Free Transamerica 401K Withdrawal PDF Template

Free Transamerica 401K Withdrawal PDF Template

The Transamerica 401K Withdrawal form is a comprehensive document designed to facilitate various types of distributions from a participant’s 401K account. It stipulates that an individual, along with their spouse (if married and if the plan permits annuities) and the plan administrator, trustee, or an authorized signer, must complete and sign this form to request a distribution. It's critical to note that this form is not suitable for death benefit claims, required minimum distributions, or hardship withdrawal requests, directing users to seek alternative processes for such circumstances. The form provides detailed instructions for participants and employers, emphasizing the importance of accurately completing sections A through H and submitting the form according to specified guidelines. Distribution can be requested for several reasons, such as employment termination, retirement, or due to disability, each with its associated conditions and details for processing. Options for the form of payment include direct rollovers, partial distributions, or cash, with specific conditions applied to Roth 401(k) accounts and traditional 401(k) accounts to ensure compliance with tax laws and plan rules. Additional sections address situations like outstanding loan payoffs and spousal consent, indicating the form’s thoroughness in adhering to federal regulations and plan specifics. To ensure lawful compliance and proper processing, the document clearly outlines the requirements for federal and state income tax withholdings on distributions, providing essential information to participants on the tax implications of their withdrawal requests.

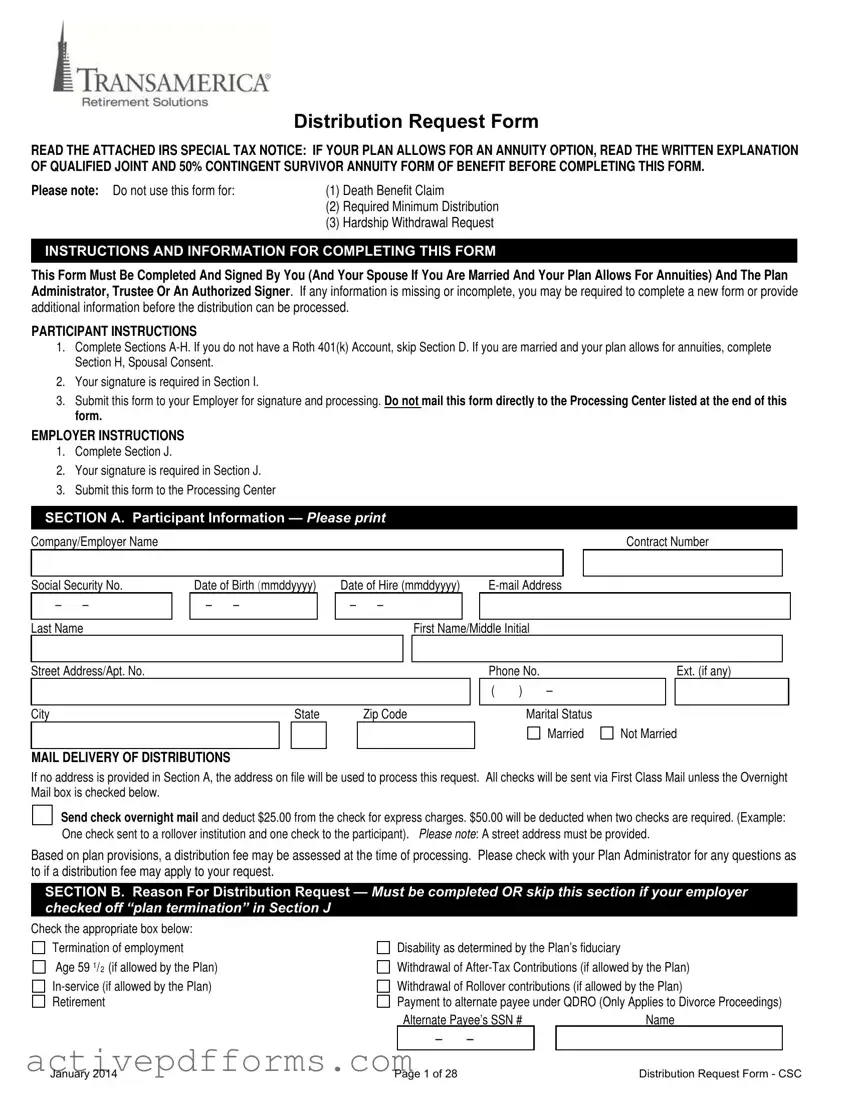

Distribution Request Form

READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF YOUR PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF QUALIFIED JOINT AND 50% CONTINGENT SURVIVOR ANNUITY FORM OF BENEFIT BEFORE COMPLETING THIS FORM.

Please note: Do not use this form for: |

(1) |

Death Benefit Claim |

|

(2) |

Required Minimum Distribution |

|

(3) |

Hardship Withdrawal Request |

INSTRUCTIONS AND INFORMATION FOR COMPLETING THIS FORM

This Form Must Be Completed And Signed By You (And Your Spouse If You Are Married And Your Plan Allows For Annuities) And The Plan Administrator, Trustee Or An Authorized Signer. If any information is missing or incomplete, you may be required to complete a new form or provide additional information before the distribution can be processed.

PARTICIPANT INSTRUCTIONS

1.Complete Sections

2.Your signature is required in Section I.

3.Submit this form to your Employer for signature and processing. DoUnot mailUthis form directly to the Processing Center listed at the end of this form.

EMPLOYER INSTRUCTIONS

1.Complete Section J.

2.Your signature is required in Section J.

3.Submit this form to the Processing Center

SECTION A. Participant Information — Please print

Company/Employer Name |

|

Contract Number |

|

|

|

Social Security No.

– –

Last Name

Date of Birth (mmddyyyy)

– –

Date of Hire (mmddyyyy) |

|

||

– |

– |

|

|

|

|

|

|

First Name/Middle Initial

Street Address/Apt. No. |

|

|

|

|

|

|

Phone No. |

|

|

Ext. (if any) |

||

|

|

|

|

|

|

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

Zip Code |

|

Marital Status |

|

|

|

|||

|

|

|

|

|

|

|

|

|

Married |

Not Married |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

MAIL DELIVERY OF DISTRIBUTIONS

If no address is provided in Section A, the address on file will be used to process this request. All checks will be sent via First Class Mail unless the Overnight Mail box is checked below.

Send check overnight mail and deduct $25.00 from the check for express charges. $50.00 will be deducted when two checks are required. (Example: One check sent to a rollover institution and one check to the participant). Please note: A street address must be provided.

Based on plan provisions, a distribution fee may be assessed at the time of processing. Please check with your Plan Administrator for any questions as to if a distribution fee may apply to your request.

SECTION B. Reason For Distribution Request — Must be completed OR skip this section if your employer checked off “plan termination” in Section J

Check the appropriate box below:

Termination of employment

Age 59 1P /P R2R (if allowed by the Plan)

Disability as determined by the Plan’s fiduciary

Withdrawal of

Withdrawal of Rollover contributions (if allowed by the Plan)

Payment to alternate payee under QDRO (Only Applies to Divorce Proceedings)

Alternate Payee’s SSN # |

Name |

– –

January 2014 |

Page 1 of 28 |

Distribution Request Form - CSC |

SECTION C. Form of Payment For Traditional 401(k) Account - Only choose one of the three options

SECTION C. Form of Payment For Traditional 401(k) Account - Only choose one of the three options

²Option 1 (Rollover) - I am requesting a Direct Rollover of

all or a

partial amount of my Traditional 401(k) account.

¹Partial amount to be rolled over: $___________________

Direct Rollover to: (Select Only One)

_____ AN IRA OFFERED THROUGH Transamerica (Minimum rollover amount is $5,000). If you are interested in the Rollover IRA option

through Transamerica, call (866)

_____ AN ELIGIBLE RETIREMENT PLAN (401(a), 401(k), 403(b), and Governmental 457)

_____ AN IRA

|

NEW ACCOUNT INFORMATION: |

MAILING ADDRESS: |

|

|

|

|

|

|

|

|

|

|

IRA Account Number (Required) / Plan Name |

Name of Trustee or Custodian for the New Plan or IRA |

|

|

|

|

|

|

|

|

|

|

Make Check Payable To: |

Address – Number & Street |

|

|

|

|

|

City |

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

²Option 2 (Combination) - I am requesting a distribution of my Traditional 401(k) account to be paid partially to me and partially as a Direct Rollover.

I understand that the portion payable to me may be subject to 20% federal income tax withholding.

Distribute __________% of my Traditional 401(k) account:

____________% of the above paid directly to me, and

____________% of the above applied to the Direct Rollover Account indicated below.

The above two percentages must equal 100%

Direct Rollover to: (Select Only One)

_____ AN IRA OFFERED THROUGH Transamerica (Minimum rollover amount is $5,000). If you are interested in the Rollover IRA option

through Transamerica, call (866)

_____ AN ELIGIBLE RETIREMENT PLAN (401(a), 401(k), 403(b), and Governmental 457)

_____ AN IRA

NEW ACCOUNT INFORMATION: |

MAILING ADDRESS: |

IRA Account Number (Required) / Plan Name |

Name of Trustee or Custodian for the New Plan or IRA |

Make Check Payable To:

Address – Number & Street

|

|

City |

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Option 3 (Cash) - I am requesting a distribution of |

all or a |

partial amount of my Traditional 401(k) account. I am not electing a Direct |

||

Rollover of any portion of the distribution. I understand the check will be made payable to me and that the portion payable to me may be subject to 20% federal income tax withholding.

¹Partial amount to be paid directly to me: $_____________

¹Actual Value of the distribution may vary based on the final market closing price at the time the distribution is processed, and any applicable processing fees.

PARTIAL DISTRIBUTION AMOUNTS

²DIRECT ROLLOVER

In a Direct Rollover, an eligible rollover distribution is paid from your retirement plan directly to an IRA or your new Employer's 401(a), 401(k), 403(b) or governmental 457 Plan. An IRS Form

January 2014 |

Page 2 of 28 |

Distribution Request Form - CSC |

SECTION D. Form of Payment For A Roth 401(k) Account – Complete only if your plan allows for Roth Contributions. Only choose one of the three options

²Option 1 (Rollover) - I am requesting a Direct Rollover of

all or a

partial amount of my Roth 401(k) account.

¹Partial amount to be rolled over: $___________________

Direct Rollover to: (Select Only One)

_____A ROTH IRA OFFERED THROUGH Transamerica. (Minimum rollover amount is $5,000.) If you are interested in the Rollover IRA

option through Transamerica, call (866)

______A DESIGNATED ROTH ACCOUNT (401(k) or 403(b)) OR ROTH IRA

NEW ACCOUNT INFORMATION: |

MAILING ADDRESS: |

|

|

Roth IRA Account Number (Required) / Plan Name |

Name of Trustee or Custodian for the New Roth 401(k) or Roth IRA |

Make Check Payable To:

Address – Number & Street

City |

State |

Zip Code |

²Option 2 (Combination) - I am requesting a distribution of my Roth 401(k) account to be paid partially to me and partially as a Direct Rollover.

I understand that the portion payable to me may be subject to 20% federal income tax withholding.

Distribute __________% of my Roth 401(k) account:

____________% of the above paid directly to me, and

____________% of the above applied to the Direct Rollover Account indicated below.

The above two percentages must equal 100%

Direct Rollover to: (Select Only One)

_____ A ROTH IRA OFFERED THROUGH Transamerica. (Minimum rollover amount is $5,000.) If you are interested in the Rollover IRA

option through Transamerica, call (866)

_____ A DESIGNATED ROTH ACCOUNT (401(k) or 403(b)) OR ROTH IRA

NEW ACCOUNT INFORMATION: |

MAILING ADDRESS: |

IRA Account Number (Required) / Plan Name |

Name of Trustee or Custodian for the New Plan or IRA |

Make Check Payable To:

Address – Number & Street

|

|

City |

State |

Zip Code |

||

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Option 3 (Cash) - I am requesting a distribution of |

all or a |

partial amount of my Roth 401(k) account. I am not electing a Direct Rollover of |

|||

any portion of the distribution. I understand the check will be made payable to me and that the portion payable to me may be subject to 20% federal income tax withholding.

¹Partial amount to be paid directly to me: $___________

¹Actual Value of the distribution may vary based on the final market closing price at the time the distribution is processed, and any applicable processing fees.

DISTRIBUTION AMOUNTS

²DIRECT ROLLOVER

In a Direct Rollover, an eligible rollover distribution is paid from your retirement plan directly to an IRA or your new Employer's 401(a), 401(k), 403(b) or governmental 457 Plan. An IRS Form

For participants required to take a minimum distribution during the current year that was not satisfied, please note the following: Your required minimum distribution (RMD) for the current year will need to be completed and made payable to you prior to the processing of your direct rollover request.

January 2014 |

Page 3 of 28 |

Distribution Request Form - CSC |

SECTION E. Annuity Request (Not applicable to vested account under $5000 or if your plan does not offer annuities)

Skip this section if you made an election in Section C or D.

By selecting this option your entire account balance will be distributed in order to purchase the annuity

Annuity: If the plan offers annuities as a form of benefit payment, I elect payment as a monthly annuity with payments to commence ___________________.

Upon my death, my spouse’s payments should be _____% (from 50% to 100%) of my payments. My spouse’s date of birth is _________________. Such

annuity will be a Joint and Contingent Survivor Annuity if I am married and a Single Life Annuity if I am not married. I also understand that if I am married, my spouse need not consent to this election if I choose a Qualified Joint and Contingent Survivor Annuity (“QJSA”).

SECTION F. Outstanding Loan Payoff Instructions — Skip this section if you do not have an outstanding loan or are requesting an

One of the following will occur if you have an outstanding loan amount and your reason for a distribution request in Section B is for Termination of Employment, Disability or a Retirement Benefit.

♦Your Loan will be considered paid in full if you have submitted your payment for the outstanding loan amount to your employer or have attached a money order or cashier’s check to this form.

♦Your outstanding loan balance will default and become taxable to you if Transamerica receives this form and your payment has not been received and processed.

SECTION G. Income Tax Withholding

The income tax withholding requirements vary depending on whether or not the distribution requested is an eligible rollover distribution. Please see the attached Special Tax Notice for the definition of eligible rollover distribution and a detailed explanation of the federal income tax withholding rules. If you request a Direct Rollover, no federal income tax will be withheld from the amount directly rolled over.

FEDERAL INCOME TAX

Eligible Rollover Distributions:

•If you request a Direct Rollover, no federal income tax will be withheld from the amount directly rolled over.

•If you request any portion that is an Eligible Rollover Distribution and payable to you: 20% mandatory federal income tax withholding will apply if the taxable amount of the distribution is more than $200 unless paid over 10 or more years.

STATE INCOME TAX

If your address of record is within a mandatory withholding state, state taxes will be withheld from your distribution in accordance with the respective state rules. Other states allow an independent election and in these states, state tax will be withheld unless you elect otherwise. If your state does not allow withholding, no state tax can be withheld. Please consult a tax advisor or Transamerica if you have questions regarding state tax withholding.

Do not withhold state income tax (ONLY IF INDEPENDENT ELECTION IS PERMITTED).

Withhold state income tax:__________% (If your state requires a greater withholding percentage than what you have indicated, the mandatory state

tax will apply).

SECTION H. Spousal Consent

Check with your Employer/Plan Administrator or Summary Plan Description to determine whether your plan is subject to spousal consent requirements. If spousal consent is required, complete this section. If your plan is not subject to spousal consent requirements, skip to Section I. Please note: You must have your spouse’s signature notarized or have a plan representative witness your spouse’s signature if your vested account balance is greater than $5,000 and your plan provides for joint and survivor annuities. However, if your vested account balance is less than $5,000 spousal consent is not required.

Spousal Consent

I, the undersigned spouse of the participant, have read the “Special Tax Notice Regarding Payments From Qualified Plans” provided to me and understand the effects of the waiver. I understand that federal law requires that the retirement benefit of my spouse must be paid under a Qualified Joint and Survivor Annuity Form as described in the attached “Special Tax Notice Regarding Payments From Qualified Plans,” unless I consent otherwise in writing to another benefit form. I hereby consent to the waiver of the annuity and consent to the form of benefit elected by my spouse.

Signature of Participant’s Spouse: |

|

Date: |

||

|

|

|

Statement of Plan Representative or Notary Public |

|

The spouse whose signature I have witnessed is known to me and signed this form in my presence. |

||||

Plan Representative: |

|

|

Date: |

|

Notary Public Signature: |

|

|

Date: |

|

PLACE SEAL HERE (if applicable)

January 2014 |

Page 4 of 28 |

Distribution Request Form - CSC |

SECTION I. Participant Signature

SECTION I. Participant Signature

My signature acknowledges that I have read, understand and agree to all the terms of this Distribution Request form, and affirm that all information that I have provided is true and correct. Further, I acknowledge that I have received the “Special Tax Notice Regarding Payments From Qualified Plans” and other required notices. The above information is true and correct to the best of my knowledge. I further understand that I may revoke this election at any time prior to the distribution taking place.

Signature of Participant |

Date |

PARTICIPANT: RETURN COMPLETED FORM TO YOUR PLAN ADMINISTRATOR FOR PROCESSING

Section J. For Completion by Plan Administrator, Trustee Or Authorized Signer Only

Section J. For Completion by Plan Administrator, Trustee Or Authorized Signer Only

Plan Name

Contract Number |

Sub ID/Division # (if applicable) |

Participant’s SSN # |

– –

Participant’s Termination Date (if applicable):

– –

The Participant is entitled to a vested benefit of% of company matching contributions.

The Participant is entitled to a vested benefit of _______________________% of profit sharing contributions.

The Number of hours worked in the Plan Year of Termination: __________________

Please refer to your Plan Document for the vesting schedule. If this information is not provided, the distribution will be processed with the data in Transamerica’s recordkeeping system.

Is payment of this benefit subject to Plan Termination?

No

Yes

By signing below, I hereby authorize Transamerica to process the distribution described in this form. This request is in compliance with plan provisions.

If spousal consent is not provided, then in accordance with the terms and provisions of the plan and under the current law, spousal consent is not required for payment of the requested benefit.

If this request is for a disability distribution, I certify that the participant meets the requirements of Section 72(m)(7).

Only submit this form after final contributions and loan repayments have been processed for termination distributions

Once this form has been completed with all of the necessary information and required signatures, please forward to the Processing Center. This form cannot be processed without the Plan Administrator, Trustee or Authorized Signer’s signature.

Be sure to keep a copy for your records.

By: Signature of Plan Administrator, Trustee or Authorized Signer |

|

Date |

|

|

|

|

|

Print Name of Plan Administrator, Trustee or Authorized Signer |

|

Date |

|

FOR PLAN ADMINISTRATOR USE ONLY - MAIL TO: 8488 Shepherd Farm Drive, West Chester, OH 45069,Fax #: (877)

January 2014 |

Page 5 of 28 |

Distribution Request Form - CSC |

SPECIAL TAX NOTICE

REGARDING PAYMENTS FROM QUALIFIED PLANS

YOUR ROLLOVER OPTIONS

You are receiving this notice because all or a portion of a payment you are receiving from your Employer’s plan (the "Plan") is eligible to be rolled over to an IRA, a Roth IRA, an employer plan, or a designated Roth account in an employer plan. This notice is intended to help you decide whether to do a rollover.

This notice describes the rollover rules that apply to two types of payments that you may be eligible to receive from the Plan: payments that are from a designated Roth account and payments that are not from a designated Roth account. A designated Roth account is a type of account with special tax rules that is available in some employer plans. If you are eligible to receive payments from the Plan that are from a designated Roth account and payments that are not from such an account, the Plan administrator or the payor will tell you the amount that is being paid from each account.

Rules that apply to most payments from a plan are described in the "General Information About Rollovers" section. In addition, additional rules that apply to most payments from a designated Roth account are described in the "General Information About Rollovers From A Designated Roth Account" section. Special rules that only apply in certain circumstances are described in the "Special Rules and Options" section.

Your Right to Waive the

Generally, neither a Direct Rollover nor a payment can be made from the plan until at least 30 days after your receipt of this notice. Thus, after receiving this notice, you have at least 30 days to consider whether or not to have your withdrawal directly rolled over. If you do not wish to wait until this

GENERAL INFORMATION ABOUT ROLLOVERS

How can a rollover affect my taxes?

You will be taxed on a payment from the Plan if you do not roll it over. If you are under age 59 1/2 and do not do a rollover, you will also have to pay a 10% additional income tax on early distributions (unless an exception applies). However, if you do a rollover, you will not have to pay tax until you receive payments later and the 10% additional income tax will not apply if those payments are made after you are age 59 1/2 (or if an exception applies).

Where may I roll over the payment?

You may roll over the payment to either an IRA (an individual retirement account or individual retirement annuity) or an employer plan (a

January 2014 |

Page 6 of 28 |

Distribution Request Form - CSC |

How do I do a rollover?

There are two ways to do a rollover. You can do either a direct rollover or a

If you do a direct rollover, the Plan will make the payment directly to your IRA or an employer plan. You should contact the IRA sponsor or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit into an IRA or eligible employer plan that will accept it. You will have 60 days after you receive the payment to make the deposit. If you do not do a direct rollover, the Plan is required to withhold 20% of the payment for federal income taxes (up to the amount of cash and property received other than employer stock). This means that, in order to roll over the entire payment in a

How much may I roll over?

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is eligible for rollover, except:

●Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

●Required minimum distributions after age 70 1/2 (or after death)

●Hardship distributions

●ESOP dividends

●Corrective distributions of contributions that exceed tax law limitations

●Loans treated as deemed distributions (for example, loans in default due to missed payments before your employment ends)

●Cost of life insurance paid by the Plan

●Contributions made under special automatic enrollment rules that are withdrawn pursuant to your request within 90 days of enrollment

●Amounts treated as distributed because of a prohibited allocation of S corporation stock under an ESOP (also, there will generally be adverse tax consequences if you roll over a distribution of S corporation stock to an IRA).

The Plan administrator or the payor can tell you what portion of a payment is eligible for rollover.

If I don't do a rollover, will I have to pay the 10% additional income tax on early distributions?

If you are under age 59 1/2, you will have to pay the 10% additional income tax on early distributions for any payment from the Plan (including amounts withheld for income tax) that you do not roll over, unless one of the exceptions listed below applies. This tax is in addition to the regular income tax on the payment not rolled over.

The 10% additional income tax does not apply to the following payments from the Plan:

●Payments made after you separate from service if you will be at least age 55 in the year of the separation

●Payments that start after you separate from service if paid at least annually in equal or close to equal amounts over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

●Payments from a governmental defined benefit pension plan made after you separate from service if you are a public safety employee and you are at least age 50 in the year of the separation

●Payments made due to disability

●Payments after your death

●Payments of ESOP dividends

●Corrective distributions of contributions that exceed tax law limitations

●Cost of life insurance paid by the Plan

●Payments made directly to the government to satisfy a federal tax levy

●Payments made under a qualified domestic relations order (QDRO)

●Payments up to the amount of your deductible medical expenses

●Certain payments made while you are on active duty if you were a member of a reserve component called to duty after September 11, 2001 for more than 179 days

●Payments of certain automatic enrollment contributions requested to be withdrawn within 90 days of the first contribution.

January 2014 |

Page 7 of 28 |

Distribution Request Form - CSC |

If I do a rollover to an IRA, will the 10% additional income tax apply to early distributions from the IRA?

If you receive a payment from an IRA when you are under age 59 1/2, you will have to pay the 10% additional income tax on early distributions from the IRA, unless an exception applies. In general, the exceptions to the 10% additional income tax for early distributions from an IRA are the same as the exceptions listed above for early distributions from a plan. However, there are a few differences for payments from an IRA, including:

●There is no exception for payments after separation from service that are made after age 55.

●The exception for qualified domestic relations orders (QDROs) does not apply (although a special rule applies under which, as part of a divorce or separation agreement, a

●The exception for payments made at least annually in equal or close to equal amounts over a specified period applies without regard to whether you have had a separation from service.

●There are additional exceptions for (1) payments for qualified higher education expenses, (2) payments up to $10,000 used in a qualified

Will I owe State income taxes?

This notice does not describe any State or local income tax rules (including withholding rules).

January 2014 |

Page 8 of 28 |

Distribution Request Form - CSC |

GENERAL INFORMATION ABOUT ROLLOVERS

FROM A DESIGNATED ROTH ACCOUNT

How can a rollover affect my taxes?

If the payment from the Plan is not a qualified distribution and you do not do a rollover to a Roth IRA or a designated Roth account in an employer plan, you will be taxed on the earnings in the payment. If you are under age 59 1/2, a 10% additional income tax on early distributions will also apply to the earnings (unless an exception applies). However, if you do a rollover, you will not have to pay taxes currently on the earnings and you will not have to pay taxes later on payments that are qualified distributions.

If the payment from the Plan is a qualified distribution, you will not be taxed on any part of the payment even if you do not do a rollover. If you do a rollover, you will not be taxed on the amount you roll over and any earnings on the amount you roll over will not be taxed if paid later in a qualified distribution.

A qualified distribution from a designated Roth account in the Plan is a payment made after you are age 59 1/2 (or after your death or disability) and after you have had a designated Roth account in the Plan for at least 5 years. In applying the

Where may I roll over the payment?

You may roll over the payment to either a Roth IRA (a Roth individual retirement account or Roth individual retirement annuity) or a designated Roth account in an employer plan (a

●If you do a rollover to a Roth IRA, all of your Roth IRAs will be considered for purposes of determining whether you have satisfied the

●If you do a rollover to a Roth IRA, you will not be required to take a distribution from the Roth IRA during your lifetime and you must keep track of the aggregate amount of the

●Eligible rollover distributions from a Roth IRA can only be rolled over to another Roth IRA.

January 2014 |

Page 9 of 28 |

Distribution Request Form - CSC |

How do I do a rollover?

There are two ways to do a rollover. You can either do a direct rollover or a

If you do a direct rollover, the Plan will make the payment directly to your Roth IRA or designated Roth account in an employer plan. You should contact the Roth IRA sponsor or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit within 60 days into a Roth IRA, whether the payment is a qualified or nonqualified distribution. In addition, you can do a rollover by making a deposit within 60 days into a designated Roth account in an employer plan if the payment is a nonqualified distribution and the rollover does not exceed the amount of the earnings in the payment. You cannot do a

If you do a direct rollover of only a portion of the amount paid from the Plan and a portion is paid to you, each of the payments will include an allocable portion of the earnings in your designated Roth account.

If you do not do a direct rollover and the payment is not a qualified distribution, the Plan is required to withhold 20% of the earnings for federal income taxes (up to the amount of cash and property received other than employer stock). This means that, in order to roll over the entire payment in a

How much may I roll over?

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is eligible for rollover, except:

●Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

●Required minimum distributions after age 70 1/2 (or after death)

●Hardship distributions

●ESOP dividends

●Corrective distributions of contributions that exceed tax law limitations

●Loans treated as deemed distributions (for example, loans in default due to missed payments before your employment ends)

●Cost of life insurance paid by the Plan

●Contributions made under special automatic enrollment rules that are withdrawn pursuant to your request within 90 days of enrollment

●Amounts treated as distributed because of a prohibited allocation of S corporation stock under an ESOP (also, there will generally be adverse tax consequences if S corporation stock is held by an IRA).

The Plan administrator or the payor can tell you what portion of a payment is eligible for rollover.

January 2014 |

Page 10 of 28 |

Distribution Request Form - CSC |

| Fact Number | Fact Detail |

|---|---|

| 1 | The Transamerica 401K Withdrawal form is not for use with death benefit claims, required minimum distributions, or hardship withdrawal requests. |

| 2 | Participants and their spouses (if applicable) must complete and sign the form, which then must be signed by the plan administrator, trustee, or an authorized signer. |

| 3 | Participants with a Roth 401(k) account should only complete Section D of the form. |

| 4 | For distributions, the form offers multiple options, including direct rollover, combination of payment and rollover, or cash payment. |

| 5 | The form includes provisions for annuity payments if the plan offers annuities as a form of benefit payment. |

| 6 | Spousal consent is required if the vested account balance is greater than $5,000 and the plan provides for joint and survivor annuities. |

| 7 | For processing a distribution, the participant’s signature acknowledges understanding and agreement with the terms of the form. |

| 8 | State tax withholding rules vary by state, and the form includes instructions for handling state income tax depending on the participant's address. |

| 9 | The form requires specifying a reason for the distribution request, with several options provided including termination of employment and retirement. |

| 10 | The form must be submitted to the plan administrator for processing, not mailed directly to the processing center. |

When it's time to withdraw funds from your Transamerica 401K account, completing the Distribution Request Form correctly is essential to ensure a smooth process. Whether you're nearing retirement, facing financial hardships, or considering rolling over your account to another plan, understanding how to fill out this form properly is your first step. This guide outlines the necessary steps to complete your withdrawal request.

Once all parts of the form are completed, do not mail it yourself. Instead, submit it to your employer or plan administrator for processing. They will forward it to the appropriate Processing Center. Ensuring all information is accurate and complete on your end speeds up the process, getting you one step closer to accessing your funds as planned.

What is the purpose of the Transamerica 401K Withdrawal form?

This form is designed for participants in a Transamerica 401(k) plan who wish to request a distribution of their retirement funds. It's not to be used for specific requests such as death benefits, required minimum distributions, or hardship withdrawals. Participants, and if applicable, their spouses and plan administrators, must complete and sign the form to authorize the withdrawal.

How should I complete the Transamerica 401K Withdrawal form?

Participants need to fill out Sections A-H, skipping Section D if they don’t have a Roth 401(k) account and Section H if not married or if their plan doesn’t offer annuities. All participants must sign Section I. If married and your plan includes annuities, you must complete spousal consent (Section H). Employers must complete and sign Section J. Do not send the form directly to Transamerica; your employer will forward it for processing.

How can I request a rollover with this form?

To request a rollover, select option 1 in either Section C (for Traditional 401(k) accounts) or Section D (for Roth accounts), indicating whether you want a complete or partial rollover and where the funds should be transferred. You'll need to provide the account information for the new plan or IRA where the funds will be moved. This option allows for the transfer of funds directly, avoiding withholding taxes.

Can I receive a distribution as cash directly to me?

Yes. For both Traditional and Roth 401(k) accounts, select option 3 in the respective section (C for Traditional, D for Roth) to have a full or partial distribution made directly to you. Be aware that this distribution may be subject to 20% federal income tax withholding, in addition to potential state taxes, depending on your state's rules.

What is the spousal consent section, and when is it needed?

Section H requires the consent of a participant’s spouse if the vested account balance is over $5,000 and the plan includes options for joint and survivor annuities. This consent verifies that the spouse agrees to waive their right to certain benefits in favor of the chosen distribution method. It's not required for accounts under $5,000 or if the plan doesn’t offer annuities.

What happens if I don’t fill out the form correctly?

If any required information is missing or the form is incomplete, the processing of your distribution request may be delayed. You might be asked to fill out a new form or provide the missing details before your request can be processed.

How can I request a withdrawal due to hardship or a required minimum distribution (RMD)?

This particular form cannot be used for hardship withdrawals or required minimum distributions. If you need to request these types of distributions, you’ll need to use a different form specifically designed for that purpose. Contact your plan administrator or Transamerica's customer support for the appropriate forms and instructions.

What should I do after completing the form?

After filling out the form, return it to your plan administrator (and not directly to Transamerica or any processing center) for them to complete their portion and submit it for processing. Make sure to keep a copy of the completed form for your records.

Not attaching the IRS Special Tax Notice: Failing to review and attach the IRS Special Tax Notice, as required, can lead to misunderstandings about the tax implications of the withdrawal.

Skipping necessary sections: For example, participants sometimes skip Section D about Roth 401(k) Account withdrawals or Section H concerning Spousal Consent, when these sections are relevant to their situation.

Incorrect mailing instructions: People often forget to provide a street address for overnight mail delivery, or they fail to check the appropriate box for overnight mail, which delays the receipt of their funds.

Choosing the wrong distribution reason: In Section B, selecting an incorrect reason for the distribution request can result in processing delays or the submission being returned for correction.

Improper form of payment selection: Not clearly indicating a choice among the options provided in Sections C (for Traditional 401(k)) and D (for Roth 401(k)) can complicate processing the form.

Incomplete new account information: In the rollover options of both Sections C and D, failing to provide complete new IRA or plan account information can stall the distribution process.

Not specifying distribution amounts correctly: Not clearly stating the partial amount to be rolled over or directly paid to them can lead to incorrect distribution amounts being processed.

Ignoring the Outstanding Loan Payoff Instructions: Applicants sometimes skip Section F when they have an outstanding loan that needs to be addressed as part of the withdrawal process.

Lack of required signatures: Failing to obtain the necessary signatures, especially in Section H for Spousal Consent (when applicable), or to properly complete Section I (Participant Signature) results in invalid submissions that cannot be processed.

When it comes to managing your retirement savings, especially when preparing for a 401(k) withdrawal, it's vital to understand not only the primary form you're filling out but also other documents that might be needed during the process. Whether you're considering making changes to your 401(k) plan, taking a distribution, or rolling the funds over into another retirement account, each action requires specific forms and documents to legally complete these transactions. This overview will shed some light on other forms and documents that are often used alongside the Transamerica 401(k) Withdrawal form, ensuring a smooth and compliant transition.

Each document and form plays a unique role in managing and accessing your 401(k) funds, impacting everything from tax liabilities to future income security. Being informed and prepared with the necessary paperwork will help streamline the process, ensuring you can make the most out of your retirement savings. Make sure to consult with a financial advisor or tax professional to fully understand the implications of each form and to ensure all your submissions are compliant with current laws and regulations.

401(a) Withdrawal Form: Similar to the Transamerica 401K Withdrawal form, a 401(a) Withdrawal Form is also designed for participants to request distributions from their retirement accounts. Both forms require participants to choose a form of payment and indicate if the distribution will be a direct rollover, a combination, or cash.

457(b) Distribution Request Form: This form, used in 457(b) plans, captures requests for distributions due to reasons such as retirement or reaching a particular age, similar to the reasons enumerated in the Transamerica form. Both include sections for distributing to an IRA or another plan via a direct rollover.

403(b) Distribution Request Form: 403(b) plans, mainly utilized by nonprofit organizations, have a distribution request form with options like direct rollover to an IRA, combining distribution types, and cash payouts, akin to the options presented in the Transamerica form.

Roth IRA Distribution Form: This form is for Roth IRA account holders seeking distributions. The similarity with the Transamerica form lies in the option to roll over funds into another eligible retirement account or opting for a cash distribution, showcasing the flexibility in managing post-tax contributions.

IRA Distribution Form: Traditional IRA distribution forms also facilitate withdrawals, offering options such as direct rollovers or cash payments, similar in structure to the options provided in the Transamerica 401K Withdrawal form. These forms consider the tax implications of distributions.

Profit Sharing Plan Withdrawal Form: Like the Transamerica form, this document is used for requesting distributions from a profit-sharing plan. It details similar payment options, including rollovers to eligible retirement plans, and specifies tax withholdings as applicable.

Annuity Election Form: While not precisely a withdrawal form, an Annuity Election Form allows for the selection of annuity options as a form of distribution from retirement plans, similar to the annuity option in the Transamerica form for plans allowing for such distributions.

Qualified Domestic Relations Order (QDRO) Distribution Form: This form is utilized for the division of retirement plan assets pursuant to a divorce or legal separation, similar to the Transamerica form's section for payment to an alternate payee under a QDRO.

Loan Repayment Form for Retirement Plans: Although primarily for loan repayments, these forms share similarities with the Transamerica 401K Withdrawal form's section on outstanding loan payoff instructions, providing options for handling loans in the context of a distribution request.

When it comes to managing your retirement savings, filling out a withdrawal form, such as the Transamerica 401K Withdrawal Form, is a critical step that requires careful attention to detail. It’s important to avoid common mistakes to ensure that your request is processed smoothly and efficiently. Here are several do’s and don’ts to consider:

Following these guidelines will help ensure your Transamerica 401K Withdrawal request is processed smoothly, allowing you to access your funds in a manner that best suits your financial goals and needs.

Understanding the Transamerica 401K Withdrawal form is crucial for anyone considering accessing their retirement savings early. However, there are several common misconceptions that can lead to confusion and potential financial consequences. Here are six key misunderstandings to be aware of:

It's imperative for participants to carefully read the instructions and fully understand their options and the implications of their choices, including potential tax liabilities and the effect on their retirement savings, before submitting a Transamerica 401K Withdrawal request.

Filling out and using the Transamerica 401K Withdrawal form requires careful attention to a variety of details to ensure the process is completed accurately and efficiently. Here are seven key takeaways to guide participants and employers through this process:

Understanding these key aspects can help streamline the withdrawal process, ensuring that distributions are made in accordance with plan provisions and federal regulations.

Pt Observation Hours - This form bridges your practical experience with your academic aspirations in physical therapy.

W-9 Form Filled Out Example - Often requested by financial institutions from individuals who are setting up interest-bearing accounts or investments.