Free Loan Estimate PDF Template

Free Loan Estimate PDF Template

When navigating the path to homeownership, one of the most critical steps involves understanding the Loan Estimate form. This comprehensive document, provided by lenders soon after you apply for a loan, serves as a blueprint of the proposed terms. It includes the address and details of the lending institution, the property in question, and crucial figures such as the loan amount, interest rate, and whether the rate is locked. With a breakdown of the loan term, purpose, and product type, the form also dives into the specifics of projected payments, detailing what the homeowner is expected to pay over the course of the loan. Beyond the numbers, it informs borrowers about potential prepayment penalties and balloon payments, indicating the flexibility and future financial implications of the loan. It meticulously lists closing costs, dividing them into origination charges, services you can and cannot shop for, and other costs, ensuring a clear picture of upfront expenses. Further, it outlines the estimated cash to close, incorporating down payments and seller credits. Additional information covers lender details, comparisons to other loans, and other considerations like appraisal requirements and late payment fees, providing an essential tool for consumers to compare offers and make informed decisions about their future home.

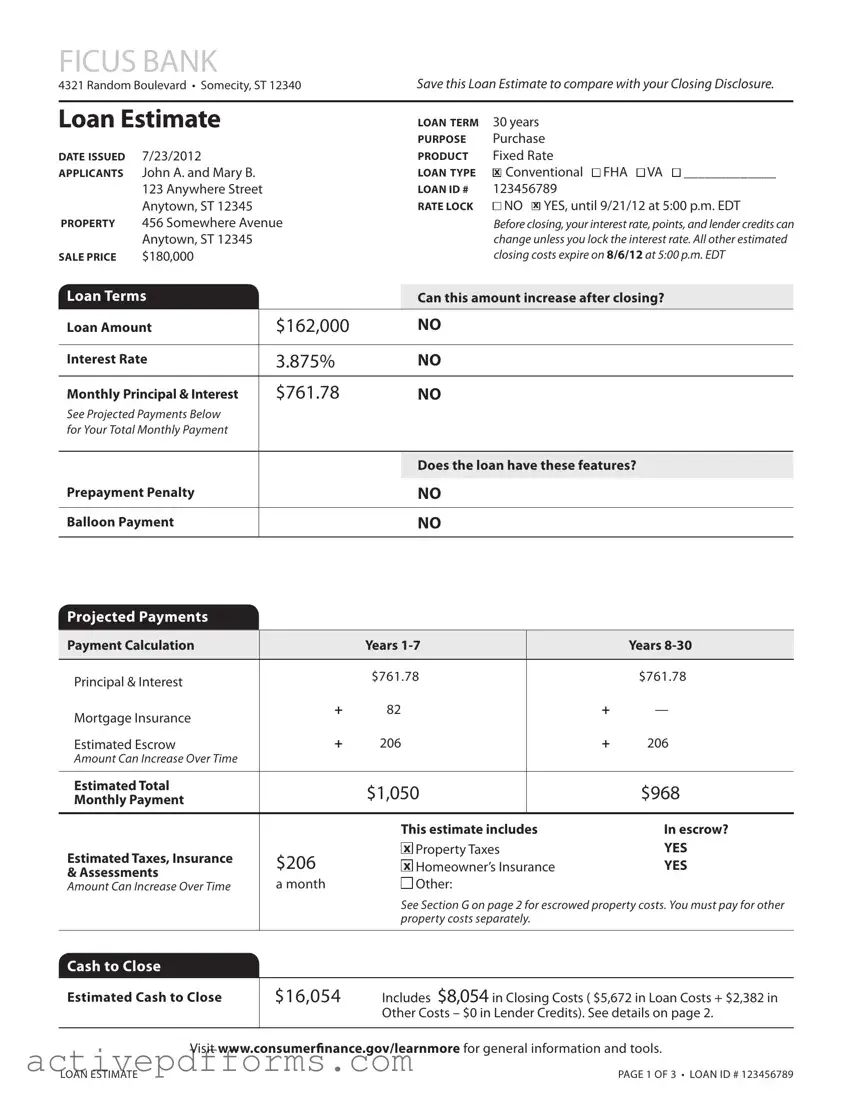

FICUS BANK

4321 Random Boulevard • Somecity, ST 12340Save this Loan Estimate to compare with your Closing Disclosure.

Loan estimate |

LOAN TeRM |

30 years |

|

|

|

PuRPOse |

Purchase |

DATe IssueD |

7/23/2012 |

PRODuCT |

Fixed Rate |

APPLICANTs |

John A. and Mary B. |

LOAN TyPe |

x Conventional FHA VA _____________ |

|

123 Anywhere Street |

LOAN ID # |

123456789 |

|

Anytown, ST 12345 |

RATe LOCK |

NO x YES, until 9/21/12 at 5:00 p.m. EDT |

PROPeRTy |

456 Somewhere Avenue |

|

Before closing, your interest rate, points, and lender credits can |

|

Anytown, ST 12345 |

|

change unless you lock the interest rate. All other estimated |

sALe PRICe |

$180,000 |

|

closing costs expire on 8/6/12 at 5:00 p.m. EDT |

Loan Terms |

|

Can this amount increase after closing? |

Loan Amount |

$162,000 |

NO |

|

|

|

Interest Rate |

3.875% |

NO |

|

|

|

Monthly Principal & Interest |

$761.78 |

NO |

See Projected Payments Below |

|

|

for Your Total Monthly Payment |

|

|

|

|

|

|

|

Does the loan have these features? |

Prepayment Penalty |

|

|

|

NO |

|

|

|

|

Balloon Payment |

|

NO |

|

|

|

Projected Payments

Payment Calculation |

|

years |

|

|

years |

|

|

|

|

|

|

Principal & Interest |

|

$761.78 |

|

|

$761.78 |

|

|

|

|

|

|

Mortgage Insurance |

+ |

82 |

|

+ |

— |

|

|

|

|

|

|

Estimated Escrow |

+ |

206 |

|

+ |

206 |

Amount Can Increase Over Time |

|

|

|

|

|

|

|

|

|

|

|

estimated Total |

|

$1,050 |

|

|

$968 |

Monthly Payment |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This estimate includes |

|

In escrow? |

|

estimated Taxes, Insurance |

$206 |

x Property Taxes |

|

yes |

|

x Homeowner’s Insurance |

|

yes |

|||

& Assessments |

|

||||

a month |

Other: |

|

|

||

Amount Can Increase Over Time |

|

|

|||

|

|

See Section G on page 2 for escrowed property costs. You must pay for other |

|||

|

|

property costs separately. |

|

|

|

|

|

|

|

|

|

Cash to Close |

|

|

|

|

|

|

|

|

|

||

estimated Cash to Close |

$16,054 |

Includes $8,054 in Closing Costs ( $5,672 in Loan Costs + $2,382 in |

|||

|

|

Other Costs – $0 in Lender Credits). See details on page 2. |

|||

|

|

|

|

|

|

Visit www.consumerinance.gov/learnmore for general information and tools.

LOAN ESTIMATE |

page 1 of 3 • Loan ID # 123456789 |

Closing Cost Details

Loan Costs

A. Origination Charges |

$1,802 |

.25 % of Loan Amount (Points) |

$405 |

Application Fee |

$300 |

Underwriting Fee |

$1,097 |

Other Costs

e. Taxes and Other Government Fees |

$85 |

||||||

Recording Fees and Other Taxes |

|

|

$85 |

||||

Transfer Taxes |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

F. Prepaids |

|

|

$867 |

||||

Homeowner’s Insurance Premium ( |

6 months) |

$605 |

|||||

|

|

|

|

|

|

|

|

Mortgage Insurance Premium ( 0 |

months) |

$0 |

|||||

|

|

|

|

|

|

||

Prepaid Interest ( $17.44 per day for 15 days @ 3.875%) |

$262 |

||||||

Property Taxes ( 0 months) |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

B. services you Cannot shop For |

$672 |

Appraisal Fee |

$405 |

Credit Report Fee |

$30 |

Flood Determination Fee |

$20 |

Flood Monitoring Fee |

$32 |

Tax Monitoring Fee |

$75 |

Tax Status Research Fee |

$110 |

G. Initial escrow Payment at Closing |

|

|

$413 |

|

Homeowner’s Insurance |

$100.83 per month for |

23mo. $202 |

||

Mortgage Insurance |

per month for |

0 |

mo. |

|

Property Taxes |

$105.30 per month for |

2 |

mo. |

$211 |

H. Other |

$1,017 |

Title – Owner’s Title Policy (optional) |

$1,017 |

C. services you Can shop For |

$3,198 |

Pest Inspection Fee |

$135 |

Survey Fee |

$65 |

Title – Insurance Binder |

$700 |

Title – Lender’s Title Policy |

$535 |

Title – Title Search |

$1,261 |

Title – Settlement Agent Fee |

$502 |

D. TOTAL LOAN COsTs (A + B + C) |

$5,672 |

I. TOTAL OTHeR COsTs (e + F + G + H) |

$2,382 |

|

|

J. TOTAL CLOsING COsTs |

$8,054 |

|

|

D + I |

$8,054 |

Lender Credits |

$0 |

Calculating Cash to Close |

|

|

|

Total Closing Costs (J) |

$8,054 |

Closing Costs Financed (Included in Loan Amount) |

$0 |

Down Payment/Funds from Borrower |

$18,000 |

Deposit |

– $10,000 |

Funds for Borrower |

$0 |

Seller Credits |

$0 |

Adjustments and Other Credits |

$0 |

estimated Cash to Close |

$16,054 |

|

|

LOAN ESTIMATE |

page 2 of 3 • Loan ID # 123456789 |

Additional Information About This Loan

LeNDeR NMLs/LICeNse ID

LOAN OFFICeR

NMLs ID

PHONe

Ficus Bank

Joe Smith 12345 joesmith@icusbank.com

MORTGAGe BROKeR NMLs/LICeNse ID LOAN OFFICeR NMLs ID

eMAIL PHONe

Comparisons |

use these measures to compare this loan with other loans. |

||

|

|

|

|

In 5 years |

$56,582 |

Total you will have paid in principal, interest, mortgage insurance, and loan costs. |

|

$15,773 |

Principal you will have paid of. |

||

|

|||

|

|

|

|

Annual Percentage Rate (APR) |

4.494% |

Your costs over the loan term expressed as a rate. This is not your interest rate. |

|

|

|

|

|

Total Interest Percentage (TIP) |

69.447% |

The total amount of interest that you will pay over the loan term as a |

|

|

|

percentage of your loan amount. |

|

|

|

|

|

Other Considerations

Appraisal |

We may order an appraisal to determine the property’s value and charge you for this |

|

appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. |

|

You can pay for an additional appraisal for your own use at your own cost. |

Assumption |

If you sell or transfer this property to another person, we |

|

will allow, under certain conditions, this person to assume this loan on the original terms. |

|

x will not allow this person to assume this loan on the original terms. |

Homeowner’s |

This loan requires homeowner’s insurance on the property, which you may obtain from a |

Insurance |

company of your choice that we ind acceptable. |

Late Payment |

If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly |

|

principal and interest payment. |

Reinance |

Reinancing this loan will depend on your future inancial situation, the property value, and |

|

market conditions. You may not be able to reinance this loan. |

servicing |

We intend |

|

to service your loan. If so, you will make your payments to us. |

|

x to transfer servicing of your loan. |

Conirm Receipt

By signing, you are only conirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature |

Date |

Date |

LOAN ESTIMATE |

page 3 of 3 • Loan ID #123456789 |

| Fact Name | Description |

|---|---|

| Document Purpose | Provides an estimate of loan costs to help consumers compare offers. |

| Issuing Bank | Ficus Bank |

| Loan Term | 30 years |

| Product Type | Fixed Rate |

| Loan Type | Conventional |

| Interest Rate Lock | Yes, until 9/21/12 at 5:00 p.m. EDT |

| Included Costs | Origination charges, service fees, prepaids, initial escrow payment. |

| Loan Costs | Total loan costs amount to $5,672. |

| Other Costs | Total other costs amount to $2,382. |

| Cash to Close | Estimated cash to close is $16,054. |

After receiving the Loan Estimate form, it’s crucial for applicants to carefully review each section to ensure all details are correct and fully understood. This document is foundational for understanding the terms of the loan, including interest rates, monthly payments, and closing costs. To avoid surprises at closing, each applicant should use this opportunity to compare these terms with any other offers and to interrogate details that may affect the long-term affordability of the loan. Here's a step-by-step guide to filling out the Loan Estimate form efficiently and accurately.

Understanding each segment of the Loan Estimate form is crucial for making informed decisions throughout the home buying process. After thorough review and discussion with your lender regarding any aspects of the form, the next steps involve moving towards finalizing the loan details, preparing for the closing process, and, ultimately, closing on your new home. Keep this document for your records and as a comparison tool for your Closing Disclosure to ensure consistency in terms of and fees.

Here are some of the most common questions about the Loan Estimate form:

A Loan Estimate is a three-page document that you receive after applying for a mortgage. It provides detailed information about the loan you've applied for. This includes the estimated interest rate, monthly payments, and costs associated with the mortgage, like closing costs. The form is designed to help you understand the terms of the loan and compare offers from different lenders.

Lenders are required to provide you with your Loan Estimate within three business days of receiving your mortgage application. This timeframe allows you to quickly assess your loan terms and costs and compare them with other options. If you don't receive it within this period, it's a good idea to contact your lender for an update.

Yes, certain aspects of your Loan Estimate can change before your loan closes. For example, if you decide to lock in your interest rate after receiving the Loan Estimate, this will alter your initial estimate. Other costs, like closing costs, can also change due to changes in the real estate transaction or if the lender finds inaccuracies in the initial application. However, the lender must provide an updated Loan Estimate if significant changes occur.

The Loan Estimate form is designed to standardize the information provided by lenders, making it easier for you to compare different loans. Look closely at the interest rate, monthly payment, and both the upfront and long-term costs of each loan. Don't forget to consider whether the rate is fixed or adjustable. The "Comparisons" section on the second page can be particularly helpful, as it shows how much you will have paid after five years and the APR, which reflects the cost of your loan as an annual rate.

Not checking or incorrectly marking the loan type. It's crucial to correctly select whether it's a Conventional, FHA, or VA loan, as this affects loan terms and eligibility.

Forgetting to verify the rate lock. If "YES" is not marked when the rate is locked, or the information is inaccurate, there could be unexpected changes in the interest rate.

Overlooking to fill in the estimated property value or sale price. This can significantly impact the accuracy of loan terms and the amount of funding needed.

Miscalculating the estimated cash to close. This includes not accounting for all the closing costs correctly, leading to surprises at the closing table.

Misunderstanding the "Projected Payments" section by not accurately considering how the monthly payment can change over time, especially in relation to escrow costs and insurance.

Incorrectly filling in personal information or loan ID numbers. This can lead to processing delays or the application getting associated with the wrong loan profile.

Not reviewing the "Other Considerations" and "Additional Information" sections carefully. This area contains essential information about loan servicing, appraisals, and insurance requirements that are often overlooked.

When you're navigating the path to securing a mortgage, the Loan Estimate form is just the beginning. This document provides a detailed breakdown of your potential loan's terms, costs, and other important information. However, to fully understand and complete the mortgage process, several other documents also come into play. Here's a look at four of them:

Understanding these documents can make the mortgage process less daunting and help ensure you're well-informed every step of the way. Each document plays a crucial role in defining the terms of your loan, your rights as a borrower, and the responsibilities you have. It's important to review these documents carefully and ask questions if anything is unclear, ensuring a smooth path to securing your new home.

The Closing Disclosure form is intricately connected to the Loan Estimate form, primarily because both aim to provide clear and concise financial details concerning a mortgage. The Closing Disclosure, issued closer to the finalization of the loan process, offers a detailed account of the finalized fees, interest rates, and other costs associated with the mortgage loan, ultimately serving as a final review document that directly compares to the preliminary estimates provided in the Loan Estimate form.

Good Faith Estimate (GFE) previously served a similar purpose to the Loan Estimate form before the implementation of the TILA-RESPA Integrated Disclosure (TRID) rule. The GFE outlined estimated costs one might incur during the loan process. Although the Loan Estimate form has replaced the GFE for most types of loans, their objectives align closely in offering borrowers a clear, upfront snapshot of their potential loan costs.

The Truth in Lending Act (TILA) disclosure closely mirrors the Loan Estimate in its mission to inform borrowers about the key terms of a credit offer, including the annual percentage rate (APR), total cost of the loan, and payment schedule. Where the Loan Estimate form consolidates and simplifies this information, the TILA disclosure traditionally provided it in a more detailed format.

Mortgage Servicing Disclosure Statement complements the information found on the Loan Estimate form by informing the borrower about the entity that will be servicing their loan, indicating whether the servicing may be transferred to another lender or servicing company. This document expands on the servicing disclosure provided in the Loan Estimate form.

The Appraisal Disclosure offers information similar to that found in a section of the Loan Estimate form detailing the borrower's rights regarding receiving a copy of the property appraisal. Both documents underscore the importance of the appraisal in the mortgage lending process and ensure borrowers are informed about the valuation of their property.

HUD-1 Settlement Statement served a role analogous to both the Loan Estimate and the Closing Disclosure forms before the latter two were introduced. Providing detailed information on all charges to the borrower and seller as part of the settlement process, the HUD-1's relevance has been mostly superseded but its function remains a precursor to modern disclosure requirements, ensuring clarity and transparency in closing costs.

The Initial Escrow Statement provides detailed information on the expected costs to be paid from the escrow account during the first year of the loan, including insurance and taxes, similar to the escrow information disclosed on the Loan Estimate form. This statement builds on the preliminary estimates by offering a detailed projection of escrow expenses.

When filling out the Loan Estimate form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Here are things you should and shouldn't do:

Paying close attention to these details will help in accurately completing the Loan Estimate form, setting a clear expectation of loan terms and closing costs.

Understanding the Loan Estimate form can often involve navigating through various misconceptions. Here are nine common misunderstandings clarified to help borrowers accurately interpret this important document.

Misconception 1: The Loan Estimate is a binding agreement. In reality, the Loan Estimate is not a commitment from the lender to provide a loan. Rather, it provides detailed estimates of the loan terms, projected payments, and closing costs to help consumers compare offers.

Misconception 2: The interest rate is guaranteed once you receive the Loan Estimate. The truth is that interest rates can still change unless you have locked in your rate with the lender. Rate locks typically come with a specific expiration date and time.

Misconception 3: The Loan Estimate shows the final costs of the mortgage. Although it provides a comprehensive overview of estimated costs, the actual closing costs may differ. Changes can occur due to factors such as changes in the loan amount or adjustments in property taxes.

Misconception 4: All potential borrowers receive the same Loan Estimate format. Though standardized, the Loan Estimate's details are customized based on the specific loan product, terms, and costs applicable to the individual applicant's situation.

Misconception 5: The Loan Estimate includes all costs associated with purchasing a home. The document provides details about loan-related expenses and estimated closing costs. However, it may not account for all expenses, such as certain inspections or homeowner association fees, unless specifically noted.

Misconception 6: You must accept the loan once you sign and return the Loan Estimate. Signing the Loan Estimate is simply an acknowledgment of receipt. It does not bind the applicant to proceed with the loan from that lender.

Misconception 7: The cash to close amount is non-negotiable. The 'estimated cash to close' figure is an estimate. This amount can often be negotiated or amended, especially as buyers negotiate seller credits or make adjustments to the down payment.

Misconception 8: The Loan Estimate only matters if you're a first-time homebuyer. This document is crucial for all borrowers, regardless of their experience with purchasing property. It provides essential information that impacts the overall cost of a loan over time.

Misconception 9: You should only focus on the monthly mortgage payment. While the monthly payment is a critical factor, it's equally important to consider other details listed, such as the APR, total interest percentage (TIP), and cash to close, which reflect the loan's overall affordability and cost.

By understanding these aspects of the Loan Estimate, borrowers can make more informed decisions and feel confident when navigating the mortgage process.

Filling out and using the Loan Estimate form is a crucial step in understanding the costs involved with obtaining a mortgage. Here are five key takeaways:

Ultimately, the Loan Estimate form is designed to provide transparency and help borrowers make informed decisions about their mortgage options.

Printable Truck Driver Employment Application Template Word - A requirement for emergency contact information ensures quick communication in case of an emergency.

Advanced Beneficiary Notice - In the context of managed healthcare, the ABN form plays a pivotal role in informing Medicare beneficiaries about their financial responsibilities for services not covered, preempting surprise billing issues.

Apartment Information Sheet - Define your ideal apartment experience, from the price range to move-in date, to streamline your search.