Free Wv Tax Exempt PDF Template

Free Wv Tax Exempt PDF Template

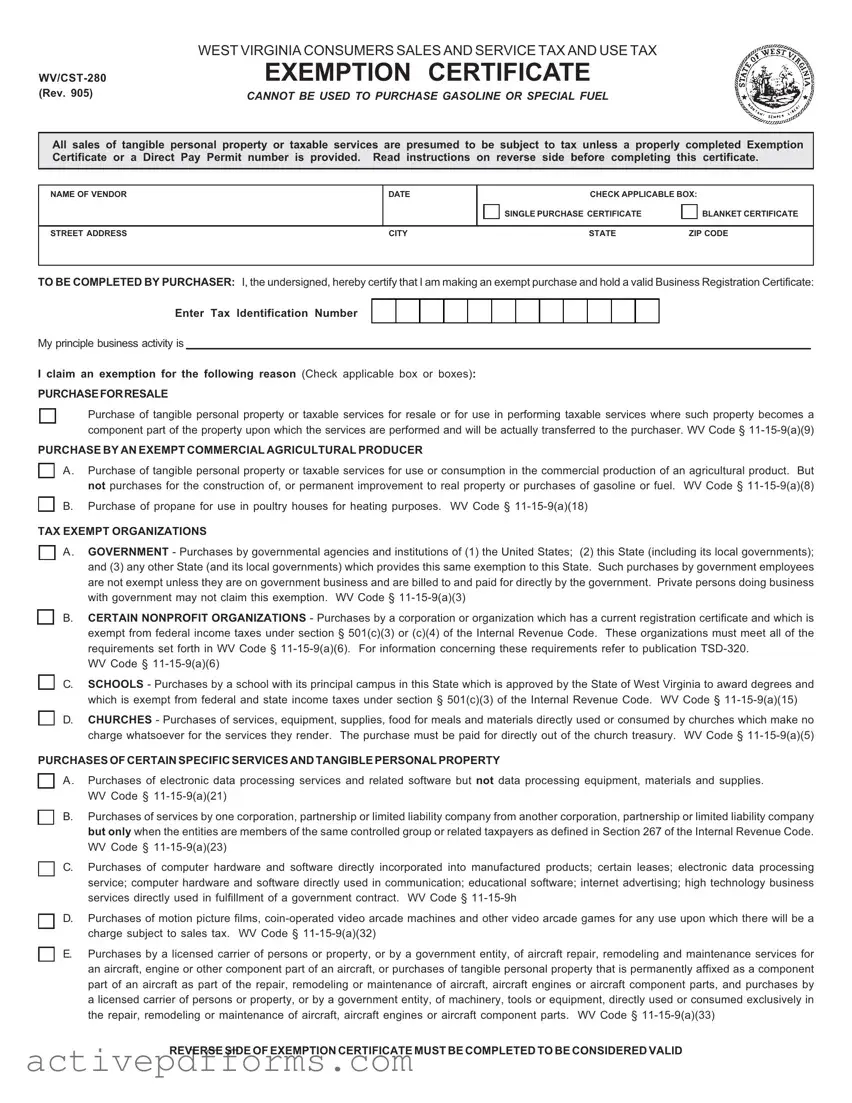

In the state of West Virginia, the process of managing sales and use tax for various transactions can be navigated using the West Virginia Consumers Sales and Service Tax and Use Tax Exemption Certificate (WV/CST-280, Rev. 905). This document is crucial for both vendors and purchasers, as it outlines the specific conditions under which sales of tangible personal property or taxable services can be exempt from sales tax. The certificate can be issued either as a single purchase certificate or as a blanket certificate, which covers multiple transactions. It is essential for purchasers to hold a valid Business Registration Certificate and to provide their Tax Identification Number when completing this form. The exemption can be claimed for a variety of reasons, including but not limited to, purchases for resale, purchases by exempt commercial agricultural producers, tax-exempt organizations, schools, churches, and specific services and tangible personal property acquisitions such as electronic data processing services and related software. Misuse of this certificate, whether intentionally erroneous or fraudulent, can result in substantial penalties, interest, and the potential suspension or revocation of the purchaser's Business Registration Certificate. Therefore, it's imperative for both purchasers and vendors to thoroughly understand and comply with the guidelines and instructions provided on the reverse side of the exemption certificate to ensure valid and lawful transactions.

|

WEST VIRGINIA CONSUMERS SALES AND SERVICE TAX AND USE TAX |

EXEMPTION CERTIFICATE |

|

(Rev. 905) |

CANNOT BE USED TO PURCHASE GASOLINE OR SPECIAL FUEL |

All sales of tangible personal property or taxable services are presumed to be subject to tax unless a properly completed Exemption Certificate or a Direct Pay Permit number is provided. Read instructions on reverse side before completing this certificate.

NAME OF VENDOR

DATE

CHECK APPLICABLE BOX:

SINGLE PURCHASE CERTIFICATE

BLANKET CERTIFICATE

STREET ADDRESS |

CITY |

STATE |

ZIP CODE |

TO BE COMPLETED BY PURCHASER: I, the undersigned, hereby certify that I am making an exempt purchase and hold a valid Business Registration Certificate:

Enter Tax Identification Number

My principle business activity is

I claim an exemption for the following reason (Check applicable box or boxes):

PURCHASEFORRESALE

Purchase of tangible personal property or taxable services for resale or for use in performing taxable services where such property becomes a component part of the property upon which the services are performed and will be actually transferred to the purchaser. WV Code §

PURCHASE BY AN EXEMPT COMMERCIAL AGRICULTURAL PRODUCER

A. Purchase of tangible personal property or taxable services for use or consumption in the commercial production of an agricultural product. But not purchases for the construction of, or permanent improvement to real property or purchases of gasoline or fuel. WV Code §

B. Purchase of propane for use in poultry houses for heating purposes. WV Code §

TAX EXEMPT ORGANIZATIONS

A. GOVERNMENT - Purchases by governmental agencies and institutions of (1) the United States; (2) this State (including its local governments); and (3) any other State (and its local governments) which provides this same exemption to this State. Such purchases by government employees are not exempt unless they are on government business and are billed to and paid for directly by the government. Private persons doing business with government may not claim this exemption. WV Code §

B. CERTAIN NONPROFIT ORGANIZATIONS - Purchases by a corporation or organization which has a current registration certificate and which is exempt from federal income taxes under section § 501(c)(3) or (c)(4) of the Internal Revenue Code. These organizations must meet all of the requirements set forth in WV Code §

WV Code §

C. SCHOOLS - Purchases by a school with its principal campus in this State which is approved by the State of West Virginia to award degrees and which is exempt from federal and state income taxes under section § 501(c)(3) of the Internal Revenue Code. WV Code §

D. CHURCHES - Purchases of services, equipment, supplies, food for meals and materials directly used or consumed by churches which make no charge whatsoever for the services they render. The purchase must be paid for directly out of the church treasury. WV Code §

PURCHASES OF CERTAIN SPECIFIC SERVICES AND TANGIBLE PERSONAL PROPERTY

A. Purchases of electronic data processing services and related software but not data processing equipment, materials and supplies. WV Code §

B. Purchases of services by one corporation, partnership or limited liability company from another corporation, partnership or limited liability company but only when the entities are members of the same controlled group or related taxpayers as defined in Section 267 of the Internal Revenue Code. WV Code §

C. Purchases of computer hardware and software directly incorporated into manufactured products; certain leases; electronic data processing service; computer hardware and software directly used in communication; educational software; internet advertising; high technology business services directly used in fulfillment of a government contract. WV Code §

D. Purchases of motion picture films,

E. Purchases by a licensed carrier of persons or property, or by a government entity, of aircraft repair, remodeling and maintenance services for an aircraft, engine or other component part of an aircraft, or purchases of tangible personal property that is permanently affixed as a component part of an aircraft as part of the repair, remodeling or maintenance of aircraft, aircraft engines or aircraft component parts, and purchases by a licensed carrier of persons or property, or by a government entity, of machinery, tools or equipment, directly used or consumed exclusively in the repair, remodeling or maintenance of aircraft, aircraft engines or aircraft component parts. WV Code §

REVERSE SIDE OF EXEMPTION CERTIFICATE MUST BE COMPLETED TO BE CONSIDERED VALID

I understand that this certificate may not be used to make tax free purchases of items or services which are not for an exempt purpose and that I will pay the Consumers Sales or Use Tax on tangible personal property or services purchased pursuant to this certificate and subsequently used or consumed in a taxable manner. In addition, I understand that I will be liable for the tax due, plus substantial penalties and interest, for any erroneous or false use of this certificate.

NAME OF PURCHASER |

STREET ADDRESS |

|

|

|

|

SIGNATURE OF OWNER, PARTNER, OFFICER OF CORPORATION, ETC. |

CITY |

|

|

|

|

TITLE |

STATE |

ZIP CODE |

|

|

|

GENERALINSTRUCTIONS

An Exemption Certificate may be used only to claim exemption from tax upon a purchase of tangible personal property or services which will be used for an exempt purpose as stated on the front of this form.

ApurchasermayfileablanketExemptionCertificatewiththevendortocoveradditionalpurchasesofthesamegeneraltypeofproperty or service. However, each subsequent sales slip or purchase invoice evidencing a transaction covered by a blanket Exemption Certificate must show the purchaser’s name, address and Business Registration Certificate Number for purposes of certification.

INSTRUCTIONSFORPURCHASER

To purchase tangible personal property or services tax exempt, you must possess a valid Business Registration Certificate and you must properly complete this Exemption Certificate and present it to your supplier. To be properly completed, all entries on this Exemption Certificate must be filled in.

Your Business Registration Certificate (and any duplicates) may be suspended or revoked if you or someone acting on your behalf willfully issues this certificate for the purpose of making a tax exempt purchase of tangible personal property and/or services that is not used in a tax exempt manner (as stated on the front of this form).

When property or services are purchased tax exempt with an Exemption Certificate, but later used or consumed in a non exempt manner, the purchaser must pay Sales or Use Tax on the purchase price.

The willful issuance of a false or fraudulent Exemption Certificate with the intent to evade Sales or Use Tax is a misdemeanor.

Your misuse of this Certificate with intent to evade the Sales or Use Tax shall also result in your being subject to:

A penalty of fifty percent of the tax that would have been due

had there not been a misuse of such certificate.

This is in addition to any other penalty imposed by the Law.

In the event you make false or fraudulent use of this Certificate with intent to evade the tax, you may be assessed for the tax at any time subsequent to such use.

INSTRUCTIONSFORVENDOR

At the time the property is sold or the service is rendered, you must obtain from your customer this Certificate, properly completed, (or a Direct Pay Permit number issued by the West Virginia Department of Tax and Revenue), or the sale will be deemed a taxable sale, unless the property or service sold is exempt per se from Sales Tax. Your failure to collect tax on such taxable sale will make you personally liable for the tax, plus penalties and interest.

Additionalinformationmayberequiredtosubstantiatethatthesalewasforexemptpurposes. InorderforthisCertificatetobeproperly completed, it must be issued by a purchaser who has a valid Business Registration Certificate and must have all entries completed by the purchaser.

A timely received certificate which contains a material deficiency will be considered satisfactory if such deficiency is subsequently corrected.

You must keep this certificate for at least three years after the due date of the last return to which it relates, or the date when such return was filed, if later.

You must maintain a reasonable method of associating a particular exempt sale to a customer with the Exemption Certificate you have on file for such customer.

INSTRUCTIONSFORVENDORANDPURCHASER

If you, as vendor or as a purchaser, engage in any business activity in West Virginia without possessing a valid Business Registration Certificate (and you do not clearly qualify for an exemption), you shall be subject to a penalty in an amount not exceeding $100 for the first day on which such sales or purchases are made, plus an amount not exceeding $100 for each subsequent day on which such sales or purchases are made.

Please begin using this Certificate immediately.

| Fact Number | Fact Detail |

|---|---|

| 1 | The form is titled "WEST VIRGINIA CONSUMERS SALES AND SERVICE TAX AND USE TAX WV/CST-280 EXEMPTION CERTIFICATE." |

| 2 | This exemption certificate specifically prohibits the tax-free purchase of gasoline or special fuel. |

| 3 | All sales of tangible personal property or taxable services in West Virginia are presumed to be subject to tax unless an exemption certificate or a direct pay permit number is provided. |

| 4 | The purchaser must hold a valid Business Registration Certificate to use the form. |

| 5 | There are multiple specific reasons for exemption listed, including but not limited to: purchases for resale, purchases by exempt commercial agricultural producers, tax-exempt organizations, schools, and churches. |

| 6 | The governing laws for the exemptions include West Virginia Code § 11-15-9 with various subsections relevant to each type of exemption. |

| 7 | There are provisions for both single purchase certificates and blanket certificates, which cover multiple purchases of the same general type of property or service. |

| 8 | The front of the form must be completed, including the purchaser's tax identification number and principle business activity. |

| 9 | Purchases using this certificate that are later used or consumed in a non-exempt manner require the purchaser to pay Sales or Use Tax on the purchase price. |

| 10 | Misuse of the exemption certificate with intent to evade Sales or Use Tax can result in a misdemeanor charge, substantial penalties, and interest. |

Filling out the West Virginia (WV) Tax Exempt Form, or WV/CST-280, is an essential step in conducting tax-exempt transactions in the state—for those who qualify. This document, critical for purchasers and vendors alike, ensures that sales of tangible personal property or taxable services, which are to be used for exempt purposes, are not taxed in accordance with West Virginia state laws. The distinction between types of certificates, either for a single purchase or as a blanket for multiple, plays a crucial role, as does the specificity of exemption reasons ranging from agricultural use to educational and religious purposes. Proper completion and appropriate use of this form not only facilitate compliance with tax laws but also prevent potential penalties related to misuse or fraudulent claims. Here’s a step-by-step guide to correctly fill out the form:

Once duly filled, this form serves as an assertion of the rights to conduct tax-exempt transactions under specified conditions. It’s crucial, therefore, to ensure every detail is correctly entered and the form is retained as part of transaction records. Mishandling or misrepresenting information on this form can lead to serious legal ramifications, including penalties, interest, or the revocation of the Business Registration Certificate itself. Responsible use of the WV Tax Exempt form is a testament to the trustworthiness and integrity of a business navigating the complexities of tax obligations.

What is the WV Tax Exempt Form?

The WV Tax Exempt Form, officially known as WV/CST-280, is a document utilized in West Virginia to claim exemption from consumers sales and service tax and use tax for eligible purchases. This includes tangible personal property or taxable services that are used for an exempt purpose, as outlined in the certificate. This form cannot be used to purchase gasoline or special fuel.

Who can use the WV Tax Exempt Form?

This form can be used by various entities, including those making purchases for resale, exempt commercial agricultural producers, tax-exempt organizations like certain nonprofits, schools, churches, and governmental agencies, as well as businesses purchasing specific services and tangible personal property for exempt purposes. It is essential that the purchaser holds a valid Business Registration Certificate to use this form.

How do I properly complete the WV Tax Exempt Form?

To properly complete the form, you must fill in all entries, including the name and address of the vendor, the tax identification number, the main business activity, and the specific reason for claiming the exemption. You must indicate whether it's a single or blanket certificate and sign the form, effectively certifying that the purchases are for tax-exempt purposes. Remember, the reverse side of the exemption certificate must also be completed for it to be valid.

What are the consequences of misusing the WV Tax Exempt Form?

Misusing the form to evade sales or use tax can lead to substantial penalties, interest, and potentially criminal charges. If you use this certificate for tax-exempt purchases of items or services not used for an exempt purpose, you are required to pay the appropriate taxes. The law imposes a penalty of fifty percent of the tax that would have been due, in addition to any other imposed penalties.

Can the WV Tax Exempt Form be used for all purchases?

No, the form cannot be used for every purchase. Specifically, it cannot be used to make tax-free purchases of gasoline or special fuel. Additionally, the exempt purchase must be directly related to the entity's exempt purpose as defined by West Virginia Code and the instructions provided on the form.

How long should I retain a completed WV Tax Exempt Form?

Vendors are required to retain completed exemption certificates for at least three years after the due date of the last return to which it relates, or the date when such return was filed, whichever is later. It's crucial for record-keeping and substantiating exempt sales should the need arise for verification by tax authorities.

What do I do if I’m unsure about my eligibility to use the WV Tax Exempt Form?

If you're uncertain about your eligibility, it's best to consult directly with the West Virginia Department of Tax and Revenue or a tax professional familiar with West Virginia tax laws. This will help ensure compliance and prevent potential penalties associated with misuse of the exemption certificate.

Not providing a valid Business Registration Certificate number. Every individual or entity seeking a tax exemption in West Virginia must possess a valid Business Registration Certificate. This certificate number must be accurately recorded on the WV/CST-280 form. Failing to do so may result in the form being deemed incomplete or invalid, thereby negating the intended tax exemption.

Incorrectly checking the applicable box for the type of exemption. The WV/CST-280 form outlines several types of tax-exempt purchases, including those for resale, use by exempt organizations, or specific types of services and tangible personal property. The purchaser must carefully review and select the precise reason for the exemption that applies to their purchase. Failing to correctly identify the applicable exemption type can result in the inability to claim the tax exemption properly.

Using the form for ineligible purchases, such as gasoline or special fuel. The instructions clearly state that the WV/CST-280 Exemption Certificate cannot be used to make tax-exempt purchases of gasoline or special fuel. Attempting to use the certificate for such purchases is a misuse of the form and could lead to penalties or the revocation of tax-exempt privileges.

Omitting essential details such as signature and title of the owner, partner, or officer of the corporation making the purchase. The form requires the signature and title of the person certifying the exemption claim on behalf of the purchaser. This omission can undermine the validity of the certificate, as it ensures accountability and verifies the intent to make a tax-exempt purchase.

When applying for tax exemptions with the WV/CST-280, individuals and businesses must meticulously review and complete the form to ensure compliance with West Virginia’s tax laws. Proper completion and use of this certificate allow for a smoother transaction process while avoiding unnecessary legal and financial complications.

When handling the West Virginia Consumers Sales and Service Tax and Use Tax Exemption Certificate (WV/CST-280), it is typically part of a broader documentation process that encompasses various financial and operational aspects of a business or organization. These documents are vital for compliance, financial reporting, and operational purposes. Here is a concise description of each document that is often used alongside the WV Tax Exempt form.

Understanding and managing these documents require careful attention to detail and an awareness of statutory deadlines and requirements. The purpose behind each form is to ensure that businesses and organizations not only comply with the relevant laws but also maintain a structured approach to their financial and operational undertakings. Having these documents in order solidifies an entity's standing and facilitates smoother transactions, both with vendors and governmental bodies.

State Sales Tax Exemption Certificate: Similar to the WV Tax Exempt form, this document is used across various states to certify that a purchase is being made for a reason that exempts it from sales tax. Both forms require the buyer to indicate the purpose of the exemption, whether it's for resale, use by a governmental or nonprofit entity, or another tax-exempt purpose under state law.

Resale Certificate: This certificate, much like the WV Tax Exempt form when used for purchasing items for resale, allows businesses to buy goods without paying sales tax if the items are to be resold in their business operation. Both certificates necessitate the disclosure of the purchaser’s intent at the time of purchase to avoid the imposition of sales tax.

Agricultural Exemption Certificate: Specifically designed for the agricultural sector, this certificate closely resembles the WV Tax Exempt form section that pertains to purchases by an exempt commercial agricultural producer. Items necessary for the production of agricultural goods can be bought without sales tax, paralleling the exemptions provided for certain agricultural purchases in West Virginia.

Direct Pay Permit: Entities holding a Direct Pay Permit agree to directly remit taxes due to the state rather than having vendors collect tax at the point of sale. While the Direct Pay Permit itself is different, it's mentioned in the WV Tax Exempt form as an alternative means of handling tax exemptions on purchases, underlining the coordination between different types of tax-handling documentation.

Nonprofit Exemption Certificate: Nonprofit organizations often qualify for sales tax exemptions on purchases related to their charitable or educational missions. This certificate shares similarities with the segments of the WV Tax Exempt form reserved for tax-exempt organizations, schools, and churches, allowing these entities to certify their tax-exempt status for purchases.

Government Purchase Order: This document authorizes purchases made by government entities and, akin to the government section in the WV Tax Exempt form, signifies that the purchase is exempt from sales tax. Both require that the purchase be made directly by the governmental entity and directly billed to and paid for by the same to qualify for the exemption.

Use Tax Exemption Certificate: While the primary focus of the WV Tax Exempt form is on sales tax, use tax exemptions are also relevant. The Use Tax Exemption Certificate allows for the certification of tax-exempt purchases that, although not directly exempt from sales tax at the point of purchase, should not incur use tax subsequently. This parallels the preemptive exemption claim process facilitated by the WV form for qualifying purchases.

Charitable Organization Exemption Certificate: Charitable organizations often have a tax-exempt status that exempts them from paying sales tax on purchases. This certification is akin to parts of the WV Tax Exempt form that exempt purchases made by churches and certain nonprofits, illustrating how specific types of entities can purchase goods and services tax-free for their operation.

When dealing with a West Virginia Consumers Sales and Service Tax and Use Tax Exemption Certificate (WV/CST-280), understanding the do's and don'ts is crucial for ensuring compliance and utilizing the benefits correctly. Below are key points to consider when completing this form.

By following these guidelines, businesses can effectively navigate the process of claiming tax exemptions on eligible purchases in West Virginia, ensuring compliance and avoiding penalties.

When it comes to navigating the complexities of tax exemptions in West Virginia, several misconceptions often arise, especially regarding the WV Tax Exempt Form (WV/CST-280). Here's a list of common misunderstandings and the truths behind them:

Understanding the facts about the WV Tax Exempt Form ensures that both purchasers and vendors can navigate the exemptions properly, avoiding misconceptions that lead to improper use and potential penalties.

Understanding the West Virginia Tax Exempt Form (WV/CST-280) properly ensures that eligible purchases made by businesses, nonprofit organizations, and government agencies can be exempt from sales tax. Here are nine key takeaways for effectively filling out and using this form.

By adhering to these guidelines, eligible entities can correctly claim tax exemptions for qualifying purchases, thereby ensuring compliance with West Virginia tax laws while managing their tax liabilities effectively.

Allodial Title Pdf - After Joe Stevens' passing, Augustus Blackstone took on the task of editing and publishing the Allodial Title material, honoring Stevens' dedication to property rights.

Aspen Dental Health Information Release - A structured request to Aspen Dental allowing the disclosure of your dental health information to an external party.

Us Sales Tax Exemption - Organizations not solely operated for exempt purposes as defined by Section 501(c)(3) will not qualify under this application.