Free Nc 242 PDF Template

Free Nc 242 PDF Template

The NC-242 form plays a fundamental role in the tax administration process in North Carolina, offering taxpayers a formal avenue to dispute proposed assessments, adjustments, or denials of refunds by the Department of Revenue. Designed for both individuals and entities, this form requires detailed personal and business information, including names, social security numbers, contact details, and specifics regarding the tax matter at hand. Crucially, it allows taxpayers to articulate their objections clearly and submit necessary documentation for review. The process stipulated by the NC-242 is time-sensitive, with a 45-day window post-notice to lodge an objection, emphasizing the importance of prompt and accurate submission. The form also outlines the requirement for a Power of Attorney if representation is involved, ensuring that taxpayers' rights are protected while they navigate through potential disputes with the Department of Revenue. This procedure not only underscores the taxpayer's responsibility to adhere to tax laws but also their right to question or appeal decisions deemed incorrect or unfair. Thus, the NC-242 form serves as a crucial tool within the tax administration system to ensure fairness, accuracy, and the reconciliation of disputes between taxpayers and the state's revenue department.

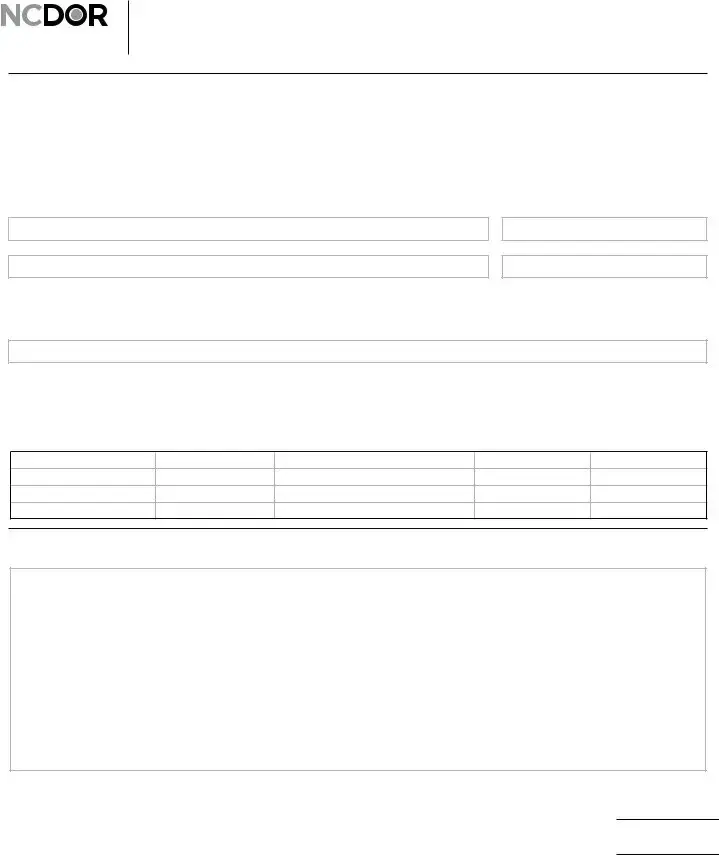

Objection and Request for Departmental Review

Individual’s First Name |

M.I. |

|

Individual’s Last Name |

|

Individual’s Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s First Name (If joint return filed) |

M.I. |

|

Spouse’s Last Name (If joint return filed) |

|

Spouse’s Social Security Number (If joint return filed) |

||

|

|

|

|

|

|

|

|

Individual Phone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Entity’s Legal Name

Entity’s Trade Name

Entity’s Federal Employer ID Number

Account Number/NCDOR ID

Entity Contact Person |

|

Entity Contact Person Phone Number |

|

|

|

|

|

|

|

|

|

Street Address

City |

|

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reason for Objection and Request for Departmental Review (Provide the requested information about the notice(s) that you are requesting the Department to review. Important: Attach a copy of the notice(s) of proposed assessment, proposed denial of refund, or proposed adjustment.)

Notice Number

Date of Notice

Tax Type

Period Beginning

Period Ending

Use the space below to state in detail your specific objections to the Notice of Proposed Assessment, Notice of Proposed Denial of Refund, or Notice of Proposed Adjustment. (Attach additional pages if necessary. Attach all supporting documentation to your request for Departmental review.)

Taxpayer Signature: |

|

Title: |

|

Date: |

|

Signature of |

|

|

|

||

Taxpayer’s Representative: |

|

|

|

Date: |

|

If a taxpayer’s representative signs this form, a Power of Attorney must accompany this request.

If you object to a proposed assessment, proposed adjustment, or proposed denial of refund, you must request a Departmental review of the proposed action as the first step in the appeals process. To request a review, complete this form and mail it, along with all supporting documentation, to the address shown below. This form may be used for any State or local tax administered by the Department of Revenue. The request for review must be filed with the Department within 45 days after the following: (1) the date the Notice of the Proposed Assessment, Proposed Denial of Refund, or Proposed Adjustment was mailed by the Department, or (2) the date the Notice of Proposed Assessment, Proposed Denial of Refund, or Proposed Adjustment was personally delivered by a Department employee.

MAIL TO: North Carolina Department of Revenue, Customer Interaction Center, P.O. Box 471, Raleigh, NC

| Fact Name | Description |

|---|---|

| Form Identifier | NC-242 |

| Title | Objection and Request for Departmental Review |

| Version | Web-Fill 5-20 |

| Purpose | To object to a proposed assessment, proposed adjustment, or proposed denial of refund by requesting a Departmental review. |

| Submission Requirement | Must be completed and mailed with all supporting documentation to the specified address within 45 days of the notice date. |

| Governing Law | Managed under North Carolina State tax laws and regulations. |

| Applicability | Applicable for individual and entity objections to any State or local tax administered by the Department of Revenue. |

| Key Sections | Individual and Spouse Information, Entity Information, Reason for Objection, Taxpayer/Representative Signature. |

| Additional Requirement | If represented by a taxpayer’s representative, a Power of Attorney must accompany the request. |

Filling out the NC-242 form is a critical step for individuals or entities who wish to object to a proposed tax assessment, proposed adjustment, or proposed denial of refund by the North Carolina Department of Revenue. It marks the beginning of the departmental review process, which is the first phase in challenging the decision made by the tax authority. This guide will walk you through each step to ensure your form is completed accurately and your objection is clearly communicated.

Remember, it is important to submit this form within 45 days after receiving the notice from the Department of Revenue. Promptly completing and sending the NC-242 form with all necessary documentation is crucial for having your objection considered. This form allows for the structured submission of your arguments against the proposed tax decision, serving as the foundational documentation for the review process.

What is Form NC-242 used for?

Form NC-242, known as the Objection and Request for Departmental Review, is a critical document used by individuals or entities to formally object to a proposed assessment, proposed adjustment, or proposed denial of refund by the North Carolina Department of Revenue (NCDOR). This form initiates the departmental review process, which is the first step in the appeals process if you disagree with the NCDOR's proposed action regarding your state or local taxes.

Who needs to fill out Form NC-242?

Any taxpayer, whether an individual or an entity, who objects to a notice of proposed assessment, proposed denial of refund, or notice of proposed adjustment received from the NCDOR, needs to fill out Form NC-242. This includes both individuals and entities who have disputes related to any state or local tax administered by the NCDOR.

What information is required on Form NC-242?

The form requires various pieces of information, including the individual or entity's name, social security number (for individuals), federal employer ID number (for entities), contact information, and the details of the objection. Specifically, you need to provide the notice number, the tax type in question, the period beginning and ending dates, and a detailed explanation of your objection(s). Attaching supporting documentation and a copy of the notice(s) being contested is also necessary.

What is the deadline for submitting Form NC-242?

The deadline for submitting Form NC-242 is within 45 days after either the date the notice (of proposed assessment, proposed denial of refund, or proposed adjustment) was mailed by the Department, or the date it was personally delivered by a Department employee. It's crucial to meet this deadline to ensure that your request for review is considered.

Where should Form NC-242 be sent?

Once completed, Form NC-242, along with all required documents and supporting evidence, should be mailed to the North Carolina Department of Revenue, Customer Interaction Center, P.O. Box 471, Raleigh, NC 27602-0471. This address is specifically designated for handling these objections and requests for departmental review.

Is a Power of Attorney required if someone else fills out or submits Form NC-242 on my behalf?

Yes, if a taxpayer’s representative fills out or submits Form NC-242 on behalf of the taxpayer, a Power of Attorney (POA) must accompany the request. This legal document grants the representative the authority to act on the taxpayer's behalf in matters related to the objection and request for departmental review process.

When filling out the NC-242 form, attention to detail is crucial. Small errors can lead to significant delays or even the rejection of your submission. Below are common mistakes people often make during this process:

By avoiding these mistakes, you can improve the chances of your NC-242 form being processed smoothly and efficiently.

When dealing with tax-related forms, the NC-242 form serves a crucial role for individuals and entities in North Carolina who wish to object to a proposed assessment, adjustment, or denial of refund by the Department of Revenue. However, in the process of filing objections or dealing with tax matters, various other forms and documents often come into play. Knowing what these documents are and understanding their purposes can be instrumental in navigating the process smoothly and efficiently.

Understanding these forms and their associated processes can offer a clear pathway through tax objections and amendments. Each document serves a unique but interconnected role in ensuring taxpayers can accurately and effectively communicate with the Department of Revenue, set the stage for a fair review of their case, and maintain compliance with state tax laws.

IRS Form 843 (Claim for Refund and Request for Abatement): Similar to the NC-242, IRS Form 843 is used for challenging tax assessments, requesting refunds, or asking for abatements of certain taxes, penalties, fees, or interest. Both forms require detailed explanations of the reasons behind the request and support the taxpayer’s position with relevant documentation.

Form 12203 (Request for Appeals Review): This form, used for federal tax disputes, closely mirrors the NC-242 in its function as a preliminary step in the appeals process. Taxpayers fill out Form 12203 to request a review of a decision by the IRS, providing a structured way to object to findings similar to the structured objection process in North Carolina.

Form 3949-A (Information Referral): Although primarily used to report suspected tax law violations to the IRS, Form 3949-A and NC-242 share the procedural aspect of initiating a review based on provided information. Whereas the NC-242 is used by the taxpayer to object to a state tax decision, Form 3949-A is for third parties to initiate IRS reviews of others’ tax behaviors.

Property Tax Appeal Form: Local jurisdictions often have specific forms for appealing property tax assessments that require similar information to the NC-242, such as detailing objections to assessments and providing supporting documentation. These forms initiate a review process at the local level, akin to how NC-242 triggers a state-level review in North Carolina.

Sales Tax Exemption Certificate: While used for a different purpose—to certify a purchase is exempt from sales tax—this certificate and the NC-242 involve providing detailed information to tax authorities to affect tax liability. Both require thorough documentation and understanding of applicable tax laws.

Power of Attorney and Declaration of Representative (IRS Form 2848): Like the note in the NC-242 regarding representation and the need for a Power of Attorney, IRS Form 2848 serves a similar purpose at the federal level, authorizing individuals to represent a taxpayer before the IRS and to make requests or objections on their behalf.

Change of Address Form (IRS Form 8822): This form is used to notify the IRS of a change in address, comparable to updating information with the NC-242 when contesting tax issues. Both forms ensure that communication about tax matters is sent to the correct address, preventing delays or losses in correspondence.

Offer in Compromise (IRS Form 656): Employed by taxpayers to settle tax debts for less than the full amount owed, Form 656 involves detailed financial disclosures and offers to the IRS, akin to the detailed objections and proposals provided in the NC-242 to challenge tax assessments or seek adjustments in North Carolina.

Filling out the NC-242 form correctly is essential for requesting a departmental review in response to proposed tax assessments, adjustments, or denials of refunds by the North Carolina Department of Revenue. To ensure accuracy and compliance, here are 10 do's and don'ts to consider:

Complying with these do's and don'ts will help streamline the review process and increase the chances of a favorable outcome for your objection. Remember, accuracy and timeliness are crucial in financial matters, particularly when dealing with tax objections and appeals.

Understanding the NC-242 form, which is used for objecting and requesting a departmental review of a tax notice, involves navigating through some common misconceptions. It's important for individuals and entities in North Carolina to grasp the actual uses and stipulations of this form to ensure they manage their tax disputes effectively.

Misconception #1: The NC-242 form is only for businesses

This form is not solely for the use by businesses. Both individuals and entities can use the NC-242 to object to a proposed tax assessment, proposed adjustment, or proposed denial of refund. This means that whether you've filed a personal or joint tax return, or represent a business, you have the right to dispute a decision made by the Department of Revenue.

Misconception #2: You can submit the NC-242 form at any time

Timing is crucial when submitting the NC-242 form. There's a 45-day window to request a departmental review after the date the notice in dispute was either mailed by the Department or personally delivered. Waiting too long to file this request can result in losing the opportunity to contest the Department's decision.

Misconception #3: A Power of Attorney is not necessary when a representative signs

If a taxpayer's representative is signing the NC-242 form, a Power of Attorney must accompany the request. This document is essential to ensure that the representative has the legal authority to act on behalf of the taxpayer, safeguarding both the taxpayer's rights and the integrity of the review process.

Misconception #4: You don’t need to provide detailed objections or supporting documents

Simply submitting the form without a thorough explanation of your objections and relevant supporting documents will not suffice. The form provides space for detailing the specific objections to the notice received, and attaching additional pages or documents is necessary. These details and evidence are vital for a comprehensive review of your case.

Misconception #5: The NC-242 form is the final step in disputing a tax notice

Filing the NC-242 form is actually just the beginning of the appeals process. It requests a departmental review as the first step. Depending on the outcome of this review, further actions or appeals may be necessary to resolve the dispute. Understanding that this form initiates a process rather than concluding it is essential for setting realistic expectations.

Navigating tax disputes can be challenging, but understanding the correct use and procedures relating to the NC-242 form can help individuals and entities in North Carolina manage these disputes more effectively.

Filling out and using the NC-242 Objection and Request for Departmental Review form is a crucial step in contesting a decision made by the North Carolina Department of Revenue regarding tax assessments, refund denials, or adjustments. Here are six key takeaways to guide individuals and entities through this process:

Adhering to these guidelines when completing the NC-242 form increases the likelihood of a successful objection to the North Carolina Department of Revenue's initial decision. It's the first step in what may lead to a more extensive appeals process, so accuracy and thoroughness are paramount.

Yugioh Deck List Form - Judges will also initial and keep track of any deck checks round by round, so make sure everything is compliant.

Military Hurt Feelings Report - Acts as a mechanism for leaders to identify and counsel individuals who frequently feel emotionally slighted or misunderstood.

Pt Observation Hours - The checklist format of the settings and diagnoses observed makes it user-friendly and straightforward.