Free St 108 PDF Template

Free St 108 PDF Template

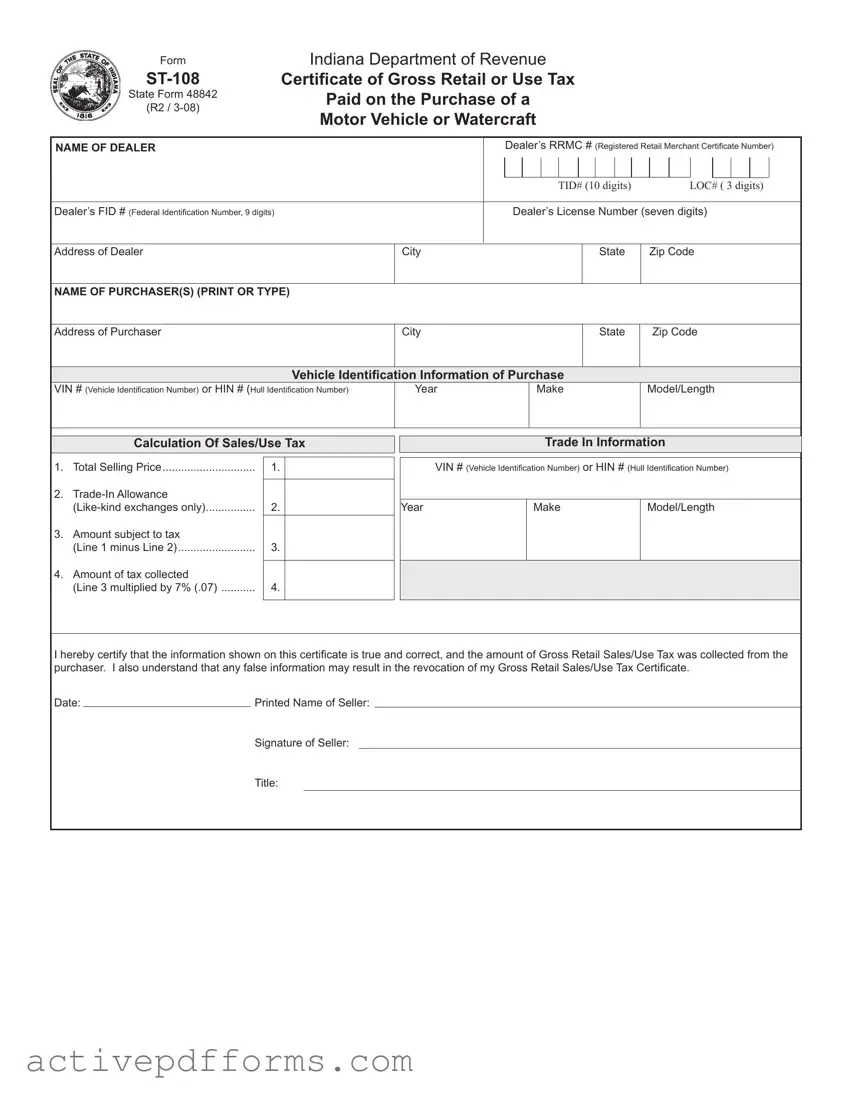

Understanding the intricacies of the Form ST-108, officially termed as State Form 48842, is crucial for anyone involved in the purchase of motor vehicles or watercraft in Indiana. This document serves as a Certificate of Gross Retail or Use Tax Paid, which is a vital component in the ownership transfer process. Designed by the Indiana Department of Revenue, the form ensures that the correct amount of sales or use tax is collected at the time of purchase and is subsequently reported and remitted by the dealer. Key sections detail the seller's and purchaser's information, vehicle identification, and a calculation area for determining the exact tax amount due. Especially noteworthy is the requirement for the dealer to include their Registered Retail Merchant Certificate number, alongside their Federal Identification Number, to validate the document. Additionally, the form accommodates a trade-in allowance, potentially affecting the tax calculation. Missteps in completing the form or failure to submit the necessary tax can lead to complications, underscoring the importance of accuracy when dealing with the ST-108. For transactions where an exemption is claimed, an ST-108E form must be completed, further emphasizing the need for thoroughness in adhering to state taxation laws concerning vehicle and watercraft purchases.

Form

State Form 48842

(R2 /

Indiana Department of Revenue

Certificate of Gross Retail or Use Tax

Paid on the Purchase of a

Motor Vehicle or Watercraft

NAME OF DEALER |

|

|

Dealer’s RRMC # (Registered Retail Merchant Certificate Number) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TID# (10 digits) |

|

|

LOC# ( 3 digits) |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Dealer’s FID # (Federal Identification Number, 9 digits) |

|

|

Dealer’s License Number (seven digits) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Dealer |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Purchaser(s) (pRINT OR tYPE) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Purchaser |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

Vehicle Identification Information of Purchase

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number) |

Year |

Make |

Model/Length |

|

|

|

|

Calculation Of Sales/Use Tax

1. |

Total Selling Price |

1. |

|

2. |

|

|

|

|

2. |

|

|

3. |

Amount subject to tax |

|

|

|

(Line 1 minus Line 2) |

3. |

|

4. |

Amount of tax collected |

|

|

|

|

||

|

(Line 3 multiplied by 7% (.07) |

4. |

|

|

|

|

|

Trade In Information

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number)

Year |

Make |

Model/Length |

|

|

|

|

|

|

I hereby certify that the information shown on this certificate is true and correct, and the amount of Gross Retail Sales/Use Tax was collected from the purchaser. I also understand that any false information may result in the revocation of my Gross Retail Sales/Use Tax Certificate.

Date: |

|

Printed Name of Seller: |

|

|

|

Signature of Seller: |

|

|

|

Title: |

|

Instructions for completing Form

or Use Tax on the Purchase of a Motor Vehicle or Watercraft.

INDIANA CODE

The

If an exemption from the tax is claimed, the purchaser and the dealer must complete Form

Seller Information

NAME OF DEALER: Indicate the name of the dealer as it appears on the Registered Retail Merchant Certificate (RRMC).

FID # (Federal Identification Number): Indicate the Federal Identification Number of the dealer, if applicable.

Dealer’s License #: Indicate the Dealer’s License Number(seven digits) as it appears on the Dealer’s License Certificate.

RRMC # (same as TID # - 10 Digits + LOC # - 3 Digits): Indicate the Indiana Taxpayer Identification Number and Location Number as it appears on the Registered Retail Merchant Certificate. This number must be in the following format:

Address of Dealer: Indicate the address of the dealer as it appears on the Registered Retail Merchant Certifi- cate.

Vehicle Identification Information

VIN or HIN ID #: Enter the Vehicle ID # (VIN) or the Hull ID # (HIN).

YEAR: Indicate the year the motor vehicle or watercraft was manufactured.

MODEL # OR WATERCRAFT LENGTH: If a motor vehicle is being sold indicate the model name for the vehicle. If a watercraft is being sold indicate the length of the craft.

Calculation of Sales/Use Tax

TOTAL SELLING PRICE: When determining the total selling price include all delivery, make ready, repair, or other costs incurred prior to transfer to the buyer. Federal excise tax is NOT included.

You must also indicate the make, model, year, and ID # of the

AMOUNT SUBJECT TO TAX: Line 1 minus Line 2 results in the amount on which the sales/use tax will be calcu- lated.

AMOUNT OF TAX COLLECTED: Line 3 multiplied by 7% or .07 equals the amount to be collected by the seller.

Signature Section: The Seller must sign the

| Fact Name | Description |

|---|---|

| Purpose of Form ST-108 | This form serves as a certificate for the Indiana Department of Revenue, verifying that gross retail or use tax has been paid on the purchase of a motor vehicle or watercraft. |

| Governing Law | The requirement to present this certification comes under INDIANA CODE 6-2.5-9-6, which ensures that the state gross sales and use tax on motor vehicles and watercraft purchases are documented and paid appropriately. |

| Key Information Included | The form collects details about the dealer and purchaser, vehicle or watercraft identification information, including VIN or HIN, and a calculation of the sales/use tax collected based on the total selling price and trade-in allowance. |

| Dealer and Seller Verification | The seller confirms the collection of gross retail sales/use tax from the purchaser with their signature, which is essential for the form's acceptance by the Indiana Department of Revenue and the Bureau of Motor Vehicles (BMV). |

| Exemption Provision | If a tax exemption is claimed, Form ST-108E must be completed by the purchaser and the dealer, and submitted to the license branch at the time of vehicle or watercraft licensing, serving as an affidavit of exemption. |

Filling out the ST-108 form is a critical step in documenting that the appropriate sales tax was collected for the purchase of a motor vehicle or watercraft in Indiana. This document serves as a certificate of the gross retail or use tax paid, which is necessary for the buyer to present when titling a vehicle or watercraft. It's vital that the information provided is accurate and complete to avoid any issues with the Bureau of Motor Vehicles. Following the steps below will guide you through the process of filling out the form correctly.

After completing the form, it’s crucial to review it for any errors or missing information. The seller must then submit the sales/use tax to the Department of Revenue along with a sales and use tax report. If the vehicle or watercraft purchase qualifies for an exemption, both the purchaser and the dealer must complete the ST-108E form and present it at the time of titling. Ensuring the ST-108 is correctly filled out and submitted is essential for the smooth registration and titling of your vehicle or watercraft.

What is Form ST-108?

Form ST-108, officially known as the Certificate of Gross Retail or Use Tax Paid on the Purchase of a Motor Vehicle or Watercraft, is a document utilized in the state of Indiana. It serves as proof that the gross retail sales or use tax has been collected on the purchase of a motor vehicle or watercraft. This certification is necessary when titling a vehicle or watercraft, ensuring the Indiana Department of Revenue has received the appropriate sales or use tax.

Who needs to complete the ST-108 form?

Dealers selling a motor vehicle or watercraft in Indiana are required to complete the ST-108 form. This form must be filled out accurately by the dealer to indicate the amount of tax collected from the purchaser, which must then be remitted to the Department of Revenue along with a sales and use tax report.

What information is required on the ST-108 form?

The ST-108 form requires detailed information regarding the seller and the buyer, including the dealer’s name, license number, and address, as well as the purchaser's name and address. Vehicle identification details, such as the VIN or HIN, year, make, and model or length, are also necessary. Additionally, the form includes sections for calculating the sales/use tax based on the total selling price and trade-in allowance, if applicable.

How do you calculate the amount of sales/use tax on the ST-108?

To calculate the sales/use tax on the ST-108 form, start with the total selling price of the vehicle or watercraft, including any pre-transfer costs but excluding federal excise tax. If a trade-in allowance for a like-kind vehicle or watercraft is applicable, subtract its value from the total selling price. The resulting amount is then multiplied by 7% (.07), which is the tax rate, to determine the tax amount collected from the purchaser.

What are the consequences of providing false information on the ST-108?

Providing false information on the ST-108 form is a serious matter that could result in the revocation of the dealer's Gross Retail Sales/Use Tax Certificate. This revocation could have significant implications, including penalties and legal consequences for the dealer. It is crucial that all information on the form is accurate and truthful.

Can a trade-in reduce the taxable amount on the ST-108 form?

Yes, a trade-in can reduce the taxable amount on the ST-108 form, but only if it’s a like-kind vehicle or watercraft. This means that the trade-in and the newly purchased item must be of similar types (e.g., a boat for another boat). The value of the trade-in is subtracted from the total selling price to determine the amount subject to tax. Non like-kind items do not qualify for reducing the taxable selling price.

What happens if the ST-108 form is not signed?

If the ST-108 form is not signed by the seller, the form will be rejected by the license branch. This rejection necessitates the purchaser to return to the seller to obtain the necessary signature. A signature on the ST-108 certifies that the sales/use tax has been collected and will be forwarded to the Department of Revenue with the Sales/Use Tax Return.

Is there an exemption form related to the ST-108?

Yes, if a tax exemption is claimed on the purchase of a motor vehicle or watercraft, Form ST-108E, an affidavit of exemption, must be completed by both the purchaser and the dealer. This form lists the available exemptions for qualified purchases and must be submitted to the license branch at the time of licensing.

What should you do if the dealer's information is incorrect on the ST-108?

If the dealer's information on the ST-108 form is incorrect or incomplete, especially the Indiana Taxpayer Identification Number and Location Number in the required format, the form will be rejected. It is essential for the purchaser to return to the dealer to rectify any errors and ensure the form is accurate before resubmission to the license branch.

Where do you submit the completed ST-108 form?

The completed ST-108 form must be submitted to a Bureau of Motor Vehicles (BMV) license branch as part of the vehicle or watercraft titling process. Furthermore, the dealer is responsible for submitting the collected sales/use tax to the Indiana Department of Revenue through a sales and use tax report.

Not properly entering the dealer's information, including the Federal Identification Number (FID #), Dealer’s License Number, and the specific format of the Taxpayer Identification Number (TID #) which combines 10 digits plus the 3-digit location number (LOC #). Forgetting to format these numbers correctly or failing to provide them in full can lead to the rejection of the form at the license branch, necessitating a return visit to the dealer to correct the oversight.

Omitting or inaccurately completing the Vehicle Identification Information section, particularly neglecting to include the Vehicle Identification Number (VIN) or Hull Identification Number (HIN) as required. The year, make, and model or length of the vehicle or watercraft must also be accurately detailed to avoid issues in the processing of the form.

Failing to calculate the sales/use tax correctly, which involves a three-step process: identifying the total selling price (inclusive of all pre-transfer costs minus the federal excise tax), determining the applicable trade-in allowance for like-kind exchanges only, and then subtracting the trade-in value from the total selling price to find the taxable amount before applying the 7% tax rate. Incorrect calculations in this section can result in either underpayment or overpayment of taxes.

Overlooking the trade-in information section for those who are trading in a like-kind vehicle or watercraft. This includes not specifying the make, model, year, and ID number of the trade-in item. This omission can forfeit the potential tax exemption on the trade-in value, leading to an inflated tax payment obligation.

Not signing the form or neglecting to fill in the date, printed name of the seller, and their title in the signature section. This certification is crucial as it attests to the seller's collection and future remittance of the stated gross retail sales/use tax to the Department of Revenue. Unsigned forms will be outright rejected, causing delays in the registration process for the purchaser.

The Form ST-108 serves a critical function in validating the payment of gross retail or use tax on the purchase of vehicles and watercrafts within Indiana. It's part of a suite of documents often necessary for a seamless transaction and compliance with state regulations. Here, we outline additional forms and documents frequently used alongside Form ST-108, each with its essential purpose in the broader context of vehicle or watercraft purchase and registration.

Understanding each of these documents and how they interact with Form ST-108 is vital for anyone involved in the sale or purchase of a motor vehicle or watercraft in Indiana. They ensure transparency, compliance with tax laws, and protection for all parties throughout the transaction process.

The W-9 Form, or Request for Taxpayer Identification Number and Certification, shares similarities with the ST-108 Form in that it collects the seller's Federal Identification Number (FID#). Both forms are used to ascertain tax-related identification and information from individuals or entities engaging in transactions that have tax implications. The W-9, much like the ST-108, requires the individual or entity to certify the accuracy of the information provided, under penalty of perjury.

The Title Application for vehicles or watercraft is another document that parallels the ST-108 Form. Both require detailed information about the vehicle or watercraft, including the Vehicle Identification Number (VIN) or Hull Identification Number (HIN), make, model, and year. This information is necessary for proving ownership, tax collection, and registration purposes. The focus on the identification of vehicles or watercraft makes both forms essential in the transactions they are designed to facilitate.

The Sales and Use Tax Return form is closely related to the ST-108 Form in terms of its purpose. The ST-108 facilitates the collection of sales/use tax at the point of sale, while the Sales and Use Tax Return is the document on which the collected tax is reported to the tax authorities. In essence, the ST-108 Form provides the initial step of collecting tax from the purchaser, and the Sales and Use Tax Return completes the process by remitting the tax to the government. Both are integral in ensuring the compliance with state tax laws.

The Bill of Sale document shares similarities with the ST-108 as both serve as evidence of a transaction between a buyer and a seller. While a Bill of Sale documents the transfer of ownership and the transaction details between the parties, the ST-108 specifically records the transaction for tax purposes. Both documents are critical for legal and tax compliance, detailing the parties' information, the item sold, and financial transactions involved, including the sales tax collected, if applicable.

Filling out Form ST-108, which is the Certificate of Gross Retail or Use Tax Paid on the Purchase of a Motor Vehicle or Watercraft, is a critical step during the buying process. To make sure you complete this form correctly and avoid any potential setbacks, here are 7 dos and don'ts to keep in mind:

By following these guidelines, you can ensure that the process of reporting and paying the necessary taxes on your vehicle or watercraft purchase is smooth and error-free. Remember, accurate and complete documentation is key to avoiding delays or additional trips to the license branch. Take your time, double-check your work, and make sure every piece of information is correct and clearly stated.

There are several common misconceptions regarding the ST-108 form, which is essential for reporting and paying gross retail or use tax on motor vehicle or watercraft purchases in Indiana. Understanding these misconceptions is crucial for both buyers and sellers to ensure compliance with Indiana tax law.

Understanding these key points can help ensure that the ST-108 form is completed correctly and efficiently, facilitating a smoother transaction process for both the seller and the purchaser.

Understanding the Form ST-108 is crucial for anyone purchasing a vehicle or watercraft in Indiana. This form serves as a certificate of the Gross Retail or Use Tax that has been paid at the time of purchase. Here are key takeaways about filling out and using the ST-108 form:

Adhering to these key points ensures that the purchase process for a motor vehicle or watercraft complies with Indiana's legal requirements, preventing any unnecessary delays or issues arising from the taxation aspect of the transaction.

What Is a Form 8300 Used For? - Individuals and businesses must provide detailed information on the form, including the identity of the payer and the nature of the business transaction.

104r - Helps ROTC program administrators monitor cadets' academic progress and adherence to commissioning prerequisites.