2 form exactly match the information on the individual's Social Security card to avoid processing issues.

Failure to report all income. All forms of income, including tips and any other earnings, must be reported accurately. Omitting income can lead to discrepancies and potential audits.

Incorrectly filling out tax withheld amounts. The federal, state, and other taxes withheld must be reported precisely as these figures are critical for calculating the individual’s tax liability or refund.

Misclassifying employee benefits. Certain non-cash benefits, such as health insurance or retirement plan contributions, must be reported accurately. Misclassification can result in incorrect tax calculations.

Failing to provide complete state information. This includes correctly filling out the employer’s state ID number and the state wages and taxes. Inaccuracies or omissions can cause delays in state tax processing.

Mixing up boxes. Each box on the W-2 form has a specific purpose and must contain the correct information. Placing information in the wrong box can lead to misinterpretation of data.

Forgetting to sign and date the form (if submitting a paper copy). A common oversight is the failure to sign and date the form, which is necessary for validation.

Avoiding these mistakes requires meticulous attention to detail and a thorough understanding of the form's requirements. Double-checking all entries before submission can significantly reduce the risk of errors.

When dealing with tax documents, particularly around the filing season, it's essential to have a comprehensive understanding of the materials that often accompany the IRS W-2 form. The W-2 form is a fundamental document that reports an employee's annual wages and the amount of taxes withheld from their paycheck. However, to ensure a smooth and compliant tax filing process, several other forms and documents are frequently required to provide a complete picture of an individual's financial situation for the tax year.

Understanding the purpose and requirement of each of these documents can significantly simplify the tax filing process. It's not just about compiling numbers but gathering a precise, complete set of records that accurately reflect an individual's financial activities over the tax year. Proper documentation is crucial for compliance and ensuring that individuals take full advantage of any tax benefits or deductions to which they are entitled. Navigating through this process with a clear understanding of each document's role can alleviate some of the complexities associated with tax season.

Filling out the IRS W-2 form correctly is crucial for both employers and employees. It not only helps in maintaining accurate pay records but also ensures compliance with tax regulations. To guide you through the process, here’s a list of dos and don'ts:

Do:

Don’t:

When it comes to understanding the IRS W-2 form, many misconceptions can lead to confusion and frustration. It is important to clear these misunderstandings to ensure compliance with tax regulations and to prevent any unnecessary errors. Here are seven common misconceptions about the IRS W-2 form:

Only full-time employees receive a W-2 form. This is incorrect. Whether an individual is a full-time or part-time employee, if an employer has paid them wages, they should provide the employee with a W-2 form. The key factor is not the number of hours worked but whether the individual is classified as an employee.

Contractors should expect to receive a W-2 form. This is a common misconception. Independent contractors do not receive a W-2 form; instead, they should receive a Form 1099-NEC from the entities that paid them. This form reflects the income they earned as non-employees.

Employees can opt to receive their W-2 forms electronically only. While many employers offer electronic W-2 forms for convenience and environmental reasons, employees must consent to receive their W-2 form in an electronic format only. Otherwise, employers are required to provide a paper copy.

All the information on my W-2 form is accurate. While employers strive to ensure accuracy in reporting, mistakes can happen. It's important for employees to review their W-2 forms carefully for any discrepancies in personal information or reported earnings and taxes. If errors are found, they should contact their employer to correct the form.

I don’t need to file a tax return if I didn’t earn enough to receive a W-2 form. This is a misconception that can lead to tax issues. Even if an individual didn't earn enough to require an employer to issue a W-2 form, they may still be required to file a tax return based on other criteria, such as self-employment earnings or other sources of income.

W-2 forms are private and cannot be shared with anyone besides the IRS. While W-2 forms contain sensitive personal information, they are often required to be shared with state tax agencies, and individuals may need to provide copies when applying for loans or financial assistance. It is crucial, however, to ensure this information is shared securely to protect against identity theft.

The deadline for employers to issue W-2 forms is flexible. The IRS sets a strict deadline for employers to provide W-2 forms to their employees, typically January 31st of the year following the reported earnings. This deadline is important for allowing employees adequate time to file their tax returns.

The IRS W-2 form, a critical document for both employers and employees in the United States, serves as a report detailing the wages paid and taxes withheld for an employee over the tax year. Understanding its nuances can significantly ease the tax filing process, ensuring compliance with federal regulations and potentially averting common pitfalls. Here are five key takeaways regarding the completion and utilization of the IRS W-2 form:

Adhering to these guidelines will ease the annual tax reporting burden, facilitate compliance with federal tax obligations, and ensure the accuracy and timeliness of information submitted to the IRS and Social Security Administration.

Scedule C - Proper documentation and record-keeping throughout the year assist taxpayers in completing the Schedule C accurately and maximize deductions.

Ncaa Physical Form 2023 - Encourages thorough consideration of an athlete's medical history, including surgeries and hospitalizations, in determining sports fitness.