Free Ncui 101 PDF Template

Free Ncui 101 PDF Template

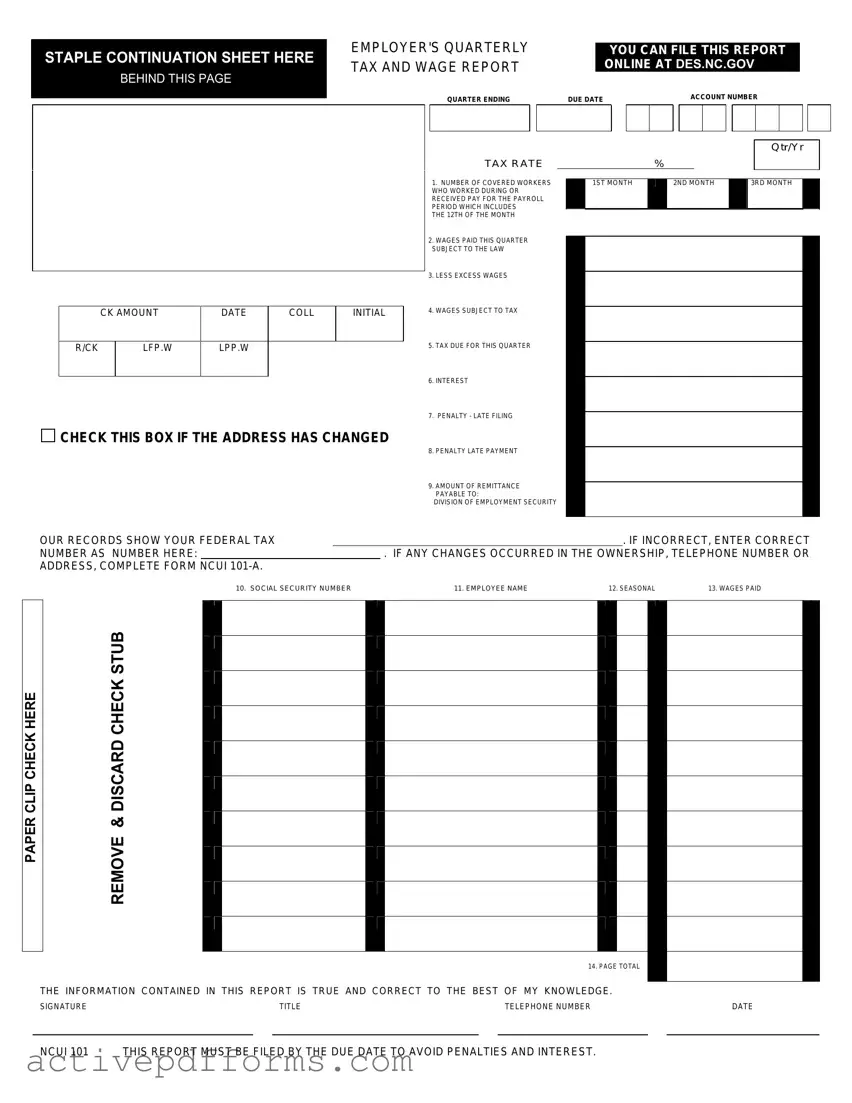

Managing payroll and taxes is a critical aspect of running a business, with specific forms designed to streamline this process, such as the NCUI 101 form. This form, known officially as the Employer's Quarterly Tax and Wage Report, is a fundamental document for employers in North Carolina, providing a structured way to report wages paid, taxes due, and other pertinent information. It covers essential items such as the number of covered workers each month, total wages subject to tax, and deductions for excess wages. It also outlines penalties for late filings and payments, thus emphasizing the importance of timely and accurate submissions. The form allows for adjustments in the event of ownership changes or incorrect information previously submitted. In addition to basic wage reporting, it accommodates special payments like bonuses or commissions, underscoring its comprehensive nature. With the option to file online, the NCUI 101 form represents a critical tool in maintaining compliance with state employment security law, ensuring proper tax payment, and avoiding unnecessary penalties. Employers are encouraged to familiarize themselves with each section of this document to fulfill their reporting obligations effectively and support the smooth operation of their businesses.

STAPLE CONTINUATION SHEET HERE

BEHIND THIS PAGE

EMPLOYER'S QUARTERLY TAX AND WAGE REPORT

QUARTER ENDING

TAX RATE

YOU CAN FILE THIS REPORT ONLINE AT DES.NC.GOV

DUE DATE |

|

|

|

ACCOUNT NUMBER |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qtr/Yr

%

1. NUMBER OF COVERED WORKERS |

1ST MONTH |

2ND MONTH |

3RD MONTH |

WHO WORKED DURING OR |

|

|

|

RECEIVED PAY FOR THE PAYROLL |

|

|

|

PERIOD WHICH INCLUDES |

|

|

|

THE 12TH OF THE MONTH |

|

|

|

|

CK AMOUNT |

DATE |

COLL |

INITIAL |

R/CK |

LFP.W |

LPP.W |

|

|

CHECK THIS BOX IF THE ADDRESS HAS CHANGED

CHECK THIS BOX IF THE ADDRESS HAS CHANGED

2.WAGES PAID THIS QUARTER SUBJECT TO THE LAW

3.LESS EXCESS WAGES

4.WAGES SUBJECT TO TAX

5.TAX DUE FOR THIS QUARTER

6.INTEREST

7.PENALTY - LATE FILING

8.PENALTY LATE PAYMENT

9.AMOUNT OF REMITTANCE PAYABLE TO:

DIVISION OF EMPLOYMENT SECURITY

OUR RECORDS SHOW YOUR FEDERAL TAX |

|

|

. IF INCORRECT, ENTER CORRECT |

|

NUMBER AS NUMBER HERE: |

|

. IF ANY CHANGES OCCURRED IN THE OWNERSHIP, TELEPHONE NUMBER OR |

||

ADDRESS, COMPLETE FORM |

NCUI |

|

|

|

CLIP CHECK HERE |

DISCARD CHECK STUB |

PAPER |

REMOVE & |

|

|

10. SOCIAL SECURITY NUMBER |

11. EMPLOYEE NAME |

12. SEASONAL |

13. WAGES PAID |

|

|

14. PAGE TOTAL |

|

THE INFORMATION CONTAINED IN THIS REPORT IS TRUE AND CORRECT TO THE BEST OF MY KNOWLEDGE.

SIGNATURE |

TITLE |

TELEPHONE NUMBER |

DATE |

NCUI 101 THIS REPORT MUST BE FILED BY THE DUE DATE TO AVOID PENALTIES AND INTEREST.

INSTRUCTIONS FOR COMPLETING FORM NCUI 101, EMPLOYER'S QUARTERLY TAX AND WAGE REPORT

ITEM 1: For each month in the calendar quarter, enter the number of all

ITEM 2: Enter all wages paid to all employees, including

(A)CORPORATION, the wages paid to all employees who performed services in North Carolina should be reported. Corporate officers are employees and their wages and/or draws are reportable.

(B)A PARTNERSHIP, the draws or payments made to general partners should not be reported.

(C)A PROPRIETORSHIP, the draws or payments made to the legal owner of the business (the proprietor) should not be reported. Wage paid to the children of the proprietor under the age of 21 years, as well as wages paid to the spouse or parents of the proprietor, should not be reported.

Special payments given in return for services performed, I.E., commissions, bonuses, fees, prizes, are wages and reportable under the Employment Security Law of North Carolina. These payments (or dollar value of the gifts/prizes) are to be included in the payroll of each employee by the employer for the calendar quarter(s) in which they are given.

If no wages were paid, enter NONE.

ITEM 3: Enter the amount of wages paid during this quarter that is in excess of the applicable North Carolina taxable wage base. This entry cannot be more than item 2.

Example: An employer using the 2012 taxable wage base of $20,400 and reporting one employee, John Doe, earning $6,000 per quarter.

1ST QTR 2ND QTR 3RD QTR 4TH QTR

ITEM 2: |

$6,000.00 |

$6,000.00 |

$6,000.00 |

$6,000.00 |

ITEM 3: |

$3,600.00 |

|||

ITEM 4: |

$6,000.00 |

$6,000.00 |

$6,000.00 |

$2,400.00 |

ITEM 4: Subtract Item 3 from Item 2. THE RESULTS CANNOT BE A NEGATIVE AMOUNT.

ITEM 5: Multiply Item 4 by the tax rate shown on the face of this report. (Example: .012% = .00012) If the tax due is less than $5.00, you do not have to

pay it, but you must file a report.

NOTE: ITEMS 6,7, AND 8 MUST BE COMPUTED ONLY IF THE REPORT IS NOT FILED (POSTMARKED) BY THE DUE DATE.

ITEM 6: Multiply the tax due (Item 5) by the current interest rate for each month, or fraction thereof, past the due date. The applicable interest rate may be obtained at des.nc.gov or by contacting the nearest Division of Employment Security Office.

ITEM 7: Multiply the tax due (Item 5) by 5% (.05) for each month, or fraction thereof, past the due date. The maximum late filing penalty is 25% (.25).

ITEM 8: Multiply the tax due (Item 5) by 10% (.1). The minimum late payment penalty is $5.00.

ITEM 9: Enter the sum of Items 5, 6, 7 and 8. Remittance should be made payable to the Division of Employment Security.

IF YOUR FEDERAL IDENTIFICATION NUMBER AS PRINTED ON THE REPORT IS INCORRECT, ENTER THE CORRECT NUMBER IN THE SPACE PROVIDED. STATE TAX CREDITS WILL BE REPORTED TO THE INTERNAL REVENUE SERVICE USING THIS NUMBER. IF YOUR FEDERAL IDENTIFICATION NUMBER IS NOT PREPRINTED; ENTER IT IN THIS SPACE.

ITEM 10: Enter the federal Social Security number of every worker whose wages are reported on this form.

ITEM 11: Enter the name of every worker whose wages are reported on his form. If the last name is listed first, it must be followed by a comma.

ITEM 12: Enter an 'S' in this space if the wages reported are seasonal, otherwise leave this space blank. To report seasonal wages you must have

been determined a seasonal pursuit by this agency.

ITEM 13: Wages are reportable in the quarter paid to the employee, regardless of when the wages were earned. Enter each worker's total quarterly

wages paid, whether or not the worker has exceeded the taxable wage base for this year. Do not show credit or minus amounts to adjust for

ITEM 14: Enter the sum of wages shown in Item 13 for this page only. The sum of the page totals of all pages must equal the amount shown in Item 2.

Additional information is available at: des.nc.gov

| Fact Name | Description |

|---|---|

| Form Title | NCUI 101 - Employer's Quarterly Tax and Wage Report |

| Online Filing Availability | Employers can file this report online at des.nc.gov |

| Due Date | This report must be filed by the specified due date to avoid penalties and interest. |

| Covered Workers | Employers must report the number of workers who worked or received pay for the period including the 12th of the month for each month in the quarter. |

| Wages Paid Subject to Law | Employers must report all wages paid to employees within the quarter, subject to specific exclusions based on the business type (corporation, partnership, or proprietorship). |

| Excess Wages and Taxable Wages | Excess wages above the North Carolina taxable wage base are not taxed. Wages subject to tax are calculated by subtracting excess wages from total wages paid. |

| Calculating Taxes Due | Taxes due are calculated by multiplying the taxable wages by the tax rate shown on the form. Penalties apply for late filing or payment. |

| Penalties | Interest, late filing, and late payment penalties are assessed if the report is not filed by the due date. Penalties are calculated as a percentage of the tax due. |

| Remittance Payable To | Division of Employment Security |

| Governing Law | Employment Security Law of North Carolina |

Filling out the NCUI 101 form, the Employer's Quarterly Tax and Wage Report, is a crucial step in ensuring compliance with state regulations. This process doesn't have to be overwhelming. By following the steps outlined below, employers can confidently complete the form, ensuring accurate reporting of wages and taxes for their employees. Remember, timely submission of this report helps avoid potential penalties and interest charges.

Once the form is completed and checked for accuracy, ensure it is submitted by the due date to the Division of Employment Security to avoid any penalties or interest charges. Additional assistance and information can be found on the DES website if needed.

The NCUI 101 form, known as the Employer's Quarterly Tax and Wage Report, is a document that employers in North Carolina must file each quarter. It reports the wages paid to employees, taxes due for these wages, and other related information to the Division of Employment Security.

Any employer in North Carolina who pays wages to employees for services performed within the state is required to file the NCUI 101 form each quarter.

Yes, the form can be filed online. Employers are encouraged to file this report online at DES.NC.GOV to ensure accuracy and speed in processing.

The form requires several pieces of information, including:

'Excess wages' refer to the portion of an employee's earnings that exceed North Carolina's taxable wage base for the year. These wages are not subject to additional unemployment tax for the remainder of the year once the wage base is exceeded.

To calculate the tax due, subtract the 'excess wages' from the total wages paid (Item 3 from Item 2), and multiply the result by the tax rate provided on the form.

If the report is filed after the due date, employers must calculate and include additional interest and penalties. These are computed based on the tax due, using the rates stipulated in Items 6, 7, and 8 of the form.

This report is due quarterly. The specific due dates are April 30th for Q1, July 31st for Q2, October 31st for Q3, and January 31st for Q4.

If you make an error on the form, you should request or download Form NCUI 685 for the quarter needing correction. This allows adjustments to previously reported wages or taxes.

The NCUI 101 form, essential for reporting an employer's quarterly tax and wage details to the Division of Employment Security, regularly sees a range of common errors. Careful attention to detail can prevent these mistakes, ensuring compliance and avoiding unnecessary penalties.

Incorrectly entering the number of covered workers for each month in the quarter under Item 1, often due to overlooking part-time or temporary employees who were working or received pay for the payroll period, which includes the 12th of the month.

Failing to accurately report all wages paid during the quarter under Item 2, which should include all employees, part-time and temporary. Mistakes here often occur when excluding corporate officers in a corporation, or mistakenly including general partners in a partnership and the proprietor or their family members in a proprietorship.

Miscalculating the amount in excess of the North Carolina taxable wage base under Item 3, either by overstating or understating, can lead to incorrect wage subject to tax calculations.

Not subtracting the excess wages from the total wages paid to calculate the wages subject to tax correctly under Item 4, resulting in either an overpayment or underpayment of taxes.

Incorrectly applying the tax rate to compute the tax due for the quarter under Item 5. This mistake hinges on not verifying the current tax rate indicated on the form, resulting in inaccurately calculated tax dues.

Overlooking to include interest owed for late filings under Item 6, often due to missing the due date for filing the report and not applying the current interest rate correctly.

Calculating late filing penalties under Item 7 inaccurately by not applying the 5% rate correctly for each month or part of a month past the due date, or not knowing the maximum penalty limit.

Incorrect calculations of late payment penalties under Item 8 by either not applying the 10% rate correctly or not adhering to the minimum penalty rule.

Forgetting to accurately total the amounts for tax due, interest, and penalties under Item 9, which leads to incorrect remittance amounts being paid to the Division of Employment Security.

Errors in entering federal Social Security numbers or employee names under Items 10 and 11, including typos or formatting errors (e.g., not placing a comma after the last name when it is listed first), which can cause discrepancies or delay processing.

In the endeavor to file accurately, it is vital to review these common pitfalls and ensure that each section of the NCUI 101 form is completed with precision. For additional guidance, resources are available at des.nc.gov, providing employers with the necessary tools to meet reporting requirements efficiently.

When managing employment and payroll responsibilities, businesses often need to complete and submit various forms in addition to the NCUI 101 Form, Employers Quarterly Tax and Wage Report. Each document plays a critical role in ensuring compliance with state and federal regulations. Simplifying these tasks, here's a brief overview of other frequently used forms and documents.

Each of these documents serves a vital function in the employment process, complementing the NCUI 101 Form by ensuring accurate reporting and compliance with legal obligations. For employers, familiarizing themselves with these forms can streamline payroll processes, prevent legal issues, and maintain a smooth operational flow.

Form 940 (Employer's Annual Federal Unemployment (FUTA) Tax Return): This form is similar to the NCUI 101 because it deals with reporting wages paid and unemployment taxes owed at a federal level, whereas the NCUI 101 serves a similar function at the state level for North Carolina businesses. Both forms require detailed wage information and calculations for taxes due.

Form 941 (Employer's Quarterly Federal Tax Return): Similar to the NCUI 101, Form 941 is submitted quarterly and requires employers to report wages paid, as well as withholdings from employees' paychecks for federal income, Social Security, and Medicare taxes. It entails reporting the number of employees, similar to item 1 on the NCUI 101.

W-2 (Wage and Tax Statement): While the W-2 is an annual statement provided to employees detailing their earned wages and taxes withheld, it parallels the wage reporting aspect of the NCUI 101. Both documents require accurate reporting of an employee's earnings and deductions throughout the year.

State Unemployment Tax Forms (varies by state): Each state has its own version of unemployment tax forms that are equivalent to the NCUI 101, tailored to their specific laws and requirements concerning unemployment insurance. They collect similar information on wages paid to employees and taxes due to fund state unemployment benefits.

Form W-3 (Transmittal of Wage and Tax Statements): This form summarizes the information of all W-2 forms for a business's employees, similar to how the NCUI 101 compiles quarterly wage and tax information. While the W-3 is for federal income and payroll taxes, the principle of summarizing employee compensation and taxes is akin to the reporting on the NCUI 101.

Form W-4 (Employee's Withholding Certificate): Although the Form W-4 is primarily used by employees to indicate their tax withholding preferences, it indirectly impacts the information reported on the NCUI 101, especially in terms of taxable wages. Both forms have a role in determining the financial obligations (either withholdings or unemployment taxes) related to employees' wages.

Form 1099-MISC (Miscellaneous Income): For independent contractors, the 1099-MISC serves a similar purpose to the NCUI 101 by reporting income earned, except it's used for non-employee compensation. Although it pertains to a different category of worker, the underlying concept of reporting earnings to tax authorities is a shared characteristic with the NCUI 101.

The NCUI 101 form, formally known as the Employer's Quarterly Tax and Wage Report, plays a crucial role in maintaining compliance with employment security laws in North Carolina. Ensuring accurate and timely submission not only upholds the law but also supports the state’s workforce by funding unemployment insurance. Below, find ways to navigate the filling out of this form with care and precision.

By adhering to these guidelines, employers can avoid common pitfalls and ensure that their reporting obligations are met with accuracy and timeliness.

Many employers and employees harbor misunderstandings regarding the NCUI 101 form, a crucial document for unemployment tax and wage reporting in North Carolina. Let's dispel some common misconceptions:

Only full-time employees need to be reported: Contrary to this belief, the NCUI 101 form requires the reporting of all full-time and part-time workers who worked during or received pay for the payroll period that includes the 12th of the month.

Corporate officer salaries are not reportable: In reality, corporate officers are considered employees, and their wages or draws are indeed reportable if services were performed in North Carolina.

Partner draws in a partnership are reportable: Actually, draws or payments made to general partners within a partnership are not to be reported on the NCUI 101 form.

Salaries paid to the owner's family are always reportable: Wages paid to the children (under 21 years of age), spouse, or parents of the proprietor are exceptions and should not be reported.

Special payments are not considered wages: Payments such as commissions, bonuses, fees, prizes, etc., are considered wages and are reportable under the Employment Security Law of North Carolina.

If no wages were paid in a quarter, the form need not be filed: Even if no wages were paid during a quarter, "NONE" must be entered in the relevant section, indicating the form still needs to be filed.

Tax due on wages is a flat rate irrespective of earnings: The tax due is actually calculated by multiplying the wages subject to tax (after exclusions) by the tax rate shown on the face of this report, which can vary.

Interest and penalties apply only to late payments: Interest and penalties can apply both for late filing and late payment, with specific calculations provided for each scenario.

The Federal identification number is not crucial: The correctness of the Federal identification number is essential as state tax credits are reported to the Internal Revenue Service using this number.

Wages are reportable only up to the taxable wage base: While the excess wages over the taxable wage base are not subject to further taxes, initial wages up to the base need to be reported, and each worker's total quarterly wages paid must be included, regardless of when the wages were earned.

Understanding the specifics of the NCUI 101 form is vital for accurate and compliant reporting of unemployment taxes and wages in North Carolina. Employers must ensure they are fully aware of the requirements to avoid common pitfalls and ensure their reporting is correct and timely.

Understanding how to properly complete the NCUI 101 form, the Employer's Quarterly Tax and Wage Report, is crucial for businesses to comply with state regulations and avoid unnecessary penalties. Here are key takeaways to guide employers through the process:

Timely and accurate completion of the NCUI 101 form is not merely a bureaucratic necessity; it ensures compliance with North Carolina's unemployment insurance laws. Employers can avoid penalties and maintain good standing by paying close attention to detail and adhering to the submission deadlines.

Truck Drivers Daily Run Sheet - Planning document for aligning event details, from timing to task distribution among team members.

I-983 Form Instructions - Completion of the I-983 form is a crucial step for maintaining lawful status during a STEM OPT period.

2 Mindset - The form is structured to facilitate the identification of food intolerances or sensitivities by monitoring reactions to certain foods.