Free IRS W-3 PDF Template

Free IRS W-3 PDF Template

Every year, businesses face the task of wrapping up their payroll responsibilities, a crucial part of which involves reporting to the Internal Revenue Service (IRS). In this context, the IRS W-3 form plays a pivotal role. It acts as a summary or transmittal form for all W-2 forms issued by an employer, consolidating vital data on the earnings, social security wages, Medicare wages, and tax withholdings for all employees over the past year. This form is mandatory for employers who opt for paper filing and serves as a key document to ensure the IRS has a comprehensive overview of an organization's payroll information. The accuracy of the information on the W-3 is paramount, as it directly affects the accuracy of an employee's social security benefits among other things. Understanding its purpose, knowing when and how to file it, and recognizing its impact on an organization's annual tax reporting obligations is essential for businesses of all sizes.

Attention:

You may file Forms

The maximum amount of dependent care assistance benefits excludable from income may be increased for 2021. The American Rescue Plan Act of 2021 permits employers to increase the amount of dependent care benefits under their plans that can be excluded from an employee’s income from $5,000 ($2,500 for married filing separately) to up to $10,500 ($5,250 for married filing separately). See section C of Notice

Internal Revenue Bulletin:

Note: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file Copy A downloaded from this website with the SSA; a penalty may be imposed for filing forms that can’t be scanned. See the penalties section in the current General Instructions for Forms

Please note that Copy B and other copies of this form, which appear in black, may be downloaded, filled in, and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns such as Forms

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

DO NOT STAPLE

33333

b

Kind of Payer

(Check one)

a Control number |

|

|

For Official Use Only ▶ |

||

|

|

|

|

|

OMB No. |

|

941 |

Military |

943 |

|

944 |

▲ |

|

||||

|

|

|

|

Kind |

|

|

|

Hshld. |

Medicare |

of |

|

|

Employer |

||||

|

emp. |

govt. emp. |

|||

|

|

|

|

|

(Check one) |

▲

None apply |

501c |

|||||||||

|

|

|

|

|

|

|

|

sick pay |

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

(Check if |

||

State/local |

State/local 501c Federal govt. |

|||||||||

applicable) |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

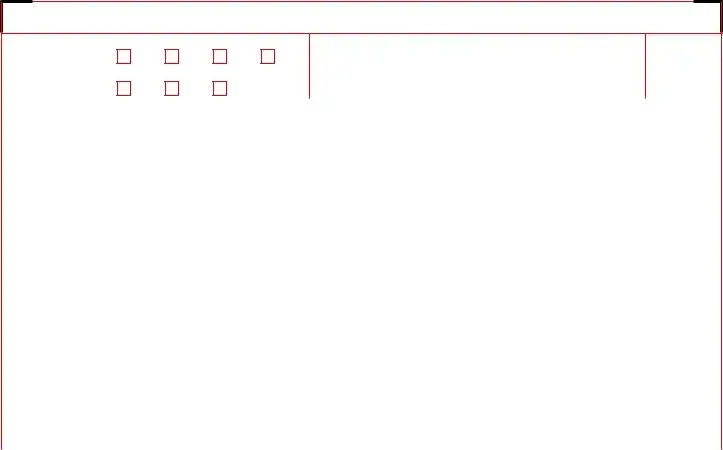

c Total number of Forms |

|

d Establishment number |

1 Wages, tips, other compensation |

2 Federal income tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

e Employer identification number (EIN) |

3 Social security wages |

4 Social security tax withheld |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f Employer’s name |

|

5 |

Medicare wages and tips |

6 Medicare tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

8 Allocated tips |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

10 Dependent care benefits |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

11 Nonqualified plans |

12a Deferred compensation |

|

||||

|

g Employer’s address and ZIP code |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

h Other EIN used this year |

|

13 For |

12b |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|||||

|

15 State |

Employer’s state ID number |

14 Income tax withheld by payer of |

|

||||||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 State wages, tips, etc. |

|

17 State income tax |

18 Local wages, tips, etc. |

19 Local income tax |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s contact person |

|

|

Employer’s telephone number |

For Official Use Only |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s fax number |

|

|

Employer’s email address |

|

|

|

|

||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return and accompanying documents, and, to the best of my knowledge and belief, they are true, correct, and complete.

Signature ▶ |

Title ▶ |

|

Date ▶ |

Form |

2022 |

Department of the Treasury |

|

Internal Revenue Service |

|||

Send this entire page with the entire Copy A page of Form(s)

Do not send any payment (cash, checks, money orders, etc.) with Forms

Reminder

Separate instructions. See the 2022 General Instructions for Forms

Purpose of Form

Complete a Form

The SSA strongly suggests employers report Form

•

•File Upload. Upload wage files to the SSA you have created using payroll or tax software that formats the files according to the SSA’s Specifications for Filing Forms

When To File Paper Forms

Mail Form

Where To File Paper Forms

Send this entire page with the entire Copy A page of Form(s)

Social Security Administration

Direct Operations Center

Note: If you use “Certified Mail” to file, change the ZIP code to

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions.

Cat. No. 10159Y

| Fact Number | Description |

|---|---|

| 1 | The IRS W-3 form is a summary or transmittal form that accompanies the W-2 forms sent to the Social Security Administration. |

| 2 | It summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the previous year. |

| 3 | Employers must file the W-3 form only when they are sending paper copies of the W-2 forms to the Social Security Administration. |

| 4 | The deadline for filing the W-3 form is January 31 each year, aligning with the deadline for W-2 forms. |

| 5 | There are no state-specific versions of the IRS W-3 form as it is a federal document; however, some states may require separate state-specific wage reporting. |

| 6 | Filing the W-3 form accurately is crucial as it helps the Social Security Administration properly credit employees' earnings records, which affects future benefits. |

| 7 | The IRS does not require electronic filers to submit a W-3, as the electronic submission system automatically generates a summary of the W-2 information. |

Filling out the IRS W-3 form is a critical step for employers at the end of the tax year. This document, often referred to as the "Transmittal of Wage and Tax Statements," is essential for summarizing the information reported on your employees' W-2 forms. It's necessary when you are sending W-2 forms to the Social Security Administration. Accuracy and timeliness in completing this process cannot be overstated, as it ensures compliance with federal regulations and facilitates the correct reporting of employee earnings and withholdings. While the task may seem daunting at first, understanding each part of the form and what information is required can make the process smoother and more efficient.

Successfully completing and submitting the IRS W-3 form is a direct contribution to the smooth operation of national social security and health care programs. It demonstrates your commitment to complying with federal requirements and supporting your employees' rights and benefits. If you find any of the steps confusing or need further clarification, the IRS provides detailed instructions and resources that can help guide you through the process.

What is the purpose of the IRS W-3 form?

The IRS W-3 form, also known as the Transmittal of Wage and Tax Statements, serves a critical function in the United States tax system. It is used by employers to report the total earnings, Social Security wages, Medicare wages, and withholding for all employees over the previous tax year. Essentially, it summarizes the information contained in all of an employer's W-2 forms, which are provided to individual employees. The W-3 form, along with the W-2 forms, is sent to the Social Security Administration (SSA) to ensure accurate record-keeping and tax compliance.

Who needs to file the W-3 form?

Any employer required to file Form W-2, Wage and Tax Statement, must also file Form W-3. This includes businesses, government agencies, non-profit organizations, and any other entity that has paid wages to employees from which income, social security, or Medicare tax was withheld. It is also required for those who paid wages that aren't subject to withholding but are covered by Medicare or Social Security tax.

When is the W-3 form due?

The W-3 form is due by January 31st of the year following the tax year for which the wages were paid. This deadline aligns with the due date for Form W-2 submissions to employees and the Social Security Administration. Ensuring the form is submitted on time is essential to comply with federal tax obligations and to avoid potential penalties for late submission.

How do you file the W-3 form?

Employers can file the W-3 form either electronically or on paper. The Social Security Administration encourages electronic filing because it is faster and reduces errors. Employers who opt to file paper forms must use a version that is scannable for the SSA processing equipment. Using the correct version of the form and following the specific instructions for filing are crucial steps to ensure efficient and accurate processing.

Is it possible to correct errors on a W-3 form after it has been submitted?

Yes, employers can correct errors on a W-3 form after submission by filing Form W-2c, Corrected Wage and Tax Statement, along with Form W-3c, Transmittal of Corrected Wage and Tax Statements. These forms are used to correct previously submitted W-2 and W-3 forms. Employers should provide detailed explanations for the changes and submit the corrected forms as soon as possible to minimize potential complications with employee tax records and the employer's tax obligations.

Filing the IRS W-3 form, which summarizes the total earnings, taxes withheld, and other pertinent payroll information for all employees for the year, can seem straightforward. Yet, it is quite easy to make mistakes that can lead to delays or additional scrutiny from the IRS. Being aware of common pitfalls can help ensure that this essential document is submitted correctly.

Incorrect Employer Identification Number (EIN): One of the most common errors is entering the wrong EIN. This number is crucial for the IRS to accurately record and process your company's information. Double-checking the EIN for accuracy before submission can prevent processing delays.

Not Using the Correct Year's Form: The IRS updates forms annually, which can include significant changes. Using an outdated form can lead to inaccuracies in reporting and may result in the need to re-submit using the correct document.

Failure to Report All Wages, Tips, and Other Compensation: Every dollar of compensation paid to employees must be reported. Missing or underreporting income can lead to penalties and interest charged to the employer for underpayment of taxes.

Incomplete or Illegible Information: Entries on the W-3 form must be clear and complete. Illegible handwriting or missing information can lead to processing delays or incorrect tax calculations.

Miscalculations: Human errors in calculating totals can occur, especially when done manually. These miscalculations can affect the amounts reported for social security wages, Medicare wages, and income tax withheld. Using software or double-checking calculations can help mitigate these errors.

Not Filing Electronically When Required: For businesses with 250 or more W-2 forms to submit, electronic filing is mandated by the IRS. Failure to comply with this requirement can result in penalties. Even for smaller businesses, electronic filing is recommended for better accuracy and confirmation of receipt.

Attention to these details can save businesses time and resources, ensuring that their submission of the W-3 form is accurate, compliant, and efficient. Consulting with a professional for guidance or to review the form before submission can also be beneficial.

When businesses prepare their annual tax documents, the IRS W-3 form, known as the "Transmittal of Wage and Tax Statements," serves a critical role. This form summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the year. However, the W-3 form rarely travels alone to the IRS. Several other forms and documents complement its journey, ensuring compliance with federal tax obligations. Below are five forms commonly used alongside the IRS W-3 form, each playing its unique part in the tax filing process.

Understanding each of these forms and their purpose can significantly simplify the tax filing process for businesses. Accurate and timely submission of these documents, in concert with the IRS W-3, not only ensures compliance with federal tax laws but also helps maintain the financial well-being of both employees and the business itself. Together, they form a comprehensive snapshot of a business's payroll obligations and fulfillment over the fiscal year.

IRS W-2 Form: This form, called the Wage and Tax Statement, is closely related to the W-3. Employers provide individual W-2 forms to their employees, detailing earnings, tax withholdings, and other related payroll information. The W-3 is essentially a summary or compilation of all the W-2 forms an employer submits, sent to the Social Security Administration.

IRS W-4 Form: Known as the Employee's Withholding Certificate, the W-4 form is used by employees to inform their employers of their tax situation, which determines how much federal income tax to withhold from their paychecks. Its connection to the W-3 is indirect—data from W-4 forms influence the information reported on W-2 forms, which are summarized by the W-3.

IRS Form 940: This is the Federal Unemployment Tax Act (FUTA) Tax Return form. Businesses use it to report yearly federal unemployment taxes. There’s a similarity in the sense that both the 940 and W-3 forms deal with employment taxes, although they report different types of taxes to different federal agencies.

IRS Form 941: Employers use this form to report income taxes, Social Security tax, or Medicare tax withheld from employee's paychecks. Also, they report their portion of Social Security or Medicare tax. This makes Form 941 akin to the W-3 since it deals with payroll reporting on a quarterly basis, compared to the W-3’s annual summary function.

IRS Form 944: This form is designed for small employers with annual tax liabilities of $1,000 or less. It allows them to report withheld federal income tax and employer and employee Social Security and Medicare taxes once a year. Similar to the W-3, Form 944 also summarizes annual payroll tax responsibilities but is intended for smaller taxpayers.

IRS Form 1099-NEC: This form reports non-employee compensation. It is relevant to freelancers, independent contractors, and other non-employees. The connection to the W-3 comes from the fact that while the W-3 summarizes employee compensation and taxes, the 1099-NEC does so for non-employees. Both forms are necessary for a complete picture of a business's payroll obligations.

IRS Form 1099-MISC: Before the introduction of the 1099-NEC for reporting non-employee compensation, the 1099-MISC was used for this purpose. It is still used to report various types of income other than wages, salaries, and tips. The relation to the W-3 is in the broad category of summarizing payments made in the course of a business’s operation.

IRS Form 1096: This form is a summary or transmittal form used to submit information returns to the IRS for forms like the 1099-MISC. Although it serves a different subset of tax documents, its role as a summary form is the connection point with the W-3, which serves a similar summary function for W-2s.

IRS Form 1120: The U.S. Corporation Income Tax Return form is used by corporations to report their income, gains, losses, deductions, credits, and to figure out their federal income tax liability. This form connects with the W-3 conceptually; both are integral parts of annual financial and tax reporting requirements for business entities.

When filing out the IRS W-3 form, it is important to follow specific guidelines to ensure the process is completed correctly and efficiently. Here are the dos and don'ts to keep in mind:

Do:The IRS W-3 form, a critical document used to summarize the total earnings, Social Security wages, Medicare wages, and withholding for all employees for a year, is often misunderstood. Several myths and misconceptions surround this form, leading to errors and confusion for employers. Here's a breakdown of the most common misconceptions and the truth behind them:

Only large businesses need to file the W-3 form: Size doesn't matter when it comes to the W-3. If you're an employer who files W-2 forms, you're required to submit a W-3 to the Social Security Administration. This applies whether your business is large, small, or even if you have just one employee.

Electronic filing is optional: Depending on the number of W-2 forms you're filing, electronic submission might indeed be mandatory. For employers with 250 or more W-2 forms, electronic filing of both W-2s and the W-3 is required by the IRS. This rule makes processing more efficient and reduces errors.

The W-3 is just a summary and doesn't need to be accurate: Accuracy is crucial. The W-3 form is not merely a summary; it's a reflection of the collective information provided on all an employer's W-2 forms. It must match the W-2 forms exactly. Any discrepancies can lead to audits and penalties.

You can file a W-3 form without W-2 forms: The W-3 form is a transmittal document. It accompanies the W-2 forms sent to the Social Security Administration. You cannot submit a W-3 without also submitting W-2 forms for your employees, as it serves as a cover sheet summarizing the W-2 information.

Amendments are a major hassle: Correcting errors is straightforward. If you discover a mistake after filing the W-3 and W-2 forms, you can file a W-2c (Corrected Wage and Tax Statement) and a W-3c (Transmittal of Corrected Wage and Tax Statements). The process for making amendments is clear and is designed to ensure accurate payroll reporting.

Understanding these facts about the W-3 form helps employers maintain compliance with IRS regulations, ensuring accurate and timely reporting of employee wage information. With proper attention to detail and adherence to IRS guidelines, the process can be both smooth and free from penalties.

The IRS W-3 form, often referred to as the Transmittal of Wage and Tax Statements, is an essential document for employers as it summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for a given tax year. Understanding how to properly fill out and utilize this form is critical to ensure compliance with IRS requirements. Here are six key takeaways:

Progressive Virtual Inspection - A preparatory document designed to give car owners a clear view of the financial implications of necessary repairs.

How to Get Divorce Records in California - The final judgment in a divorce case, documenting the dissolution of the marriage, distribution of property, and the self-representation agreement.

Communication Attitude Test - Encourages self-analysis about whether speech concerns are internal or influenced by external feedback.