Free IRS W-8BEN PDF Template

Free IRS W-8BEN PDF Template

The intricacies of tax obligations in the United States can present a considerable challenge, particularly for those who are not American citizens but are engaged in financial activities within the country. Among the array of forms and documents that the Internal Revenue Service (IRS) requires, the IRS W-8BEN form stands out for non-U.S. individuals. This document plays a pivotal role in defining the tax status of foreign nationals, ensuring that they are correctly identified under U.S. tax regulations and enabling them to claim benefits under a tax treaty, if applicable. Essentially, it serves to certify the foreign status of the beneficiary or individual receiving income from U.S. sources, thereby possibly reducing the amount of tax withheld from payments made to them. Moreover, it addresses the complex issue of tax reporting for entities and individuals not residing in the U.S., offering a streamlined process that aids in the avoidance of unnecessary tax burdens. Understanding the nuances and the proper completion of the IRS W-8BEN form can significantly impact the financial dealings of non-U.S. entities in the United States, making it a critical document for international taxpayers.

Form |

|

|

Certificate of Foreign Status of Beneficial Owner for United |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

States Tax Withholding and Reporting (Individuals) |

|

|

|

|

|

|

(Rev. October 2021) |

|

|

▶ For use by individuals. Entities must use Form |

|

|

OMB No. |

|||

Department of the Treasury |

|

|

▶ Go to www.irs.gov/FormW8BEN for instructions and the latest information. |

|

|

|

|

|

|

Internal Revenue Service |

|

|

▶ Give this form to the withholding agent or payer. Do not send to the IRS. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Do NOT use this form if: |

|

|

|

Instead, use Form: |

|||||

• You are NOT an individual |

. |

. |

. . |

. |

|||||

• You are a U.S. citizen or other U.S. person, including a resident alien individual |

. |

. |

. . |

. |

. |

. |

|||

• You are a beneficial owner claiming that income is effectively connected with the conduct of trade or business within the United States |

|

|

|

||||||

(other than personal services) |

. |

. |

. . |

. |

. |

||||

• You are a beneficial owner who is receiving compensation for personal services performed in the United States . . . |

. |

. |

. . |

|

8233 or |

||||

• You are a person acting as an intermediary |

. |

. |

. . |

. |

. |

||||

Note: If you are resident in a FATCA partner jurisdiction (that is, a Model 1 IGA jurisdiction with reciprocity), certain tax account information may be provided to your jurisdiction of residence.

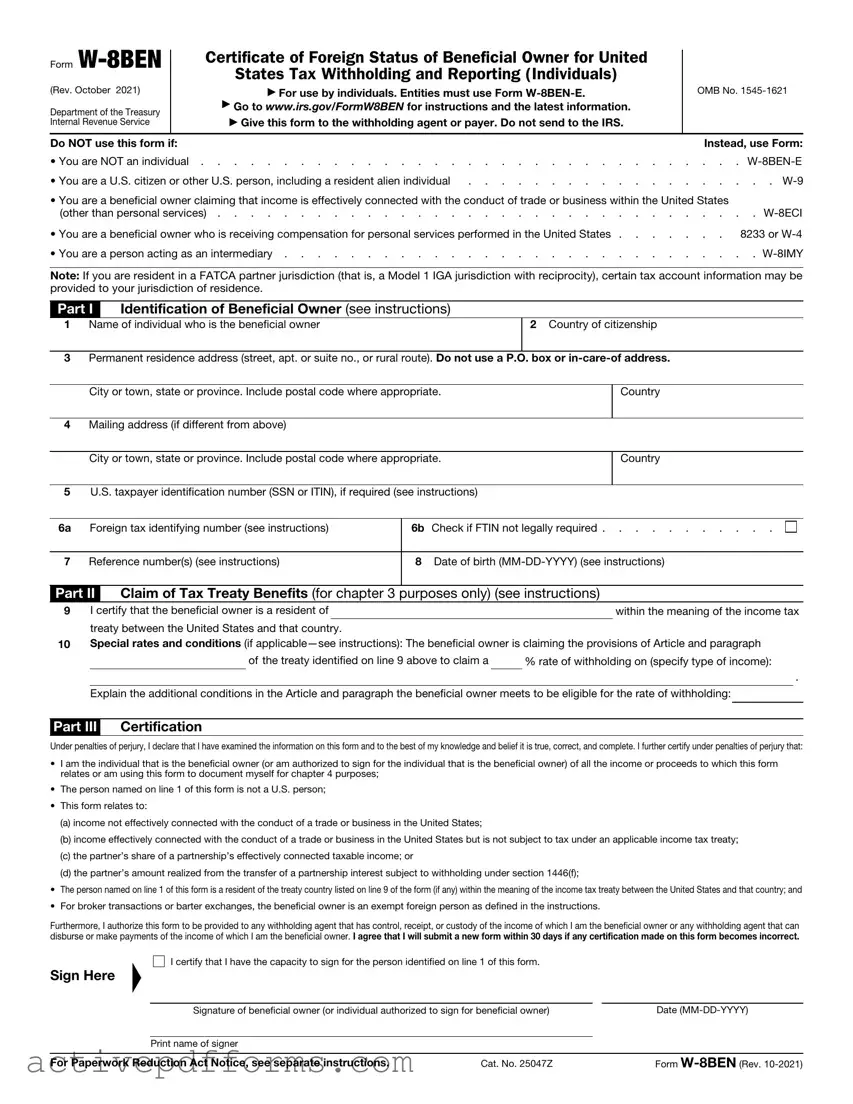

Part I Identification of Beneficial Owner (see instructions)

1Name of individual who is the beneficial owner

2Country of citizenship

3Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box or

City or town, state or province. Include postal code where appropriate.

Country

4Mailing address (if different from above)

City or town, state or province. Include postal code where appropriate.

Country

5U.S. taxpayer identification number (SSN or ITIN), if required (see instructions)

6a Foreign tax identifying number (see instructions) |

6b Check if FTIN not legally required |

|

|

7 Reference number(s) (see instructions) |

8 Date of birth |

Part II Claim of Tax Treaty Benefits (for chapter 3 purposes only) (see instructions)

9 I certify that the beneficial owner is a resident of treaty between the United States and that country.

10Special rates and conditions (if

of the treaty identified on line 9 above to claim a |

% rate of withholding on (specify type of income): |

.

Explain the additional conditions in the Article and paragraph the beneficial owner meets to be eligible for the rate of withholding:

Part III Certification

Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that:

•I am the individual that is the beneficial owner (or am authorized to sign for the individual that is the beneficial owner) of all the income or proceeds to which this form relates or am using this form to document myself for chapter 4 purposes;

•The person named on line 1 of this form is not a U.S. person;

•This form relates to:

(a)income not effectively connected with the conduct of a trade or business in the United States;

(b)income effectively connected with the conduct of a trade or business in the United States but is not subject to tax under an applicable income tax treaty;

(c)the partner’s share of a partnership’s effectively connected taxable income; or

(d)the partner’s amount realized from the transfer of a partnership interest subject to withholding under section 1446(f);

•The person named on line 1 of this form is a resident of the treaty country listed on line 9 of the form (if any) within the meaning of the income tax treaty between the United States and that country; and

•For broker transactions or barter exchanges, the beneficial owner is an exempt foreign person as defined in the instructions.

Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner. I agree that I will submit a new form within 30 days if any certification made on this form becomes incorrect.

Sign Here

▲

I certify that I have the capacity to sign for the person identified on line 1 of this form.

|

Signature of beneficial owner (or individual authorized to sign for beneficial owner) |

|

Date |

|

|

|

|

|

|

|

Print name of signer |

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 25047Z |

|

Form |

|

| Fact Number | Description |

|---|---|

| 1 | The IRS W-8BEN form is officially titled "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)." |

| 2 | It is used by individuals who are not U.S. citizens or resident aliens to certify their foreign status regarding tax withholding from U.S. income sources. |

| 3 | The purpose of the form is to inform U.S. payers that the foreign individual is exempt from certain U.S. information return reporting and backup withholding regulations. |

| 4 | W-8BEN forms must be submitted directly to the withholding agent, payer, or financial institution that requested it. They are not filed with the IRS. |

| 5 | Filing the form allows eligible individuals to claim a reduced rate of, or exemption from, withholding as permitted by an applicable income tax treaty between the United States and a foreign country. |

| 6 | The form is valid for the year in which it is signed and for the next three calendar years unless a change in circumstances makes any information on the form incorrect. |

| 7 | Foreign individuals must submit a new Form W-8BEN when their personal or tax status changes in a way that affects the accuracy of the form. |

| 8 | Failure to provide a valid W-8BEN when required may result in 30% withholding on applicable U.S. source income, or the withholding tax rate applicable under U.S. tax law or income tax treaty. |

| 9 | The form requires typical information such as the individual's name, country of citizenship, address, and tax identification number (TIN), among other things. |

Filling out the IRS W-8BEN form is a straightforward process, but it's vital to complete it accurately to ensure that you're taxed correctly on income from U.S. sources if you're a non-resident alien or a foreign entity. This form is crucial for individuals who conduct business or have certain financial interactions in the United States but are not U.S. citizens or residents. Let's walk through the steps to fill it out properly.

Once you've completed the form, review it carefully to ensure all information is accurate and complete. Incorrect or incomplete forms can lead to unnecessary withholding or delays. After reviewing, submit the form to the requesting entity, not the IRS. This might be a financial institution, an employer, or another party that needs to determine your tax status in the U.S. Keep a copy of the completed form for your records. Remember, the W-8BEN form does not need to be sent directly to the IRS but should be made available upon request.

What is the IRS W-8BEN form and who needs to fill it out?

The IRS W-8BEN form, officially titled "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)", is a document that foreign individuals must complete to certify their non-U.S. residency status. This certification helps in claiming tax treaty benefits, including reduced rates of withholding tax, on income tied to the U.S. It's necessary for individuals who receive certain types of income from U.S. sources, such as interest, dividends, rents, or royalties, but who are not U.S. citizens or residents.

Why is it important to complete the W-8BEN form?

Completing the W-8BEN form is crucial because it helps foreign individuals to establish their eligibility for lower withholding tax rates under tax treaties between the U.S. and their country of residence. Without this form, U.S. payers have to withhold taxes at the maximum rate. It also serves to confirm that the income is not connected with a U.S. trade or business, exempting it from certain taxes.

How often should the W-8BEN form be updated or renewed?

The W-8BEN form is valid for the year in which it's signed and for the next three calendar years. It means that it generally should be renewed every three years to ensure that the information and claims of tax treaty benefits remain accurate and up to date. However, if any of the information provided on the form changes (for example, the individual's address or tax residency status), a new W-8BEN form must be submitted to reflect these changes.

Are there any penalties for not completing the W-8BEN form?

Yes, there can be penalties for failing to complete the W-8BEN form. Individuals may face a 30% withholding on their U.S.-source income if the form is not provided, because the payer will have to withhold taxes at the highest rate. Moreover, inaccuracies or false statements on the form can lead to penalties, including fines and legal consequences.

What information is needed to fill out the W-8BEN form?

To properly complete the W-8BEN form, you need to provide your name and country of citizenship as they appear on your passport, your address in the foreign country where you claim tax residency, your U.S. taxpayer identification number (TIN) if you have one (if not, your foreign TIN), and the details of the beneficial owner if you are completing the form on someone else’s behalf. Also, you should clearly state the tax treaty country and the article number under which you claim treaty benefits.

Can the W-8BEN form be submitted electronically?

Yes, the W-8BEN form can often be submitted electronically, depending on the payer's processes. Many financial institutions, brokers, and other entities that require this form offer online submission options. This can make it easier and faster to comply with the U.S. tax requirements. However, it’s important to ensure that any electronic submission meets the IRS guidelines for electronic signatures.

Is there a W-8BEN form for entities, or is it only for individuals?

The W-8BEN form is specifically designed for individuals. Entities, such as corporations or partnerships, must use the Form W-8BEN-E, which is a separate document tailored for the needs of foreign entities. This version of the form collects information about the entity’s status and eligibility under tax treaties, similar to the individual form, but with fields relevant to entities.

Where can one find help for filling out the W-8BEN form?

For assistance with the W-8BEN form, individuals can refer to the IRS website for detailed instructions. Additionally, consulting a tax professional who is familiar with international tax laws and treaties can be particularly helpful. Some payers, such as financial institutions and investment firms, also offer guidance and resources to help foreign individuals and entities fill out the form correctly.

When individuals fill out the IRS W-8BEN form, a document primarily used by foreign entities to claim tax treaty benefits, several common mistakes can lead to processing delays or incorrect withholding taxes. Avoiding these mistakes is crucial for ensuring compliance with U.S. tax law.

Failing to use the proper form version. The IRS periodically updates forms, including the W-8BEN, to reflect current tax regulations. Using an outdated form can invalidate the submission.

Entering incorrect personal information. It is essential to provide accurate information, such as the individual's name, country of citizenship, and address. Mismatches between the form and official documents can cause issues.

Omitting required fields. Every question on the form serves a purpose. Leaving a mandatory field blank, especially those related to tax treaty claims or foreign tax identifying number (FTIN), can result in the form being rejected.

Not properly indicating tax treaty benefits. The W-8BEN allows foreign entities to claim reduced withholding tax rates under tax treaties between their country and the U.S. Incorrectly stating the treaty or failing to adequately justify the claim can lead to the standard withholding rate being applied.

Forgetting to sign and date the form. An unsigned or undated W-8BEN form is not valid. The IRS considers these forms incomplete, and as a result, tax withholding may be processed at the maximum rate.

To ensure the W-8BEN form is filled out correctly, individuals should carefully review the IRS instructions, double-check their answers, and consider consulting with a tax professional if they have questions or concerns about their specific situation.

When engaging in financial activities within the United States, foreign individuals and entities often use the IRS W-8BEN form to certify their foreign status and claim benefits under a tax treaty. This form is just one piece of the larger compliance puzzle. Alongside the W-8BEN, there are several other documents and forms that are frequently utilized to ensure proper reporting and compliance with U.S. tax laws. Understanding these forms can provide a clearer picture of the regulatory environment for foreign investors and individuals.

These documents collectively help in navigating the complex landscape of U.S. taxation for foreign nationals and entities. Whether it's declaring the status to avoid unnecessary taxation or claiming benefits under a treaty, each form has a specific role in the financial and regulatory framework of international commerce and investment in the United States.

The IRS W-8BEN form is a critical document for non-U.S. residents, detailing their status to avoid or reduce tax withholding from U.S. income. However, it's not the only form of its kind. Here are seven other documents bearing a resemblance in purpose and utility:

Each of these documents serves a unique role in the tapestry of IRS documentation required for non-U.S. citizens and foreign entities. Understanding which form to use in specific situations is crucial for ensuring compliance with U.S. tax laws and securing the most favorable tax treatment available under various international agreements and domestic regulations.

The IRS W-8BEN form is important for non-U.S. persons to accurately claim tax treaty benefits and report income related to the United States. Filling it out properly ensures compliance with U.S. tax law and can prevent unnecessary withholding. Here are some key dos and don'ts to remember when completing the form.

It's common for individuals and businesses to navigate the intricacies of tax obligations, particularly when it comes to international dealings. The IRS W-8BEN form plays a crucial role here, but myths and misunderstandings about it abound. Let's demystify some of these common misconceptions.

Understanding the IRS W-8BEN form is essential for non-U.S. persons engaging in any kind of financial activity that generates U.S.-sourced income. Clearing up these misconceptions can pave the way for proper compliance and potentially beneficial tax treatments.

The IRS W-8BEN form, officially titled "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)," is a crucial document for non-U.S. residents who receive certain types of income from U.S. sources. Understanding how to properly fill out and use this form is important to ensure compliance with U.S. tax laws and to potentially reduce withholding taxes on this income. Here are eight key takeaways about the W-8BEN form:

Properly understanding and completing the W-8BEN form can significantly impact an individual's tax liabilities and compliance with U.S. tax regulations. Therefore, it's advisable for non-U.S. residents who have U.S. source income to familiarize themselves with this form and, if necessary, seek professional guidance to ensure correct compliance.

Nc 242 - Contributes to a more transparent, fair, and just tax system in North Carolina.

I Hereby Certify in Resume - This document is proof of the writer’s business involvement and professional readiness, articulated for an audience like the Fire Department and notarized for formality.