Free Mortgage Statement PDF Template

Free Mortgage Statement PDF Template

Navigating through the complexities of managing a mortgage can at times feel overwhelming, but understanding your Mortgage Statement is key to maintaining control over this significant financial commitment. At its core, this document, furnished by your loan servicer, provides a comprehensive overview of your mortgage account. It includes crucial details such as the servicer’s name, contact information, and website, alongside your own name and address. Importantly, it outlines the statement date, account number, the due date for your next payment, and the amount due. Further breakdowns include an explanation of the amount due—dividing it into principal, interest, and any escrow amounts for taxes and insurance. Additionally, crucial information about late fees, the outstanding principal, and interest rate until a certain date, alongside any prepayment penalty, is clearly detailed. The statement also records transaction activity within a specified period, detailing charges, payments, and any late fees applied. It offers a glimpse into your payment history, breaking down past payments into principal, interest, escrow, and fees. The final sections highlight any important messages, delinquency notices, and vital information about partial payments, emphasizing the consequences of not staying current with payments. Understanding each segment of this statement is integral for homeowners to stay informed about their mortgage’s status, manage their finances effectively, and avoid potential pitfalls such as foreclosure.

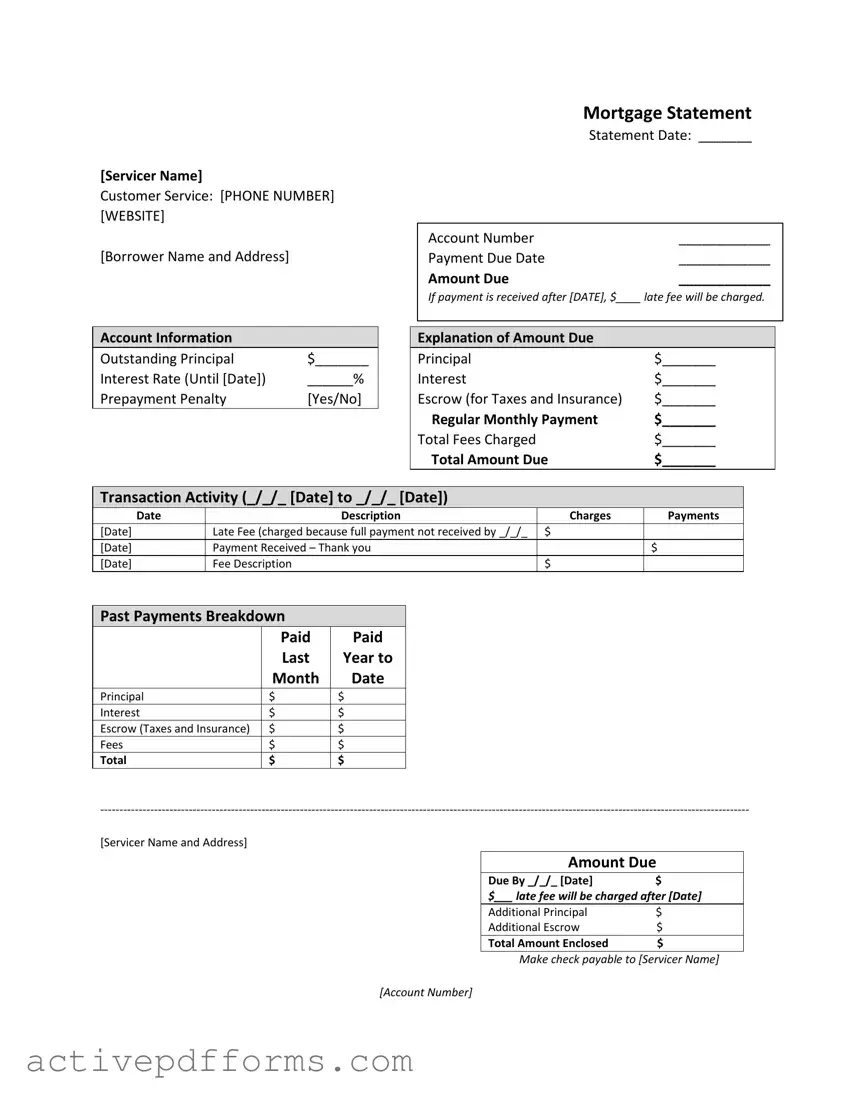

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact Name | Description |

|---|---|

| Statement Overview | This section includes the servicer’s name, contact information, borrower's name and address, statement date, account number, payment due date, and the total amount due. It is designed to give the borrower a quick snapshot of the most crucial information regarding their mortgage. |

| Payment Information | Details the amount due, breaking it down into principal, interest, and escrow amounts. It also states the late fee amount and its applicable conditions, providing clear expectations around the financial obligations by the due date. |

| Account Activity | Records detailed transactions within a specific period, including dates, descriptions of transaction activity (such as payments received and fees charged), and amounts. This section aims to track financial movements and keep the borrower informed of any charges or credits to their account. |

| Payment Breakdown and History | Offers a comparison of payments made in the current year against the previous year, detailing how much has been paid towards principal, interest, escrow, and fees. This historical perspective helps borrowers understand their payment progress over time. |

| Important Messages and Notices | Communicates critical information regarding the handling of partial payments, delinquency notices, recent account activity, and guidance for borrowers experiencing financial difficulties. This section often includes legal notices and resources for borrower assistance. |

Filling out a mortgage statement form accurately is essential for keeping your account up to date and avoiding any unnecessary fees. The process ensures that all transactions and payment details between the borrower and the lender are recorded methodically. This step-by-step guide aims to simplify the completion of the mortgage statement form, making it accessible for homeowners to maintain their mortgage account efficiently.

Upon completing the form, ensure all the information provided is accurate and reflective of your current mortgage account status. It is advisable to retain a copy for your records before submission. Timely and accurate completion of your mortgage statement form can aid in preventing misunderstandings, ensuring that your mortgage payments are recorded accurately, and helping you to maintain good standing with your loan servicer.

What is a Mortgage Statement and what information does it contain?

A Mortgage Statement is a document provided by your mortgage servicer that gives you an overview of your current mortgage status. It includes your servicer's name and contact information, your name and address, the statement date, your account number, and payment due date. The amount due, including if there's a late fee for payments received after a certain date, is clearly stated. It breaks down your outstanding principal, interest rate, whether there is a prepayment penalty, and explains the components of your amount due such as principal, interest, escrow (for taxes and insurance), regular monthly payments, total fees charged, and the total amount due. The statement also records transaction activity, like late fees charged and payments received, and provides a breakdown of past payments. Furthermore, it offers details on how to make your payment, any additional amounts due for principal or escrow, and important messages regarding partial payments and delinquency notices.

What happens if I make a partial payment on my mortgage?

When you make a partial payment, the funds are not immediately applied to your mortgage. Instead, they are held in a separate account known as a suspense account. These funds will stay in the suspense account until you pay the balance of the partial payment. Once the full payment is made, the funds will be applied to your mortgage. This policy ensures that payments are accounted for accurately but also emphasizes the importance of making full payments to avoid complications.

What are the consequences of late payments on my mortgage?

If your mortgage payment is received after the specified due date, a late fee will be charged. Continuously late payments may lead to more severe consequences, including the risk of falling into delinquency. The statement includes a delinquency notice, warning borrowers that failure to bring the loan current could result in fees and possible foreclosure—the loss of your home. It specifies how many days you are delinquent and the total amount due to bring your loan current. Making timely payments is crucial to avoid these risks and maintain good standing on your mortgage.

What should I do if I am experiencing financial difficulty and cannot make my mortgage payments?

If you find yourself in a tough financial situation and are unable to make mortgage payments, it's important to act promptly. The mortgage statement advises borrowers to refer to the back of the statement for information about mortgage counseling or assistance programs. These resources can offer guidance and potentially offer solutions to help manage your mortgage payments better. Seeking help as soon as you realize you might have difficulty paying your mortgage can prevent the situation from worsening and provide you with options to address payment issues.

When filling out a Mortgage Statement form, people often make several common mistakes that can impact their mortgage management. Being aware of these mistakes helps in ensuring that the mortgage process goes smoothly. Here are eight mistakes to avoid:

By avoiding these common mistakes, you can help ensure your mortgage management is as accurate and trouble-free as possible.

When dealing with mortgages, a multitude of documents and forms beyond the Mortgage Statement are commonly used to ensure clarity, legality, and the smooth functioning of the borrowing process. These documents serve various purposes such as ensuring the correct processing of payments, legally securing the mortgage, and providing protections to both the lender and the borrower. Below is a brief overview of some of these essential documents.

Each of these documents plays a crucial role in securing and maintaining a mortgage. They provide a framework for the terms of the loan, establish legal protections, and set out the responsibilities of each party involved in the property transaction. Understanding these documents is vital for anyone involved in the buying or selling of property, as well as for those seeking to secure a mortgage for their home.

Loan Amortization Schedule: This document is similar to the Mortgage Statement as it provides a breakdown of payments over the duration of the loan. It details how much of each payment is applied towards the principal versus interest, which mirrors the mortgage statement's section on the explanation of amount due.

Annual Escrow Statement: Like the Mortgage Statement, the Annual Escrow Statement outlines the amounts collected for and paid from the escrow account for taxes and insurance. It helps borrowers understand how their escrow payments are being used, analogous to how the mortgage statement includes escrow amounts.

Truth in Lending Disclosure: This document shares similarities with the Mortgage Statement through its presentation of the interest rate, though it primarily focuses on the initial terms at the outset of the loan. The Truth in Lending Disclosure offers detailed information on the cost of borrowing, similar to how the mortgage statement outlines ongoing costs.

Loan Estimate: The Loan Estimate document, provided early in the loan application process, forecasts the expected monthly payments, fees, and other loan costs, akin to the Mortgage Statement which details the current status of these aspects mid-loan. Both documents aim to give borrowers a clear understanding of their financial obligations.

Homeowners Insurance Declaration Page: This document, detailing the coverage and costs associated with a homeowner's insurance policy, bears resemblance to the parts of the Mortgage Statement discussing the escrow for taxes and insurance. It provides critical information about the protection of the borrower's property, akin to how the Mortgage Statement accounts for insurance within the escrow calculations.

Property Tax Statement: Similar to the Mortgage Statement, a Property Tax Statement offers an accounting of the property taxes due or paid on a property. When mortgage statements include escrowed tax amounts, they reflect some of the information found in a standalone Property Tax Statement.

Payment Coupon Book: Like Mortgage Statements, Payment Coupon Books are used to remind borrowers of their upcoming payment amounts and due dates. Both serve the purpose of guiding borrowers on when and how much to pay, ensuring the loan is kept current.

When filling out your Mortgage Statement Form, it's important to ensure that everything is correct to keep your mortgage account in good standing. Here is a list of things you should and shouldn't do:

What You Should Do:Understanding your mortgage statement is crucial to managing your home loan effectively. However, several misconceptions may lead to confusion and mismanagement of your finances. Below are ten common misconceptions about the Mortgage Statement form, explained in clear terms:

By debunking these misconceptions, borrowers can better understand their mortgage statements, making informed decisions about their home loans. Knowledge about the specifics of your mortgage statement can empower you to manage your loan more effectively, avoid unnecessary fees, and maintain good standing on your loan.

Understanding your Mortgage Statement form is crucial for managing your home loan effectively. Here are seven key takeaways that can help you navigate through it:

This detailed breakdown not only aids in maintaining current payments but also in planning for future financial decisions related to your mortgage.

Da - The DA Form 2062 is governed by directives found in DA PAM 710-2-1, with its procedural use specified by the Office of the Deputy Chief of Staff for Logistics (ODCSLOG).

Hunting Liability Waiver Template - It brings attention to the voluntary nature of entering into such agreements, emphasizing the lessee's conscious decision to accept risks for accessing the leased land.